Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 59.12 Billion |

| Market Size (2026) | USD 61.70 Billion |

| Market Size (2031) | USD 76.43 Billion |

| Growth Rate (2026 - 2031) | 4.37% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. |

|

Europe Used Car Market Analysis by ���ϲ�����

The European used car market size is expected to grow from USD 59.12 billion in 2025 to USD 61.7 billion in 2026 and is forecast to reach USD 76.43 billion by 2031 at a 4.37% CAGR over 2026-2031. Digital marketplaces, OEM-backed certified pre-owned (CPO) programs, and embedded finance solutions together accelerate demand by improving price transparency, trust, and affordability. Cross-border inventory flows unlock incremental volume as diesel phase-out policies in Western Europe redirect vehicles to Central and Eastern Europe. The mid-age supply wave of 3- to 5-year-old ex-lease cars offsets persistent shortages of younger stock, while battery-electric vehicles (BEVs) add a fast-growing premium layer despite valuation uncertainty. Competitive intensity is rising as traditional dealers, digital disruptors, and OEM captive channels pursue omnichannel models that blend online research with showroom or delivery hand-offs, reshaping margins and customer ownership cycles.

Key Report Takeaways

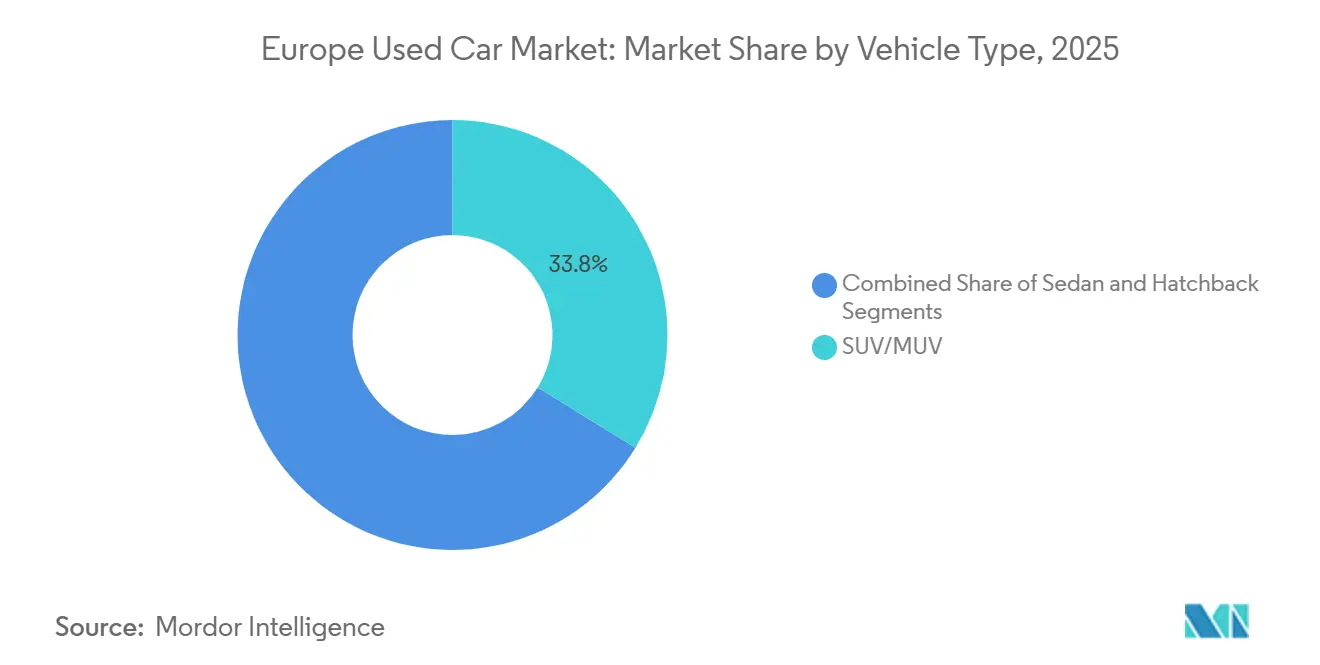

- By vehicle type, SUV/MUV models captured 33.78% of the European used-car market share in 2025; BEV-compatible SUVs are advancing at a 9.67% CAGR through 2031.

- By fuel type, diesel retained 41.52% of the European used-car market share in 2025; BEVs posted the fastest growth at a 17.95% CAGR over 2026-2031.

- By vendor type, the unorganized channel held 54.60% of the European used-car market share in 2025, whereas the organized channel grew at a 6.18% CAGR through 2031.

- By sales channel, offline routes still accounted for 87.35% of the European used-car market share in 2025; online transactions are scaling fastest at a 16.35% CAGR through 2031.

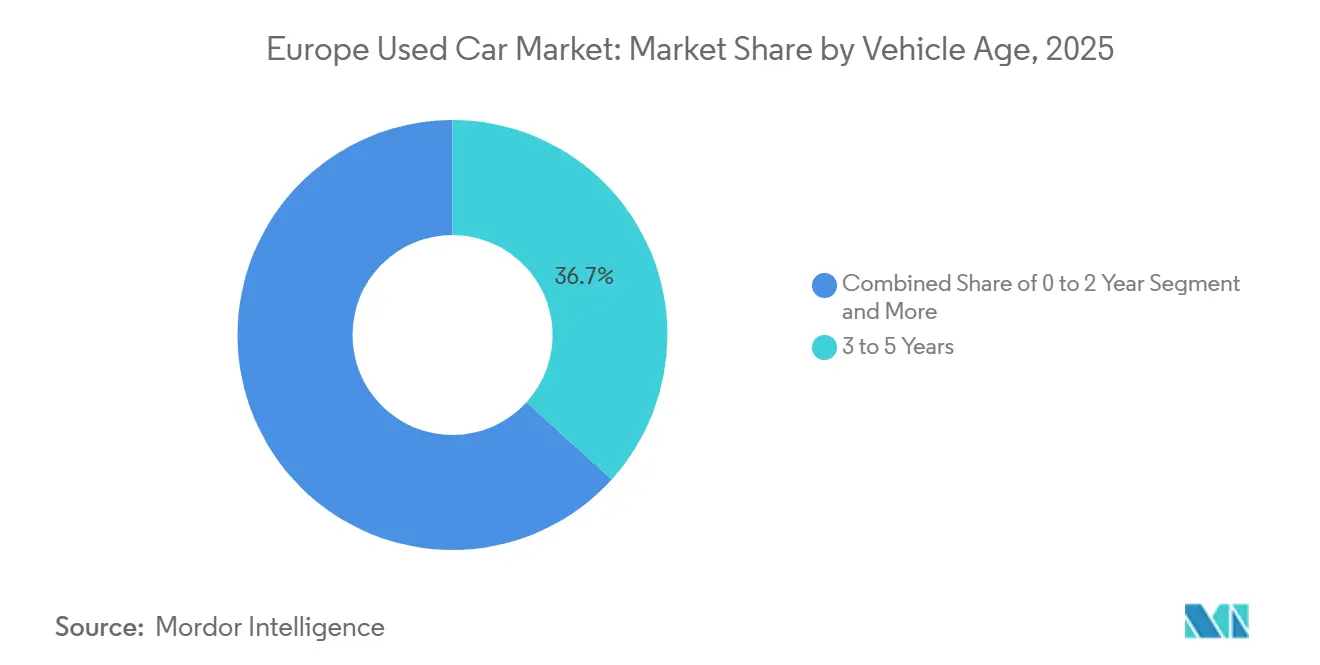

- By vehicle age, the 3 to 5 years bracket accounted for 36.72% of the European used car market share in 2025; the 0 to 2 years cohort is expanding at a 10.84% CAGR through 2031.

- By ownership count, single-owner cars accounted for 61.55% of the European used-car market share in 2025; multi-owner units are trending upward at a 5.31% CAGR through 2031.

- By price band, the USD 10k to 20k range held 40.62% of the European used-car market share in 2025, while the more than USD 30k tier is growing at a 9.71% CAGR through 2031.

- By finance type, outright purchases dominate with a 60.92% of the European used car market share in 2025, while the financed purchase segment, though currently at 8.66%, is the fastest-growing by CAGR through 2031.

- By country, Germany led with 17.85% of the European used-car market share in 2025, while Poland is forecast to expand at a 7.42% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Used Car Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| OEM-Backed CPO Program Surge | +1.2% | Germany, UK, France | Medium term (2–4 years) |

| Ex-Lease Vehicle Supply Rises With Fleet Electrification | +1.1% | Germany, Netherlands, Sweden | Short term (≤ 2 years) |

| Online Marketplaces Drive Digital Growth | +0.6% | UK, Germany, France | Medium term (2–4 years) |

| WLTP/Euro-7 Push Widens New-Used Price Gap | +0.5% | EU-wide | Short term (≤ 2 years) |

| Diesel Phase-Out Spurs Cross-Border Trade | +0.4% | Germany, France to Eastern Europe | Medium term (2–4 years) |

| Embedded Finance & BNPL Boost Affordability | +0.3% | UK, Germany, Spain | Medium term (2–4 years) |

| Source: ���ϲ����� | |||

���ܰ�������������������-�����������������پ��ھ�������ʰ���-���ɲԱ����(��ʰ�)���ʰ��Dz���������

OEM CPO schemes inject manufacturer warranties, refurbishment standards, and digital booking tools into the resale journey, positioning near-new cars as credible substitutes for new models. Strong residuals and higher per-unit profitability motivate brands to mainstream CPO in core planning. Consumer awareness, however, remains muted; ongoing education initiatives by dealer councils in Germany and the UK aim to translate technical coverage into clearer value messaging. Effective programs also loop owners back into authorized service lanes, reinforcing accessory and maintenance revenue streams across the ownership lifecycle[1]Stowe, Andrew, "CPO Programs Benefit OEMs, Dealers and Buyers," WardsAuto, wardsauto.com.

�龱�����Բ������ܱ��������Ǵ�������-���������ձ���������(3–5-�۱���������������)���ٰ������������������������������ٰ����ھ������پ��Dz����Ѳ��Ի岹�ٱ��

The influx of off-lease vehicles, especially in the 3–5-year age bracket, is significantly reshaping inventory dynamics across the European used-car market, presenting both challenges and opportunities for dealers, fleet operators, and financiers. Corporate fleet electrification mandates are accelerating this shift, as organizations cycle vehicles more quickly to meet sustainability goals and to incorporate the latest technology, including battery-electric and hybrid models. The supply increase is most pronounced in countries with high leasing penetration, such as Germany and the Netherlands, where leasing remains a dominant acquisition route for BEVs. This trend is creating a more competitive market for nearly new vehicles, driving dealers to optimize remarketing strategies, invest in certification programs, and leverage digital sales channels to maintain margins and manage stock efficiently.

�Ұ��Ƿɳٳ����Ǵ����ʳܰ���-�ʱ����������Ա����Ա����Ѳ������ٱ��������������Գ��������Բ����پ������ٲ������ʱ�Ա�ٰ����پ��Dz�

Digital transformation is reshaping the European used car market, with online platforms expected to grow rapidly and capture up to 10% of the B2C segment by 2025. This expansion is driven by evolving consumer preferences for seamless purchasing experiences, greater pricing transparency, and convenience. Pure-play online marketplaces are addressing traditional friction points through innovations such as digital vehicle inspections, algorithmic price guidance, and doorstep delivery services. Success in this evolving landscape depends on building trusted brands, leveraging data analytics for inventory and pricing decisions, integrating online and physical touchpoints, operating efficient refurbishment and inspection centers, and diversifying sourcing channels to maintain a broad and high-quality vehicle supply. These strategies collectively enable dealers and digital operators to meet modern buyer expectations while scaling efficiently across multiple European markets.

�����𱹲��ٱ���������-�䲹�����ʰ�����������ڰ��dz����³��ձ�/���ܰ���-7����dz���������Գ������¾����Ծ��Բ����ʰ����������Ҳ������ٴ����������

Implementing stringent emissions standards, particularly the Worldwide Harmonized Light Vehicles Test Procedure (WLTP) and the upcoming Euro-7 regulations, has significantly increased new-vehicle production costs and retail prices. This widening price gap between new and used vehicles redirects consumer demand toward the secondary market, especially in price-sensitive segments. This price disparity creates opportunities for dealers to position nearly-new used vehicles as value alternatives to factory-fresh models.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Odometer Fraud Undermines Buyer Trust | -0.9% | Eastern Europe, Italy, Spain | Medium term (2-4 years) |

| Fragmented Tax Rules Hinder Cross-Border Trade | -0.7% | EU-wide | Long term (≥ 4 years) |

| Slow EV Battery Standards Hurt Used BEV Values | -0.5% | EU-wide | Medium term (2-4 years) |

| Quality Concerns in Older Vehicles | -0.4% | Eastern Europe, Southern Europe | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

�ʱ���������پ��Բ�������dz���ٱ����������ܻ������Ի��������Ծ��Բ������ܲ������հ��ܲ���

Odometer fraud remains a persistent challenge in the European used car market, undermining consumer confidence and reducing resale values across affected segments. By artificially lowering reported vehicle mileage to inflate sale prices, this practice costs European consumers billions of euros each year. It poses particular risks in cross-border transactions, where verification is more difficult. The issue is especially pronounced in Eastern Europe, Italy, and Spain, where regulatory oversight and enforcement differ widely. Emerging digital solutions, such as blockchain‑based vehicle history records and centralized mileage registries, offer potential to improve transparency and reduce fraud. Still, adoption and implementation remain uneven across the continent. Strengthening harmonized regulatory standards and incentivizing technology integration are, therefore, critical to restoring trust and stability in the European used-car market.

�����Ƿ��������������ٳٱ����-����ٳ������ٲ��Ի岹���徱�����پ��Dz����ٱ�����������Բ�����������ܲ������ղ����ܱ�����Ǵ�����������������ղ�

The absence of standardized battery health assessment protocols is significantly hampering the growth of the used electric vehicle (EV) market in Europe, creating uncertainty around residual values. This issue is particularly critical as the EV fleet expands, with the EU aiming for 100% zero-emission mobility for new vehicles by 2035. The United Nations is developing Global Technical Regulation No. 22 to standardize battery health assessments, which could serve as a European benchmark. At the same time, the Euro 7 standards, effective July 1, 2025, will require BEV and PHEV batteries to retain specific energy storage capacities over time[2] "The Road to a New European Automotive Strategy," Notre Europe - Jacques Delors Institute, institutdelors.eu/wp.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: SUV/MUV Leadership Driving Volume

SUV/MUV models commanded 33.78% of the European used-car market in 2025, reflecting consumer appetite for versatility and higher seating positions, even after fuel-cost pressures peaked. BEV-compatible SUVs now exit lease pools in greater numbers, which underpins a 9.67% CAGR outlook. Sedans continue to slide as urban congestion charges penalise longer body formats. Hatchbacks retain loyalty inside dense city cores among price-sensitive first-time buyers.

Dynamic residuals encourage franchised dealers in France and Spain to dedicate rooftop space to mid-spec crossovers, while LCV uptake remains steady in service-oriented SMEs. Euro 6-compliant vans trade at 12% premiums inside low-emission zones, highlighting a bifurcation between compliant and non-compliant workhorses. Southern Europe leans even harder into SUVs; Portugal’s demand for sub-compact crossovers such as the Peugeot 2008 grows by double digits.

By Fuel Type: Diesel Dominance Fading as BEVs Surge

Diesel vehicles captured 41.52% of the European used car market share in 2025, down from previous highs as clean-air measures rise. Though starting small, battery-electric vehicles are advancing at a 17.95% CAGR as early-adopter fleets de-risk technology concerns by releasing documented vehicles. Petrol remains relevant in countries with nascent charging grids, while HEV and PHEV address compliance and range concerns.

Cross-border arbitrage channels diesel cars from France and Germany into Bulgaria and Romania, prolonging lifecycle yields. Meanwhile, BEV bargains appear in the Netherlands, where resale subsidies tighten. Transparency around battery state of health remains a gating factor, yet growth in verification kits is expected to unlock further liquidity after Euro 7 implementation.

By Vendor Type: Digital Transformation Favoring Organized Players

Independent traders, private classifieds, and micro-dealerships still account for 54.60% of the volume, but organized players scale quicker at 6.18% CAGR as investors back data-rich marketplaces. OEM-sponsored CPO outlets add inventory discipline, bundled service plans, and financing that resonate with risk-averse shoppers.

The European used car market rewards platforms able to syndicate stock, automate reconditioning, and guarantee title. In Poland, bundled transport and taxation services enable organised sellers to undercut fragmented rivals on cross-border purchases, boosting trust and repeat business.

By Sales Channel: Digital-Physical Integration Reshaping Retail

Offline showrooms still excel at tactile inspection and immediate gratification, locking in 87.35% of units in 2025, while online transactions scale at a 16.35% CAGR. Online journeys influence almost every purchase. For example, Video walk-arounds, digital trade-in valuations, and doorstep hand-overs recreate showroom confidence on a screen.

Over the forecast horizon, the European used-car market is expected to see most dealers converge on hybrid models, with pricing, paperwork, and financing conducted online. At the same time, the final handover or test drive takes place at a regional hub. Northern Europe pioneered such integration, but Spain and Italy rapidly implemented virtual appointments as broadband infrastructure strengthened.

By Vehicle Age: Ex-lease Vehicles Driving Mid-age Segment

Cars aged 3 to 5 years dominated, with a 36.72% share in 2025 as fleet and leasing contracts matured. This slice offers the sweet spot between the depreciation curve and the remaining warranty, attracting middle-income households. Nearly new 0- to 2-year-old units grow at a 10.84% CAGR, driven by tactical OEM registrations and short-cycle rentals.

Older cohorts aged 9+ benefit from affordability but face reliability concerns, particularly in safety-conscious Scandinavian markets. The average German parc age has climbed to 10.3 years, underpinning robust parts and service demand. Inspection networks expand warranty add-ons to prolong usable life and bolster confidence in older units.

By Ownership Count: Preference for Single-history Vehicles

Single-owner cars hold a 61.55% share because maintenance records are usually complete, and accidents are easier to trace. Digital registries are popular in Sweden and Finland, boosting this advantage by providing verified mileage and service histories. Multi-owner units grow at 5.31% CAGR as car-sharing models rotate keys more often, especially in large cities.

In the European used-car market context, transparent presentation of owner changes is pivotal when exporting to markets with varying documentation standards. Dealers who bundle third-party checks convert lingering sceptics and command higher gross margins.

By Price Band: Mid-market Dominance Amid Polarization

The USD 10k to 20k price band accounts for 40.62% of the European used car market in 2025, representing the sweet spot for mainstream buyers seeking reliable transportation with modern features at accessible price points. This segment includes various vehicle types and ages, from older premium models to newer economy vehicles. The segment over USD 30k is growing fastest at 9.71% CAGR (2026-2031), driven by the increasing presence of premium electric vehicles and late-model luxury cars in the used market.

The Less than USD 10k segment serves price-sensitive buyers, including first-time car owners and those seeking secondary vehicles for specific purposes. The USD 20k-30k band bridges the gap between mainstream and premium offerings, featuring newer mainstream models and older luxury vehicles. The market is experiencing increasing polarization, with growth concentrated at the premium end while the entry-level segment faces pressure from alternative mobility solutions in urban areas. In Germany, vehicles under USD 10,000 make up about 5% of the market, while those under USD 20,000 account for around 30%. The ADAC recommends considering non-German brands like Honda, Kia, and Toyota for budget-friendly options under USD 10,000.

By Financing Type: Innovative Solutions Expanding Access

Outright purchase remains the dominant financing method in the European used car market with 60.92% market share in 2025, reflecting traditional buying patterns and the significant proportion of lower-priced vehicles where financing may not be cost-effective. However, financed purchases are growing at 8.66% CAGR (2026-2031), driven by innovative financing solutions and the increasing presence of higher-value vehicles in the used market. The rise of embedded finance and Buy Now Pay Later (BNPL) options is expanding access to vehicle financing, particularly for younger buyers and those with limited credit histories.

The financing landscape varies significantly by country, with Northern European markets showing higher finance penetration rates than Southern and Eastern European markets. Digital platforms are streamlining the financing process, with integrated solutions that provide instant approval and personalized terms based on vehicle characteristics and buyer profiles.

Geography Analysis

Germany, with its robust retail network and rigorous inspection culture, will hold a 17.85% share of the European used car market in 2025.

The United Kingdom ranks second, propelled by record enquiries for used EVs as charging coverage improves nationwide. France, Italy, and Spain round out the top five. Italy recorded 8.5% growth in 2024 sales volume while Spain posted a 16% surge, although Spanish units take longer to sell due to regional tax disparities. Each market exhibits distinctive regulatory permutations that shape inventory mix and pricing latitude.

Poland posts the fastest trajectory at 7.42% CAGR through 2031. Income elasticity drives divergent patterns; rising household earnings lift new-car uptake while dampening demand for older imports, nudging traders to specialise in younger, low-kilometre stock. The Netherlands and Sweden illustrate advanced electrification and leasing density, respectively, both feeding well-specified returns into regional auctions. Emerging Balkan and Baltic states inside the Rest of Europe category absorb significant diesel inflows, reinforcing cross-border arbitrage loops.

Competitive Landscape

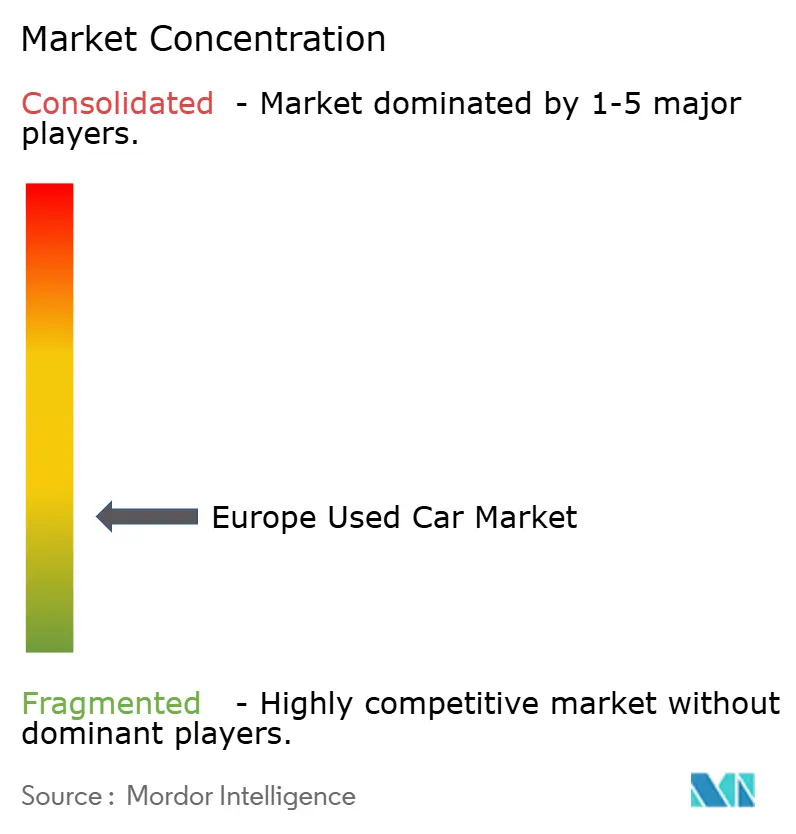

The European used car market is structurally fragmented, underscoring room for consolidation. Incumbent franchised dealers anchor trust through physical footprints and after-sales packages, yet digital natives scale rapidly by capturing search traffic and automating appraisal decisions. AUTO1 Group reported a 2.7% price uptick in Q1 2025 as its algorithmic bidding tightened supply disciplines[3]"AUTO1 Group Price Index: Used car prices increased in Q1 2025, fueled by petrol and diesel vehicle demand," AUTO1 Group, auto1-group.com.

OEMs intensify competition by rolling out pan-European CPO ecosystems that lock buyers into brand service suites and create residual value floors for BEVs. Stellantis, Volkswagen, and BMW now syndicate multi-country listings with unified warranty wording, bridging confidence gaps in cross-border deals. Battery health certification startups partner with these networks to underpin resale pricing for electric vehicles.

Data analytics underpin modern playbooks: predictive pricing, micro-targeted advertising, and VIN-level stocking rules unlock cost savings. Operators that couple real-time market scans with vertically integrated refurbishment gain speed and margin advantages. Investors, therefore, channel capital into online platforms that can bolt on regional dealer groups, execute asset-light logistics, and recycle cash by shortening days-to-sale.

Europe Used Car Industry Leaders

-

Lookers Plc

-

Emil Frey AG

-

Pendragon Plc

-

Auto1 Group SE

-

Aramis Group SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: In Q1 2025, AUTO1 Group reported a 2.7% rise in its Price Index, climbing from 135.2 in January to 138.8 in March. This surge was largely fueled by a spike in demand for petrol and diesel vehicles.

- February 2025: Barcelona-based Dealcar raised EUR 3 million to digitize used-car dealerships and commence entry into Germany.

Europe Used Car Market Report Scope

Pre-owned vehicles, commonly known as used cars, have had one or more retail owners before their current sale. These cars find new homes through various outlets, including independent dealers and online sales channels.

Europe's used-car market is segmented by vehicle type, vendor type, fuel type, and country. Based on vehicle type, the market is segmented into Hatchbacks, sedans, Sports Utility Vehicles, and Multi-purpose Vehicles. Based on the vendor type, the market is segmented into organized and unorganized. Based on fuel type, the market is segmented into gasoline, diesel, electric, and other. By country, the market is segmented into Germany, the United Kingdom, France, Italy, Spain, Russia, and the Rest of Europe. For each segment, market sizing and forecasts have been conducted based on value (USD) and volume (Units).

By Vehicle Type

| Sedan |

| SUV/MUV |

| Hatchback |

By Fuel Type

| Gasoline |

| Diesel |

| Battery Electric Vehicle (BEV) |

| Hybrid and Plug-in Hybrid (HEV/PHEV) |

| Others (LPG, CNG, Bio-fuel) |

By Vendor Type

| Organized |

| Unorganized |

By Sales Channel

| Offline |

| Online |

By Vehicle Age

| 0 to 2 Years |

| 3 to 5 Years |

| 6 to 8 Years |

| More Than 9 Years |

By Ownership Count

| Single-Owner Vehicles |

| Multi-Owner Vehicles |

By Price Band (USD)

| Less than 10k |

| 10k to 20k |

| 20k to 30k |

| More than 30k |

By Financing Type

| Financed Purchase |

| Outright Purchase |

By Country

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Russia |

| Netherlands |

| Sweden |

| Poland |

| Rest of Europe |

| By Vehicle Type | Sedan |

| SUV/MUV | |

| Hatchback | |

| By Fuel Type | Gasoline |

| Diesel | |

| Battery Electric Vehicle (BEV) | |

| Hybrid and Plug-in Hybrid (HEV/PHEV) | |

| Others (LPG, CNG, Bio-fuel) | |

| By Vendor Type | Organized |

| Unorganized | |

| By Sales Channel | Offline |

| Online | |

| By Vehicle Age | 0 to 2 Years |

| 3 to 5 Years | |

| 6 to 8 Years | |

| More Than 9 Years | |

| By Ownership Count | Single-Owner Vehicles |

| Multi-Owner Vehicles | |

| By Price Band (USD) | Less than 10k |

| 10k to 20k | |

| 20k to 30k | |

| More than 30k | |

| By Financing Type | Financed Purchase |

| Outright Purchase | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Netherlands | |

| Sweden | |

| Poland | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current value of the Europe used car market?

The Europe Used Car Market size is expected to reach USD 61.7 billion in 2026 and grow at a CAGR of 4.37% to reach USD 76.43 billion by 2031.

Why are BEVs important to the future European used-car landscape?

Battery-electric vehicles are the fastest-growing fuel segment at an 17.95% CAGR and underpin premium growth, although battery health certification remains a challenge.

Which country leads the Europe used car market?

Germany leads with an 17.85% share in the market in 2025.

What drives demand for 3 to 5-year-old cars?

The steady release of ex-lease vehicles, complete with maintenance records and residual warranty cover, supplies attractive mid-age stock.

Page last updated on: