Vietnam Floriculture Market Analysis by ���ϲ�����

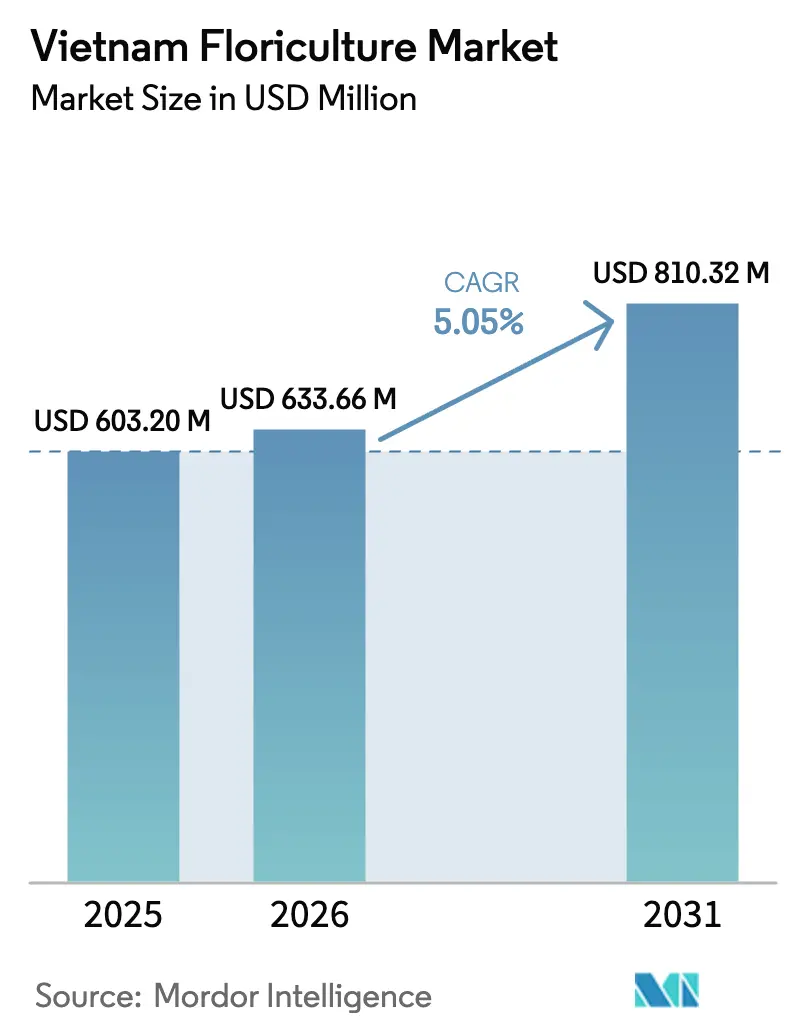

The Vietnam floriculture market size is anticipated to increase from USD 0.67 billion in 2025 to USD 0.74 billion in 2026 and reach USD 1.05 billion by 2031, growing at a CAGR of 9.4% over 2026-2031. Favorable climatic diversity across the country enables continuous production of temperate roses, carnations, and chrysanthemums in the Central Highlands while sustaining tropical orchids in lowland deltas, reducing the need for costly year-round climate control and underpinning a steady domestic supply. Bilateral free-trade agreements with Japan and Korea have removed tariffs on cut flowers, widening export margins by 8–12 percentage points and elevating Vietnam from a subsistence grower to a top-tier regional supplier. Rapid cold-chain expansion, especially in the Dalat- Ho Chi Minh City corridor, equipped with 2–8 °C trucks, has lowered post-harvest losses from 22% to 4% and extended rose shelf life to 9 days. With 20% of capital costs subsidized, Lam Dong province expanded its high-tech greenhouses to 5,600 hectares, achieving annual yields of VND 2 billion (USD 81,300) per hectare and bolstering Vietnam's floral exports to East Asia.

Key Report Takeaways

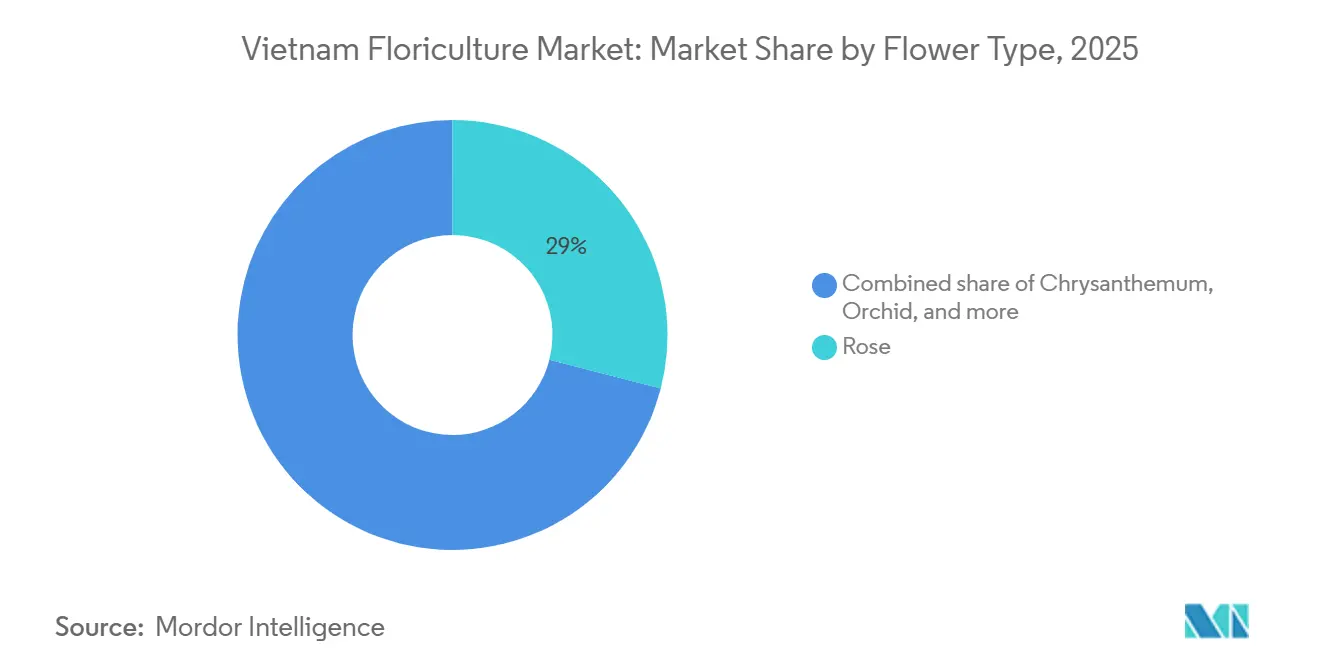

- By flower type, rose commanded a 29% share of the Vietnam floriculture market size in 2025, while orchid is forecast to record a 10.6% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Vietnam Floriculture Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Favorable climatic diversity along Vietnam’s latitude | +2.1% | Central Highlands and Northern mountain zones | Long term (≥ 4 years) |

| Growing bilateral flower-trade agreements | +1.8% | Nationwide, with an export focus in the Central Highlands and Southeast | Medium term (2-4 years) |

| Expansion of cold-chain logistics corridors | +1.5% | Dalat-Ho Chi Minh City and Mekong Delta corridors | Medium term (2-4 years) |

| Government subsidies for greenhouse modernization | +1.3% | Central Highlands and Red River Delta | Short term (≤ 2 years) |

| Pilot carbon-credit pricing for sustainable floriculture | +0.9% | Central Highlands and Southeast | Long term (≥ 4 years) |

| Bundled micro-finance for smallholder ornamental growers | +1.2% | Mekong Delta and South Central Coast | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Favorable Climatic Diversity Along Vietnam’s Latitude

Vietnam stretches from 8°N to 23°N, creating cool highland microclimates suited to premium temperate flowers and warm lowland zones ideal for orchids. Lam Dong’s 1,500-meter elevation delivers stable 18-22 °C temperatures that meet optimal rose requirements and save growers 30-40% in heating and cooling costs compared with single-climate markets[1]Source: Lam Dong Meteorological Station, “Lam Dong Climate Data 2024-2025,” lamdong.nchmf.gov.vn. By utilizing 0% tariffs under the CPTPP, Vietnam increased its share of Japan's flower imports to over 14% in 2025, effectively replacing higher-cost suppliers from Kenya and Ecuador due to its logistical advantages and duty-free access. Hanoi’s Red River Delta now hosts 3,000 hectares of high-tech flower farms that exploit four-season conditions to supply chrysanthemums to China within 48 hours. Staggered planting across altitudes supports non-stop harvesting, lowering inventory costs by 18% and improving exporter cash cycles. Widespread climatic flexibility positions the Vietnam floriculture market as a consistent supplier when seasonal shortages constrain competitors.

Growing Bilateral Flower-Trade Agreements

The Japan-Vietnam Economic Partnership Agreement and the Korea-Vietnam Free Trade Agreement eliminated tariffs on cut flowers, shrinking landed costs for Vietnamese stems by up to 12 percentage points[2]Source: Korea Customs Service, “Korea Flower Import Statistics 2023,” customs.go.kr . In 2023, Vietnam became South Korea's largest flower supplier by volume accounting for 3.45 thousand metric tons and the second largest by value accounting for USD 13.5 million, with orchids and chrysanthemums accounting for 68% of shipments to meet ceremonial and retail demand. Duty-free access also propelled Japan-bound sales to USD 45 million in 2021, and Vietnam added 2.3 percentage points of Japanese market share in 2024 by guaranteeing 7-day delivery versus 12-day South American transits. Vietnamese floriculture is utilizing duty-free access under the The Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP) and The Regional Comprehensive Economic Partnership (RCEP) agreements to target Australia as a high-value market. Premium tropical orchids are positioned to command significantly higher prices compared to regional markets, supported by a broader bilateral trade relationship valued at USD 14.1 billion. In 2025, Vietnam's Plant Protection Department (PPD) will implement streamlined e-Phyto protocols, enabling perishable goods to clear borders within 24 hours. This aims to cut rejection rates below 2% and reduce spoilage, boosting exporter margins.

Expansion of Cold-Chain Logistics Corridors

In 2025, upgrading the Dalat-Tan Son Nhat route to 2–8°C refrigerated logistics extended rose shelf life to 9 days and cut transit spoilage from 22% to under 5%, boosting Vietnam's export competitiveness. In late 2025 and early 2026, DHL and FedEx expanded logistics operations at Tan Son Nhat International Airport. DHL Group increased its Container Freight Station (CFS) capacity to 6,800 m² to accelerate the consolidation of temperature-sensitive and high-value exports to Japan and Korea. To become a 'Flower City' by 2026, Dong Thap has set up a centralized cold storage in Sa Dec, aiming to cut logistics costs by 12% and reduce post-harvest waste for flower and ornamental plant exporters. Eight relay stations along the Mekong Delta- Ho Chi Minh City artery now maintain unbroken cool chains, cutting chrysanthemum spoilage from 18% to 6%. Internet-of-Things sensors across 376 hectares of Lam Dong greenhouses issue real-time alerts within 15 minutes, preventing USD 2.8 million of annual rejected shipments.

Government Subsidies for Greenhouse Modernization

Under the 2021–2025 High-Tech Agriculture Project, Vietnam allocated VND 20 billion (USD 770.12 million) in Hai Duong for greenhouse construction and introduced a VND 750 trillion (USD 28.8 billion) green credit pool with 2% interest subsidies to shorten payback periods for investors[3]Source: Vietnam Ministry of Agriculture and Rural Development, “National Floriculture Development Strategy 2024-2030,” mard.gov.vn. By Q1 2024, Lam Dong had developed 5,600 hectares of advanced floral structures, generating up to VND 2 billion (USD 77.01 thousand) per hectare annually with 40% less water than traditional methods. High-tech Phalaenopsis orchid farms in Hai Phong, using Israeli-designed automated greenhouse systems, require up to VND 40 billion (USD 1.54 million) per hectare and deliver returns far exceeding traditional agriculture in the Red River Delta. The subsidy prioritizes 10-hectare cooperatives, channeling 68% of disbursements into Central Highlands and Mekong Delta sites where scale maximizes paybacks. Upgraded greenhouses reduce pesticide use by 30% and strengthen compliance with Global Good Agriculture Practices (GlobalGAP) requirements, which are critical for export entry.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront drip-irrigation retrofit costs | -1.4% | Nationwide, acute in Mekong Delta and South Central Coast | Medium term (2-4 years) |

| Rising incidence of pest infestations | -1.1% | Central Highlands and Red River Delta | Short term (≤ 2 years) |

| Lack of pathogen-free tissue-culture labs outside Lam Dong | -0.8% | Mekong Delta, Northern highlands, South Central Coast | Long term (≥ 4 years) |

| Increasing coastal water-salinity from upstream dams | -0.7% | Mekong Delta and South Central Coast | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

High Upfront Drip-Irrigation Retrofit Costs

Professional drip and fertigation systems require an initial investment of USD 18,000 per hectare. Lam Dong’s high-value floral exporters recover these costs within three years, but long-term payback periods challenge smallholders reliant on volatile wholesale vegetable markets. High-tech irrigation can halve water use, but with a low agricultural tariff of VND 1,200 (USD 0.046) per unit, annual savings of USD 195–341 make 9% commercial interest rates viable only with yield-driven revenue gains and a 2% government interest-rate subsidy. Smallholders in Vietnam, averaging 0.8 hectares, often lack collateral for traditional loans, extending payback periods to 8 years without the 2026 government's 'Green Credit' subsidies. High-tech irrigation in Lam Dong covers over 23,900 hectares in the vegetable sector, while the floriculture sector is expanding through the USD 120 million 'Smart Flower Village' initiative. The Vietnamese government offers a 20% subsidy, reducing the cost of high-tech irrigation to USD 14,400. However, nine-month bureaucratic delays limit participation to 15% of eligible farms, leaving much of the market without financial support.

Rising Incidence of Pest Infestations

Tuta absoluta remains the most destructive pest of tomatoes in Lam Dong, with the potential for complete yield loss. As of 2025, no significant host shift to carnations has been observed. Floral producers focus on managing thrips and mites to meet export standards for Japan and South Korea. The higher rate of insecticide spraying per month raises pesticide outlays to a significant share of total costs, and risking residue rejections in Japan and Korea. In the Me Linh rose-growing district, 95% of households face challenges from resistant thrips and spider mites. Chemical application rates here have reached 28.6 kg of active ingredient per hectare, nearly five times the 5.6 kg/ha standard in the Netherlands, where biological controls are prevalent. Monoculture rose belts on the Lang Biang Plateau are facing severe whitefly infestations, exceeding the economic threshold by 20 times. Provincial authorities are supporting high-tech farming models to stabilize incomes and improve pest resilience. Vietnam mitigates the risk of invasive species such as Drosophila suzukii through 9 Regional Plant Quarantine Sub-departments and 40 border stations, supporting 61 provincial sub-departments in protecting its vast agricultural landscape.

Segment Analysis

By Flower Type: Export-Oriented Orchids Overtake Traditional Staples

Rose maintained the highest 29% consumption share of the Vietnam floriculture market size in 2025, while orchid registered to be the fastest-growing segment, projected to register a 10.6% CAGR through 2031. Using in vitro tissue culture to reduce disease risks, Lam Dong expanded orchid cultivation to 100 hectares by 2025, producing 16 million pots annually and solidifying its position in the Northeast Asian export market. High-tech Phalaenopsis orchid farms in Hai Phong, using Israeli-designed automated greenhouse systems, generate VND 80 billion (USD 3.25 million) per hectare annually, tripling the revenue from rose harvests and making them the city's top floral export. Premium export pricing in Japan and Australia, where orchids sell 40-60% above roses, underlies the rising adoption by growers.

High-tech production in highland areas like Lang Biang generates VND 1–3 billion (USD 38-115 million) per hectare annually, meeting peak demand during Tet and Valentine’s Day. Chrysanthemums hold a prominent share, supported by year-round supply from Sa Dec to China and Taiwan. Lily hectares in Khanh Hoa climbed to 180 by 2025 and deliver 38-42% gross margins, displacing disease-stricken carnations. IoT irrigation on 376 hectares curbed water use 30-50%, raising net margins for orchid and lily growers by up to nine points.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

The Central Highlands led Vietnam's floriculture market share in 2025, owing to significant production of billions of stems and growing exports, while the Mekong River Delta is forecast to expand rapidly at a CAGR over 2026-2031. With 5,600 hectares of advanced greenhouses, Lam Dong's floral industry uses a 4-hour cold-chain corridor to Tan Son Nhat Airport, ensuring freshness for exports to Japan and South Korea. The region’s dominance is reinforced by Dalat Hasfarm’s 340-hectare hub, which dispatches 150 million stems annually. Dak Lak supports 1,800 hectares of orchids and foliage geared to Chinese and Taiwanese landscapers.

The Southeast region, anchored by Ho Chi Minh City and Binh Duong, accounts for 18% of value through its wholesale markets, which move 2 million stems daily during peak weeks. The Red River Delta holds 3,000 hectares of chrysanthemums and lilies for quick export to China. South Central Coast provinces such as Khanh Hoa grow lilies and carnations across 180 hectares that mature 8-10 days sooner than Central Highlands crops. Each zone leverages distinct climate niches and transport pathways to segment supply.

Regional expansion hinges on the build-out of the cold chain and access to financing. New Mekong cold stores, micro-finance, and water-saving lilies are anticipated to lift that region’s share by three points by 2031. Central Highlands growth will rely on carbon-credit income and Global Good Agriculture Practices (GlobalGAP) certification to capture European Union (EU) orders. Salinity-affected delta districts may shift into salt-tolerant ornamentals pending reservoir completion. Together, these regional dynamics will shape future gains in Vietnam's floriculture market size.

Competitive Landscape

Dalat Hasfarm, Dutch Flower Group, Langbiang Farm, Dümmen Orange, and Fresh Flower World complete the top five players list with a combined majority share of the Vietnam floriculture market in 2025 leveraging proprietary genetics and vertically integrated logistics that shave 12-15% off landed costs. In December 2025, Hasfarm Holdings acquired the Lynch Group for USD 270 million, establishing a vertically integrated floriculture platform in the Asia-Pacific. This strengthened cold-chain capabilities, ensuring year-round supply for retail markets in Australia, China, and Japan. Dutch Flower Group introduces high-royalty cultivars that earn 20-25% price premiums, locking in supermarket buyers seeking novelty blooms.

Both deploy Internet of Things (IoT)-enabled greenhouses that deliver 18% input savings and a consistent 60-centimeter stem length demanded by Japanese wholesalers. Langbiang’s 7-hectare greenhouse, in partnership with Netherlands-based Rijk Zwaan, is trialing 12 climate-adapted eustoma lines, improving yields by 20%. Dummen Orange supplies 8 million disease-indexed plantlets yearly while its 500-kilowatt solar array lowers energy costs by 60%. Fresh Flower World focuses on domestic ecommerce, offering next-day delivery to 35 cities and boosting urban demand.

Future competition will revolve around carbon-credit monetization, organic certification, and native species breeding. Early adopters of solar-thermal heating and biogas digesters already achieve 2-4% EBITDA uplift under the 2025 pilot. Organic floriculture now accounts for less than 2% of output, signaling white-space potential as European Union (EU) retailers expand pesticide-free aisles. Native Curcuma varieties face no import competition but require investment in breeding to meet export standards. Companies that integrate genetics, finance, and climate-smart tech will consolidate gains as the Vietnam floriculture market grows.

Recent Industry Developments

- February 2026: Hanoi expanded high-tech flower farming by rolling out greenhouses and net houses across 1,800 hectares in five suburban districts, integrating automated irrigation, light, and temperature-control systems that push annual revenue potential to VND 2.2 billion (USD 83,300) per hectare

- February 2026: The Vietnam National University of Agriculture opened the Flower-Ornamental Plant Festival 2025 and, together with the Ministry of Agriculture and Environment, set out five strategic solution groups, including formal sector recognition, technology adoption, and brand building to elevate Vietnamese floriculture into a nationally branded, policy-backed growth engine

- July 2025: Dalat Hasfarm completed its USD 180 million acquisition of Australia’s Lynch Group, unifying 340 hectares of production and 150 million annual stem capacity.

Vietnam Floriculture Market Report Scope

Floriculture is a branch of horticulture that involves cultivating flowering and ornamental plants.

The Vietnamese floriculture market is segmented by type (rose, chrysanthemum, orchid, carnation, and lilies). The report also includes an import (volume and value) and export (volume and value) analysis of the abovementioned flower types.

The report offers market size and forecasts in terms of value (USD) for all the above segments.

By Flower Type

| Rose | Production Analysis | Production Volume | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Trade Analysis (Value and Volume) | Import Market Analysis | Import Value and Volume | |

| Key Supplying Markets | |||

| Export Market Analysis | Export Value and Volume | ||

| Key Destinations Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Seasonality Analysis | |||

| Chrysanthemum | Production Analysis | Production Volume | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Import Value and Volume | |||

| Key Supplying Markets | |||

| Export Value and Volume | |||

| Key Destinations Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Seasonality Analysis | |||

| Orchid | Production Analysis | Production Volume | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Import Value and Volume | |||

| Key Supplying Markets | |||

| Export Value and Volume | |||

| Key Destinations Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Seasonality Analysis | |||

| Carnation | Production Analysis | Production Volume | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Import Value and Volume | |||

| Key Supplying Markets | |||

| Export Value and Volume | |||

| Key Destinations Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Seasonality Analysis | |||

| Lily | Production Analysis | Production Volume | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Import Value and Volume | |||

| Key Supplying Markets | |||

| Export Value and Volume | |||

| Key Destinations Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Seasonality Analysis | |||

| By Flower Type | Rose | Production Analysis | Production Volume | |

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Trade Analysis (Value and Volume) | Import Market Analysis | Import Value and Volume | ||

| Key Supplying Markets | ||||

| Export Market Analysis | Export Value and Volume | |||

| Key Destinations Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Chrysanthemum | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destinations Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Orchid | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destinations Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Carnation | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destinations Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Lily | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destinations Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the projected value of the Vietnam floriculture market in 2031?

The market is forecast to reach USD 1.05 billion by 2031.

Which flower type is growing fastest in Vietnam?

Orchids are anticipated to post a 10.6% CAGR between 2026 and 2031.

Why are cold-chain corridors important for Vietnamese flowers?

They cut post-harvest spoilage from 22% to 4% and extended rose shelf life to 9 days, enabling profitable exports.

How concentrated is competition among Vietnamese floriculture firms?

The five largest companies together hold the majority of revenue, indicating moderate concentration.