Fluorescence Guided Surgery Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 146.75 Million |

| Market Size (2031) | USD 303.59 Million |

| Growth Rate (2026 - 2031) | 15.65% CAGR |

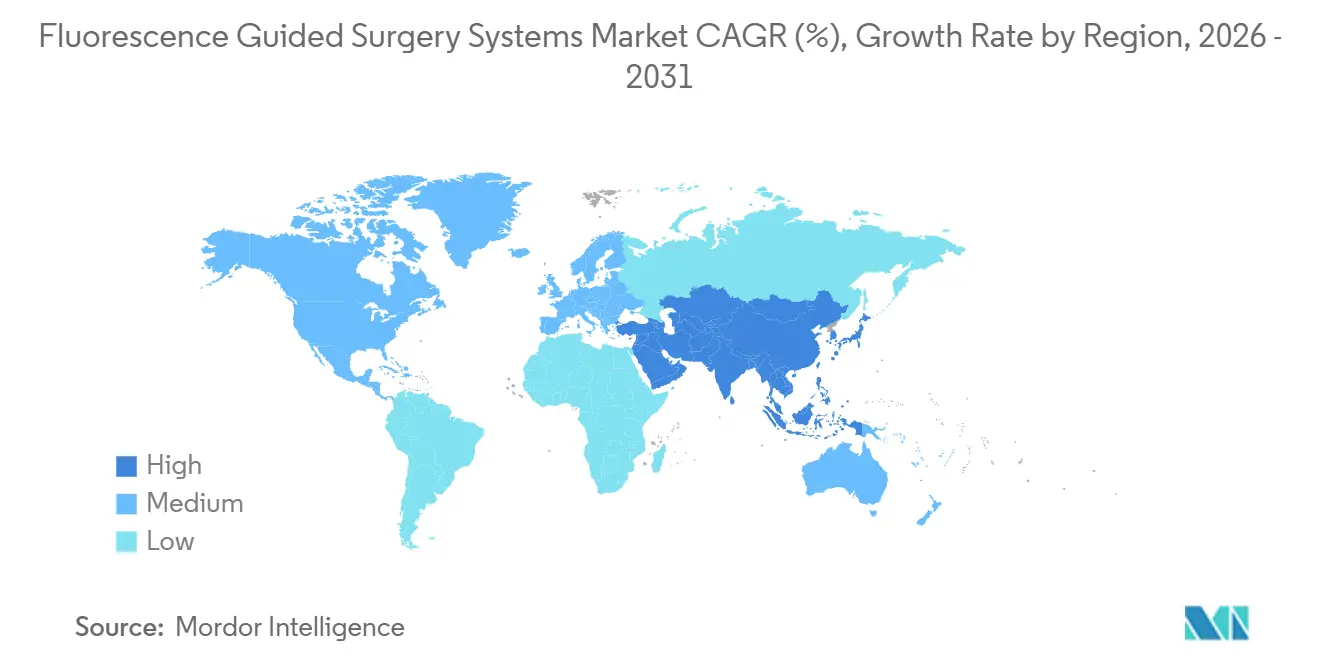

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

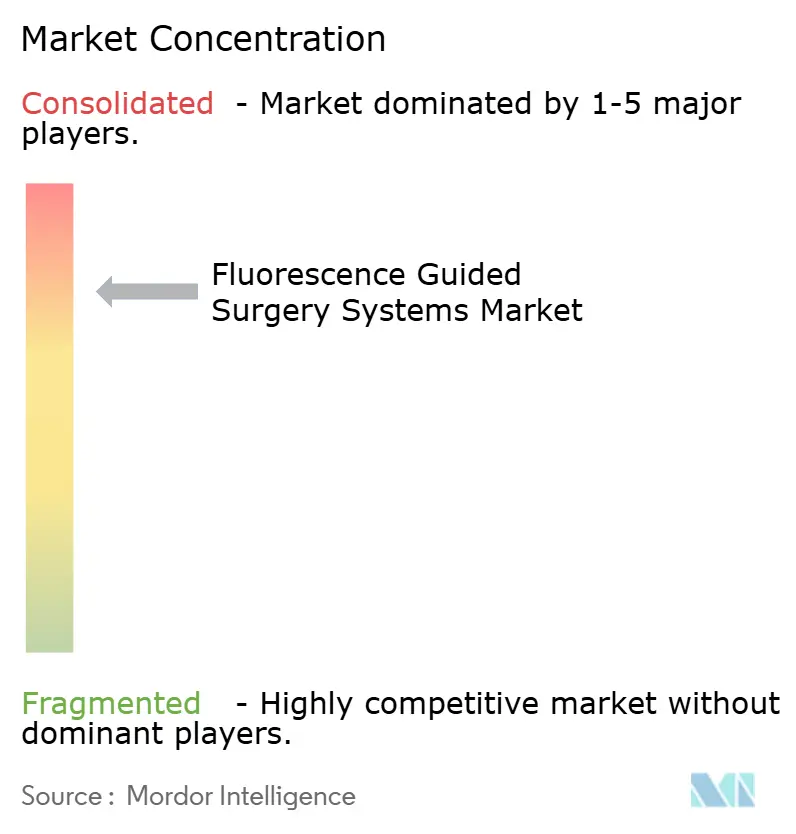

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Fluorescence Guided Surgery Systems Market Analysis by ���ϲ�����

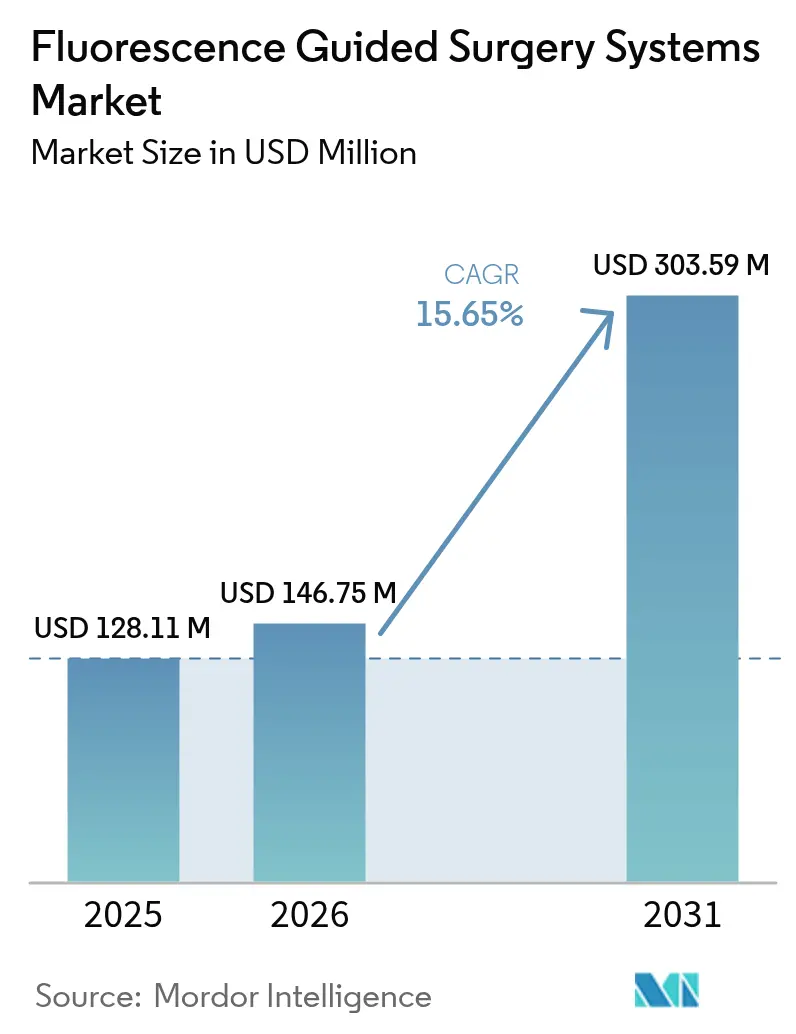

The Fluorescence Guided Surgery Systems Market size is expected to grow from USD 128.11 million in 2025 to USD 146.75 million in 2026 and is forecast to reach USD 303.59 million by 2031 at 15.65% CAGR over 2026-2031.

Robust demand reflects the way real-time near-infrared (NIR) visualization has shifted from experimental trials into mainstream workflows across oncology, cardiovascular, and reconstructive procedures. Hospitals continue to anchor spending, yet cost-conscious ambulatory surgical centers now regard fluorescence as essential, a change reinforced by bundled-payment policies that reward lower readmission rates. Hardware vendors are embedding NIR channels directly inside robotic consoles, removing the need for standalone carts and shortening case setup times. Recurring dye revenue is beginning to overshadow initial hardware margins, encouraging manufacturers to subsidize camera leases in middle-income regions.

Key Report Takeaways

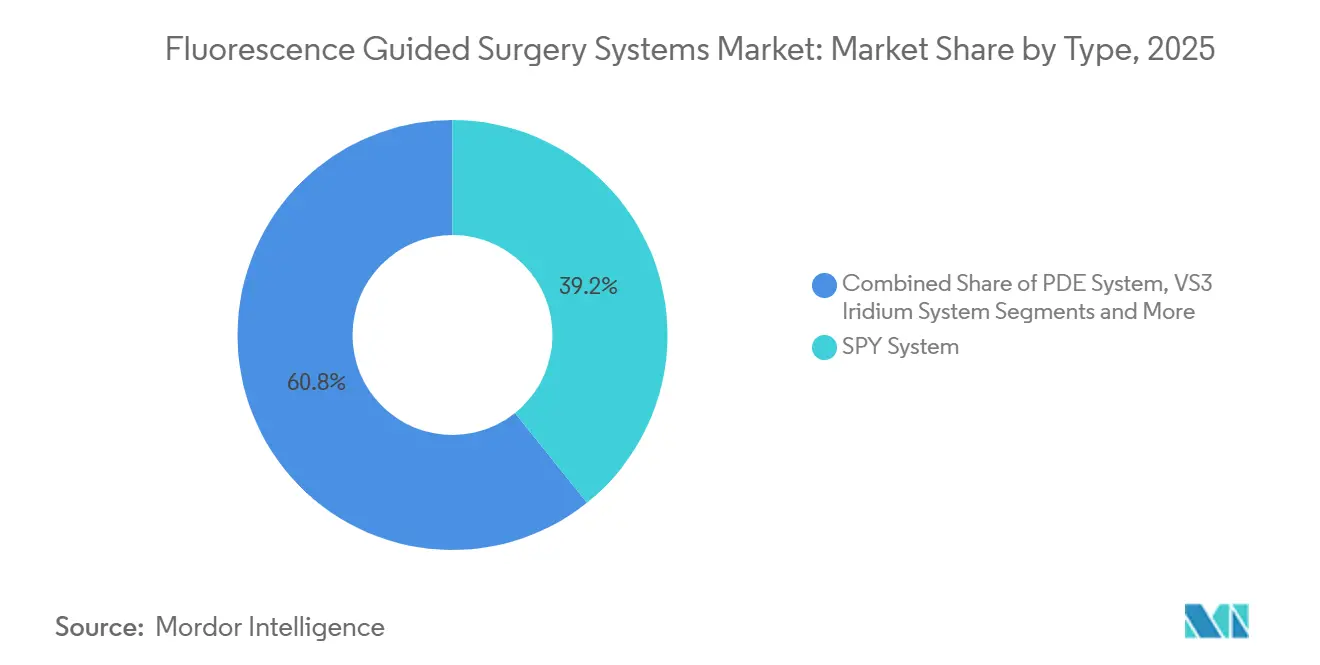

- By type, SPY platforms led with 39.24% of fluorescence-guided surgery system market share in 2025. VS3 Iridium systems are projected to expand at an 18.35% CAGR through 2031.

- By component, imaging devices accounted for 62.56% of revenue in 2025. Fluorescent agents are forecast to grow at a 20.52% CAGR to 2031.

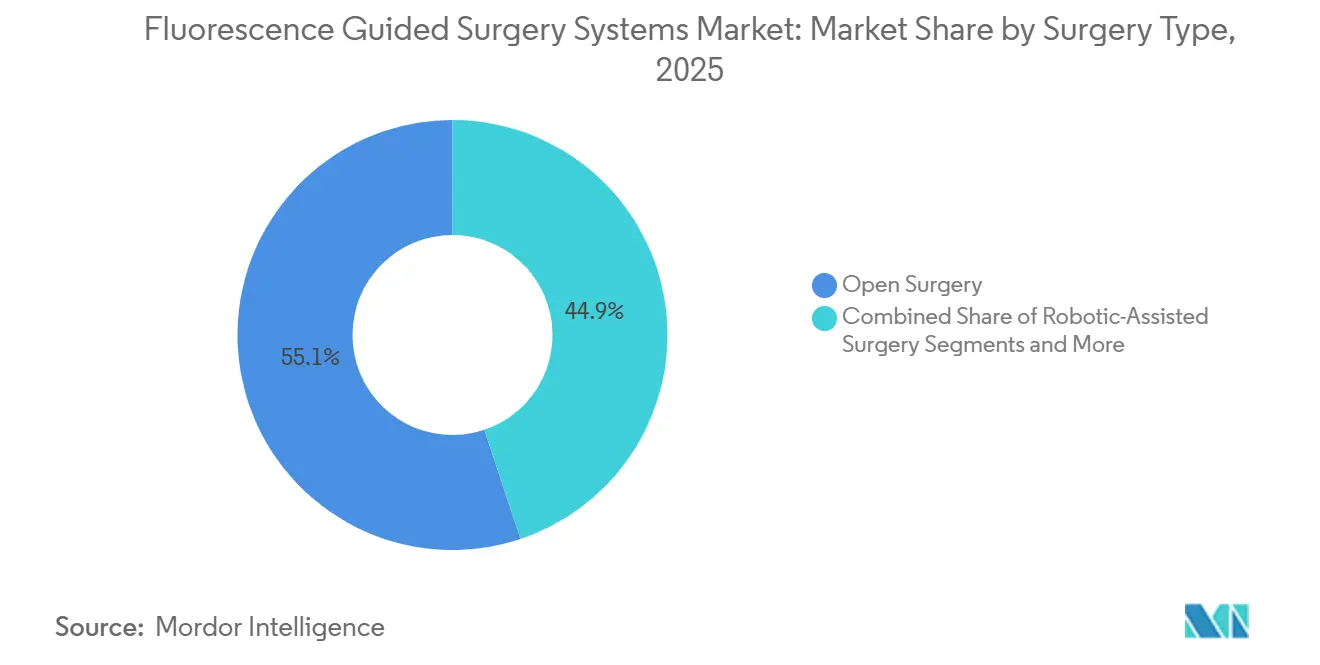

- By surgery type, open procedures held 55.14% of fluorescence-guided surgery system market share in 2025, robotic-assisted procedures are advancing at an 18.21% CAGR through 2031.

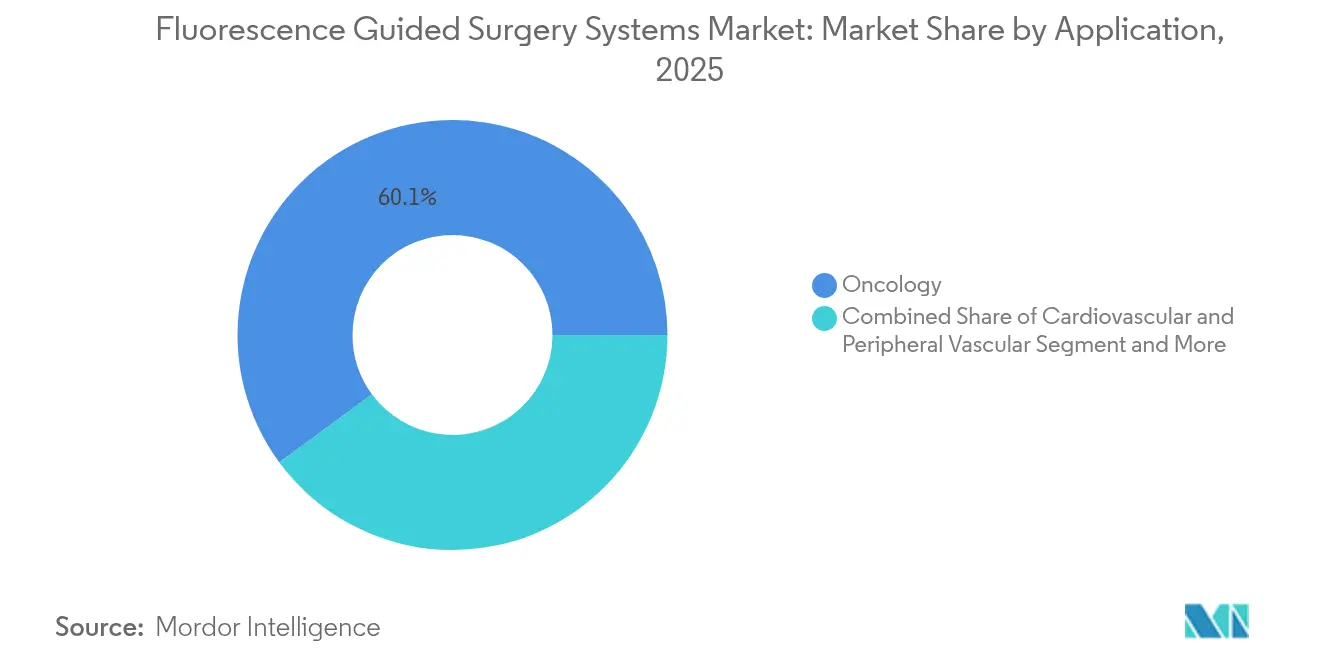

- By application, cancer surgeries commanded 59.83% of revenue in 2025, cardiovascular procedures are expected to rise at a 17.25% CAGR between 2026 and 2031.

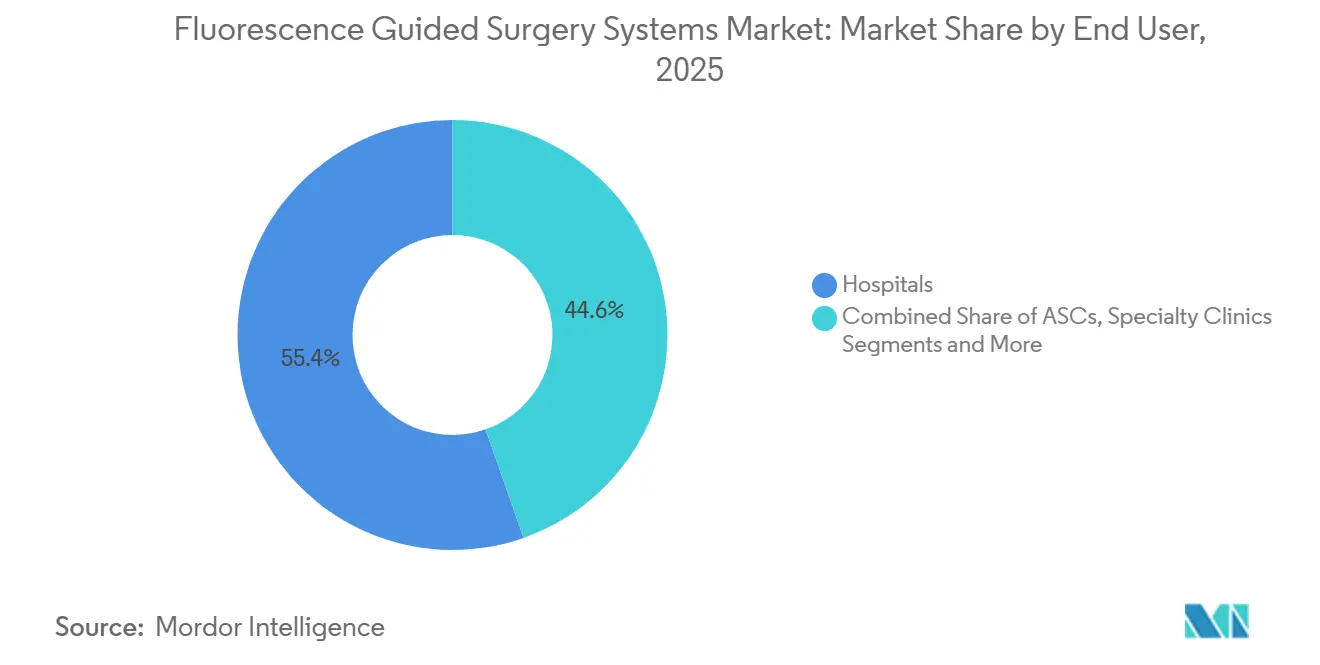

- By end user, hospitals captured 55.37% of revenue in 2025, ambulatory surgical centers are set to grow at a 19.35% CAGR through 2031.

- By geography, North America generated 38.82% of global revenue in 2025, Asia-Pacific is forecast to register a 17.02% CAGR over 2026–2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Fluorescence Guided Surgery Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption of Minimally-Invasive & Robotic Surgeries | +3.2% | North America, Western Europe, urban APAC | Medium term (2–4 years) |

| Escalating Global Cancer Incidence Demanding Precision Oncology | +2.8% | North America, Europe, East Asia | Long term (≥ 4 years) |

| Continuous Advances in NIR Cameras & Targeted Fluorophores | +2.5% | North America, Europe, Japan | Medium term (2–4 years) |

| Quantitative Perfusion Analytics Embedded in OR Workflow | +2.1% | North America, Western Europe, GCC states | Short term (≤ 2 years) |

| Emerging Government Digital-OR Procurement in Middle-Income Nations | +2.4% | China, India, Indonesia, Vietnam, LATAM, Middle East | Medium term (2–4 years) |

| AI-Enabled Fluorescence Overlay Shortening Surgeon Learning Curves | +1.9% | North America, Western Europe, Singapore, South Korea | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Rising Adoption of Minimally-Invasive & Robotic Surgeries

Intuitive Surgical disclosed that more than 60% of new da Vinci Xi and da Vinci 5 consoles shipped in 2025 included the Firefly module, up from 42% in 2023, confirming that integrated fluorescence now represents baseline specification rather than premium upgrade. This integration trims average setup time by eight minutes per case and frees valuable operating-room space previously occupied by separate carts. Robotic platforms also support real-time overlay, letting surgeons toggle between white-light and fluorescence without instrument repositioning. Uptake is especially strong in bariatric, colorectal, and gynecologic oncology, where lymph-node mapping consumes more than 1.2 vials of indocyanine green per procedure at high-volume U.S. centers. Accelerated dye utilization reinforces consumable-led revenue growth for vendors.

Escalating Global Cancer Incidence Demanding Precision Oncology

The World Health Organization recorded 20.8 million new cancer diagnoses in 2024, a 12% rise over 2020, with liver, pancreatic, and colorectal tumors climbing fastest in older populations.[1]Freddie Bray, “Global Cancer Statistics 2024,” International Agency for Research on Cancer, iarc.fr Intraoperative margin assessment remains subjective for many solid tumors, so targeted fluorophores such as OnLume OTL38, approved in 2024, extend visualization beyond generic perfusion agents. Memorial Sloan Kettering showed that folate-targeted fluorescence cut positive-margin rates in ovarian debulking by 23 percentage points, prompting U.S. and German payers to broaden coverage.[2]Anastasia L. Wysham, “Folate-Targeted Fluorescence Reduces Positive Margins in Ovarian Cancer Surgery,” Annals of Surgical Oncology, springer.com Growing evidence strengthens hospital ROI cases and secures budget lines for new systems.

Continuous Advances in NIR Cameras & Targeted Fluorophores

Hamamatsu’s C15440 digital CMOS sensor, released in 2025, delivers 40% greater signal-to-noise ratio than prior models, detecting dye concentrations under 0.5 µg/mL.[3]Hiroshi Yamaoka, “C15440 Series NIR Camera Technical Specifications,” Hamamatsu Photonics, hamamatsu.com Concurrently, Curadel’s CLR1502 nerve-specific agent finished Phase II trials and targets regulatory submission in 2026. Enhanced cameras and specialized dyes converge to enable multi-spectral imaging, so surgeons can view perfusion, tumor margins, and nerve anatomy simultaneously, a capability unavailable before 2024.

Quantitative Perfusion Analytics Embedded in OR Workflow

Stryker’s SPY-Q software converts pixel intensity into objective metrics such as time-to-peak and ingress slope, guiding anastomotic site selection. A 2025 multicenter study of 1,200 colorectal cases documented leak reduction from 8.3% to 4.1%, saving hospitals roughly USD 12,000 per patient. Quantitative data also support post-hoc quality audits and accelerate academic adoption.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Capital Cost of Integrated Platforms | -1.8% | Global; strongest in APAC, LATAM, Middle East | Medium term (2–4 years) |

| Stringent Regulatory Timelines for New Fluorophores | -1.3% | North America, Europe | Long term (≥ 4 years) |

| Supply-Chain Fragility of Indocyanine-Green Raw Materials | -1.1% | Global, sourcing concentrated in China, India | Short term (≤ 2 years) |

| Lack of Standardized Training Curricula Across Regions | -0.9% | Global; acute in emerging markets | Medium term (2–4 years) |

| Source: ���ϲ����� | |||

High Upfront Capital Cost of Integrated Platforms

Integrated fluorescence towers list between USD 300,000 and USD 800,000. Stryker’s SPY-PHI package carries a USD 650,000 sticker and adds annual service contracts equal to 8–12% of purchase price. A 2025 survey of 120 U.S. ambulatory centers showed 68% flagged capital cost as the primary barrier despite proven clinical savings. Lease terms help but often bind facilities to exclusive dye contracts, limiting price leverage.

Stringent Regulatory Timelines for New Fluorophores

OnLume OTL38 required 22 months from FDA filing to approval even under priority review. EMA’s ongoing evaluation of Curadel CLR1502 is expected to span until late 2026. The disparity between rapid hardware clearance and elongated dye approval delays full clinical utility.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: SPY Systems Lead, VS3 Iridium Accelerates

SPY platforms held 39.24% of fluorescence-guided surgery system market share in 2025, capitalizing on extensive cardiac and plastic-surgery installations. VS3 Iridium units are expanding at an 18.35% CAGR, leveraging high-resolution optics favored in neurosurgery and ENT. PDE systems remain steady in legacy open procedures, whereas modular carts from Quest and OptoMedic entice ambulatory centers with sub-USD 150,000 entry pricing. The fluorescence-guided surgery system market is thus splitting between premium integrated ecosystems and portable value lines that promise lower total cost of ownership.

Service-driven ecosystem effects amplify SPY dominance, as real-world data harvested from its installed base refine perfusion algorithms and support reimbursement negotiations. VisionSense focuses on narrow-field niches where microscope mounting trumps laparoscopic integration. Portable “other systems” meet the needs of outpatient facilities lacking floor space for robotic stacks, demonstrating how capital constraints can redirect share inside the fluorescence-guided surgery system market.

By Component: Imaging Devices Dominate, Dyes Outpace

Imaging hardware generated 62.56% of 2025 revenue, yet fluorescent agents are forecast to climb 20.52% annually, showing the installed-base-to-consumable flywheel typical of maturing capital-equipment sectors. Software modules that deliver AI segmentation and quantitative analytics are increasingly bundled, muddying stand-alone revenue visibility but boosting switching costs.

Indocyanine green still represents 85% of dye volume, although premium tumor- or nerve-specific agents are gaining traction where clinical benefit justifies higher price points. The fluorescence-guided surgery system market size attributed to dyes will therefore expand faster than hardware, creating new entry points for specialty pharma and pushing device vendors toward vertical integration to protect margins.

By Surgery Type: Open Dominates, Robotic Surges

Open surgery commanded 55.14% of 2025 procedures, reflecting ongoing reliance in complex resections and trauma. Robotic-assisted cases, while smaller in volume, are growing at 18.21% through 2031 as fluorescence becomes a default line item in console procurement. Laparoscopy retains mid-tier share, especially in cost-sensitive regions, yet faces long-term attrition as robotic ergonomics improve.

Hospitals continue to purchase handheld fluorescence cameras for open cases that lack robotic access, ensuring the fluorescence-guided surgery system market retains a hardware mix. Laparoscopy will persist where capital budgets cannot stretch to robotics, but vendors are increasingly positioning robotic stack upgrades as lifecycle replacements for end-of-life laparoscopic towers.

By Application: Cancer Anchors, Cardiovascular Accelerates

Cancer surgery generated 59.83% of 2025 revenue, driven by sentinel-node mapping and margin visualization across breast, colorectal, ovarian, and head-and-neck procedures. Cardiovascular applications are on track for a 17.25% CAGR as perfusion analytics lower graft-failure-related readmissions. Neurosurgery adoption increases with 5-ALA and upcoming tumor-specific probes, while plastic & reconstructive usage sits in a stable niche awaiting broader reimbursement.

Guideline changes by the American Society of Breast Surgeons and updated cardiovascular meta-analyses validate outcomes, ensuring cancer and cardiac indications stay at the forefront of the fluorescence-guided surgery system market growth curve.

By End User: Hospitals Hold, ASCs Rise

Hospitals delivered 55.37% of 2025 sales, yet ambulatory surgical centers are projected to expand 19.35% annually through 2031 as payers push elective volumes outpatient. Specialty clinics maintain mid-tier revenue, while academic institutes drive training and protocol-development influence disproportionate to their direct spending.

ASC buyers prefer mid-tier systems priced below USD 250,000 and often negotiate dye bulk contracts through group-purchasing organizations, shifting part of the fluorescence-guided surgery system market toward lower-capex, high-utilization environments.

Geography Analysis

North America generated 38.82% of 2025 revenue, underpinned by Medicare reimbursement for fluorescence-guided sentinel-node mapping and a dense installed base of robotic suites. Value-based contracts that penalize 90-day complications further motivate adoption. Europe occupies a solid mid-tier position, buttressed by guideline endorsements from national oncology societies and reimbursement inclusion in Germany, France, and the United Kingdom.

Asia-Pacific is forecast to grow 17.02% through 2031 on the back of government digital-OR mandates that bundle fluorescence imaging with robotics and AI planning. China’s expedited NMPA pathway and India’s fast-track device approvals shorten time-to-market for domestic producers, pressuring incumbent pricing. Gulf Cooperation Council states are rolling out fluorescence requirements in new oncology centers, while South America exhibits selective private-hospital adoption despite macroeconomic headwinds.

Regulatory contrasts shape market velocity: the U.S. 510(k) route averages nine months, EU MDR reviews stretch past a year, and China’s expedited device channel now rivals Western timelines, redistributing competitive advantage. These regional nuances will continue to steer vendor strategy and pricing inside the fluorescence-guided surgery system market.

Competitive Landscape

The fluorescence-guided surgery system market a high concentration profile. Stryker, Medtronic, Intuitive Surgical, KARL STORZ, and Olympus bundle fluorescence with larger capital portfolios, leveraging service contracts and data-analytics platforms to raise switching barriers. Still, cost-effective challengers like Quest Medical Imaging, OptoMedic, and Mindray target outpatient and emerging-market tiers with modular, software-upgradeable systems priced under USD 200,000.

Patent filings emphasize AI-driven segmentation as hardware performance converges. Intuitive Surgical’s 2024 submission details real-time convolutional-neural-network processing, a direction mirrored by Zeiss and Medtronic. Meanwhile, incumbents pursue vertical dye-supply agreements to lock in consumable profit pools. Geographic diversification strategies include localized manufacturing lines in China and lease-to-own financing in India, underlining how price sensitivity guides competitive positioning across the fluorescence-guided surgery system market.

Start-ups exploit procedural niches: OptoMedic’s disposable nerve-identification probe sidesteps high capital barriers, while Trace Biosciences pursues orphan-drug fluorophores for pancreatic and biliary tumors. As regulatory pathways accelerate in Asia, domestic players will likely capture share, intensifying pressure on multinational incumbents to differentiate via data ecosystems and service breadth.

Fluorescence Guided Surgery Systems Industry Leaders

Hamamatsu Photonics K.K.

Medtronic PLC

Stryker Corp. (Novadaq)

Olympus Corp. (Quest Medical Imaging)

Karl Storz SE & Co. KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: FluoGuide received FDA clearance to initiate a registrational trial of FG001 for high-grade glioma.

- January 2026: Trace Biosciences secured IND approval for LGW16-03, its first nerve-specific fluorescent agent.

- January 2026: CPI-008, an integrin-targeted imaging dye, won orphan-drug status from both FDA and EMA for pancreatic-cancer margin detection.

Global Fluorescence Guided Surgery Systems Market Report Scope

As per the scope of the report, Fluorescence Guided Surgery (FGS) systems are intraoperative imaging technologies that use fluorescent dyes and specialized equipment to differentiate diseased tissue from healthy tissue in real-time, enhancing surgical precision and patient safety.

The Fluorescence‑Guided Surgery System Market Report is segmented by Type, Component, Surgery Type, Application, End User, and Geography. By Type, the market is segmented into SPY, PDE, VS3 Iridium, and Other Systems. By Component, the market is segmented into Imaging Devices, Fluorescent Agents, and Software. By Surgery Type, the market is segmented into Open, Laparoscopy, and Robotic‑Assisted surgeries. By Application, the market is segmented into Cancer, Cardiovascular, Neurosurgery, Plastic & Reconstructive, and Other applications. By End User, the market is segmented into Hospitals, ASCs, Specialty Clinics, and Research Institutes. By Geography, the market is segmented into North America, Europe, APAC, MEA, and South America. The report also covers the estimated market sizes and trends for 17 different countries across major regions. The report offers values in USD million for the above segments.

| SPY System |

| PDE System |

| VS3 Iridium System |

| Other Systems |

| Imaging Devices |

| Fluorescent Agents & Dyes |

| Software & Accessories |

| Open Surgery |

| Laparoscopy / Endoscopy |

| Robotic-Assisted Surgery |

| Cancer Surgeries |

| Cardiovascular Surgeries |

| Neurosurgery |

| Plastic & Reconstructive Surgeries |

| Other Applications |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Clinics |

| Research & Academic Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | SPY System | |

| PDE System | ||

| VS3 Iridium System | ||

| Other Systems | ||

| By Component | Imaging Devices | |

| Fluorescent Agents & Dyes | ||

| Software & Accessories | ||

| By Surgery Type | Open Surgery | |

| Laparoscopy / Endoscopy | ||

| Robotic-Assisted Surgery | ||

| By Application | Cancer Surgeries | |

| Cardiovascular Surgeries | ||

| Neurosurgery | ||

| Plastic & Reconstructive Surgeries | ||

| Other Applications | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Clinics | ||

| Research & Academic Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the fluorescence-guided surgery system market?

The market was valued at USD 146.75 million in 2026.

How fast is the market expected to grow?

It is projected to post a 15.65% CAGR between 2026 and 2031.

Which application generates the most revenue?

Cancer surgeries accounted for 59.83% of 2025 revenue.

Why are ambulatory surgical centers adopting fluorescence systems?

ASCs benefit from faster patient discharge and have access to mid-tier systems priced below USD 250,000, supporting a forecast 19.35% CAGR.

Which region offers the highest growth potential?

Asia-Pacific is set to grow at 17.02% through 2031, aided by government digital-OR mandates.

What is the main restraint to wider adoption?

High upfront capital cost remains the most significant barrier, particularly for budget-sensitive facilities.

Page last updated on: