Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

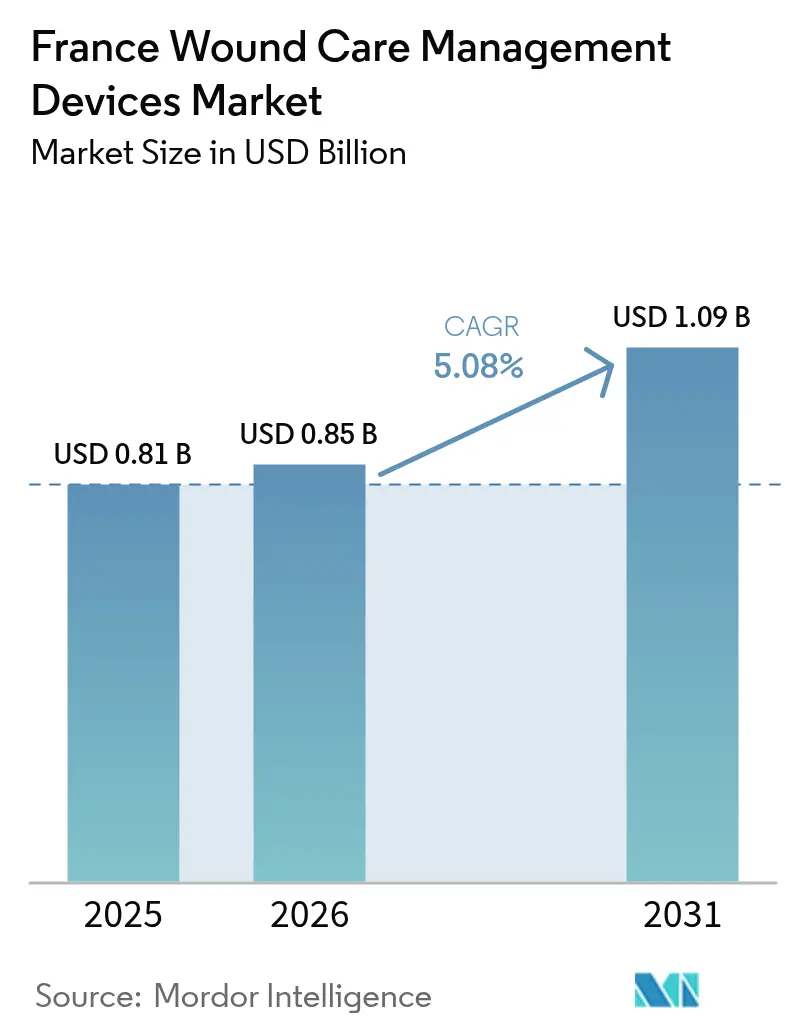

| Base Year Market Size (2025) | USD 0.81 Billion |

| Market Size (2026) | USD 0.85 Billion |

| Market Size (2031) | USD 1.09 Billion |

| Growth Rate (2026 - 2031) | 5.08% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. |

|

France Wound Care Management Devices Market Analysis by ���ϲ�����

The France Wound Care Management Devices Market size is expected to grow from USD 0.81 billion in 2025 to USD 0.85 billion in 2026 and is forecast to reach USD 1.09 billion by 2031 at 5.08% CAGR over 2026-2031.

Population aging, a diabetes burden approaching 4 million people, and policy support for ambulatory and home-based care are widening the addressable base for the France wound care management devices market. Hospitals have consolidated demand for advanced dressings and negative-pressure systems, while tissue adhesives and absorbable sutures are scaling with the expansion of day-case surgery. Reimbursement incentives under the 2024 Social Security Financing Act are accelerating the shift of chronic-wound services to Hospitalisation à Domicile (HAD), raising the strategic value of single-use NPWT kits that community nurses can deploy between professional visits.[1]Luc Teot, "Negative Pressure Wound Therapy An update for clinicians and outpatient care givers," Journal of Wound Management, journals.cambridgemedia.com.au Simultaneously, AGEC eco-design rules and digital-health pathways reward manufacturers that couple low-waste materials with tele-expertise functionality.

Key Report Takeaways

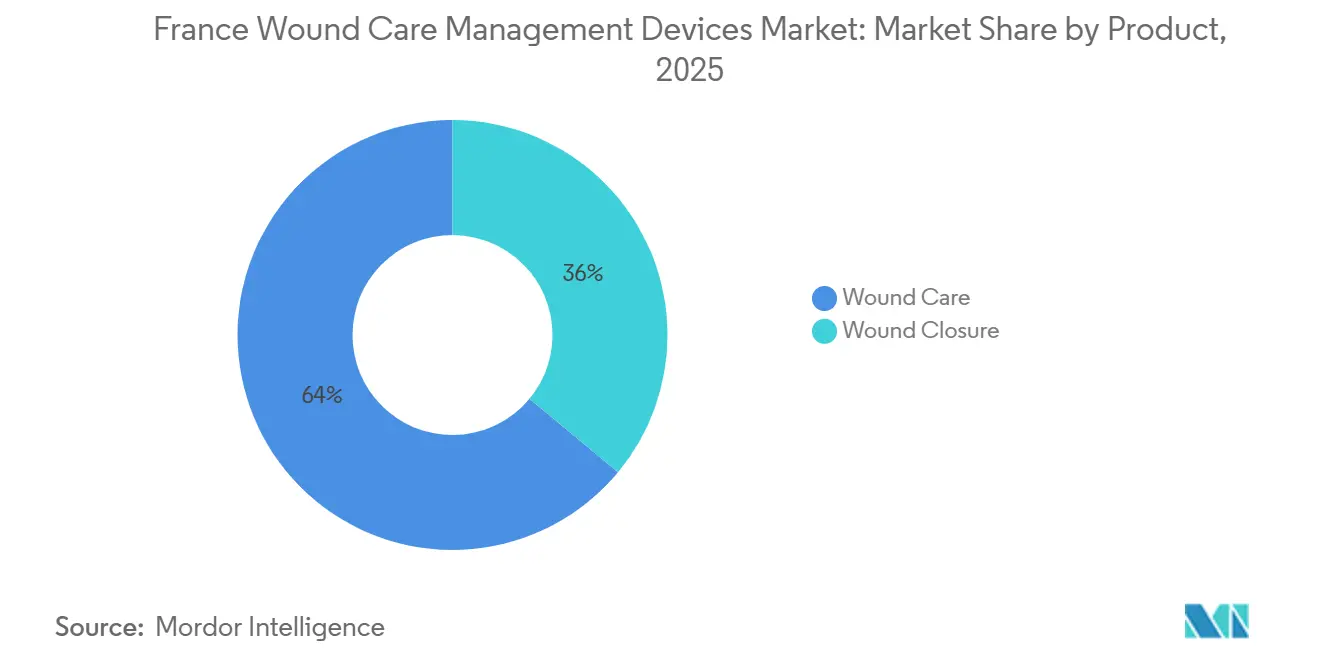

- By product, advanced dressings and NPWT systems together accounted for 63.98% of the France wound care management devices market share in 2025. In contrast, closure solutions are projected to log the fastest CAGR of 5.74% through 2031.

- By wound type, chronic wounds accounted for 58.83% of the France wound care management devices market in 2025, while acute wounds are anticipated to expand at a 5.67% CAGR over the same horizon.

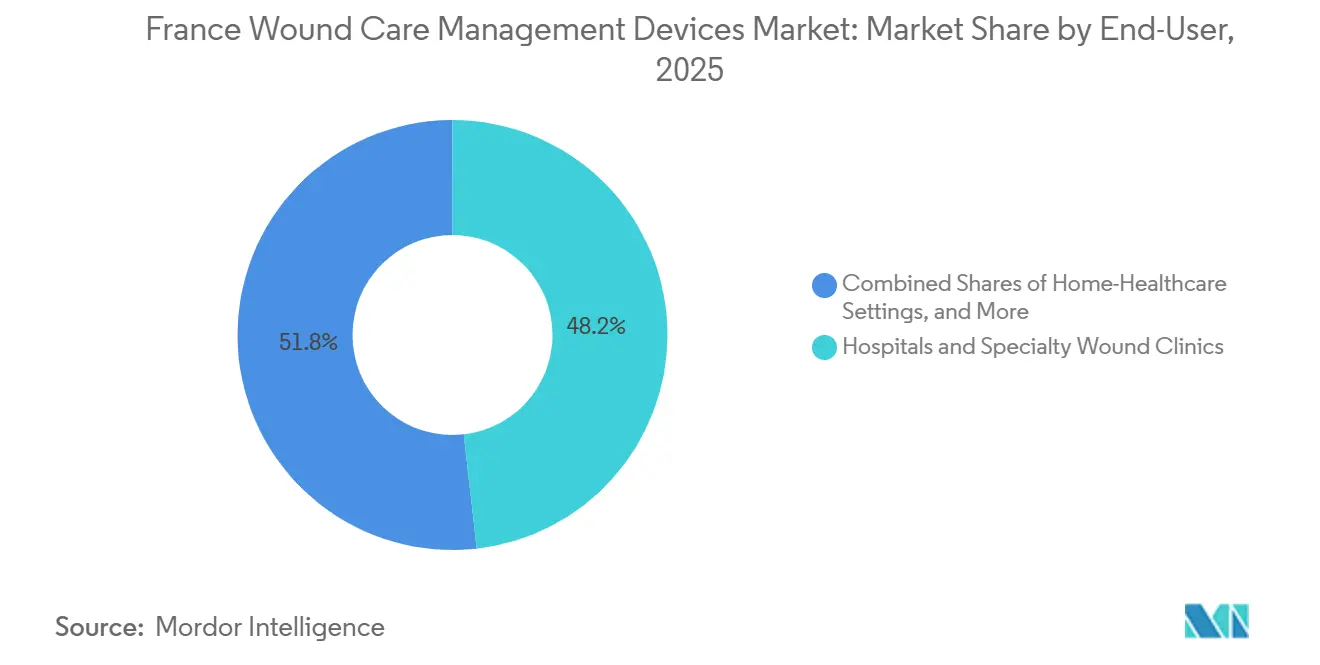

- By end user, hospitals and specialty clinics captured 48.21% of revenue in 2025; home healthcare settings represent the fastest-growing channel, with a 5.63% CAGR forecast to 2031.

- By mode of purchase, institutional procurement comprised 65.72% of 2025 sales, yet the retail/OTC channel is set to post a 5.96% CAGR, outpacing every other segment.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

France Wound Care Management Devices Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising incidence of chronic wounds & diabetic ulcers | +1.4% | National, higher in Nouvelle-Aquitaine, Bretagne, Pays de la Loire | Long term (≥ 4 years) |

| Ageing population enlarging at-risk cohort | +1.3% | National, stronger in rural and peri-urban areas | Long term (≥ 4 years) |

| Growth in day-case surgical procedures | +0.9% | National, early uptake in CHU hospitals and private clinics | Medium term (2-4 years) |

| Had-reimbursed single-use NPWT expansion | +0.7% | National, linked to HAD networks | Medium term (2-4 years) |

| AI-enabled tele-wound-care platforms | +0.5% | Pilot sites in Île-de-France and Auvergne-Rhône-Alpes | Short term (≤ 2 years) |

| Tele-wound-care platforms endorsed by ARS | +0.4% | Underserved regions | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Rising Incidence of Chronic Wounds & Diabetic Ulcers

Roughly 3.5 million French adults lived with diabetes in 2024, and the International Diabetes Federation projects the pool will reach 4.1 million by 2050.[2]International Diabetes Federation, “IDF Diabetes Atlas,” idf.org Diabetic foot ulcers already drive a large share of lower-limb amputations that strain Assurance Maladie budgets. Less than half of high-risk patients receive structured podiatric screening, keeping the recurrence rate stubbornly high. Advanced foam, hydrocolloid, and antimicrobial dressings can shorten healing times and reduce infection risk, resulting in measurable savings per wound episode. Manufacturers presenting valid cost-per-healed-wound dossiers are more likely to secure favorable ASA grades under CNEDiMTS review.

Ageing Population Enlarging At-Risk Cohort

Citizens aged 65 and above accounted for 22.15% of France’s population in 2024 and will likely climb to 26% by 2050. Seniors already consume 84% of nursing care, reflecting multimorbidity and skin fragility.[3]Institut National de la Statistique et des Études Économiques, “French Population Demographics,” insee.fr Single-use NPWT, portable oxygen units, and retail wound-care kits that caregivers can handle between nurse visits fit this demographic reality. Product design, therefore, prioritizes intuitive application, lightweight canisters, and instruction leaflets for non-specialists. Compliance with AGEC eco-design mandates, compulsory from 2024, further distinguishes offerings in hospital tenders.

Growth in Day-Case Surgical Procedures

National policies that cap inpatient bed days have pushed the ambulatory surgery rate toward 70%. Incisions from orthopedic, vascular, and bariatric procedures require prophylactic measures to avert surgical-site infections, which occur in 2-5% of cases. Incisional NPWT shows clear benefit in high-risk cohorts but less evidence in routine ankle arthroplasty, underscoring the need for indication-specific trials. Tissue adhesives and absorbable sutures that cut follow-up visits are gaining traction as hospitals chase same-day discharge targets.

HAD-Reimbursed Single-Use NPWT Expansion

HAD networks received additional funding under the 2024 Social Security Financing Act, enabling complex wound protocols to be implemented in homes. Single-use NPWT devices that run for 7-12 days without canister changes match nurse-scarcity realities and align with reimbursement bundles. Demonstrating community-setting cost-effectiveness, lower readmissions, and fewer in-person visits is now pivotal for LPPR listing. Manufacturers are training pharmacists to support device initiation, building on newly expanded pharmacy scopes of practice.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High cost of advanced wound care products | −0.6% | National, magnified in rural territories | Medium term (2-4 years) |

| Stringent reimbursement ceilings | −0.5% | National | Long term (≥ 4 years) |

| Shortage of specialized wound-care nurses | −0.4% | Rural France | Medium term (2-4 years) |

| Eco-design & single-use-plastic compliance costs | −0.3% | National | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

High Cost of Advanced Wound Care Products

Public hospitals posted a EUR 2.4 billion deficit in 2023, prompting procurement managers to scrutinise premium products despite their clinical merit. AI-enabled dressings and bioelectrical wraps carry price tags that strain budgets, especially in rural units where 27% of intensive-care beds already face intermittent closure due to staff gaps. Vendor strategies, therefore, pivot to value-based contracts and low-silver or magnesium-hydroxide antimicrobial substitutes that protect margins while easing upfront cost barriers.

Stringent Reimbursement Ceilings

The 2025 Social Security Financing Law foresees tighter Z Contribution caps for medical devices, mirroring a 25% cut recently applied to orthopaedic implants. Since 2013, tariff reductions have trimmed the prices of total hip prostheses by 17%, a precedent that signals similar pressure on wound dressings. Manufacturers now layer real-world evidence files into pricing briefs to justify premium positioning and protect volume in the France wound care management devices market. CNEDiMTS requires both clinical benefit (SA) and added value (ASA) proof before LPPR listing. Trials must therefore measure acceleration in heal rate, SSI reduction, or nurse-time savings to secure premium pricing. The EU Medical Device Regulation transition in 2024 layered new documentation costs onto the submission process. Vendors with early HAS engagement and modular trial designs tend to clear hurdles faster.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Closure Innovations Accelerate Amid Dressing Dominance

Advanced dressings and NPWT captured 63.98% of the France wound care management devices market share in 2025, cementing their role in chronic-wound protocols. Closure technologies, however, are poised for a 5.74% CAGR through 2031, the swiftest growth rate in the France wound care management devices market. Hospitals favor absorbable sutures and tissue adhesives to reduce follow-up appointments, easing nurse workloads and advancing same-day discharge goals. Stapler lines optimized for minimally invasive procedures propel volume in orthopedics and bariatrics. Eco-compliant packaging required under the AGEC law distinguishes suppliers in tender evaluations.

Closure products benefit from day-case surgical momentum: with ambulatory surgeries nearing 70%, speed and infection control at incision sites are paramount. The France wound care management devices market for closure solutions should expand as insurers support prophylactic iNPWT for high-risk cohorts. Yet many new dressing variants still receive ASA V ratings, capping price ceilings. Firms that invest in indication-specific RCTs for closure devices and integrate tele-monitoring sensors into staplers may qualify for higher reimbursement tiers.

By Wound Type: Acute Wounds Gain Momentum as Chronic Dominates

Chronic wounds accounted for 58.83% of the France wound care management devices market size in 2025, led by diabetic foot ulcers, pressure ulcers, and venous leg ulcers. Treatment cycles can last months, with recurrence rates topping 40% within five years, anchoring steady demand for foam dressings and portable NPWT. Acute wounds, however, are forecast to grow 5.67% annually, fueled by rising traumatic injuries and surgical volumes. Surgical incisions treated prophylactically with iNPWT have shown reductions in infection rates in obese and vascular cohorts, though benefits vary by indication.

Retail pharmacies dispense adhesive strips, antiseptic sprays, and tissue adhesives for lacerations and minor burns, expanding the acute-wound revenue base. The France wound care management devices market share for acute indications will likely edge up as emergency departments funnel minor trauma care into community settings to free inpatient capacity. Manufacturers with burn-care portfolios tailored to specialist centers and over-the-counter kits for minor cuts can capture both ends of the spectrum.

By End-User: Home Settings Surge as Hospitals Consolidate

Hospitals and specialty clinics accounted for 48.21% of demand in 2025, leveraging group purchasing and evidence-based requirements to guide device selection. Yet home healthcare settings are projected to log a 5.63% CAGR through 2031, reflecting HAD expansion and telecare reimbursements. The France wound care management devices market size for home use will enlarge as single-use NPWT kits and pre-packaged dressing boxes reduce the need for daily nurse visits.

Long-term care facilities experience staff turnover exceeding 13% annually, limiting dressing change frequency and increasing demand for products that prolong wear time. Liberal nurses, expected to reach 173,000 by 2050, will become pivotal prescribers and trainers for home devices. Vendors offering app-based guidance for caregivers and real-time wound imaging stand to differentiate in this segment.

By Mode of Purchase: OTC Channel Outpaces Institutional Growth

Institutional procurement accounted for 65.72% of turnover in 2025, but retail and OTC sales will grow 5.96% annually to 2031, at the quickest pace across all segmentations. Pharmacy roles expanded under the 2024 LFSS to include point-of-care testing and limited antibiotic dispensing, positioning pharmacists as first-line advisors on minor wounds. Consumers gravitate toward eco-certified bandages and recyclable packaging, reflecting awareness of AGEC laws.

Hospitals will continue to command volume discounts, but retail chains can negotiate shelf placements for premium price points. The France wound care management devices market sees OTC brands bundling antiseptic wipes, silicone dressings, and digital QR-code tutorials to improve self-management outcomes. Manufacturers that train pharmacists and deploy sustainability labelling can win share without deep discounting.

Geography Analysis

Regional disparities mold consumption patterns within the French wound care management devices market. Île-de-France and Auvergne-Rhône-Alpes host university hospitals and pilot telemedicine hubs, giving them outsized demand for advanced dressings and AI-enabled imaging. Early evidence from these regions often guides national reimbursement reviews, thereby fast-tracking the diffusion of innovation. Conversely, the “diagonale du vide,” stretching from the Ardennes to the Pyrénées, struggles with doctor shortages and nurse-to-patient ratios below national averages. Here, wound-care demand centers on single-use devices that travel well in nurse cars and on tele-expertise platforms that link remote caregivers to urban specialists.

Nouvelle-Aquitaine, Bretagne, and Pays de la Loire feature the highest shares, amplifying chronic-wound prevalence. The France wound care management devices market in these coastal regions outpaces national averages for advanced dressings and portable NPWT units. Overseas territories add complexity: Mayotte’s physician density fell to seven doctors per 100,000 residents, while diabetes prevalence runs higher among Afro-Caribbean populations. Logistics chains depend on maritime or air links, boosting demand for long-shelf-life wound-care kits and remote-monitoring software that cuts specialist trips.

Manufacturers tailoring distribution to regional health-agency priorities, such as ARS grants for tele-expertise in Guyane or co-creating nurse-training modules with regional colleges, can unlock underserved pockets. Aligning packaging with AGEC eco-scores helps win public hospital tenders in green-leaning regions like Occitanie.

Competitive Landscape

France's wound care management devices market is moderately fragmented, but several multinationals hold entrenched positions. Solventum, Smith & Nephew, Mölnlycke, and Urgo Medical rely on extensive clinical evidence archives, dedicated reimbursement teams, and nurse education programs to defend their formulary status. Urgo leverages its French heritage and local plants to respond rapidly to tender specifications, although ASA V ratings on incremental dressings pressure margins.

Growth white space lies in eco-compliant disposables and tele-wound-care ecosystems. PolyNovo gained EU MDR clearance for its NovoSorb BTM dermal scaffold in 2024 and has since expanded distribution to French burn units, tapping reconstructive surgeons seeking autograft alternatives. Mölnlycke’s investment in Siren underscores a pivot toward predictive analytics that integrate temperature-sensing textiles with cloud dashboards. Large suppliers are also re-engineering packaging to meet single-use plastic bans, introducing sugar-cane polymers or fully recyclable cartons to secure AGEC compliance points in tender scoring.

Solventum pilots a nurse-to-specialist chat feature linking V.A.C. therapy users to wound centers, positioning the device not just as hardware but as a service layer. Competitive intensity, therefore, hinges on ecosystem play rather than standalone devices.

France Wound Care Management Devices Industry Leaders

-

ConvaTec Group PLC

-

Medtronic PLC

-

Smith & Nephew plc

-

Solventum Corporation

-

Coloplast A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Smith & Nephew began a national roll-out of its AI-enabled PICO 7Y NPWT platform after completing a six-month tele-expertise pilot in Île-de-France.

- November 2025: BD launched the CE-marked Surgiphor Surgical Wound Irrigation System across France, targeting orthopedic and colorectal procedures.

- July 2025: Urgo Medical introduced a sugar-cane-based blister pack for its UrgoTul Ag dressing line, meeting AGEC recyclability thresholds.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the France wound-care management devices market as the yearly revenue generated inside the country from all single-use and reusable devices or consumables that actively manage, monitor, or close acute and chronic wounds, including dressings, negative-pressure systems, closure tools, and adjunct topical applicators, sold by OEMs and authorized distributors.

Pure OTC antiseptics, general purpose cotton or gauze, and aesthetic scar-reduction cosmetics are outside our scope.

Segmentation Overview

-

By Product

-

Wound Care

-

Dressings

- Traditional Gauze & Tape Dressings

- Advanced Dressings

-

Wound-Care Devices

- Negative Pressure Wound Therapy (NPWT)

- Oxygen & Hyperbaric Systems

- Electrical Stimulation Devices

- Other Wound Care Devices

- Topical Agents

- Other Wound Care Products

-

Dressings

-

Wound Closure

- Sutures

- Surgical Staplers

- Tissue Adhesives, Strips, Sealants & Glues

-

Wound Care

-

By Wound Type

-

Chronic Wounds

- Diabetic Foot Ulcer

- Pressure Ulcer

- Venous Leg Ulcer

- Other Chronic Wounds

-

Acute Wounds

- Surgical / Traumatic Wounds

- Burns

- Other Acute Wounds

-

Chronic Wounds

-

By End-User

- Hospitals & Specialty Wound Clinics

- Long-term Care Facilities

- Home-Healthcare Settings

-

By Mode of Purchase

- Institutional Procurement

- Retail / OTC Channel

Detailed Research Methodology and Data Validation

Primary Research

We interviewed French wound nurses, hospital procurement leads, and community pharmacists across Ile-de-France, Occitanie, and Grand Est regions. Conversations validated real-world device usage days, average selling prices, and the growing share of home-based NPWT, bridging gaps left by desk work and guiding assumption ranges.

Desk Research

Mordor analysts begin by screening high-quality, open datasets such as Eurostat hospital discharge files, the French Social Security reimbursement tariff list (LPP), INSEE demographic projections, and OECD Health Accounts. Device import codes from the French customs portal help us size cross-border flows, while peer-reviewed journals like Journal des Plaies et Cicatrisation clarify adoption curves of advanced dressings. Company 10-Ks, investor decks, and regulatory filings enrich pricing and mix trends. Select paid assets, including D&B Hoovers for supplier revenues, Dow Jones Factiva for tender wins, and WSTS for electronics-grade sensor inputs, round out hard numbers. This list is illustrative; many other public and subscription sources fed our evidence base.

Market-Sizing & Forecasting

A country-level top-down build starts with 2024 procedure counts and chronic-wound prevalence, then applies device penetration and replacement rates derived from primary calls. These outputs are cross-checked with selective bottom-up indicators, sampled supplier revenues and channel checks, to fine-tune totals.

Diabetes prevalence and associated diabetic-foot ulcer incidence

Annual surgical procedures (public plus private hospitals)

Share of wounds managed with NPWT systems

Average dressing ASP movements under LPP revisions

Import-export balance for advanced dressings

Forecasts to 2030 use multivariate regression blended with scenario analysis, where diabetes growth, elderly population shifts, and reimbursement reforms act as predictors; expert consensus provides guardrails.

Data gaps in sub-segments are interpolated from nearest observable cohorts and flagged for review.

Data Validation & Update Cycle

Every draft model passes variance and plausibility checks versus external health-economy series, after which a senior reviewer signs off. We refresh figures each year and trigger interim updates when reimbursement codes, major acquisitions, or safety alerts materially alter demand.

Why Mordor's France Wound Care Management Devices Baseline Stays Dependable

Published estimates often differ; definitions, base years, and unchecked assumptions create spread.

The table highlights how such factors shift numbers.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.81 B (2025) | ���ϲ����� | - |

| USD 0.70 B (2023) | Regional Consultancy A | Focuses mainly on advanced dressings; older base year; excludes closure tools and NPWT adoption uptick |

| USD 1.20 B (2024) | Global Consultancy B | Bundles consumables and therapy services, applies straight-line growth, limited French primary validation |

| USD 0.41 B (2025) | Trade Journal C | Narrows scope to hospital-only spend and omits OTC/home-care channels |

Differences stem primarily from scope width, refresh cadence, and depth of French stakeholder input.

By aligning device categories with LPP codes, mixing desk and field evidence, and re-checking anomalies yearly, Mordor delivers a balanced, transparent baseline that decision-makers can replicate and trust.

Key Questions Answered in the Report

How fast is spending on France wound care management devices expanding?

Expenditure is increasing at a 5.08% CAGR between 2026 and 2031, rising from USD 0.85 billion to USD 1.09 billion.

Which product category will grow quickest through 2031?

Closure solutions sutures, staplers, and tissue adhesives are forecast to post the fastest 5.74% CAGR as day-case surgeries multiply.

Why are retail pharmacies gaining relevance in wound management?

Expanded scopes under the 2024 Social Security Financing Act allow pharmacists to advise on minor wounds, lifting retail/OTC channel sales at a 5.96% CAGR.

Where are tele-wound-care pilots most active?

Île-de-France and Auvergne-Rhône-Alpes host early pilots that test AI imaging and remote expert review before nationwide roll-out.

What sustainability pressures face device makers?

The AGEC law restricts single-use plastics and imposes eco-design scores, prompting firms to adopt bio-based materials and recyclable packaging.

How severe is the nursing shortfall in wound care by 2050?

Projections show an 80,000-nurse deficit even after a 37% workforce expansion, heightening demand for user-friendly devices that cut visit frequency.

Page last updated on: