Fermented Feed Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Market Size (2025) | USD 25.12 Billion |

| Market Size (2030) | USD 35.71 Billion |

| Growth Rate (2025 - 2030) | 7.30% CAGR |

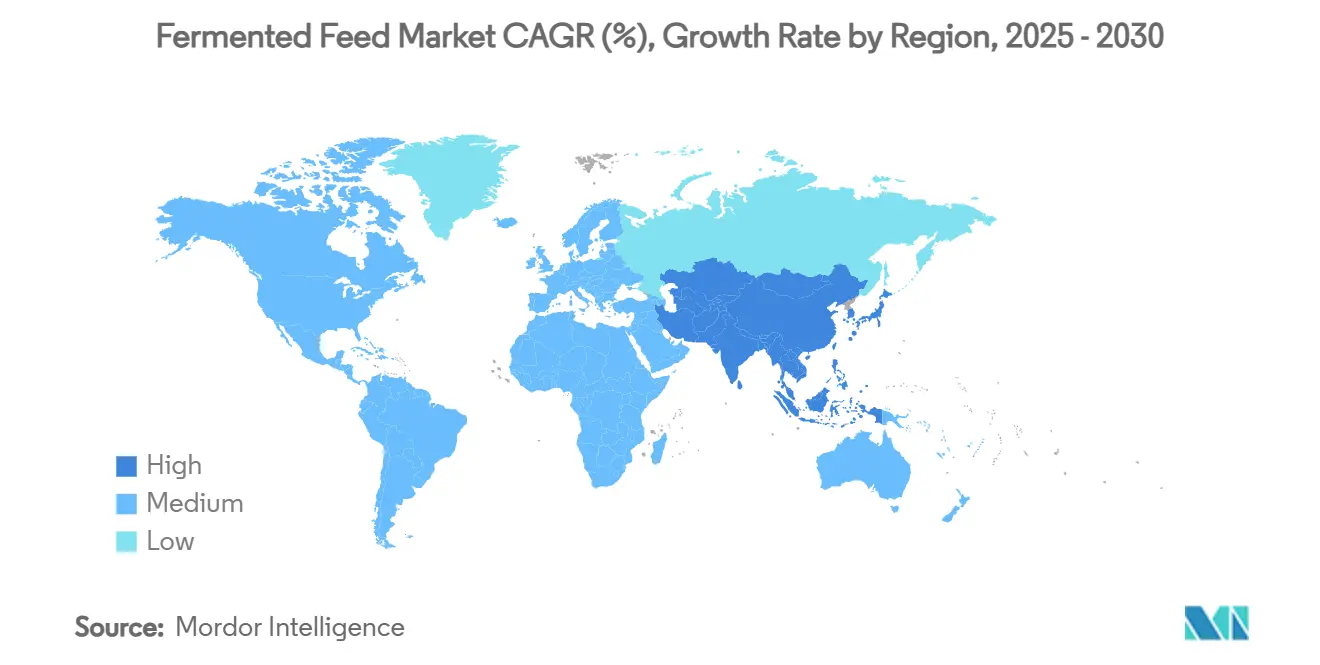

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

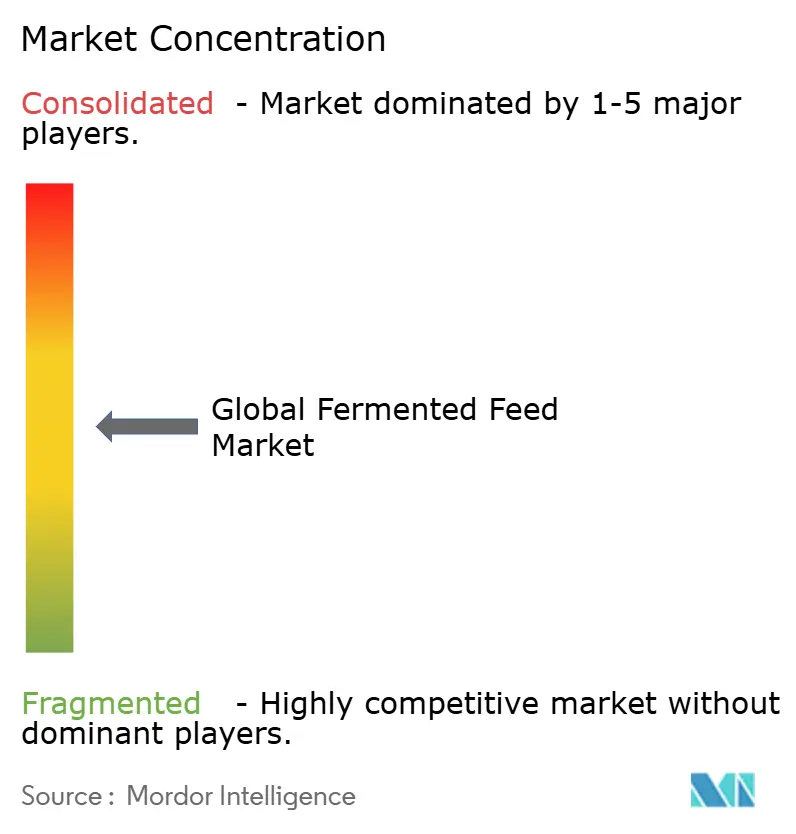

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Fermented Feed Market Analysis by ���ϲ�����

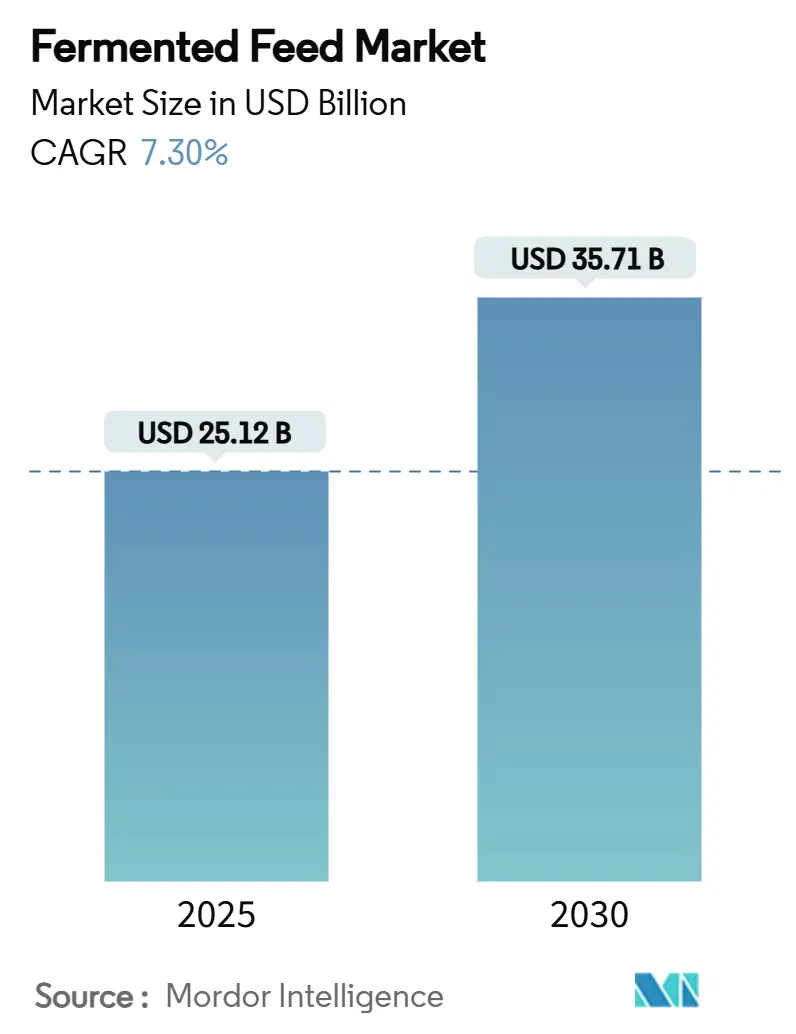

The fermented feed market size is estimated at USD 25.12 billion in 2025 and is projected to reach USD 35.71 billion by 2030, growing at a 7.30% CAGR over the forecast period. Robust demand for antibiotic-free animal protein, the industrialization of livestock production in the Asia-Pacific, and stricter regulations on medicated feed additives are the primary tailwinds propelling the fermented feed market today. Leading producers are channeling capital into advanced fermentation technologies that raise nutrient bioavailability and improve gut health, while circular-economy initiatives are pushing the industry to valorize agri-food by-products as substrates. Competitive intensity is rising as established feed majors acquire fermentation specialists to secure technology and raw-material pipelines, yet sizable white-space remains for niche innovators targeting aquaculture and pet food applications.

Key Report Takeaways

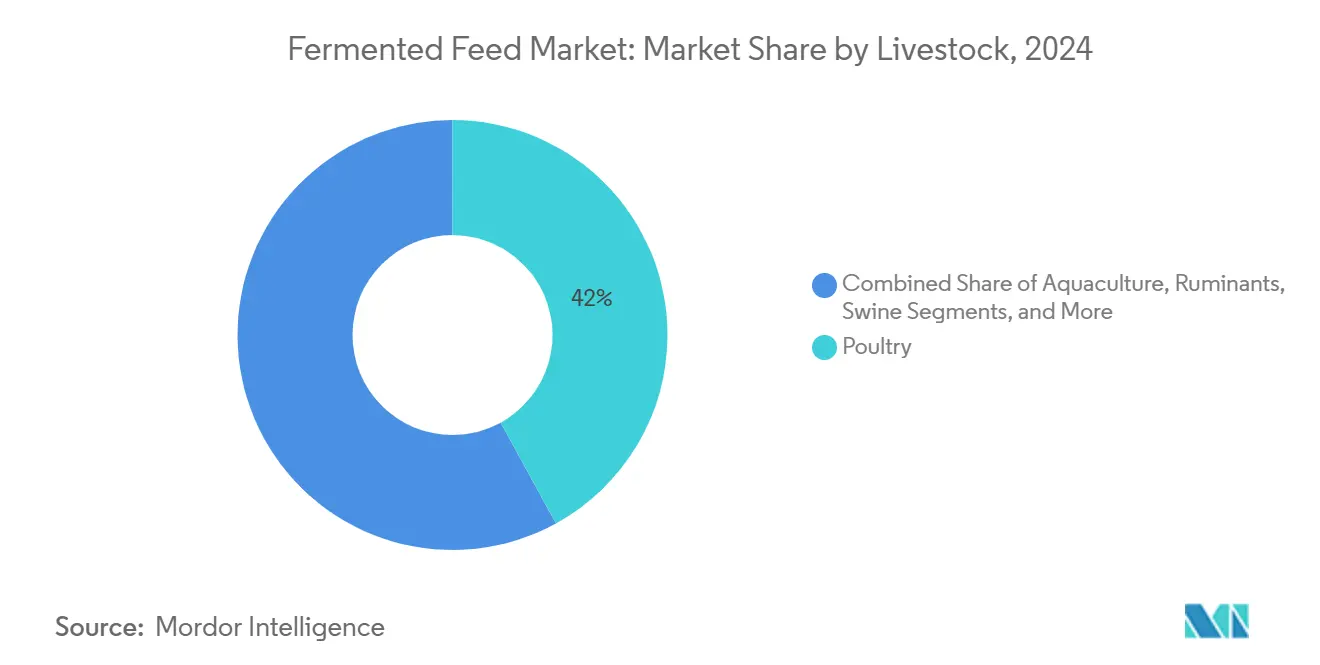

- By livestock, poultry held a 42% fermented feed market share in 2024, and aquaculture is forecast to post the fastest 9.7% CAGR, capturing an outsized slice of the fermented feed market size between 2025 and 2030.

- By substrate, soybean meal commanded 37% share of the fermented feed market in 2024, while by-products are set to climb at a 10.5% CAGR to 2030.

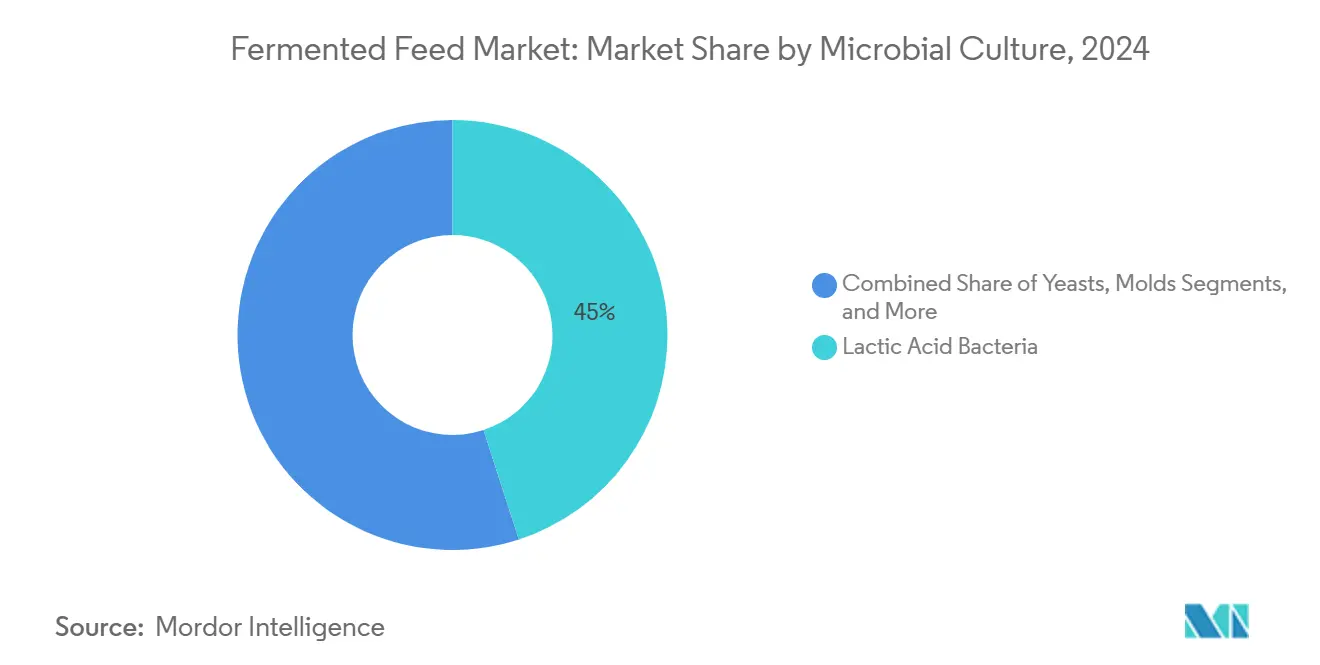

- By microbial culture, lactic acid bacteria led with a 45% market share in 2024, and mixed cultures are projected to accelerate at an 11.3% CAGR across the same horizon.

- By form, dry products dominated 62% of the market size in 2024, whereas liquid formulations are projected to clock a 9.4% CAGR.

- By geography, Europe retained 34% of the market share in 2024, while Asia-Pacific is projected to grow the fastest at a 9.1% CAGR through 2030.

Global Fermented Feed Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Antibiotic-Free Animal Protein | +1.5% | Europe and North America most pronounced | Medium term (2-4 years) |

| Focus on Livestock Gut Health and Feed Conversion Efficiency | +1.2% | Asia-Pacific and North America | Long term (≥ 4 years) |

| Government Limits on Zinc Oxide and Medicated Feed Additives | +0.8% | Europe's core, and expanding globally | Short term (≤ 2 years) |

| Rapid Industrialization of Animal Husbandry in Asia-Pacific | +1.3% | Asia-Pacific core, spill-over to the Middle East, and Africa | Long term (≥ 4 years) |

| On-Farm Solid-State Fermentation Units for Cost Control | +0.6% | North America and Europe lead | Medium term (2-4 years) |

| Upcycling of Agri-Food Waste via Microbial Biotransformation | +0.9% | Asia-Pacific and Europe | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Rising Demand for Antibiotic-Free Animal Protein

Retailer sourcing mandates and the European Union’s Farm to Fork antimicrobial targets are accelerating the fermented feed market, with producers leveraging fermented formulas to sustain animal performance while meeting residue-free standards [1]Source: European Commission, “Farm to Fork Strategy,” EUROPA.EU. Premium pricing on antibiotic-free meat offsets higher feed costs, underpinning profitable adoption. Poultry and swine integrators report commercial-scale success stories that validate fermented feed as a central pillar of antibiotic-replacement strategies, thereby cementing its role in the broader fermented feed market.

Focus on Livestock Gut Health and Feed Conversion Efficiency

Applied and Environmental Microbiology trials show fermented rations improve broiler feed conversion by 8-12% through pre-digestion of starches and proteins, lowering metabolic workload and suppressing enteric pathogens[2]Source: American Society for Microbiology, “Applied and Environmental Microbiology Journal,” ASM.ORG . Feed typically represents 60-70% of total production expense, so a single-digit efficiency gain translates into millions of dollars saved for vertically integrated meat processors. Beyond cost, healthier gut flora reduces veterinary interventions and mortality spikes that accompany heat stress or stocking-density changes.

Government Limits on Zinc Oxide and Medicated Feed Additives

The European Medicines Agency’s 2022 zinc-oxide ban abruptly removed a long-standing gut-health tool for piglets, and similar curbs on tetracycline and colistin premixes are advancing in South Korea, China, and Canada [3]Source: European Medicines Agency, “Zinc oxide: withdrawal of the marketing authorisation in the European Union,” EMA.EUROPA.EU. Chemical-additive pipelines require five to seven years for approval, so livestock companies need immediately deployable biological options. Fermented feed fills that void by delivering lactic acid bacteria and organic acids that stabilize intestinal pH and crowd out pathogens. Early adopters in Denmark cut post-weaning diarrhea cases by 30% within six months of switching, validating performance. Regulatory momentum, combined with proven field outcomes, anchors fermented feed as the default compliance solution across multiple continents.

Rapid Industrialization of Animal Husbandry in Asia-Pacific

China’s average commercial pig farm grew 23% in capacity after 2024 environmental reforms, while India added 6 million metric tons of compound poultry feed capacity in the same period [4]Source: Ministry of Agriculture and Rural Affairs China, “Livestock Industry Development Report,” MOA.GOV.CN. Scaling operations heightens demand for standardized, pathogen-controlled rations, inconsistent backyard formulations are no longer acceptable in vertically integrated supply chains. Fermented feed provides batch-to-batch reliability and mitigates ammonia emissions, an increasingly regulated metric near urban centers. Regional governments also subsidize on-farm fermentation equipment to reduce imported soybean meal dependence. Coupled with rising disposable incomes that support higher-value protein consumption, these structural shifts lock in Asia-Pacific as the fastest-growing theater for fermented feed through 2030.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capex and Opex of Controlled Fermentation Lines | -1.1% | Global, smaller producers hardest hit | Medium term (2-4 years) |

| Batch-to-Batch Variability in Starter Culture Performance | -0.7% | Universal | Short term (≤ 2 years) |

| Mycotoxin Amplification Risks During Anaerobic Fermentation | -0.9% | Tropical regions experience higher impact | Long term (≥ 4 years) |

| Limited Life-Cycle-Assessment Data for Sustainability Marketing | -0.4% | Europe and North America | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

High Capex and Opex of Controlled Fermentation Lines

Building an aerated fermenter battery with clean-in-place systems and inline analyzers costs USD 2-5 million, while specialized operators and quality-assurance labs add 15-25% to annual operating budgets. That investment threshold deters regional mills producing under 100,000 metric tons per year, pushing them toward contract tolling or traditional premixes. Energy prices compound the hurdle, particularly in Southeast Asia, where grid tariffs spiked 18% in 2024. Although compact solid-state systems shrink footprints, financing remains difficult without long-term offtake agreements. Consequently, capital intensity will continue to slow market uptake among small and mid-sized players, trimming roughly 1.1 percentage points from baseline CAGR forecasts.

Batch-to-Batch Variability in Starter Culture Performance

Microbial inoculants are sensitive to temperature swings, substrate moisture, and oxygen ingress, deviations can shift lactic-acid yields by more than 30%. Such inconsistencies translate into fluctuating protein solubility and palatability, forcing livestock producers to adjust feeding programs on the fly. Smaller mills often lack onsite labs to run rapid pH or colony-count tests, discovering quality problems only after animals refuse feed or performance dips. The reputational risk dissuades risk-averse customers from abandoning conventional rations. While DNA-barcode verification and real-time CO₂ monitoring technologies are emerging, their added cost further complicates economics for early adopters, keeping variability a notable brake on market penetration.

Segment Analysis

By Livestock: Aquaculture Drives Premium Growth

Poultry retains leadership with 42% of the fermented feed market size in 2024, supported by its first-mover adoption of antibiotic-replacement strategies. Aquaculture holds the fastest 9.7% CAGR, reflecting the sector’s urgent shift from fishmeal to sustainable alternatives. Fermented feed addresses water-quality challenges in recirculating aquaculture systems, and the segment’s rising share promises to reshape the fermented feed market over the next five years. Swine producers in Europe accelerate uptake in response to zinc-oxide bans, whereas ruminant formulations remain specialized due to rumen-microbiome complexity.

Poultry’s entrenched scale and established supply chains anchor its dominant fermented feed market share, although growth is moderating in mature regions. Conversely, pet-food manufacturers exploit the functional-ingredient appeal of fermented inputs, carving out high-margin niches that further diversify the fermented feed market landscape.

Note: Segment shares of all individual segments available upon report purchase

By Substrate: Waste Valorization Transforms Economics

Soybean meal leads with a 37% fermented feed market share in 2024, yet volatile pricing and sustainability scrutiny impede its growth. By-products clock the strongest 10.5% CAGR through 2030 as feed mills monetize distillers dried grains with solubles, rice bran, and bakery waste. This trend reinforces circular-economy objectives and cushions cost pressures within the fermented feed market. Japan Food Ecology Center’s large-scale food-waste conversion exemplifies profitable substrate diversification and demonstrates scalability.

Corn and wheat continue to hold sizable volumes in fermented feed production but increasingly face competition from human-food and biofuel sectors. As a result, feed manufacturers are diversifying toward more stable and cost-effective by-product streams. This strategic substrate shift enhances supply chain resilience, improves profit margins, and reinforces the fermented feed market’s long-term economic fundamentals and sustainability.

By Microbial Culture: Mixed Systems Enable Innovation

Lactic acid bacteria dominate 45% of revenue, driven by proven safety records, yet mixed cultures propel the highest 11.3% CAGR owing to synergistic metabolite production. Mixed consortia elevate protein digestibility by up to 20% over single strains, catalyzing innovation in the fermented feed market. Yeast solutions gain traction in ruminant diets for fiber digestion, while mold-based systems target enzyme-rich aquaculture feeds.

Intellectual-property filings around mixed-culture formulations underscore a strategic race for technological leadership. Patents increasingly focus on strain selection, co-fermentation techniques, and application specificity. This flurry of innovation reflects intensifying efforts to capture value-added niches, reinforcing competitive stratification and long-term brand differentiation within the global fermented feed market.

Note: Segment shares of all individual segments available upon report purchase

By Form: Liquid Systems Gain Traction

Dry products maintain 62% of the fermented feed market size due to shelf stability and logistics efficiency. Liquid formulations, however, grow at a 9.4% CAGR on palatability benefits and on-farm dosing precision. Automation and bulk-blending equipment in large farms facilitate adoption, but refrigerated storage and shorter shelf life temper uptake among smaller operators. Spray-drying advances that preserve probiotic viability help dry products defend market share against liquid encroachment.

To sustain competitiveness, manufacturers of dry fermented feed are investing in advanced microencapsulation and spray-drying technologies that enhance probiotic survival during processing and storage. These innovations not only extend shelf life but also improve nutrient retention and product consistency, enabling dry formats to retain dominance while addressing performance gaps traditionally favoring liquid formulations in precision livestock nutrition.

Geography Analysis

Europe preserved 34% of the fermented feed market share in 2024, driven by stringent antimicrobial policies and early adopter status. The European Medicines Agency’s zinc-oxide ban accelerated uptake, and the Farm to Fork initiative continues to anchor market expansion. Eastern Europe remains a growth pocket as farms modernize under EU compliance standards.

Asia-Pacific is the growth powerhouse, projected at a 9.1% CAGR to 2030. China’s livestock consolidation and India’s expanding poultry and fish sectors underpin demand. Government incentives for waste recycling bolster by-product fermentation, exemplified by Japanese and South Korean investments in food-waste valorization. Regional acquisitions, such as Easy Bio’s purchase of Devenish Nutrition, underscore strategic interest in fermentation expertise.

North America maintains resilient growth, driven by large integrators emphasizing antibiotic-free positioning and high-margin demand from premium pet food channels. Cargill’s recent mill acquisitions highlight vertical integration into specialty fermented feed. However, entrenched conventional feed practices and sensitivity to commodity prices pose challenges. South America shows steady progress, led by Brazil’s rising protein exports and dsm-firmenich’s new nutrition facility. The Middle East and Africa are gaining momentum, supported by strategic investments such as Saudi Arabia’s Modern Mills expansion worth USD 40 million. These emerging markets continue to broaden the global fermented feed opportunity landscape.

Competitive Landscape

The fermented feed market exhibits moderately fragmented, with the top five companies, Cargill, Incorporated, ADM, Lallemand Inc., dsm-firmenich, and Evonik Industries AG, collectively holding 35.4% of the total market share. These companies leverage extensive R&D capabilities, integrated manufacturing networks, and global distribution infrastructure to reinforce their leadership. Their presence spans multiple regions, enabling consistent supply and responsiveness to evolving feed demands. Together, they shape core market dynamics and set technological and operational benchmarks.

Strategic developments among these leaders emphasize regional expansion and integration. dsm-firmenich has established new facilities in South America to strengthen its reach in high-growth markets. Cargill, Incorporated, continues to expand its global feed operations through acquisitions and internal capacity enhancements. Lallemand Inc. focuses on extending its microbial fermentation expertise across geographies. Evonik Industries AG and ADM invest in fermentation capabilities and animal nutrition platforms to improve cost efficiency and broaden application coverage.

Outside the top five, other global players are also reinforcing their positions through innovation and infrastructure. Nutreco (SHV Holdings) is advancing its capabilities in sustainable feed systems. AB Agri Ltd explores fermentation-driven solutions for enhanced feed efficiency. Alltech, Inc., Novus International, Inc., and AngelYeast Co., Ltd. continue to focus on microbial technologies and fermentation process optimization. Tongwei Co. Ltd. integrates fermentation into its aquafeed strategies to support protein production. Collectively, these players contribute to a more diversified and resilient global fermented feed landscape.

Fermented Feed Industry Leaders

Cargill, Incorporated

ADM

Lallemand Inc.

Evonik Industries AG

dsm-firmenich

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Modern Mills has invested USD 40 million to expand its Al-Jumum feed mill in Saudi Arabia, targeting 422,000 metric tons of annual capacity by 2026. This move boosts regional supply and supports fermented feed adoption through enhanced production scale and alignment with food security goals.

- October 2024: dsm-firmenich has opened a new 100,000 metric tons animal nutrition plant in Sete Lagoas, Brazil, strengthening its production capacity in South America. This expansion supports growing regional demand and reinforces the fermented feed market’s growth through localized, high-scale manufacturing.

- September 2024: Lesaffre has acquired a 70% stake in Biorigin, expanding its yeast-based capabilities in South America. The move enhances its fermentation expertise and supports the fermented feed market through increased control of regional production assets.

Global Fermented Feed Market Report Scope

Fermented feed is animal feed processed using beneficial microorganisms to improve nutrient availability, digestibility, and feed efficiency while supporting gut health in livestock. The Fermented Feed Market Report is segmented by Livestock (Poultry, Swine, Ruminants, Aquaculture, and Others), by Substrate (Soybean Meal, Corn, Wheat, by products and Others), by Microbial Culture (Lactic Acid Bacteria, Yeasts, Molds, and Mixed Cultures), by Form (Dry and Liquid), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The market forecasts are provided in terms of value (USD).

| Poultry |

| Swine |

| Ruminants |

| Aquaculture |

| Other Livestock |

| Soybean Meal |

| Corn |

| Wheat |

| By-products (DDGS, rice bran, etc.) |

| Other Substrates |

| Lactic Acid Bacteria |

| Yeasts |

| Molds |

| Mixed Cultures |

| Dry |

| Liquid |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Livestock | Poultry | |

| Swine | ||

| Ruminants | ||

| Aquaculture | ||

| Other Livestock | ||

| By Substrate | Soybean Meal | |

| Corn | ||

| Wheat | ||

| By-products (DDGS, rice bran, etc.) | ||

| Other Substrates | ||

| By Microbial Culture | Lactic Acid Bacteria | |

| Yeasts | ||

| Molds | ||

| Mixed Cultures | ||

| By Form | Dry | |

| Liquid | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the global fermented feed market?

The fermented feed market size is USD 25.12 billion in 2025.

How fast is the market projected to grow over the next five years?

It is forecast to expand at a 7.3% CAGR, reaching USD 35.71 billion by 2030.

Which livestock segment is growing the quickest?

Aquaculture shows the fastest 9.7% CAGR due to the shift from fishmeal to sustainable feed options.

What are the main obstacles to wider adoption of fermented feed?

High capital and operating costs, starter-culture variability, and mycotoxin control challenges restrain growth.