Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

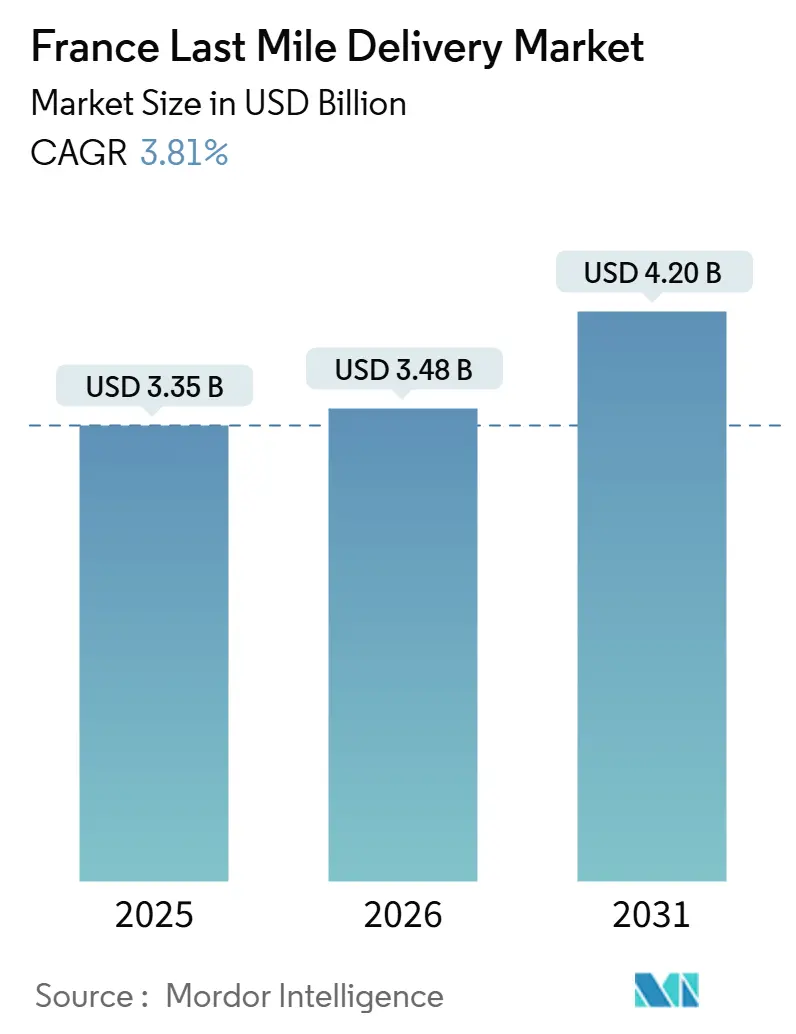

| Base Year Market Size (2025) | USD 3.35 Billion |

| Market Size (2026) | USD 3.48 Billion |

| Market Size (2031) | USD 4.20 Billion |

| Growth Rate (2026 - 2031) | 3.81% CAGR |

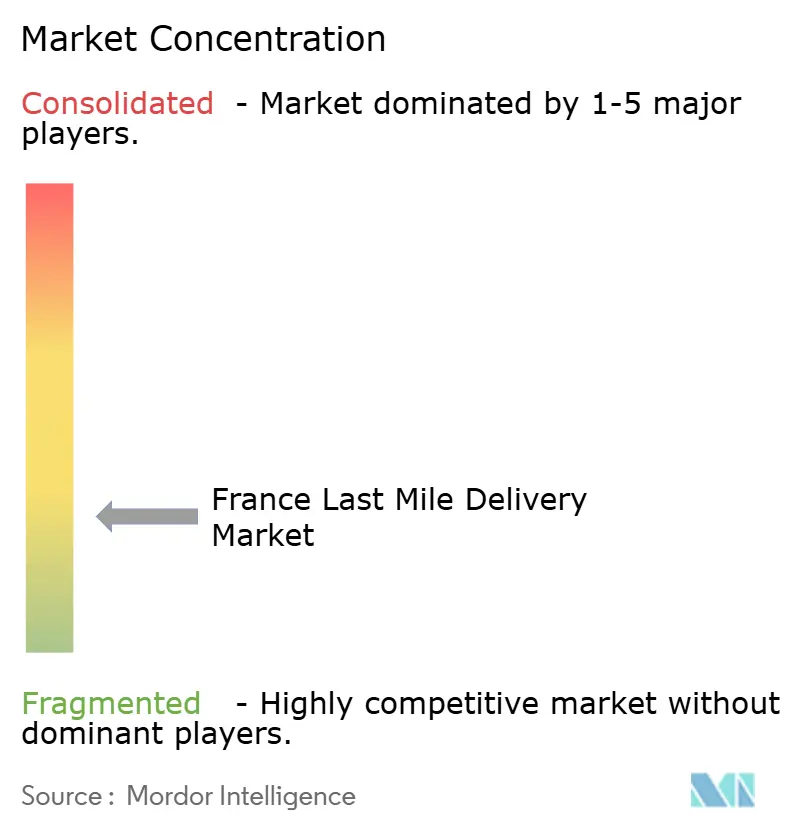

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

France Last Mile Delivery Market Analysis by ���ϲ�����

The France last-mile delivery market size is expected to increase from USD 3.35 billion in 2025 to USD 3.48 billion in 2026, and reach USD 4.20 billion by 2031, growing at a CAGR of 3.81% over 2026-2031.

A sustained shift toward e-commerce, the densification of France’s 5G network, and retailer commitments to ship-from-store fulfillment are sharpening competition while nudging operators toward technology-intensive, low-emission fleet strategies. Instant-commerce platforms surviving the 2024 consolidation now plug directly into supermarket store estates, turning in-city shops into micro-hubs that compress delivery windows to less than 30 minutes. At the same time, nationwide regulation on ESG disclosure and impending gig-worker reclassification raise compliance costs, a burden that falls heaviest on small couriers. Hydrogen truck pilots on the Paris-Lyon-Marseille corridor, together with falling battery prices, signal a progressive greening of heavy and light fleets, but cost parity is still several years away.

Key Report Takeaways

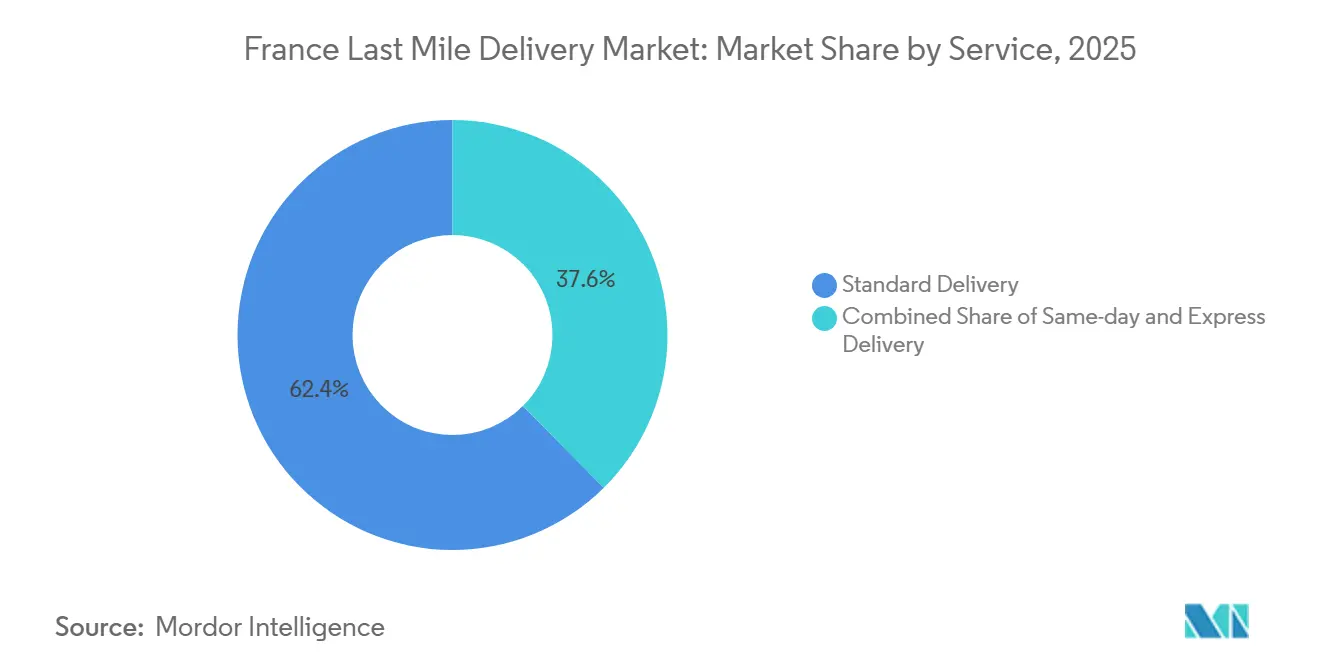

- By service, standard delivery led with 62.43% of France last mile delivery market share in 2025, where same-day delivery is forecast to expand at a 4.1% CAGR through 2031.

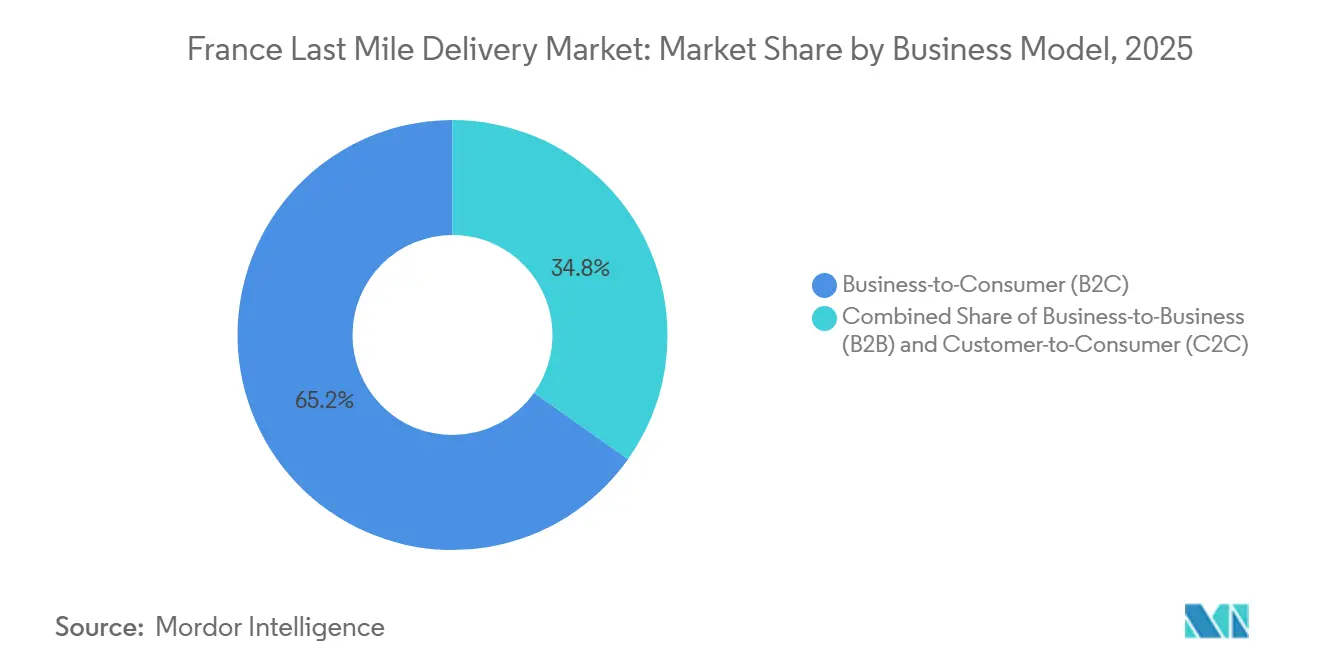

- By business model, the B2C segment held 65.2% share of the France last mile delivery market size in 2025, while C2C recorded the highest projected CAGR at 3.9% through 2031.

- By end-user, e-commerce retail captured 61.3% of France last mile delivery market size in 2025, and healthcare is advancing at a 4.3% CAGR to 2031.

- By region, Île-de-France captured 23.2% of France last mile delivery market size in 2025, and the region is advancing at a 4.4% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

France Last Mile Delivery Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid expansion of quick-commerce grocery platforms (≤ 20-minute delivery promises) | +0.9% | Urban centers, concentrated in Paris, Lyon, Marseille metropolitan areas | Short term (≤ 2 years) |

| Nationwide 5G rollout enabling AI-driven dynamic route optimisation | +0.7% | National, priority deployment in urban areas, expanding to secondary cities | Medium term (2-4 years) |

| Retailers scaling ship-from-store omnichannel fulfilment models | +0.6% | National, led by major retail chains in Ile-de-France, Auvergne-Rhone-Alpes | Medium term (2-4 years) |

| Surge in reverse-logistics volumes from circular-economy initiatives and product returns | +0.5% | National, higher concentration in urban areas with established collection infrastructure | Long term (≥ 4 years) |

| E-commerce returns-transparency law boosting forward and reverse parcel tracking demand | +0.4% | National, regulatory compliance requirement across all regions | Medium term (2-4 years) |

| Deployment of hydrogen-powered heavy-duty fleets spurring green-corridor logistics investments | +0.3% | Pilot corridors, initial deployment along Paris-Lyon-Marseille axis | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Rapid Expansion of Quick-Commerce Grocery Platforms

Quick-commerce networks that guarantee grocery arrival in under 20 minutes have reshaped urban logistics economics. After the 2024 shake-out, supermarket chains embedded rapid-delivery modules into existing stores, cutting fixed costs linked to dark-store leases. Carrefour’s Sprint service now operates from more than 1,000 shops, achieving break-even inside eight months thanks to higher order density and lower rider dead-time. Intermarche’s roll-out with Stuart across 1,320 outlets shows that in-store picking paired with algorithmic dispatch can keep unit economics positive at basket sizes below EUR 25. With venture-funded stand-alone players retreating, retailers’ hybrid model is likely to dominate, integrating premium immediacy into a broader France last mile delivery market portfolio[1]“5G Deployment in France 2025,” Autorité de Régulation des Communications Électroniques et des Postes, arcep.fr .

Nationwide 5G Rollout Enabling AI-Driven Dynamic Route Optimisation

ARCEP counted 34,000 active 5G sites by January 2025, a backbone that allows sub-minute data exchange between vehicles and cloud-based algorithms. Nomadia’s software trials in 2024 cut average delivery time 14% and fuel burn 16% across mixed diesel-electric fleets, proving that low-latency connectivity directly improves profitability. As 5G reaches secondary cities in 2026, predictive routing is expected to narrow the cost gap between high- and low-density areas, a pivotal advantage for stakeholders across the France last mile delivery market[2]“National Hydrogen Strategy 2025 Update,” Ministry of Ecological Transition, ecologie.gouv.fr .

Retailers Scaling Ship-From-Store Omnichannel Fulfilment Models

Carrefour, Auchan, and Casino have re-wired more than 1,300 stores into omnichannel hubs able to dispatch parcels within three hours to 70% of France’s population. By leveraging existing real estate and staff, retailers sidestep the capex of dedicated e-commerce warehouses. Inventory visibility platforms balance shelf and online demand, boosting in-store stock rotation while supporting the France last mile delivery industry’s need for low slack. Enhanced reverse-logistics capability, customers dropping returns at the same shop creates circular efficiencies that ripple through the wider network.

Surge in Reverse-Logistics Volumes from Circular-Economy Initiatives

Return rates that hit 22% in 2024 have not abated, propelled by the fashion and electronics segments. The Anti-Waste for a Circular Economy (AGEC) law bans the destruction of unsold goods, forcing retailers to process reverse flows. Vinted’s 1,500 pick-up points and Mondial Relay’s locker expansion signal a market pivot toward dedicated infrastructure that can grade, refurbish, and re-list items quickly. These bidirectional flows create additional revenue pools for carriers able to orchestrate complex France last-mile delivery market routes profitably.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising total cost of ownership of electric LCV fleets amid battery raw-material inflation | -0.8% | National, affecting all operators pursuing fleet electrification | Short term (≤ 2 years) |

| Strict ESG disclosure requirements increasing compliance costs for SME couriers | -0.6% | National, EU-wide regulatory requirement under CSRD | Medium term (2-4 years) |

| Low delivery density in peri-urban & rural communes eroding unit economics | -0.5% | Rural and peri-urban areas, particularly in Nouvelle-Aquitaine, Brittany, Grand Est | Long term (≥ 4 years) |

| Uncertainty around classification of gig workers under forthcoming French labour-law reforms | -0.4% | National, particularly affecting platform-based delivery services | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Rising Total Cost of Ownership of Electric LCV Fleets

Lithium carbonate’s rebound to USD 18,000 per ton in 2025 lifted battery pack prices, leaving electric vans EUR 20,000 (USD 23,526.20) costlier than diesel equivalents. Operators targeting low-emission zones must weigh upfront capex against uncertain residual values and patchy rural charging coverage. Leasing solutions that shift depreciation risk to OEMs are growing, yet smaller couriers that anchor much of the France last mile delivery market volume still postpone electrification until clearer cost trajectories emerge[3]“Raw-Material Inflation and EV Van TCO,” Transport & Environment, transportenvironment.org .

Strict ESG Disclosure Requirements Increasing Compliance Costs

The Corporate Sustainability Reporting Directive obliges around 50,000 European firms to file audited ESG statements. Annual compliance can absorb up to EUR 500,000 (USD 588,155), around 5% of revenue for a courier turning over EUR 10 million (USD 11.76 million). Data-capture, carbon accounting software, and third-party verification weigh heavily on SME balance sheets, spurring talk of mergers that could reshape competitive balance across the France last mile delivery market[4]“CSRD Transposition in France,” European Commission, finance.ec.europa.eu.

Segment Analysis

By Service: Standard Delivery Anchors Volume Amid Premium Tier Growth

Standard Delivery accounted for 62.43% of France last mile delivery market share in 2025, a dominance rooted in route density and predictable overnight sorting windows. Network efficiencies keep per-parcel tariffs low, sustaining loyalty among price-sensitive shoppers. Yet service commoditization narrows margins, motivating carriers to upsell tracking add-ons and carbon-neutral options.

Same-day volumes, while smaller, will swell at a 4.1% CAGR as grocers, pharmacies, and fashion retailers weaponize speed to reduce basket abandonment. AI dispatching, cargo-bike fleets, and micro-hubs inside supermarkets shrink urban routes below 3 km, easing cost tension. Express (next-day) remains the default B2B option for industrial spares and high-value electronics, acting as a protective middle tier between mass standard and ultra-fast niches within the wider France last mile delivery market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Business Model: B2C Dominance Faces C2C Disruption

B2C fulfilled 65.2% of parcels in 2025, benefiting from contractual demand certainty that underpins carrier network planning. Retailers negotiate annual volumes that justify hub automation and parcel-locker capex, thereby entrenching incumbents across the France last mile delivery market size hierarchy.

C2C, however, is climbing at 3.9% CAGR on the back of Vinted’s second-hand apparel ecosystem. Individual sellers create fragmented origin points that favor pickup-point models over home collection, a workflow that La Poste monetizes through Colissimo mailbox services. The France last mile delivery industry increasingly tailors APIs and smaller parcel labels to this micro-seller cohort, expanding service diversity.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-User Industry: Healthcare Acceleration Reshapes Service Requirements

Retail e-commerce still wins 61.3% of France last mile delivery market size, but incremental growth slows as penetration nears maturity. Focus has shifted to cost leadership and returns processing that safeguards thin margins.

Healthcare, rising at a 4.3% CAGR, injects new compliance layers. Pharma deliveries must hit temperature bands and signature chains set by French health authority decrees; Chronofresh’s EUR 135 million (USD 158.80 million) revenue in 2024 evidences monetization potential. This niche rewards carriers investing in ISO 13485 quality systems, offering a durable moat in the competitive France last mile delivery market.

Geography Analysis

Ile-de-France dominates with 23.2% France last mile delivery market size, and the region has high parcel flows thanks to 12 million inhabitants, concentric motorway rings, and a web of automated lockers within 500 m of 90% of households. Rapid adoption of electric cargo bikes and lightweight vans skilled at navigating Paris’s tightening low-emission zones is further cementing the capital’s lead.

Auvergne-Rhone-Alpes, Provence-Alpes-Cote d'Azur, and Hauts-de-France form a second tier, leveraging multimodal gateways in Lyon, Marseille, and Lille. Investment in logistics real estate along the “diamond” corridor boosted cross-dock capacity 30% between 2024 and 2026, shortening line-haul-to-last-mile hand-offs. However, out-of-city sprawl still drags stop density below urban break-even points.

Nouvelle-Aquitaine, Occitanie, Grand Est, and Brittany trail due to fragmented settlement patterns. Programme Marguerite pilots in Nantes tested parcel pooling among five carriers, trimming rural route length 12%, yet facing locker-installation hurdles on municipal land. Until regulatory clarity on unmanned aerial vehicles emerges, these regions are forecast to under-index relative to the overall France last mile delivery market.

Competitive Landscape

La Poste Group, through Colissimo and GeoPost, handled 53.6% of group revenue from parcels in 2025 after delivering 392 million domestic items. DHL Express, FedEx, and UPS compete on premium time-definite lanes, each deploying electric van fleets in Paris and Lyon to secure municipal access permits. Regional specialists Mondial Relay, GLS, and Colis Prive anchor pick-up-drop-off (PUDO) ecosystems, while API-centric startups such as Cubyn emphasize direct cart plug-ins for SME webshops.

Technology remains the field of play. Operators are rolling out AI-route engines, blockchain tracking, and locker clusters. Compliance with CSRD has turned verified carbon dashboards into RFP differentiators.

Scale economies appear set to intensify consolidation, with at least three mid-size couriers reportedly exploring strategic sales as ESG reporting costs bite. Collectively, these shifts define a moderately concentrated France last-mile delivery market that still leaves room for niche, value-added specialists.

France Last Mile Delivery Industry Leaders

DHL Group

La Poste Group

FedEx

United Parcel Service of America, Inc.

InPost

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- January 2026: SEGRO leased 23,351 sqm to Vinted Go at Saint-Maurice park, enlarging its second-hand logistics footprint.

- June 2025: DHL Express opens a multi-service facility at Lyon-Saint-Exupery Airport, integrating TDI and DDI flows.

- April 2025: Carrefour folded 101 Groupe Magne stores into its franchise estate, extending proximity delivery coverage.

- March 2025: La Poste Group deepened its Vinted partnership, extending Colissimo delivery via enhanced mailbox and post-office networks to support C2C parcel growth.

France Last Mile Delivery Market Report Scope

By Service

| Standard Delivery |

| Same-day |

| Express Delivery |

By Business Model

| Business-to-Business (B2B) |

| Business-to-Consumer (B2C) |

| Customer-to-Consumer (C2C) |

By End-user Industry

| E-commerce Retail |

| Fashion and Lifestyle |

| Beauty, Wellness and Personal Care |

| Home and Furniture |

| Consumer Electronics and Appliances |

| Healthcare and Medical Supplies |

| Others |

By French Region

| Ile-de-France |

| Auvergne-Rhone-Alpes |

| Provence-Alpes-Cote d'Azur |

| Hauts-de-France |

| Nouvelle-Aquitaine |

| Occitanie |

| Grand Est |

| Brittany |

| Others |

| By Service | Standard Delivery |

| Same-day | |

| Express Delivery | |

| By Business Model | Business-to-Business (B2B) |

| Business-to-Consumer (B2C) | |

| Customer-to-Consumer (C2C) | |

| By End-user Industry | E-commerce Retail |

| Fashion and Lifestyle | |

| Beauty, Wellness and Personal Care | |

| Home and Furniture | |

| Consumer Electronics and Appliances | |

| Healthcare and Medical Supplies | |

| Others | |

| By French Region | Ile-de-France |

| Auvergne-Rhone-Alpes | |

| Provence-Alpes-Cote d'Azur | |

| Hauts-de-France | |

| Nouvelle-Aquitaine | |

| Occitanie | |

| Grand Est | |

| Brittany | |

| Others |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large will parcel spending reach in France by 2031?

The France last mile delivery market size is projected to hit USD 4.20 billion by 2031, climbing at a 3.81% CAGR over 2026-2031.

Which delivery tier is expanding fastest?

Same-day delivery is forecast to post the strongest growth, advancing at a 4.1% CAGR through 2031 as urban retailers leverage micro-hubs and cargo bikes.

Why is healthcare an attractive logistics vertical?

Regulatory changes that allow direct-to-patient pharma shipping and an aging population push healthcare deliveries up at a 4.3% CAGR, rewarding carriers with temperature-controlled capability.

What is the main cost headwind for fleet electrification?

Volatile battery raw-material prices keep electric vans EUR 20,000 above diesel peers, delaying total-cost parity for many small couriers.

How is 5G improving last-mile operations?

With 34,000 active sites, France’s 5G network enables AI routing that has already cut fuel use 16% and raised on-time rates for test fleets.

Will ESG reporting rules reshape the sector?

Yes, CSRD compliance can cost small couriers up to 5% of revenue annually, favoring well-capitalized operators and accelerating consolidation.