Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

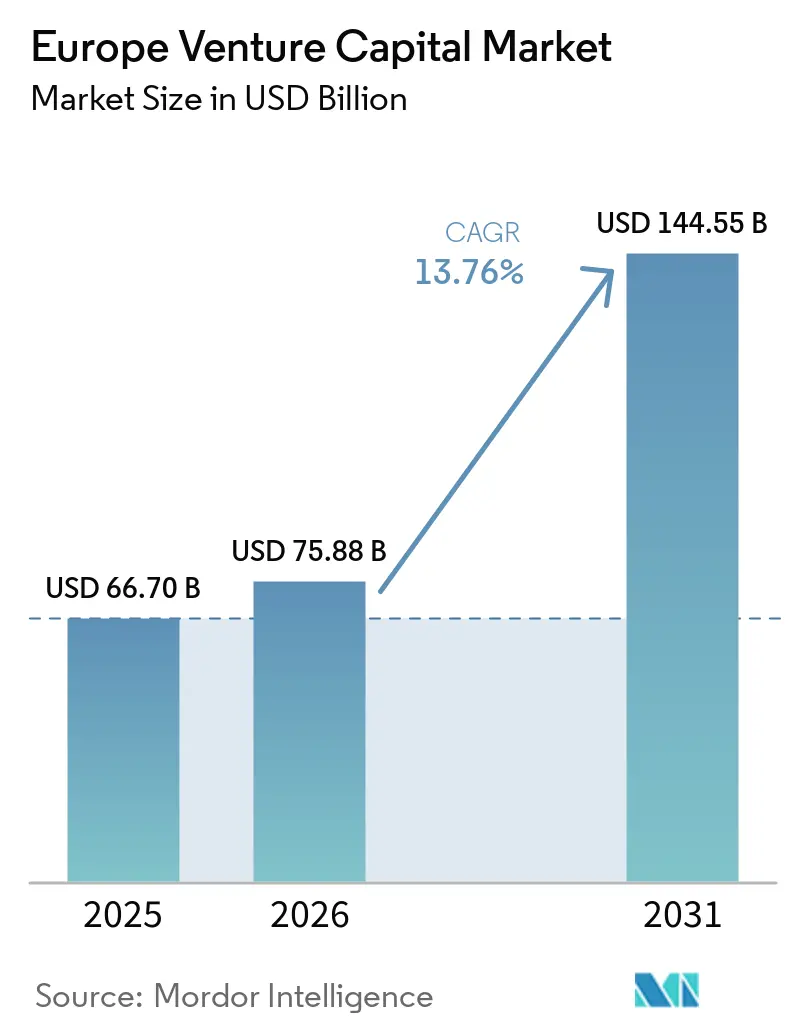

| Base Year Market Size (2025) | USD 66.70 Billion |

| Market Size (2026) | USD 75.88 Billion |

| Market Size (2031) | USD 144.55 Billion |

| Growth Rate (2026 - 2031) | 13.76% CAGR |

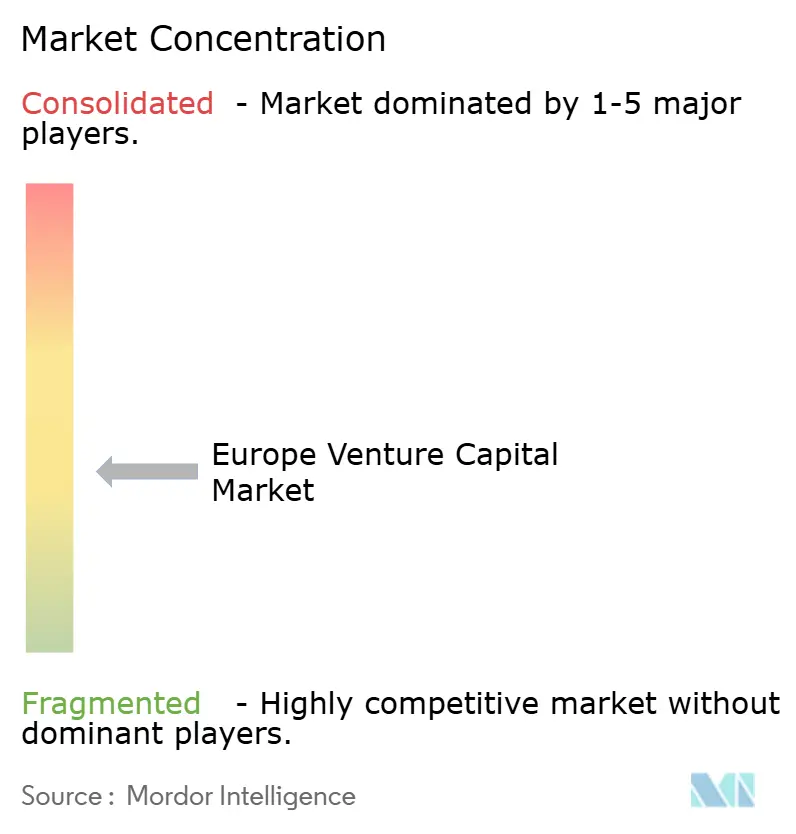

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Europe Venture Capital Market Analysis by ���ϲ�����

The Europe Venture Capital Market size is projected to expand from USD 66.70 billion in 2025 and USD 75.88 billion in 2026 to USD 144.55 billion by 2031, registering a CAGR of 13.76% between 2026 to 2031.

The rebound follows a reset in 2022-2024, with confidence supported by regulatory upgrades that improved access and exit optionality as well as deepening public anchors for late-stage capital. ELTIF 2.0’s adoption increased semi-liquid vehicles and enabled broader distribution, while the EIB Group bolstered growth equity capacity through ETCI 2.0 and a larger technology-finance envelope. Competitive intensity stayed high as international capital accounted for a majority of 2025 allocations and late-stage rounds absorbed more than half of deployed value, which widened the valuation gap between proven scale-ups and seed ventures. The Europe venture capital market is navigating tight exit channels in public markets alongside a healthier private liquidity toolkit that includes secondaries and venture debt, which together improve capital recycling and Distributions to paid-in over time.

Key Report Takeaways

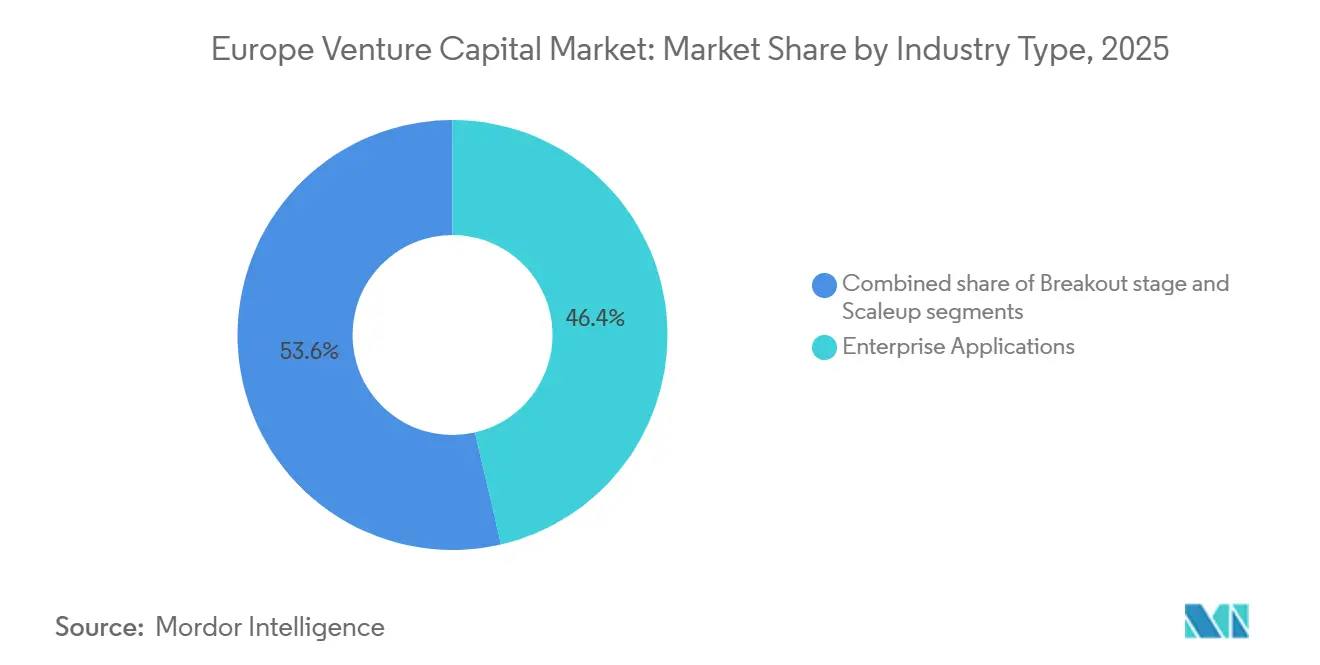

- By industry type, Enterprise Applications led with 46.38% revenue share of the Europe venture capital market in 2025, while Artificial Intelligence is projected to grow at a 14.72% CAGR through 2031.

- By the startup stage, late-stage investing accounted for 56.47% share of the Europe venture capital market in 2025 and is expected to expand at a 10.84% CAGR to 2031.

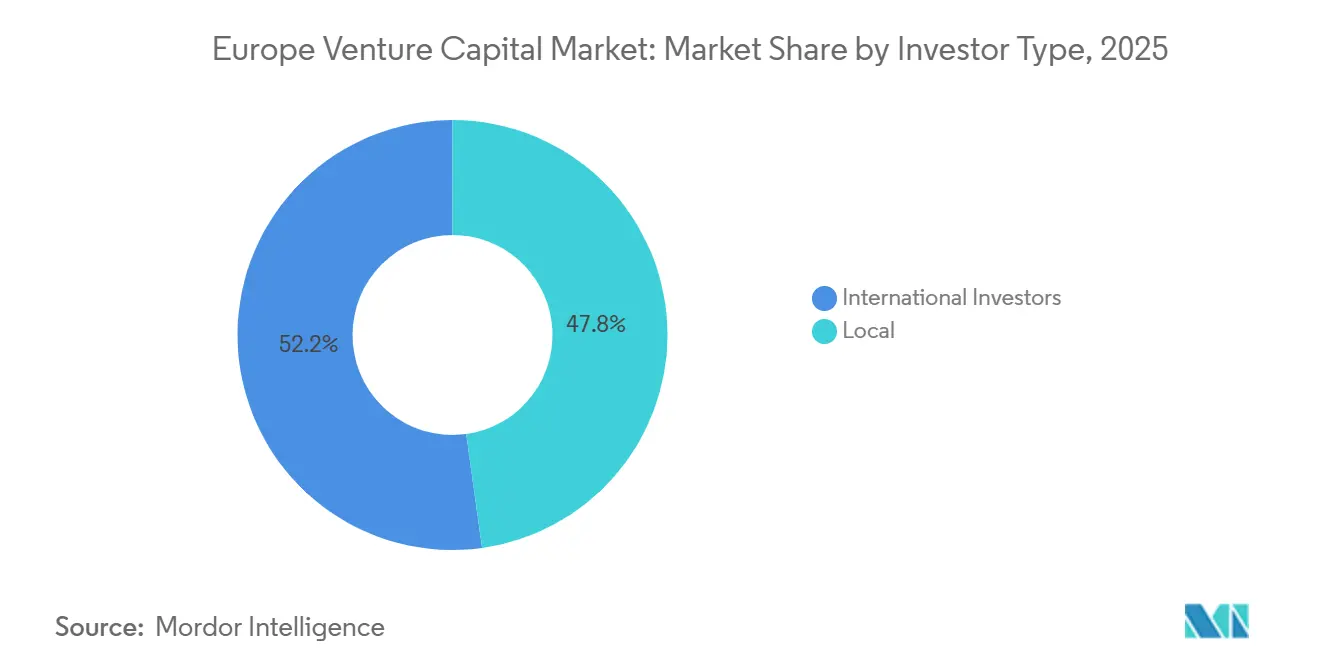

- By investor type, international participants captured 52.19% of the Europe venture capital market in 2025 and are forecast to grow at 9.63% annually through 2031.

- By geography, the United Kingdom held 31.16% share of the Europe venture capital market in 2025, with a 7.28% projected CAGR to 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Venture Capital Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| ELTIF 2.0 enables semi-liquid retail access to VC via evergreen structures and cross-border distribution | +2.3% | Global, with Luxembourg as a hub through pan-European passporting | Medium term (2-4 years) |

| EU Listing Act simplifies follow-on and growth prospectuses, improving exit and re-listing optionality | +1.8% | EU-wide, with strong uptake in the UK, Germany, France, and the Netherlands | Short term (≤ 2 years) |

| EIF and EIB initiatives such as ETCI and TechEU anchor late-stage growth equity within Europe | +2.1% | EU Member States, with deep-tech hubs in Germany, France, and the Nordics | Medium term (2-4 years) |

| AI and deeptech sovereignty agendas expand the investable pipeline including AI, quantum, chips, and dual use | +3.4% | Germany, France, the UK, and the Nordics, with spillovers to CEE manufacturing | Long term (≥ 4 years) |

| Maturing VC secondaries and NAV-based facilities improve DPI and capital recycling | +1.6% | UK, Germany, and France, with secondary hubs in Luxembourg | Medium term (2-4 years) |

| SEPA Instant Payments mandate accelerates fintech rails and B2B payments adoption | +1.4% | Eurozone core, with full coverage extending by July 2027 | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

ELTIF 2.0 Unlocks Institutional-Grade Semi-Liquid Access for Retail Wealth

ELTIF 2.0 took effect in 2024 with changes that broadened the investable scope, added evergreen designs, and removed retail minimums, which together made the vehicle more compatible with wealth-management distribution and cross-border passporting under one wrapper. Luxembourg emerged as the principal domicile, and industry AUM in ELTIFs reached near EUR 20 billion (USD 23.52 billion) by late 2024, indicating a tenfold expansion from pre-reform levels that sustained into 2025 allocations to venture and growth strategies. Managers adopted fund-of-funds designs to blend seed through growth exposure in single vehicles, soften the J-curve, and accommodate periodic subscriptions and redemptions calibrated to NAV and liquidity gates. The regime’s cross-border passport expanded addressable distribution to retail channels in multiple Member States under harmonized rules that reduce duplicative registrations, which supports broader capital formation for the Europe venture capital market. Clarifications from the European Commission in December 2025 resolved issues around redemption gates and capital-maintenance interpretations, which reduced operational uncertainty for semi-liquid designs. The combination of semi-liquidity, simplified retail access, and passport portability is bringing new investor cohorts into the Europe venture capital market, which diversifies LP bases and adds resilience to fundraising cycles.

EU Listing Act Cuts Follow-On Prospectus Burden by Two-Thirds

The EU Listing Act, adopted in October 2024 and entering into force in November 2024, capped follow-on prospectuses at 50 pages, streamlined SME growth-market prospectuses to 75 pages, and lifted the fungible-securities exemption threshold from 20% to 30%, which together compresses time-to-market for issuers and reduces advisory and underwriting costs[1]Editorial Team, “EU Listing Act Package Goes Into Effect,” Mayer Brown, mayerbrown.com . Offer periods are shortened from six to three working days, and PDMR reporting thresholds rose to EUR 20,000 (USD 23,526), which lowers operational workload for management teams and compliance functions at scale-ups preparing secondary offerings[2]Editorial Team, “Prospectus Rule Changes and Market Access,” Covington & Burling, cov.com . National reviews for follow-on prospectuses have trended toward shorter cycles compared with pre-reform baselines, an operational improvement that supports dual-track exit strategies for the Europe venture capital market. Aggregated savings for EU-listed issuers are estimated at EUR 100 million (USD 117.63 million) yearly across compliance overheads, which is meaningful for mid-cap tech companies that rely on periodic top-ups between private financing and full IPO windows. These measures improve exit optionality, particularly for firms that seek to re-list in Europe or to raise bridge capital via lighter-disclosure formats consistent with the Listing Act.

EIF and EIB Deploy EUR 22.4 Billion (USD 26.3 Billion) to Backfill Late-Stage Capital Gaps

The EIB Group expanded technology finance in 2025 with EUR 22 billion (USD 25.8 billion) deployed across equity and venture debt channels to catalyze private capital and support late-stage growth financing, which remains a historic gap in Europe compared with North America. ETCI 2.0 added EUR 1.3 billion (USD 1.5 billion) of commitments in December 2025, scaling from the initial launch in early 2023 and anchoring more mega-funds with mandates to back European scale-ups through late-stage rounds[3]Editorial Team, “TechEU, European Technology Finance Programs,” European Investment Bank, eib.org . EIF anchors extended to country and sector vehicles, such as the EIF commitment to Seaya Growth Tech Fund, which channels capital to deep tech and software scale-ups that require larger follow-on checks. Venture debt expanded in parallel, with the EIB Group accounting for a material share of the European venture-debt market in 2025, which helps companies bridge later rounds and sustain growth before public listings or trade sales. The combined instruments reduce execution risk for large rounds and support the Europe venture capital market as companies scale across multiple countries and need consistent financing partners. The broader public-private architecture also aims to keep IP and job creation rooted in Europe by anchoring funds and rounds that might otherwise be led offshore.

AI and Quantum Sovereignty Mandates Expand Deeptech Pipelines

Europe’s deeptech agenda emphasizes sovereign capabilities across AI, quantum, and enabling hardware such as semiconductors, which shapes multi-year pipelines for venture investment and corporate adoption in regulated sectors. The European Quantum Strategy, published in July 2025, mapped a path for global quantum markets to expand substantially by 2040 and documented more than EUR 11 billion (USD 12.9 billion) of cumulative EU and Member State public investment in recent years, including pilot lines in multiple countries. The talent pipeline is also a focus, including new skills academies and research infrastructure, which supports a more durable Europe venture capital market in deeptech. VC platforms and ecosystem partners reported rising allocations to robotics, applied AI, and frontier materials that can deliver near-term productivity while maintaining strategic alignment with sovereignty objectives. Sovereign-aligned mandates and public anchors crowd in private capital at key inflection points, narrowing the late-stage funding gap and lifting confidence to scale in sensitive sectors. The policy-instrument mix signals long-horizon support, encouraging founders and investors to plan around multi-year product cycles and regulatory certification paths in areas such as quantum encryption and safety-critical AI.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Exit bottlenecks and uneven late-stage liquidity despite reforms | -1.9% | EU-wide, most acute in Southern Europe and parts of CEE | Short term (≤ 2 years) |

| AIFMD II adds LMTs and loan-originating fund rules, raising compliance and operating burden | -1.2% | EU Member States, with higher friction for smaller AIFMs in key domiciles | Medium term (2-4 years) |

| Tightening FDI screening and export controls elevate clearance risk for sensitive tech | -0.9% | Germany, France, the Netherlands, and Nordics, with EU-wide application by 2027 | Long term (≥ 4 years) |

| EU AI Act obligations increase time-to-market and capital intensity for high-risk and GPAI | -1.5% | EU-wide, with highest costs in deeptech hubs with large AI exposure | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Exit Bottlenecks Persist Despite Dual-Track Reforms

IPO activity for European VC-backed companies reached decade lows in 2025, which constrained distributions and extended holding periods in many portfolios despite the Listing Act’s simplifications for follow-ons and growth prospectuses. M&A accounted for the significant majority of venture-backed exits by volume, yet the concentration in fewer, larger transactions left many mid-tier assets waiting for better pricing or clearer strategic buyers. Flagship flotations such as Klarna’s 2025 New York listing showed that some European scale-ups continue to prefer deeper U.S. liquidity and research coverage when public-market sentiment is fragile in Europe. The friction is highest in sensitive technologies, where additional regulatory clearances apply and national screenings can extend transaction timing and certainty to close. Uneven late-stage liquidity pushes GPs to reserve more capital for follow-ons, which tightens availability for seed and Series A across the Europe venture capital market during recovery phases. Taken together, these conditions lengthen time-to-exit and compress expected DPI, which keeps fundraising selective around managers with repeatable distribution strategies in tough markets.

AIFMD II Liquidity Rules Add Operational Friction for Loan-Originating Funds

AIFMD II introduces leverage caps for loan-originating AIFs, concentration limits, and mandated liquidity-management tools for open-ended structures, with a key application date in April 2026 that requires systems, policy updates, and periodic stress testing. ESMA’s technical standards further define the compatibility of open-ended funds with liquidity risk frameworks and require the selection of at least two LMTs, such as redemption gates or swing pricing, which will influence product structuring in private credit and venture-debt strategies. Transitional relief applies to older funds that close to new capital, but newer vehicles or those still fundraising must meet the 2026 compliance date, which accelerates operating-expenditure plans for smaller managers. Standardized stress testing can improve systemic resilience, yet poorly calibrated LMTs risk amplifying outflows if multiple funds activate gates in a stress period, which adds complexity for investors assessing liquidity and pricing during redemptions. Managers who use venture debt to bridge equity rounds will likely prefer closed-end structures that are less exposed to redemption dynamics, which influences the design of future fund vintages in the Europe venture capital market. The operational burden is manageable for large platforms with dedicated teams, but it creates a barrier for emerging managers without scale.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Industry Type: AI Displaces Enterprise SaaS as Primary Growth Vector

Enterprise Applications accounted for 46.38% of allocations in 2025, while Artificial Intelligence is projected to grow at a 14.72% CAGR through 2031, signalling a rotation in growth leadership within the Europe venture capital market. These balances reflect ongoing preference for predictable B2B software revenue alongside rising conviction in actionable AI that supports regulated workflows and measurable efficiency gains. European public anchors in technology finance and late-stage equity formation are reinforcing the deeptech pipeline, allowing AI companies to progress toward robust scale-up paths in local markets before pursuing global expansion. Quantum roadmaps that include skills programs and pilot lines indicate that strategic hardware and security-adjacent opportunities will continue to feed the investable universe for venture and growth investors beyond AI software. The Europe venture capital market is also evolving to support industrial automation and safety-critical deployments, which often demand certifications and longer implementation cycles that suit specialized investors. Corporations are active co-developers and buyers of AI and automation solutions, creating predictable demand for later-stage rounds when integration milestones are met. Funding structures are therefore more staged and milestone-driven than in prior cycles, which aligns with the governance needs of regulated sectors. The Europe venture capital industry is adapting deal terms and syndicate composition to reflect these realities, balancing technical risk and commercialization timelines in AI and related deeptech domains.

Segment momentum for AI is shaped by a combination of public-program anchors, corporate procurement, and founder talent density that continues to deepen across leading hubs, which together sustain the Europe venture capital market’s confidence in AI as the primary growth vector. Enterprise Applications remain a core allocation pool as midmarket and large companies modernize data, security, and workflow stacks, while AI-native features reshape product maps across sales, support, and operations. Late-stage capacity from ETCI and other EIB Group programs increases the probability of durable scale in both Enterprise Applications and AI, which supports a more complete funding escalator that the region lacked in earlier cycles. As stakeholders internalize the EU AI Act’s obligations, portfolio companies that excel at compliance can stand out in tenders and regulated-enterprise sales, which may influence internal capital rotation across software subsectors over time. With this context, Enterprise Applications can continue to attract steady allocations while AI takes the lead in expected growth for the Europe venture capital market. Where sector-level market-share data is discussed, Enterprise Applications held the largest slice of the Europe venture capital market share in 2025, while AI held the top projected growth rate to 2031.

By Startup Stage: Late-Stage Barbell Squeezes Seed and Series A Availability

Late-stage investing represented 56.47% of allocations in 2025 and is projected to increase at a 10.84% CAGR to 2031, underscoring a barbell structure in the Europe venture capital market that favours scale-ups with proven traction. The tilt reflects LP and GP priorities around capital preservation, unit economics, and quicker paths to liquidity, which remain central as IPOs lag and M&A remains the main exit route. The expanded public toolkit, including ETCI 2.0, helps sustain very large rounds, while the EIB Group’s venture-debt platform adds another track that companies can use to reach the next financing milestone or to prepare for exit. Early-stage ecosystems continue to adapt with sharper proof points for Series A, which encourages leaner build cycles and faster validation of sales motion and gross margin. In this environment, larger syndicates lean on co-investment with corporates for strategic fit, while specialist funds lead on due diligence in regulated markets. As exit conditions improve, reserve planning can normalize, which would support healthier capital availability for seed and Series A across the Europe venture capital market. In the interim, managers with strong networks, early customer references, and compliance maturity can differentiate in competitive late-stage processes.

Portfolio construction at the platform level now frequently anticipates further reserve needs in 2026 and 2027, which increases selectivity at seed and Series A during 2026 planning cycles. Sponsors also expect more structured use of secondary and NAV financing to support partial liquidity and to free capital for new deployments without sacrificing ownership in top-performing assets. This architecture reduces pressure for forced exits, which should improve DPI as exit channels open, and that would benefit upstream allocations into seed and early-stage strategies in the Europe venture capital market. At the same time, late-stage concentration implies stronger competition for category leaders and a higher bar for rounds sized above EUR 100 million (USD 117.63 million), which requires meticulous preparation on governance, compliance, and operating metrics. By startup stage, late-stage investing held the largest portion of the Europe venture capital market share in 2025, and it carries the top projected growth rate among stages to 2031. Funds that align operating support and regulatory readiness to these dynamics can command more favourable access and maintain higher win rates.

By Investor Type: International Capital Commands Majority Share Amid Domestic LP Retrenchment

International participants held 52.19% of allocations in 2025 and are forecast to grow at 9.63% through 2031, which highlights Europe’s dependence on cross-border pools of capital to close late-stage rounds in the Europe venture capital market. This structure brings benefits in larger checks, sector specialization, and global network effects for expansion, yet it also concentrates ownership and exit decision-making outside Europe in some cases. Europe’s public anchors at the fund and company levels are intended to balance these outcomes by crowding in co-investment and encouraging onshore decision centres for strategic IP. Corporate venture capital from European industrials, healthcare, and semiconductor leaders continues to complement international participation in strategic areas, which helps late-stage companies find commercial pathways. Secondary specialists and continuation vehicles led by global sponsors remain active liquidity providers, purchasing positions from time-constrained LPs and enabling GPs to hold assets longer, which adds stability to syndicates that include foreign participants. As more domestic LPs expand their private-market exposure in 2026 and 2027, the Europe venture capital market could see a gradual rebalancing between international and local investors. Until then, global allocators continue to shape the most competitive later-stage processes and influence governance models at scale-ups.

Investor-type dynamics also influence fundraising cadence and co-lead patterns across hubs, with global growth funds and sovereign vehicles often setting round pace and valuation references in 2026 plans. European platforms that build credible transatlantic and pan-Asia partnerships can better syndicate large raises while keeping core decision rights and governance onshore. At the early stage, locally anchored seed funds and accelerators remain critical for founder pipelines and talent density, while late-stage syndicates expand investor type diversity in the Europe venture capital market. As regulatory regimes in AI and financial services mature, sophisticated operating support on compliance becomes a factor in winning deals, which favors investors with platform resources aligned to new obligations. The interplay among international capital, corporate venture, and public anchors is therefore central to investment velocity and exit readiness in 2026 and beyond.

Geography Analysis

The United Kingdom retained 31.16% of allocations in 2025 and is projected to grow at a 7.28% CAGR to 2031, which keeps it the single largest national ecosystem in the Europe venture capital market. Germany and France maintain strong momentum as late-stage capacity expands and sector mandates in deeptech attract both domestic and cross-border interest. Across these core markets, corporate innovation agendas and public anchors create depth for scale-ups, an important difference from the last cycle, when many growth rounds migrated offshore. The regulatory environment is also maturing, with the EU Listing Act easing follow-on raises for listed firms considering dual-track options, which influences exit strategy design across national hubs. These improvements matter in 2026 planning as the Europe venture capital market weighs IPO readiness, liquidity windows, and sponsor appetite for secondaries.

Germany’s policy instruments include support for scale-ups and frontier technologies that complement market-led capital formation, which strengthens later-stage depth and reinforces sector clusters with industrial partnerships. France’s institutional ecosystem combines public financing capacity with private platforms across enterprise software, health, and AI, aligning with the EU AI Act’s compliance framework to position vendors for regulated sales. The UK maintains strengths in fintech, AI, and life sciences, with late-stage interest from global investors and corporates that prize engineering talent and European enterprise adoption routes. Scandinavia and the Netherlands contribute resilient hubs with high digital adoption and global customer reach, aided by strong corporate involvement in industrial innovation and electrification, which supports the Europe venture capital market’s geographic diversity. With cross-border passporting and pan-European vehicles expanding, national hubs benefit from more cohesive fundraising and distribution mechanics in 2026.

Southern Europe and parts of CEE face thinner late-stage depth and more pronounced exit timing risks, especially in sensitive technologies that require multi-jurisdictional FDI screens, which can elongate diligence and slow deal closure. These markets continue to benefit from pan-European funds and sovereign co-investment programs that aim to avoid permanent stratification, which supports earlier-stage company formation and bridges to later-stage syndicates in the Europe venture capital market. Real-time payments adoption will also improve B2B fintech infrastructure and embedded financial services across Eurozone markets by 2027, aligning product roadmaps with instant rails and improving working-capital dynamics for SMEs. As more hubs internalize Listing Act benefits and AI Act obligations, portfolio companies can plan for exits and compliance in a more predictable way, which should support improved pacing across geographies in 2026 and 2027. Within these parameters, the Europe venture capital market size will reflect stronger multi-country syndication and more balanced co-leadership between local and international investors as core markets continue to mature.

Competitive Landscape

Competitive intensity within the Europe venture capital market is elevated at late stage and more selective in early stage, with top hubs accounting for a majority of deployed value but with no single manager holding a dominant share, which indicates a moderately fragmented ecosystem. Multi-stage platforms continue to pursue sector-agnostic deal flow from seed through Series C, while specialist investors focus on deeptech, healthcare, and industrial software with tailored operating and compliance support. Strategic moves by leading firms in 2024 and 2025 strengthened their fundraising capacity and operating reach, a trend that carries into 2026 positioning for larger European rounds. Balderton announced USD 1.3 billion across new early and growth funds, reinforcing its multi-stage presence on the continent. Atomico completed a USD 1.24 billion dual-fund raise to support both early and growth investments, increasing its ability to support portfolio companies across multiple rounds. Eurazeo opened a Stockholm office to deepen Nordic coverage and support pan-European evergreen vehicles that seek retail and wealth-manager distribution.

Investors with strong operating platforms in legal, talent, finance, and sustainability are becoming more competitive in winning founder allocations, as regulatory complexity increases the value of post-investment support in areas such as AI Act documentation and FDI readiness. Secondary and continuation vehicles backed by global institutions offer portfolio-liquidity solutions that can reduce GP exposure to elongated hold periods, which improves DPI optics and supports fundraising continuity for seasoned platforms. Late-stage round competition remains intense as corporate venture programs and international growth funds target the same category leaders in AI, healthcare, and industrial software, which raises the bar on governance, go-to-market, and data room quality. Firms that differentiate on operating value, co-commercial partnerships, and compliance structuring show higher win rates in contested processes across the Europe venture capital market.

Cross-border expansion remains a priority, with European platforms increasing on-the-ground coverage to source, diligence, and support companies in high-density hubs. OTB Ventures expanded in Luxembourg to strengthen its coverage in Benelux and France for deeptech mandates, demonstrating the value of proximity to founders and partners in multi-country markets. EQT Life Sciences advanced late-stage healthcare exposure through selected co-leads, supporting clinical-stage programs and building lines of sight to global approvals and commercialization pathways. These moves signal continued maturity in platform capabilities, which aligns with founder expectations as the Europe venture capital market transitions from recovery to a new growth phase in 2026 planning.

Europe Venture Capital Industry Leaders

Index Ventures

Accel

Balderton Capital

Northzone

Atomico

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: UK autonomous-vehicle startup Wayve raised USD 1.5 billion in a Series D round led by Eclipse with participation from Balderton Capital and SoftBank, reaching an USD 8.6 billion valuation and representing one of Europe's largest AI infrastructure raises, positioning the company to scale its global autonomy platform across OEM partnerships in North America and Asia.

- January 2026: EQT Life Sciences co-led a EUR 51 million (USD 60 million) Series B in Heidelberg-based Exciva to advance its Alzheimer's therapy into Phase 2 clinical trials across the EU, United States, and Canada, with Philip Scheltens joining Exciva's Board as Director and demonstrating sustained institutional appetite for neurodegenerative therapeutics despite biotech sector volatility.

- November 2025: Eurazeo opened a Stockholm office led by Managing Director Katrin Boström to strengthen Nordic and UK investor relations, operational support for portfolio companies, and fundraising for two pan-European Evergreen funds targeting Swedish individual investors.

- March 2025: OTB Ventures launched a Luxembourg office and added senior hires to increase deal flow in Benelux and France for its pan-European deeptech investment mandate across robotics, space tech, enterprise automation, and AI.

Europe Venture Capital Market Report Scope

Venture capital is a form of private equity financing that is provided by venture capital firms or funds to startups, early-stage, and emerging companies that have been deemed to have high growth potential or which have demonstrated high growth.

A complete background analysis of the Europe venture capital market, which includes an assessment of the parental market, emerging trends by segments, and regional markets. Significant changes in market dynamics and market overview are also covered in the report.

The Europe Venture Capital Market is segmented by investments in country (UK, Germany, Finland, Spain, and Others), by the size of the deal (angel/seed investing, early-stage investing, and late-stage investing), and by the industry of investment (fintech, pharma & BioTech, consumer goods, industrial/energy, IT hardware & services, and other industries).

By Industry Type

| Fintech |

| Pharma and Biotech |

| Consumer Goods |

| Industrial/Energy |

| IT/Hardware and Services |

| Other Industries |

By Startup Stage

| Angel/Seed Investing |

| Early Stage Investing |

| Later Stage Investing |

By Investor Type

| Local |

| International |

By Geography

| United Kingdom |

| Germany |

| France |

| Sweden |

| Netherlands |

| Spain |

| Rest of Europe |

| By Industry Type | Fintech |

| Pharma and Biotech | |

| Consumer Goods | |

| Industrial/Energy | |

| IT/Hardware and Services | |

| Other Industries | |

| By Startup Stage | Angel/Seed Investing |

| Early Stage Investing | |

| Later Stage Investing | |

| By Investor Type | Local |

| International | |

| By Geography | United Kingdom |

| Germany | |

| France | |

| Sweden | |

| Netherlands | |

| Spain | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current size and growth outlook for the Europe venture capital market?

The Europe venture capital market size reached USD 66.70 billion in 2025 and is forecast to reach USD 144.55 billion by 2031 at a 13.76% CAGR over 2026-2031.

Which segments lead by share and growth within the Europe venture capital market?

Enterprise Applications held 46.38% share in 2025, while Artificial Intelligence is projected to grow at 14.72% CAGR through 2031.

How are late-stage dynamics shaping capital allocation in Europe?

Late-stage investing represented 56.47% of allocations in 2025 and is projected at a 10.84% CAGR to 2031, supported by ETCI 2.0 and EIB venture-debt capacity that reduce execution risk for larger rounds.

What policy changes are most relevant for exits and liquidity in 2026?

The EU Listing Act shortens prospectus formats and timelines for follow-ons and SME growth offerings, and a maturing secondaries market with rising NAV marks improves capital recycling and DPI.

How will the EU AI Act affect venture-backed AI companies in Europe?

The Act imposes high-risk and general-purpose AI obligations covering risk management, data-governance, documentation, conformity assessment, and human oversight, which increases near-term capital needs but can create trust advantages in regulated sectors.

Which geography holds the largest share of the Europe venture capital market?

The United Kingdom held 31.16% of 2025 allocations, with a 7.28% projected CAGR through 2031, while Germany and France show strong recovery momentum supported by public anchors and sector mandates.

Page last updated on: