Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

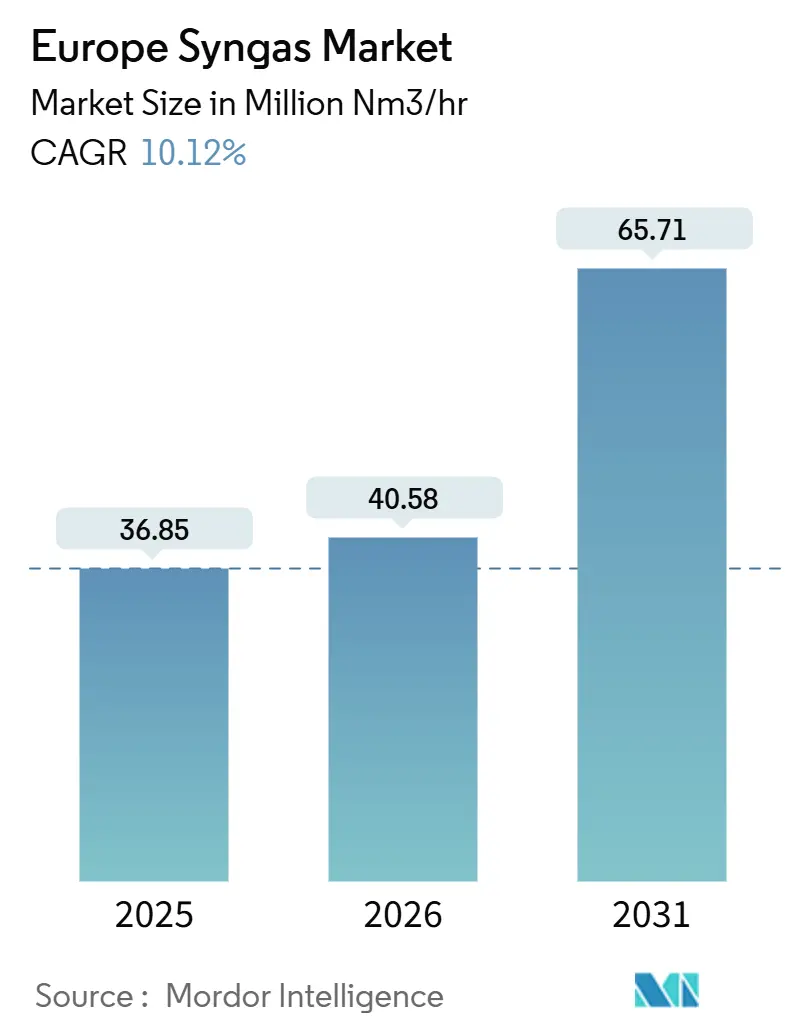

| Base Year Market Size (2025) | 36.85 Million metric normal cubic meters per hour (mm nm³/h) |

| Market Volume (2026) | 40.58 Million metric normal cubic meters per hour (mm nm³/h) |

| Market Volume (2031) | 65.71 Million metric normal cubic meters per hour (mm nm³/h) |

| Growth Rate (2026 - 2031) | 10.12% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Europe Syngas Market Analysis by ���ϲ�����

The Europe Syngas Market size is expected to grow from 36.85 million metric normal cubic meters per hour (mm nm³/h) in 2025 to 40.58 million metric normal cubic meters per hour (mm nm³/h) in 2026 and is forecast to reach 65.71 million metric normal cubic meters per hour (mm nm³/h) by 2031 at 10.12% CAGR over 2026-2031. Driven by the European Commission's REPowerEU allocation, the cost parity of blue hydrogen with gray hydrogen in Northwest Europe, and tightening mandates on maritime and aviation fuels, there is a noticeable shift toward low-carbon hydrogen carriers. Capital spending is heavily influenced by retrofit economics: integrating pre-combustion capture into existing reformers is significantly cheaper than constructing new greenfield gasifiers. Furthermore, shared CO₂ pipelines offer a significant advantage, reducing transport and storage tariffs. Investors are increasingly wary of policy risks, steering their focus toward feedstocks that enjoy long-term regulatory acceptance. Biomass residues, in particular, are in the spotlight, as they can generate double-counting renewable-gas certificates. In contrast, there is a noticeable pullback from fossil CO₂ sources, especially since these will lose their RFNBO eligibility after 2040. On another front, companies are introducing modular autothermal reformer packages. These innovations are shrinking the minimum economic plant size, empowering mid-tier chemical producers to independently source hydrogen and carbon monoxide.

Key Report Takeaways

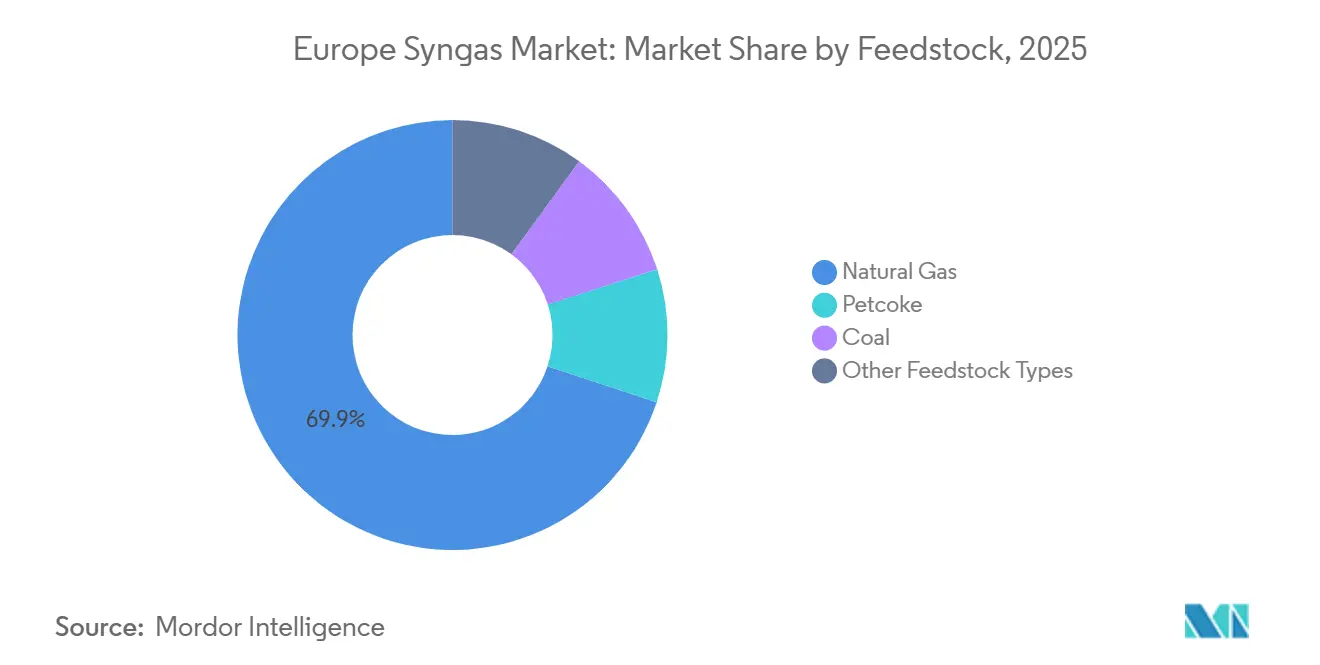

- By feedstock, natural gas led with 69.93% of Europe's syngas market share in 2025 and is set to post the fastest 16.62% CAGR (2026-2031).

- By technology, gasification held 54.80% share of the European syngas market size in 2025; steam methane reforming retrofits are advancing at a 12.94% CAGR (2026-2031).

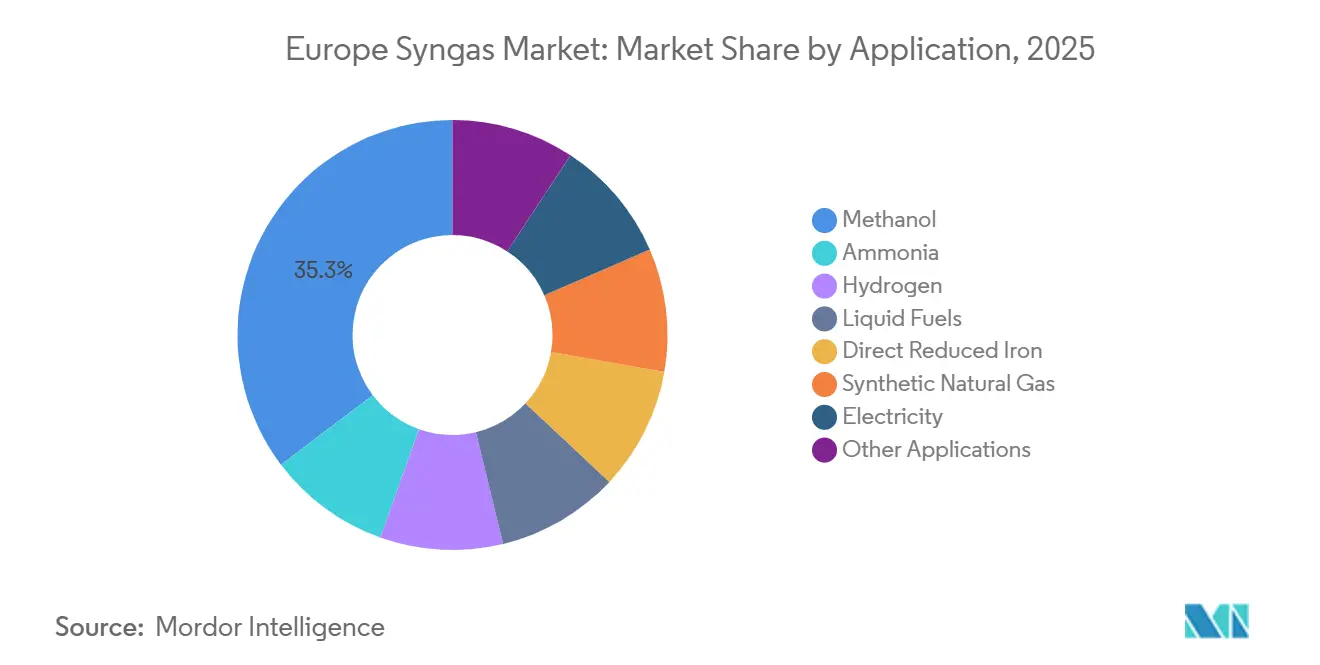

- By application, methanol accounted for a 35.30% share of the European syngas market size in 2025, and synthetic natural gas is projected to expand at a 19.45% CAGR between 2026-2031.

- By geography, Germany captured 25.12% of the European syngas market share in 2025, whereas the Rest of Europe block is forecast to record the highest 11.24% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Syngas Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Abundant refinery and steel-mill off-gases enable low-cost syngas blending | +1.8% | Germany, France, Belgium, Netherlands | Short term (≤ 2 years) |

| CO₂-tax-driven switch to blue and green hydrogen via syngas routes | +2.5% | EU-wide, concentrated in Germany, Netherlands, UK | Medium term (2-4 years) |

| Bio-SNG projects securing EU carbon-negative credits | +1.2% | Nordic countries, Germany, Austria | Medium term (2-4 years) |

| Growth of e-methanol and e-SAF mandates under FuelEU Maritime and ReFuelEU Aviation | +2.9% | Coastal nations (Netherlands, Belgium, Spain), aviation hubs (Germany, France) | Long term (≥ 4 years) |

| Industrial cluster CCUS hubs lowering capture cost for ammonia and methanol | +1.4% | Port of Rotterdam, Antwerp, Teesside, Hamburg | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Abundant Refinery and Steel-Mill Off-Gases Enable Low-Cost Syngas Blending

In 2025, integrated clusters generated millions of Nm³/h of CO- and H₂-rich streams, primarily sourced from refinery purge hydrogen and blast-furnace top gas. However, only a fraction of this output was integrated into Europe's syngas grids. ArcelorMittal's Gent route diverted coke-oven gas to a nearby methanol unit, achieving notable feedstock savings. With the EU ETS price increasing in 2026, this practice gained broader adoption. Steelmakers, grappling with idle blast furnaces, are leveraging stranded gases through tolling agreements. They are utilizing the existing Ruhr and Dunkirk pipelines, which require only minor upgrades. Although the driver reached its peak within two years due to available pipeline capacity, full adoption depends on clarity regarding RFNBO for fossil-derived off-gases.

CO₂-Tax-Driven Switch to Blue and Green Hydrogen via Syngas Routes

Due to the Carbon Border Adjustment Mechanism imposing charges on imported ammonia and methanol, unabated gray hydrogen has experienced a loss of its competitive edge. Yara's blue-ammonia facility in Sluiskil, Netherlands, captures carbon annually, ensuring a low carbon intensity in ammonia production, supported by Dutch SDE++ initiatives[1]Yara, “Yara Starts Production of Blue Ammonia at Sluiskil,” yara.com. With the ongoing expansion of CCUS and decreasing costs of electrolysis, a notable transition has been underway. Furthermore, green hydrogen is projected to achieve grid parity in Northern Europe within the forecast period of 2026–2031.

Bio-SNG Projects Securing EU Carbon-Negative Credits

Under RED III, biomethane grid injection benefits from double-counting, while bio-syngas routes secure guarantees of origin. Göteborg Energi operates a plant that gasifies wood chips, producing pipeline methane. This operation is projected to generate certificate revenue during the forecast period of 2026–2031, while achieving a life-cycle intensity with negative carbon dioxide equivalent emissions. As biomass densification hubs expand their feedstock radii, they continue to scale operations.

Growth of E-Methanol and E-SAF Mandates Under FuelEU Maritime and ReFuelEU Aviation

Starting in 2025, FuelEU Maritime mandates a reduction in GHG intensity, with further cuts required by 2030. In parallel, ReFuelEU Aviation mandates the adoption of SAF beginning in 2025, ramping up levels by 2030, and offers credit multipliers for renewable e-fuels. OCI has launched an e-methanol plant in Rotterdam, utilizing offshore wind power and biogenic CO₂, aligning with Maersk’s willingness to pay a premium. Shell is upgrading its Hamburg facility for e-SAF, poised to supply kerosene in 2028 under a partnership with Lufthansa. Demand is projected to surge post-2028 as bio-oil pathways become more cost-effective and widely accessible.

Restraints Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High-pressure oxygen supply cost for entrained-flow gasifiers | -1.6% | Germany, Poland, Czech Republic (coal/petcoke regions) | Short term (≤ 2 years) |

| Regulatory sunset for fossil-CO₂ feed after 2040 in EU RFNBO rules | -1.1% | EU-wide, acute in coastal e-methanol hubs | Long term (≥ 4 years) |

| Skilled-labor shortage for large-scale gasification EPC | -0.7% | Germany, Netherlands, UK (major project clusters) | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

High-Pressure Oxygen Supply Cost for Entrained-Flow Gasifiers

High-purity oxygen is essential for entrained-flow units, which demand it at a specific rate for each unit of syngas. The introduction of cryogenic ASUs has driven up the cost of syngas - a challenge exacerbated by rising industrial power prices. In 2026, PKN Orlen of Poland scrapped its plans for a petcoke gasifier, pointing to concerns over oxygen-related costs. Of the eleven gasifiers proposed across Europe, only three received a final investment decision (FID) during the forecast period of 2026–2031.

Regulatory Sunset for Fossil-CO₂ Feed After 2040 in EU RFNBO Rules

Preem canceled its Lysekil e-methanol project in 2025, citing concerns over stranded assets. Despite a forecasted cost decline by 2035, the high expenses associated with direct-air capture make e-methanol more expensive than its fossil-based counterpart in 2026. Consequently, investors are shifting their focus to carbon dioxide (CO₂) sources from pulp mills and waste-to-energy (WtE) plants. Furthermore, a delegated act, effective after December 31, 2040, will prohibit the use of fossil-sourced CO₂ in e-fuels[2]European Commission, “Delegated Regulation on Renewable Fuels of Non-Biological Origin,” energy.ec.europa.eu.

Segment Analysis

By Feedstock: Natural Gas Anchors Blue-Hydrogen Transition

In 2025, Europe’s syngas market saw natural gas dominate with a 69.93% share. Projections indicate a vigorous growth trajectory, eyeing a 16.62% CAGR through the forecast period of 2026–2031. This surge is attributed to operators pivoting from steam reforming to autothermal reforming, enhancing capture efficiency. A notable instance is the 750 MW Teesside complex. Meanwhile, coal and petcoke, once major players, are witnessing a decline. This downturn is primarily driven by Germany's coal-exit law, accelerating closures. However, retrofitting capture on the remaining units has prolonged their operational lifespan, at least until 2030. Europe's syngas market is capitalizing on the fuel-efficiency advantages of ATR over conventional methods. However, profit margins tighten when TTF hub prices exceed EUR 60 MWh⁻1 during peak winter months.

Other feedstocks, such as biomass, municipal solid waste (MSW), and refinery residues, currently command a modest market share. However, they are poised for significant growth, buoyed by initiatives like a plastics-gasification line. This cutting-edge project processes refuse, effectively replacing gray hydrogen. Furthermore, biomass volumes are on the rise as torrefaction hubs in Poland and Finland expand their collection radius to 300 km, all while staying compliant with RED III sustainability standards.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Technology: Gasification Legacy Meets Reforming Renaissance

In 2025, gasification commanded a dominant 54.80% share of Europe's syngas market. However, steam methane reforming is gaining momentum, with a projected growth of 12.94%. CAGR (2026-2031). This growth is largely attributed to established reformers adopting pre-combustion capture, achieving this at a fraction of the cost of new gasifiers. Johnson Matthey's HyCOgen retrofits have not only boosted hydrogen yield but also achieved impressive capture rates, all without the necessity of replacing primary tubes. By the forecast period of 2026–2031, projections indicate an almost equal distribution between gasification and reforming. This transition is evident as closures of coal facilities offset the rise of biomass gasifiers. Additionally, modular Prenflo units are empowering mid-tier Italian firms to set up gasifiers, strategically positioned alongside sawmills.

By Application: Methanol Dominance Yields to Synthetic-Fuel Surge

In 2025, Maersk's increasing demand for e-methanol and its subsequent orders for methanol-ready vessels propelled methanol to capture a commanding 35.30% share of the market. Synthetic natural gas, supported by a feed-in tariff hike in Germany, emerged as the fastest-growing segment, achieving an impressive compound annual growth rate (CAGR) of 19.45% during the forecast period of 2026–2031. Ammonia, which already holds a substantial market share, is expected to expand further, driven by the coal-to-ammonia conversion project in Wilhelmshaven. This project is scheduled to provide dispatchable power by 2028. Additionally, direct-reduced iron is preparing to leverage hydrogen's potential, with ArcelorMittal's Hamburg DRI line set to begin hydrogen utilization in late 2026.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

In 2025, Germany, fueled by its numerous ammonia and methanol plants, accounted for 25.12% of Europe's syngas market. Emsland's hybrid electrolyzer-ATR, a testament to the country's advancements and part of the HyStarter consortium, showcased seasonal wind-to-ammonia storage. The United Kingdom, supported by East Coast Cluster contracts that guarantee carbon dioxide storage, secured a significant market share. These contracts not only strengthened the United Kingdom's position but also facilitated the rollout of blue hydrogen in Teesside and Humberside. France, leveraging TotalEnergies' Normandy refinery and planning for a 2027 addition of an electrolyzer in Dunkirk, captured a noteworthy market share.

Italy and Spain, together, held a considerable stake. Eni's investments in blue-hydrogen retrofits at Taranto and Livorno, combined with Iberdrola's support for a green-hydrogen hub in Puertollano, underscored their commitment. Meanwhile, Russia, benefiting from TurkStream gas supplies, maintained operations at its Balkan ammonia plants. However, as LNG diversification gained prominence, the strategic advantage of these supplies began to diminish. Other European players, including Poland, the Netherlands, Belgium, and the Nordics, collectively held a substantial share. Cross-border carbon dioxide pipelines, which unlock stranded biomass and waste feedstocks, are driving the fastest growth rate of 11.24% in the rest of Europe, with projections indicating an even larger share by the 2026–2031 forecast period.

By the 2026–2031 forecast period, Germany's share is expected to decline as the retirement of coal gasifiers outpaces the growth of blue hydrogen. The United Kingdom's market presence is projected to expand, supported by the introduction of new blue-hydrogen capacities. In the Mediterranean region, ports are preparing to establish e-methanol import terminals, which are expected to increase Italy and Spain's combined market share. Conversely, Russia's stake is anticipated to decline as European buyers shift their focus toward Qatari and United States LNG.

Competitive Landscape

The European syngas market is moderately consolidated. New players are venturing into areas like waste-to-syngas, offshore wind-to-ammonia, and micro Fischer-Tropsch facilities. Regulatory mandates are influencing industry strategies. Projects must comply with the EU Taxonomy, limiting emissions to 3 kg CO₂e per kg H₂ and aligning closely with renewable electricity timelines. To navigate these hurdles, Air Liquide has introduced a patented battery-buffered electrolysis system, designed to counteract wind intermittency and meet regulatory standards. Firms that weave Carbon Capture, Utilization, and Storage (CCUS) or renewable energy assets into their framework stand to enjoy sturdier margins than those dependent solely on gas supplies.

Europe Syngas Industry Leaders

Linde plc

Air Liquide

Air Products & Chemicals Inc.

Haldor Topsoe A/S

Shell plc

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- February 2026: Barcelona-based WtEnergy raised EUR 10 million from SC Net Zero Ventures, Shell Ventures, and Cemex Ventures to standardize biomass and solid-waste gasifiers that produce clean syngas for hydrogen, methanol, and sustainable aviation fuel applications.

- February 2025: MET Development, Eni, and Iren Ambiente initiated permitting for a circular methanol and hydrogen plant at Eni’s Sannazzaro de' Burgondi refinery to convert 200,000 tons per year of non-recyclable waste into syngas for sustainable fuels.

Europe Syngas Market Report Scope

Syngas, short for synthesis gas, is defined as a versatile fuel blend primarily composed of hydrogen and carbon monoxide (CO), with carbon dioxide often included. It is produced by gasifying carbon-rich materials such as coal, biomass, or waste and serves as a key intermediary in generating electricity, ammonia, methanol, and synthetic fuels.

The market is segmented by feedstock, technology, application, and geography. By feedstock, the market is segmented into petcoke, coal, natural gas, and other feedstock types. By technology, the market is segmented into steam methane reforming and gasification. By application, the market is segmented into methanol, ammonia, hydrogen, liquid fuels (FT, DME, SAF), direct reduced iron, synthetic natural gas, electricity, and other applications. The report also covers the market size and forecasts for the market in 6 countries across the region. For each segment, the market sizing and forecasts are volume (Metric Normal Cubic Meters Per Hour).

By Feedstock

| Petcoke |

| Coal |

| Natural Gas |

| Other Feedstock Types |

By Technology

| Steam Methane Reforming |

| Gasification |

By Application

| Methanol |

| Ammonia |

| Hydrogen |

| Liquid Fuels (FT, DME, SAF) |

| Direct Reduced Iron |

| Synthetic Natural Gas |

| Electricity |

| Other Applications |

By Geography

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Russia |

| Rest of Europe |

| By Feedstock | Petcoke |

| Coal | |

| Natural Gas | |

| Other Feedstock Types | |

| By Technology | Steam Methane Reforming |

| Gasification | |

| By Application | Methanol |

| Ammonia | |

| Hydrogen | |

| Liquid Fuels (FT, DME, SAF) | |

| Direct Reduced Iron | |

| Synthetic Natural Gas | |

| Electricity | |

| Other Applications | |

| By Geography | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How fast is syngas demand growing across European chemical plants?

Volume expands from 40.58 MM Nm³/h in 2026 to 65.71 MM Nm³/h by 2031, registering a 10.12% CAGR.

Which feedstock will dominate new European syngas projects up to 2031?

Natural gas remains primary because autothermal reformers with carbon capture achieve 98% CO₂ removal at competitive cost.

What role does CO₂ infrastructure play in project economics?

Shared pipelines such as Porthos cut transport and storage tariffs, making blue-ammonia and blue-methanol investments viable.

When will e-methanol achieve meaningful cost parity with fossil methanol?

Widespread parity is expected post-2028 as offshore-wind electricity prices fall and RFNBO credits scale.

Which country is likely to post the strongest growth rate in syngas capacity?

The Rest of Europe block, led by Poland, the Netherlands, and Nordic nations, is forecast to grow at 11.24% CAGR (2026-2031).