Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

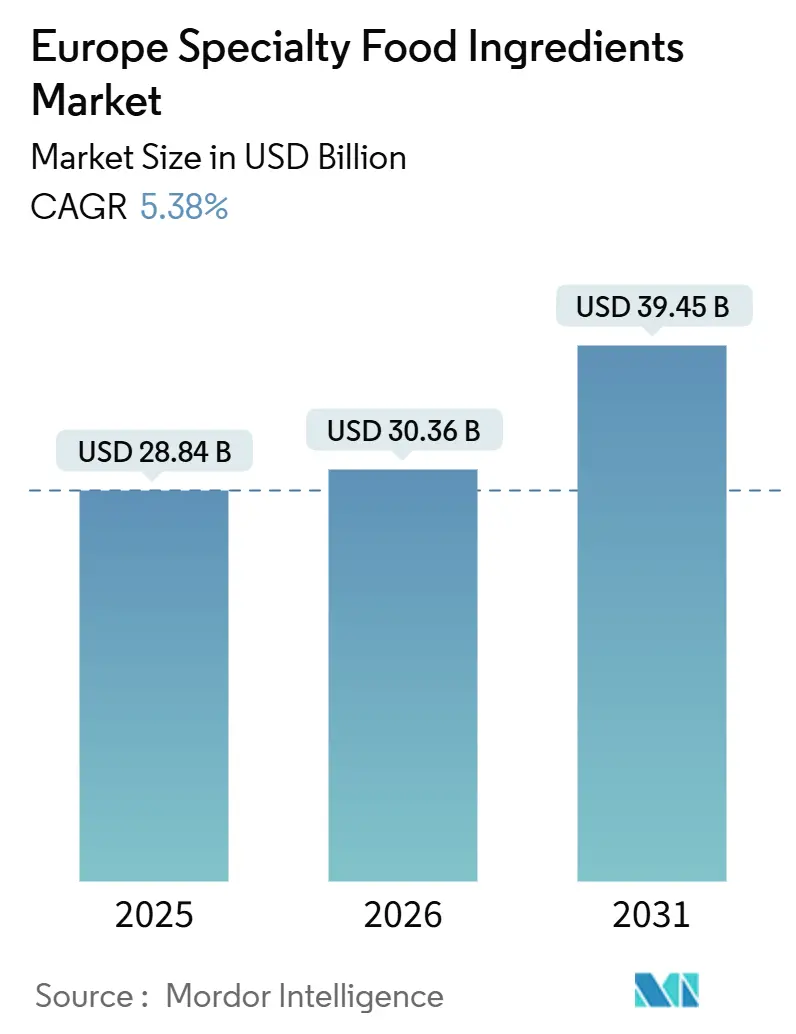

| Base Year Market Size (2025) | USD 28.84 Billion |

| Market Size (2026) | USD 30.36 Billion |

| Market Size (2031) | USD 39.45 Billion |

| Growth Rate (2026 - 2031) | 5.38% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. |

|

Europe Specialty Food Ingredients Market Analysis by ���ϲ�����

The Europe specialty food ingredients market size is expected to increase from USD 28.84 billion in 2025 to USD 30.36 billion in 2026 and reach USD 39.45 billion by 2031, growing at a CAGR of 5.38% over 2026-2031. This trajectory reflects a structural pivot toward functional nutrition, clean-label reformulation, and precision biotechnology that is reshaping ingredient portfolios across the continent. Alternative sweeteners retained high visibility as regulatory support for stevia and allulose widened accepted use levels, while natural preservatives benefited from retailer deadlines that phase out synthetic additives. Beverage formulators absorbed the largest ingredient volumes, yet dairy processors posted the fastest ingredient spend as probiotic fortification, high-protein recipes, and plant-based analogs demanded specialized cultures, texturants, and enzymes. Simultaneously, precision fermentation startups are closing performance gaps in plant-based meat, seafood, and dairy analogs, creating an ecosystem where collaboration can unlock margin-accretive niches.

Key Report Takeaways

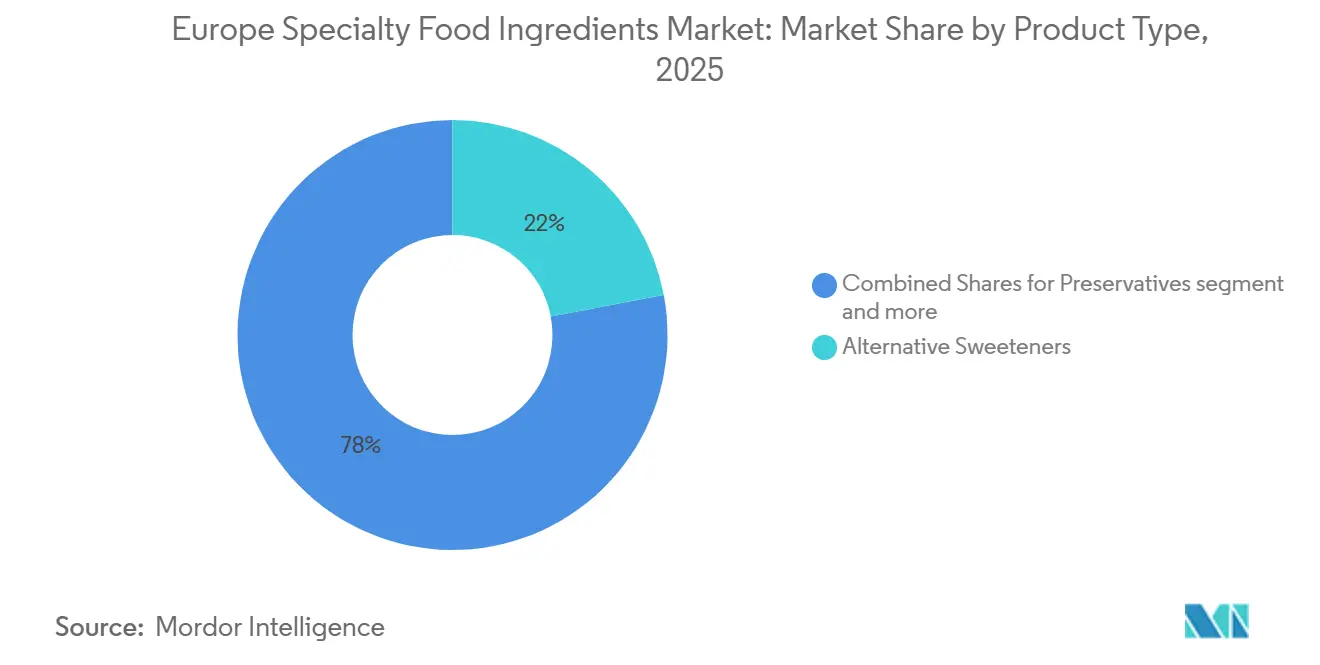

- By product type, alternative sweeteners commanded 22.04% of Europe specialty food ingredients market share in 2025, whereas preservatives are projected to expand at a 5.81% CAGR through 2031.

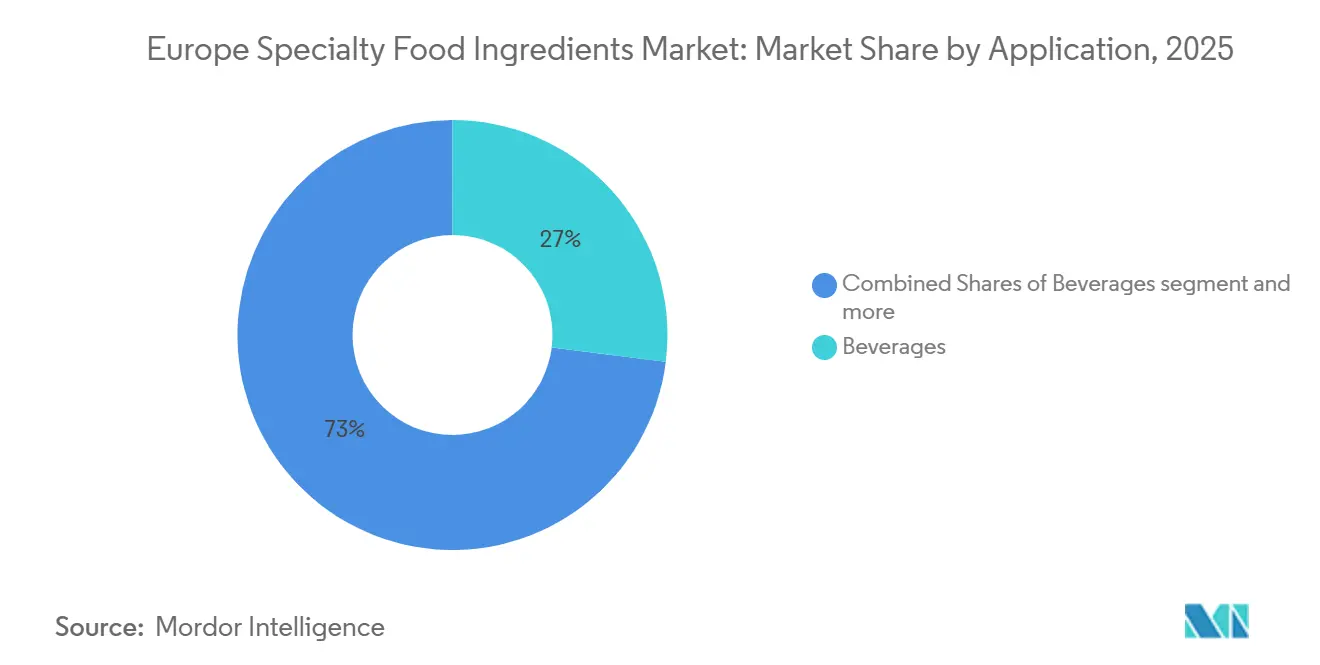

- By application, beverages led with 31.22% share of Europe specialty food ingredients market size in 2025, while dairy is advancing at a 6.58% CAGR to 2031.

- By geography, Germany held 15.57% revenue share in 2025; the United Kingdom records the highest projected CAGR at 6.34% through 203.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Specialty Food Ingredients Market Trends and Insights

Drivers Impact Analysis

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for clean-label ingredients | +1.2% | Germany, UK (United Kingdom), France, Netherlands | Medium term (2-4 years) |

| Rising adoption of functional food formulations | +1.0% | Germany, UK, Spain, Italy | Long term (≥ 4 years) |

| Expansion of plant-based product innovation | +0.9% | UK, Germany, Netherlands, France | Medium term (2-4 years) |

| Advancements in fermentation and enzyme technologies | +0.8% | Germany, the Netherlands, and France | Long term (≥ 4 years) |

| Increasing use of natural flavors and colors | +0.7% | Spain, Italy, France, Germany | Short term (≤ 2 years) |

| Premiumization trends across food and beverages | +0.6% | UK, Germany, France | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Growing Demand for Clean Label Ingredients

Consumer scrutiny of ingredient lists intensified in 2025, with the majority of European shoppers reporting they avoid products containing unrecognizable additives, according to a survey by the European Consumer Organisation. This behavioural shift is compelling manufacturers to replace synthetic preservatives, artificial colors, and modified starches with plant-derived alternatives that carry simpler nomenclature. Retailers such as Tesco and Carrefour formalized clean-label commitments in 2024, mandating that private-label suppliers eliminate E-numbers from bakery and snack categories by 2027, a deadline that accelerates reformulation timelines and elevates demand for natural antimicrobials such as rosemary extract and fermented vinegar, according to the European Consumer Organisation. Ingredient suppliers are responding by investing in extraction technologies that preserve bioactive compounds without chemical solvents, a capability that allows them to command price premiums over conventional additives. The trend is most pronounced in Germany and the Netherlands, where organic certification penetration exceeds packaged food sales, creating a pull effect for clean-label inputs across conventional product lines.

Rising Adoption of Functional Food Formulations

Functional ingredients that deliver measurable health benefits beyond basic nutrition captured a significant market of European food spending in 2025, with probiotics, omega-3s, and plant sterols leading the category. The European Food Safety Authority authorized 14 new health claims in 2025, including cognitive function benefits for DHA-enriched dairy and immune support for beta-glucan-fortified beverages, providing manufacturers with regulatory cover to market functional attributes. EFSA's novel food approval process, which typically takes 2.5 years, inadvertently fortifies established specialty ingredient suppliers by establishing regulatory barriers around approved products[1]Source: European Food Safety Authority, “Navigating Novel Foods: What EFSA’s Updated Guidance Means for Safety Assessments,” efsa.europa.eu. This approval momentum is driving ingredient innovation in encapsulation and microencapsulation, technologies that protect sensitive bioactives such as probiotics and vitamins from heat, light, and pH extremes during processing and shelf storage. Kerry Group launched a microencapsulated iron ingredient in March 2025 that eliminates metallic off-notes in fortified juices, a sensory breakthrough that expands the addressable market for iron supplementation beyond pharmaceutical formats.

Expansion of Plant-Based Product Innovation

Plant-based meat and dairy analogs generated billions in European retail sales in 2025, a figure that understates the ingredient complexity required to replicate animal-derived textures and flavors. Pea protein isolates, faba bean concentrates, and mycoprotein require specialized emulsifiers, binders, and flavor masking agents to overcome earthy off-notes and achieve the mouthfeel consumers expect from traditional products. Ingredion introduced a clean-label texturant system in June 2025 that combines modified tapioca starch with pea fiber to deliver the juiciness and bite of ground beef, a formulation that several European plant-based brands adopted for retail launches in late 2025. The UK and Netherlands lead in per-capita consumption of plant-based alternatives, yet Germany and France are experiencing faster growth as mainstream retailers expand shelf space and reduce price gaps with animal products.

Advancements in Fermentation and Enzyme Technologies

Precision fermentation and enzyme engineering are unlocking ingredient functionalities that were previously unattainable through extraction or synthesis. Novozymes commercialized a recombinant lactase enzyme in 2025 that operates at lower temperatures and broader pH ranges than conventional variants, enabling dairy processors to produce lactose-free milk with reduced energy consumption and shorter processing times. This enzyme platform is also being adapted for plant-based dairy, where it breaks down oligosaccharides in oat and almond bases that cause digestive discomfort in some consumers. Fermentation-derived ingredients such as heme protein, which imparts the iron-rich taste of meat, and animal-free collagen, which provides structural support in confectionery and bakery, are transitioning from pilot scale to commercial production, with several European co-manufacturers installing dedicated fermentation capacity in 2025.

Restraint Impact Analysis

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex regulatory approval and compliance processes | -0.5% | EU-wide, particularly Germany, France | Long term (≥ 4 years) |

| High formulation and ingredient development costs | -0.4% | Germany, UK, Netherlands, France | Medium term (2-4 years) |

| Inconsistent raw material quality and availability | -0.3% | Spain, Italy, France (botanicals), Germany (cocoa) | Short term (≤ 2 years) |

| Competition from multifunctional commodity ingredients | -0.2% | Germany, UK, France | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Complex Regulatory Approval and Compliance Processes

The European Food Safety Authority's novel food approval pathway requires comprehensive toxicology studies, stability data, and production process documentation, and extends timelines to 18-24 months, a barrier that disproportionately affects smaller innovators. Highlighting the ongoing regulatory shifts, Spain has recently updated its food hygiene regulations, compelling companies to revise their processes and documentation, as noted by Food Compliance International[2]Source: United States Department of Agriculture, " Plant-based food consumption in Germany", fas.usda.gov. Smaller suppliers of specialty ingredients are feeling the brunt of these compliance costs, a situation that could tilt the market dynamics in favor of larger players equipped with dedicated regulatory teams. The complexity is most acute for fermentation-derived ingredients and bioengineered microorganisms, where regulators demand environmental risk assessments and allergenicity testing beyond what is required for plant extracts or chemically synthesized additives.

Inconsistent Raw Material Quality and Availability

Natural ingredients sourced from agriculture face inherent variability in composition, flavor intensity, and bioactive content due to soil conditions, weather patterns, and harvest timing, a challenge that complicates standardization and quality control. Vanilla prices spiked in early 2025 following cyclone damage in Madagascar, forcing flavor houses to reformulate with synthetic vanillin or alternative botanicals, a substitution that required customer approvals and label changes. Cocoa, stevia, and turmeric face similar supply risks, with climate change exacerbating yield volatility and pushing ingredient buyers toward long-term contracts and vertical integration strategies. The European Commission's deforestation regulation, which took effect in January 2025, imposed traceability requirements on cocoa, palm oil, and soy, adding compliance costs and restricting supplier pools for ingredients derived from these commodities.

Segment Analysis

By Product Type: Preservatives Outpace Sweeteners in Growth Velocity

Preservatives are forecast to expand at 5.81% annually between 2026 and 2031, the fastest growth rate among product types, as manufacturers seek natural antimicrobials that extend shelf life without synthetic additives such as sodium benzoate or potassium sorbate. Fermented vinegar, rosemary extract, and cultured dextrose are displacing traditional preservatives in bakery, sauces, and dairy, driven by clean-label mandates from retailers and consumer demand for recognizable ingredients. Alternative Functional Food Ingredients, encompassing vitamins, minerals, amino acids, omega-3s, and probiotics, are being incorporated into dairy, beverages, and infant food at accelerating rates, with manufacturers layering multiple bioactives to target specific health outcomes such as immune support, cognitive function, and gut health.

Sweeteners held 22.04% of the market value in 2025, anchored by stevia, monk fruit, and allulose, which offer sugar-like sweetness without the caloric load or glycemic impact of sucrose. Specialty Starch and Texturants provide viscosity, mouthfeel, and freeze-thaw stability in applications ranging from plant-based meat to premium ice cream, with clean-label variants derived from tapioca, potato, and rice gaining share over chemically modified corn starch. Flavors, both natural and nature-identical, accounted for a significant portion of ingredient spending in 2025, with demand concentrated in beverages, confectionery, and savory snacks, where taste differentiation drives brand loyalty.

Note: Segment shares of all individual segments available upon report purchase

By Application: Dairy Accelerates as Beverages Maintain Volume Leadership

Beverages commanded 31.22% of application demand in 2025, driven by fortified juices, functional energy drinks, and plant-based milk alternatives that require vitamins, natural colors, and flavor masking agents to deliver consumer-acceptable taste and nutrition. Sauces, Dressings, and Condiments are incorporating natural preservatives, clean-label emulsifiers, and fermented flavors to meet retailer clean-label mandates, with reformulation cycles accelerating in 2025 as private-label suppliers align with Tesco and Carrefour standards. Bakery applications are adopting enzymes that extend shelf life and improve dough tolerance, reducing waste and enabling centralized production for multi-site distribution networks.

Dairy, however, is expanding at 6.58% annually through 2031, the fastest growth rate among applications, propelled by probiotic yogurt, high-protein cheese, and plant-based analogs that demand specialized cultures, enzymes, and texturants. Lallemand and Chr. Hansen introduced new probiotic strains in 2025 that survive pasteurization and deliver clinically validated gut health benefits. Meat, Seafood, and Alternatives are absorbing plant-based texturants, natural colors, and flavor enhancers as analog products scale from specialty to mainstream, with Ingredion and Roquette supplying pea protein isolates and specialty starches that replicate the texture and juiciness of animal proteins.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Germany held 15.57% of regional revenue in 2025, anchored by its robust bakery, confectionery, and dairy sectors that prioritize ingredient quality and functional performance. The country's Federal Institute for Risk Assessment maintains stringent safety standards that slow novel ingredient approvals but also create a quality floor that benefits established suppliers with deep regulatory expertise. The United Kingdom is expanding at 6.34% annually through 2031, the fastest growth rate among European geographies, driven by post-Brexit regulatory divergence that enables faster novel food approvals and a vibrant startup ecosystem in plant-based and precision fermentation.

The UK Food Standards Agency approved 8 novel ingredients in 2025, including fermentation-derived heme protein and algae-based omega-3, timelines that were 6-9 months shorter than equivalent EU approvals[3]Source: FSA (Food Standards Agency), "Novel Ingredients", food.gov.uk. This regulatory agility is attracting ingredient innovators who prioritize speed-to-market over pan-European scale, creating a bifurcated supply chain where UK-specific formulations diverge from continental Europe. France's ANSES approved natural preservatives derived from Mediterranean herbs in 2025, a decision that is enabling regional flavor houses to commercialize locally sourced antimicrobials for sauces and charcuterie. Spain's confectionery and snack sectors are adopting natural colors at accelerating rates, with Chupa Chups and Grefusa reformulating to eliminate synthetic dyes by 2027, a commitment that is driving demand for paprika extract and beetroot powder.

Italy's dairy and bakery industries are investing in enzyme technologies that extend shelf life and improve texture, with Barilla and Ferrero partnering with enzyme suppliers to optimize production efficiency and reduce waste. The Netherlands, with its concentration of food ingredient manufacturers and proximity to Rotterdam port infrastructure, serves as a logistics and R&D hub for multinational suppliers, hosting pilot plants and application centers that support customer formulation development. Russia and the rest of Europe are growing at moderate rates, constrained by economic volatility and regulatory uncertainty, yet they represent long-term opportunities as income levels rise and consumer preferences shift toward premium and functional products.

Competitive Landscape

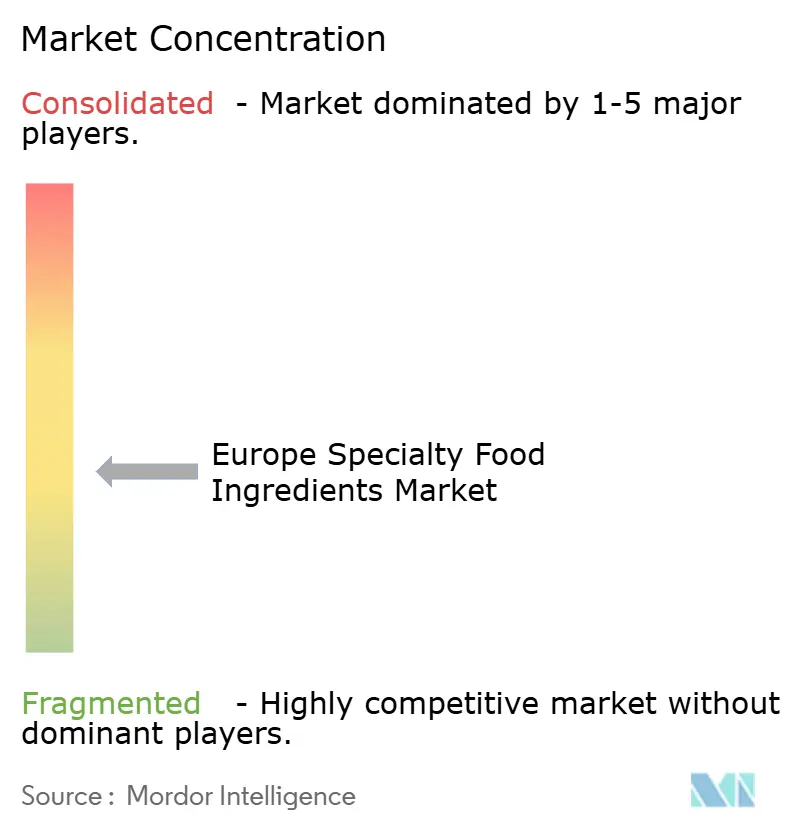

The Europe specialty food ingredients market exhibits moderate fragmentation, reflecting a landscape where multinational formulators such as Cargill, Incorporated, ADM, and Kerry Group coexist with specialized enzyme houses, flavor innovators, and fermentation startups. Scale players leverage vertical integration to secure raw materials such as cocoa, stevia, and vanilla, yet they face margin pressure in commodity segments where differentiation is limited, and customers prioritize cost over ingredient storytelling. Smaller competitors capture premium niches by licensing proprietary technologies such as microencapsulated probiotics, recombinant enzymes, and precision-fermented proteins that deliver measurable performance advantages in applications such as infant formula, sports nutrition, and plant-based analogs.

Strategic moves in 2025 centered on M&A, capacity expansion, and technology partnerships, with DSM-Firmenich acquiring a fermentation specialist to accelerate its animal-free protein portfolio and Tate & Lyle expanding allulose production in response to EFSA approval and surging demand from beverage customers. White-space opportunities exist in enzyme cocktails for plant-based dairy, natural preservatives for clean-label bakery, and bioavailable micronutrients for fortified beverages, segments where incumbents lack technical depth, and customers seek innovation partners rather than commodity suppliers. Emerging disruptors include precision fermentation companies such as Formo and Perfect Day, which produce casein and whey proteins through microbial fermentation, bypassing agriculture and offering ingredient functionality identical to dairy-derived counterparts.

Technology is becoming a competitive differentiator, with suppliers deploying AI-driven formulation software, sensory prediction models, and blockchain traceability to win customer mandates and justify premium pricing. Givaudan filed 14 flavor patents in 2024 related to natural extraction and encapsulation, a signal of its commitment to protecting proprietary processes that deliver superior taste and stability. Regulatory compliance capabilities also confer competitive advantage, as ingredient suppliers who can navigate EFSA's health-claim substantiation requirements and provide technical dossiers for novel food approvals become preferred partners for manufacturers seeking functional positioning and clean-label credentials.

Europe Specialty Food Ingredients Industry Leaders

-

Archer Daniels Midland Company

-

International Flavors & Fragrances Inc

-

Kerry Group

-

Givaudan SA

-

Cargill Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Univar Solutions secures exclusive EMEA distribution rights for Ashland’s specialized functional ingredients (like cellulose ethers), rolling out across Europe and into the Middle East beginning January–April 2026.

- December 2025: Freudenberg Italia acquires Eulip Srl, a producer of specialized plant‑based oils and fats, strengthening Capol’s position as a provider of innovative food and beverage ingredient solutions in Europe.

- November 2025: Nexture S.p.A. announces acquisition of Frulact (Portugal), expanding its capability in fruit‑based specialty ingredient preparations across Europe, North America, and Africa.

Europe Specialty Food Ingredients Market Report Scope

Specialty food ingredients offer technological and functional benefits, playing a crucial role in delivering a diverse array of tasty, safe, healthy, and sustainably produced food products. The ingredients segment of the European specialty food ingredients market comprises functional food ingredients, specialty starches and texturants, sweeteners, flavors, acidulants, preservatives, emulsifiers, colors, enzymes, cultures, proteins, specialty oils, and yeasts. By application, the market is segmented into beverages, sauces, dressings, and condiments, bakery, dairy, confectionery, dried processed foods, frozen/chilled processed foods, sweet and savory snacks, and other applications. The geographical analysis of the market includes Spain, the United Kingdom, France, Germany, Russia, Italy, and the Rest Of Europe. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Tons).

Product Type

| Functional Food Ingredient | Vitamins and Mineral |

| Amino Acids | |

| Omega-3 Ingreidents | |

| Probiotic Ingredients | |

| Specialty Starch and Texturants | |

| Alternative Sweeteners | |

| Flavors | |

| Acidulants | |

| Preservatives | |

| Emulsifiers | |

| Colors | |

| Enzymes | |

| Cultures | |

| Specialty Oils | |

| Yeasts |

Application

| Beverages |

| Sauces, Dressings and Condiments |

| Bakery |

| Dairy |

| Infant Food |

| Meat, seafood, and alternatives |

| Confectionery |

| Sweet and Savory Snacks |

| Other Applications |

Geography

| Spain |

| United Kingdom |

| France |

| Germany |

| Russia |

| Italy |

| Netherlands |

| Rest of Europe |

| Product Type | Functional Food Ingredient | Vitamins and Mineral |

| Amino Acids | ||

| Omega-3 Ingreidents | ||

| Probiotic Ingredients | ||

| Specialty Starch and Texturants | ||

| Alternative Sweeteners | ||

| Flavors | ||

| Acidulants | ||

| Preservatives | ||

| Emulsifiers | ||

| Colors | ||

| Enzymes | ||

| Cultures | ||

| Specialty Oils | ||

| Yeasts | ||

| Application | Beverages | |

| Sauces, Dressings and Condiments | ||

| Bakery | ||

| Dairy | ||

| Infant Food | ||

| Meat, seafood, and alternatives | ||

| Confectionery | ||

| Sweet and Savory Snacks | ||

| Other Applications | ||

| Geography | Spain | |

| United Kingdom | ||

| France | ||

| Germany | ||

| Russia | ||

| Italy | ||

| Netherlands | ||

| Rest of Europe |

Key Questions Answered in the Report

What is the current value of the Europe specialty food ingredients market?

The market is valued at USD 30.36 billion in 2026.

How fast is the market expected to grow?

It is forecast to expand at a 5.38% CAGR to reach USD 39.43 billion by 2031.

Which product category is growing fastest within European specialty food ingredients?

Natural preservatives are projected to expand at 5.81% per year through 2031.

Which application shows the highest growth rate?

Dairy applications show the fastest growth at 6.58% CAGR through 2031.

Page last updated on: