Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

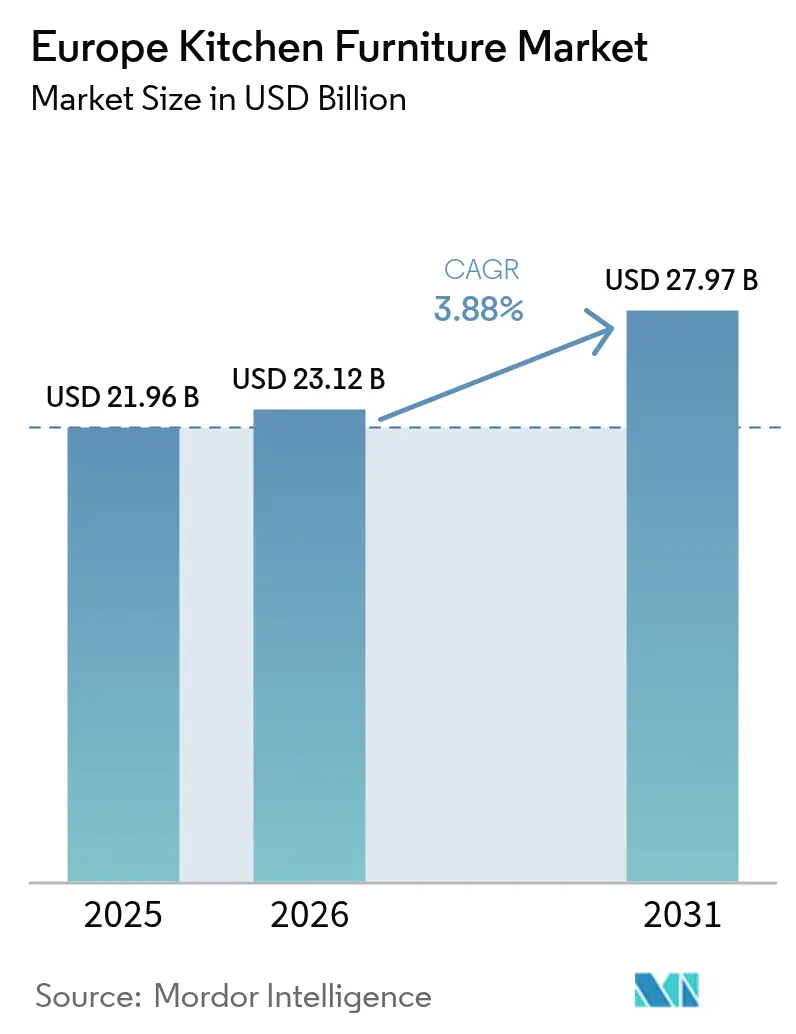

| Base Year Market Size (2025) | USD 21.96 Billion |

| Market Size (2026) | USD 23.12 Billion |

| Market Size (2031) | USD 27.97 Billion |

| Growth Rate (2026 - 2031) | 3.88% CAGR |

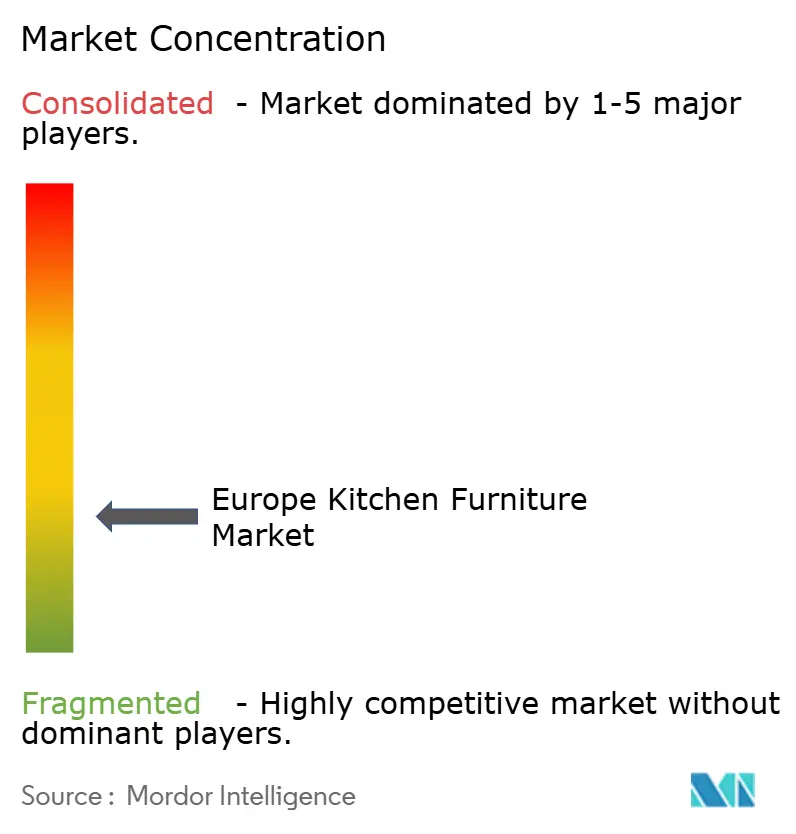

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Europe Kitchen Furniture Market Analysis by ���ϲ�����

The Europe kitchen furniture market reached a market size of USD 21.96 billion in 2025, is projected at USD 23.12 billion in 2026, and is forecast to reach USD 27.97 billion by 2031, reflecting a 3.88% CAGR during 2026–2031. Growth in the Europe kitchen furniture market continues to be anchored by renovation-driven purchasing, compliance-led retrofit cycles, and design refreshes that keep premium cabinetry on short planning horizons. Order conversion has been sensitive to housing finance conditions, yet installer-focused channels, BIM-ready project catalogs, and factory-finished modular units have reduced project risk for developers and homeowners. A structural shift in compliance is also underway as operators prepare for the EU Deforestation Regulation, which requires geolocation traceability for timber inputs and is leading many mid-sized OEMs to upgrade sourcing and digital audio capabilities. Rapid digitization of specification and showroom experiences is compressing design-to-manufacture lead times, supporting conversion in trade-focused and hybrid retail environments.

Key Report Takeaways

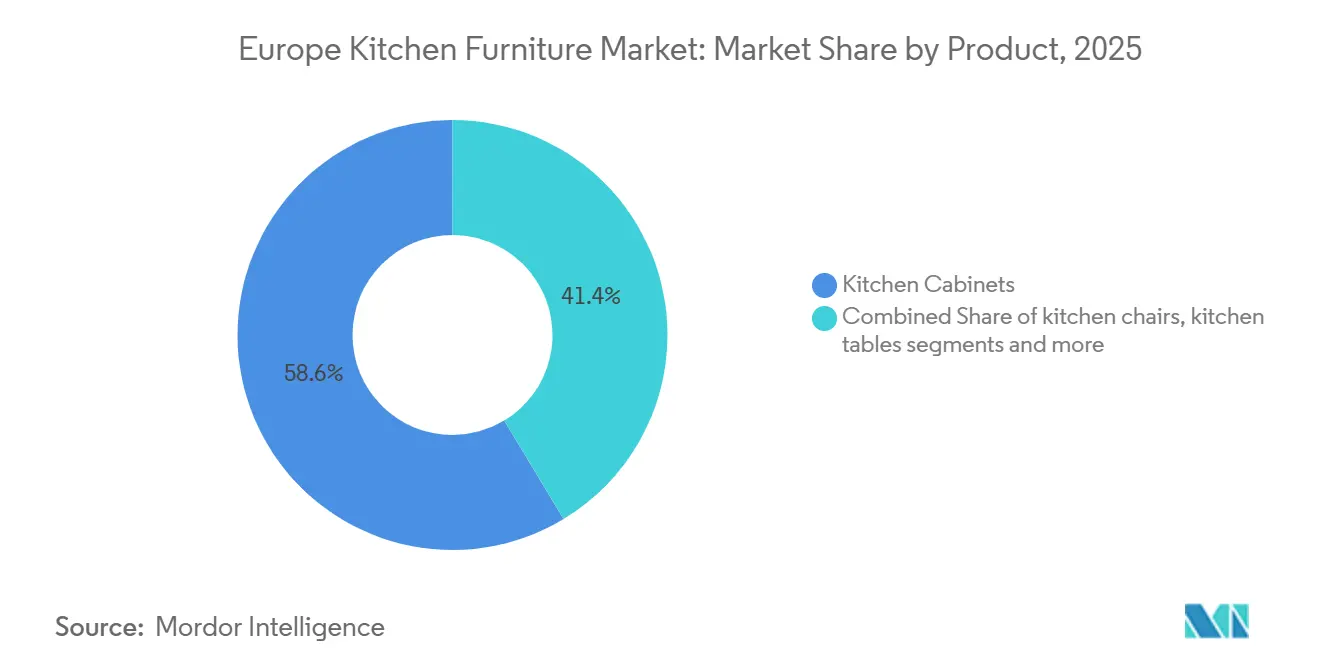

- By product, Kitchen Cabinets led with 58.64% revenue share in 2025 in Europe kitchen furniture market, while Kitchen Chairs are projected to expand at a 4.08% CAGR through 2031.

- By material, Wood held a 65.85% share in 2025, and Metal is projected to grow at 4.98%, the fastest rate among materials through 2031.

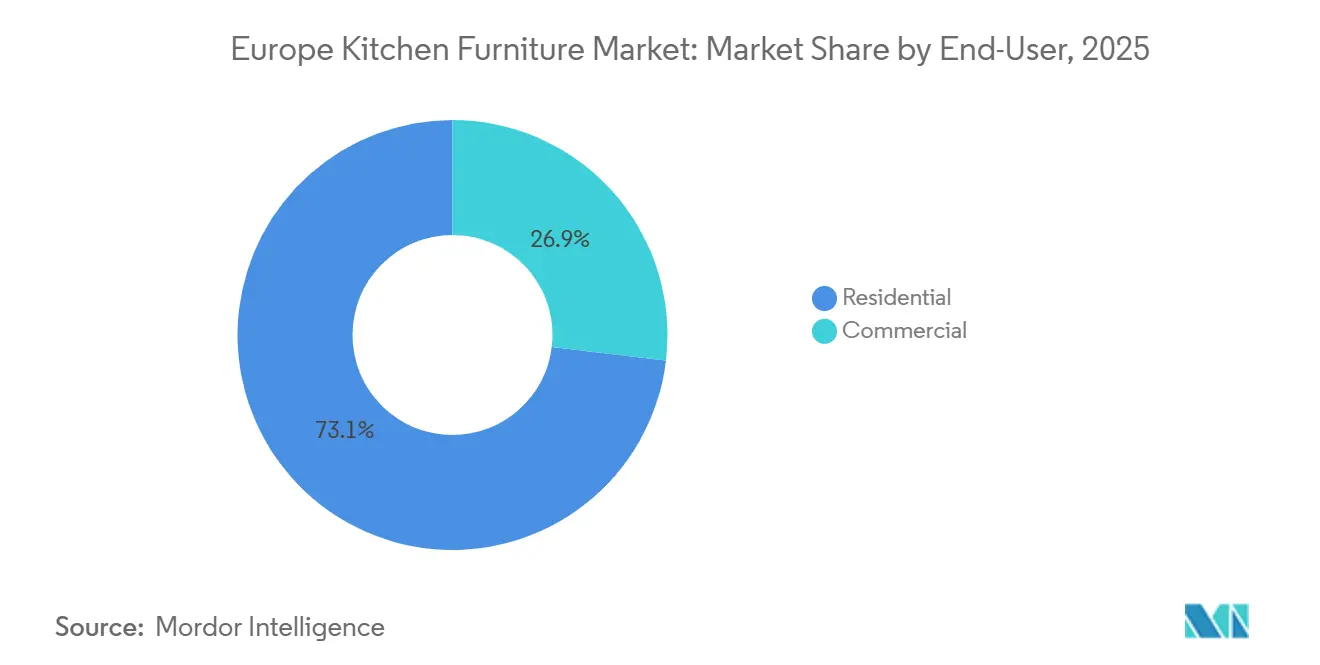

- By end-user, Residential accounted for 73.10% of 2025 sales in Europe kitchen furniture market, while Commercial is set to grow at a 5.48% CAGR through 2031.

- By distribution channel, B2C Retail captured 69.72% in 2025 in Europe kitchen furniture market, while B2B Project channels are expanding at a 5.05% CAGR through 2031.

- By geography, Germany held a 16.34% share in 2025, while France is forecast to record the fastest growth at a 4.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Kitchen Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Renovation and remodeling cycles sustain multi-year replacement demand | +1.8% | Germany, United Kingdom, France | Medium term (2-4 years) |

| Preference for modular, space-efficient, frameless kitchens | +1.2% | Global, early gains in Germany, BENELUX, Spain | Medium term (2-4 years) |

| Certified wood and circular materials gain share under EU sustainability norms | +0.7% | France, Netherlands, Nordics (PEFC/FSC baseline) | Long term (≥ 4 years) |

| Omnichannel retail and digitized showrooms lift conversion | +0.9% | Pan-European, Nordic click-and-collect pioneers | Short term (≤ 2 years) |

| EPBD-led energy renovations bundle kitchen upgrades in whole-home retrofits | +0.6% | France, Germany, Flanders | Medium term (2-4 years) |

| Build-to-rent and senior-living specify turnkey modular kitchens at scale | +0.4% | United Kingdom, Germany, Spain | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Renovation and Remodeling Cycles Sustain Multi-Year Replacement Demand

Europe’s aging housing stock keeps kitchen replacements on a steady cadence, less tied to new housing starts, which supports multi-year resilience in the Europe kitchen furniture market [1]European Investment Bank, “EU Housing Stock and Renovation Context,” European Investment Bank, eib.org . In 2025, segment momentum remained concentrated in specialist retail and trade channels that can mobilize installers and designers quickly when household budgets firm up. Replacement cycles are reinforced by consumer preference for higher-function cabinetry, upgraded storage, and layout reconfiguration that modernizes older homes. A larger share of planned household improvements is being directed to kitchens, driven by lifestyle gains and space optimization outcomes that are easy to visualize in digital planners. Countries with supportive subsidy frameworks and urban densification initiatives convert intent into project pipelines, which sustains stable demand for fitted cabinets, worktops, and integrated storage across the Europe kitchen furniture market.

Preference for Modular, Space-Efficient, Frameless Kitchens

Compact urban homes and changing household sizes are amplifying demand for frameless, modular units that maximize usable volume and streamline installation in the Europe kitchen furniture market. Manufacturers have responded with higher load-bearing base units, integrated storage, and improved hardware that allow small spaces to function more like full-size kitchens without visible clutter. Product updates entering showrooms in 2026 target clean lines and handle-free operation that simplify daily use while preserving a cohesive visual appearance. Rounded panels and softer edges have begun to diffuse the angular aesthetic of the prior decade while maintaining compatibility with modular grids, which speeds configuration and delivery. These features boost conversion in both residential and light-commercial settings as buyers prioritize ease of assembly, maintenance, and space efficiency in the Europe kitchen furniture market.

Certified Wood and Circular Materials Gain Share Under EU Sustainability Norms

Traceable wood and certified materials have moved from optional features to standard specifications in advanced European markets, a shift that is influencing sourcing strategies across the Europe kitchen furniture market. The EU Deforestation Regulation introduces geolocation traceability for timber inputs, accelerating investment in supplier transparency and digital compliance systems among medium- and large-scale operators. Circular take-back schemes are also expanding in Northern Europe, encouraging refurbishment and re-use of components, with retailers enhancing credit offers for returned modules. Leading German brands align material upgrades with sustainability messaging, combining certified content with anti-fingerprint surfaces and low-emission bonding processes to meet public-procurement and eco-label thresholds [2]Häcker Küchen, “Product Innovations and Technical Enhancements 2025,” Häcker Küchen, haecker-kuechen.de . These moves help defend share for wood-based cabinetry while enabling new value propositions in the premium tier of the Europe kitchen furniture market.

EPBD-Led Energy Renovations Bundle Kitchen Upgrades in Whole-Home Retrofits

Under the Energy Performance of Buildings Directive recast, Member States are rolling out renovation plans and minimum performance thresholds that bring kitchens into the scope of broader energy upgrades, creating bundled demand across the Europe kitchen furniture market. The renovation passport concept and one-stop-shop advisory services reduce administrative friction and support phased investment decisions that include cabinetry, ventilation, and layout optimization. As national programs encourage whole-home improvements, fitted kitchen upgrades often align with changes to HVAC, windows, and insulation for better energy outcomes. Budgetary allocations for eco-renovation encourage consumers to schedule kitchen works within the same contractors’ mobilization, which improves price certainty and completion timelines. This synchronized approach is lifting attachment rates for fitted cabinets and integrated storage within larger retrofit projects across the Europe kitchen furniture market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Weak housing starts and high rates are weighing on big-ticket purchases | -2.1% | Germany, France, the Netherlands | Short term (≤ 2 years) |

| Volatile wood/panel input costs and freight impact pricing | -0.9% | Pan-European, Nordic timber suppliers, Eastern European mills | Short term (≤ 2 years) |

| EUDR traceability adds compliance cost and supply risk in wood chains | -0.8% | Global, acute for suppliers to Italy, Spain small workshops | Medium term (2-4 years) |

| Installer/designer shortages extend lead times and raise project costs | -0.5% | Germany, France, the Netherlands, United Kingdom | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Weak Housing Starts and High Rates Weighing on Big-Ticket Purchases

Higher borrowing costs and soft housing transactions reduce willingness to commit to major kitchen upgrades, which dampens short-term momentum in the Europe kitchen furniture market. Younger cohorts face an affordability squeeze that limits the pipeline of first-time buyers who typically renovate within the early years of ownership. Elevated housing-cost burdens leave less discretionary budget for fitted cabinetry and premium finishes. Trade-focused channels continue to capture urgent replacement jobs, but full-scale remodels are postponed when consumer confidence softens. This environment favors value-engineered solutions and partial refresh programs that can be executed within compressed timelines.

EUDR Traceability Adds Compliance Cost and Supply Risk in Wood Chains

The EU Deforestation Regulation requires geolocation coordinates for timber inputs, adding documentation and audit requirements that small workshops may find difficult to meet. Secondary material flows, such as chips and sawmill by-products, complicate mapping and increase the time needed to build fully compliant chains of custody. Brands test third-party platforms and new procurement protocols to meet the compliance timeline. Well-prepared suppliers with established certification practices are positioned to gain orders as buyers consolidate around verifiable sources. The transition period introduces supply risks and incremental costs, which can weigh on margins and delivery times in the Europe kitchen furniture market.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Cabinets Lead While Seating Accelerates in Projects

Kitchen Cabinets held the largest share at 58.64% in 2025, reflecting steady attachment rates in renovation-led orders and strong design refresh cycles within the Europe kitchen furniture market. Kitchen Chairs are projected to grow at a 4.08% CAGR through 2031 as hospitality and workplace pantry zones standardize seating packages during refresh programs. Within the Europe kitchen furniture market, cabinetry updates continue to anchor project scopes because door styles, internal storage, and layout changes deliver visible gains for homeowners. Seating gains velocity in commercial and semi-commercial settings where higher traffic and layout changes drive faster replacement cycles. The Europe kitchen furniture industry is also seeing product clustering around modular islands and bar seating, which supports quick-serve and collaborative use cases in offices and boutique hotels.

The Europe kitchen furniture market benefits from frequent style updates by leading brands, which help maintain consumer interest and shorten planning cycles. Nobilia’s 2026 collection introduced new fronts and clean-lined ranges to address urban buyers who favor seamless, handle-free designs. Schüller’s product updates focus on refined forms that remain compatible with modular grids, which helps retailers compress design approval and installation schedules. Häcker’s technical enhancements to base units lift load capacity and usable space, a practical improvement that resonates in compact homes and small commercial settings. These actions reinforce cabinetry leadership while seating grows faster off a smaller base, a pattern that will shape the Europe kitchen furniture market through 2031.

By Material: Wood Dominates While Metal Gains on Durability and Aesthetics

Wood maintained a 65.85% share in 2025, supported by consumer familiarity, warmth of finishes, and compatibility with certified sourcing frameworks across the Europe kitchen furniture market. Metal is projected to be the fastest-growing material, with a 4.98% CAGR through 2031, as durable, easy-to-clean surfaces gain traction in premium residential and light-commercial spaces. The Europe kitchen furniture industry continues to innovate on wood with synchronized pore veneers, anti-fingerprint coatings, and low-emission edge bonding that improve both performance and sustainability credentials. At the same time, metal cabinetry aligns with industrial and monochrome palettes that pair well with integrated appliances, which has expanded its consideration in lofts and open-plan layouts. This mix underpins stable leadership for wood while setting a higher growth runway for metal in the Europe kitchen furniture market.

Suppliers are refining product catalogues to meet compliance and performance expectations across both materials. Häcker’s 2025 updates added surfaces and bonding technologies that meet strict emission criteria, which is important for public tenders and eco-conscious consumers. Brand storytelling around certified content and circularity helps wood defend its position, while metal’s durability supports lifecycle value in commercial settings. For retailers, pairing modular metal units with premium worktops and storage hardware creates distinct price bands for upselling. These dynamics help maintain healthy category segmentation in the Europe kitchen furniture market.

By End-User: Residential Dominates While Commercial Accelerates on Hospitality and Workplace Refresh

Residential accounted for 73.10% of sales in 2025, reflecting the central role of kitchens in home comfort and buyer priorities across the Europe kitchen furniture market. Commercial is projected to grow at 5.48% through 2031 as hotels, multi-family operators, and offices standardize turnkey kitchen packages to compress fit-out schedules and ensure consistent quality at scale. The Europe kitchen furniture market for Residential continues to benefit from digital planners and modular storage, which streamline decision-making for households and installers. In Commercial, long-run demand is tied to formula-based design, accessibility standards, and accelerated site programs where factory-finished units reduce rework. Trade-focused networks that offer same-day pickup and local availability help capture urgent Commercial replacements.

Residential growth remains tied to remodeling intent, especially when households prioritize kitchen upgrades in multi-room improvements. Commercial adoption of modular, BIM-ready catalogues is expanding as developers use pre-validated models to minimize design risk and speed procurement. Operators in senior living and build-to-rent focus on long-life materials and standardized dimensions to preserve serviceability across portfolios. These adoption patterns sustain leadership for Residential while setting a higher growth slope for Commercial within the Europe kitchen furniture market.

By Distribution Channel: B2C Retail Leads While B2B Project Builds Scale with BIM and Turnkey Models

B2C Retail captured 69.72% of 2025 sales as consumers continued to rely on tactile showroom experiences and consultative selling for fitted kitchens in the Europe kitchen furniture market. B2B Project channels are expanding at a 5.05% CAGR through 2031 as developers and operators deploy turnkey modular specifications that integrate with BIM workflows for faster, lower-risk delivery. Retailers invest in visualization and layout tools that reduce friction between discovery and purchase, while trade networks win share by compressing response times for installers and site teams. The Europe kitchen furniture market share captured by B2C remains high, but project-based demand is growing quicker as standardized units become the default for multi-site portfolios.

On the project side, manufacturers that maintain Revit-compatible libraries and ERP integration help architects and builders shorten submittal and procurement times. This unlocks time savings and lowers change-order risk for developers. In retail, upgraded surfaces and refined front options maintain strong attachment rates for premium finishes. These channel dynamics align well with the Europe kitchen furniture market, where both consumer and developer needs are met with specialized value propositions.

Geography Analysis

Germany accounted for 16.34% of regional value in 2025 on the back of concentrated manufacturing clusters and export-ready logistics that support high-volume cabinet lines in the Europe kitchen furniture market. France is projected to be the fastest-growing national market with a 4.62% CAGR through 2031, supported by urban densification and policy-driven renovation frameworks that influence whole-home upgrades, including kitchens. Spain’s coastal zones continued to benefit from hospitality refresh programs that emphasize kitchen functionality in rental properties, a pattern that channels spend into fitted units and storage solutions across the Europe kitchen furniture market.

Italy’s artisanal clusters face operational strain from stricter traceability requirements and shifting mid-tier pricing amid intensified competitive pressure from online channels. In the Nordics, circular take-back pilots and strong consumer interest in certified materials have set a higher performance bar for cabinetry and finishes. BENELUX markets continue to upgrade to factory-finished modular units that simplify site coordination in dense urban environments. These region-specific patterns contribute to a stable base of demand across the Europe kitchen furniture market and support a hybrid of retail and project-driven orders.

Within key countries, policy and channel execution matter. France’s eco-renovation frameworks and urban space constraints amplify demand for compact, full-height cabinet solutions that integrate with energy upgrades [3]Efficient Buildings Europe, “Renovation Frameworks and Timelines,” Efficient Buildings Europe, efficientbuildings.eu . Germany’s manufacturers continue to invest in robotics and precision machining to enhance throughput and quality for domestic and export orders. The United Kingdom’s depot model has demonstrated resilience, meeting installer requirements for rapid fulfillment and reliable availability. This combination of policy tailwinds, industrial capability, and channel specialization is central to the outlook for the Europe kitchen furniture market through 2031.

Competitive Landscape

Competition in the Europe kitchen furniture market balances scale advantages against strong regional brands that compete on design, availability, and compliance-readiness. Operators with established factory automation and digital showrooms are compressing design-to-order windows and lifting conversion in both retail and project channels. Investment priorities include robotic drilling, edge-banding, and improved procurement systems that absorb traceability requirements without slowing delivery. This has reinforced incumbents’ ability to update ranges annually or biennially and to maintain price bands that address entry, mid, and premium tiers across the Europe kitchen furniture market.

Product news underscores design and performance as durable differentiators. Nobilia’s 2026 collection introduced new fronts and clean-lined ranges that reflect urban preferences for minimal, integrated looks. Schüller expanded forms that balance softer profiles with grid compatibility, which helps dealers reuse plans across models and manage lead times [4]Schüller Möbelwerk, “Product Evolution,” Schüller, schuller.de . Häcker’s 2025 exhibition highlighted capacity and usability upgrades in base units and premium surfaces, aligning technical improvements with consumer-friendly narratives on function and sustainability. Retail and trade networks capable of near-immediate fulfillment, such as well-distributed depot models, continue to set the pace in service levels inside the Europe kitchen furniture market.

Corporate actions have reshaped portfolios and cost structures as players refocus on core markets and automate to counter labor and compliance headwinds. A major Nordic group streamlined operations through divestments and capacity investments, with the aim of bringing unit costs down over the medium term. Trade-focused operators reported record peak-trading outcomes in 2025, validating strategic bets on network density and manufacturing upgrades that support rapid product rollouts and high service levels. Retail consolidation and logistics optimization among large furniture groups also influence kitchen category visibility and price points in Central Europe, thereby affecting share dynamics within the Europe kitchen furniture market.

Europe Kitchen Furniture Industry Leaders

Nobilia

Nobia AB

Häcker Küchen

Schmidt Groupe

Howdens Joinery Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Nobia AB divested its United Kingdom operations to Alteri Partners for no upfront purchase price, with the buyer assuming USD 81.2 million in lease obligations. The group also announced a USD 16.2 million rights issue to fund the Nobia Park automated facility, aiming to achieve a 15% cost reduction by 2027.

- November 2025: Howdens reported record peak-trading-period sales to November 1, adding USD 10.8 million incremental revenue and pushing group growth to 3.5%, while maintaining plans to open additional depots.

- September 2025: Häcker Küchen unveiled new fronts and technical enhancements at its “the Art of Harmony” in-house exhibition, including increased base-unit capacity and expanded premium surface options.

- February 2024: Nobia AB completed a sale-leaseback of its Tidaholm factory to free capital for digital showrooms and commissioning of the Nobia Park facility.

Europe Kitchen Furniture Market Report Scope

A complete background analysis of the European kitchen Furniture market, which includes an assessment of emerging trends by segments, significant changes in market dynamics, and market overview, is covered in the report. The report also features the qualitative and quantitative assessment by analysing data gathered from industry analysts and market participants across various key points in the industry's value chain. The United Kingdom Kitchen Furniture Market is segmented by product (kitchen cabinets, kitchen chairs, kitchen tables, and others), by material (wood, metal, plastic & polymer, and other materials), by end-user (residential and commercial), by distribution channel (B2C retail and B2B project), and by region (United Kingdom, Germany, France, Spain, Italy, BENELUX (Belgium, Netherlands, Luxembourg), NORDICS (Denmark, Finland, Iceland, Norway, Sweden), and Rest of Europe). The report also covers the market sizes and forecasts for the United Kingdom Kitchen Furniture market in value (USD) for all the above segments.

By Product

| Kitchen Cabinets |

| Kitchen Chairs |

| Kitchen Tables |

| Other Products (trolley, cart, pantry shelves) |

By Material

| Wood |

| Metal |

| Plastic & Polymer |

| Other Materials |

By End-User

| Residential |

| Commercial |

By Distribution Channel

| B2C / Retail | Home Centers |

| Specialty Furniture Stores | |

| Online | |

| Other Distribution Channels | |

| B2B / Project |

By Geography

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| BENELUX (Belgium, Netherlands, Luxembourg) |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) |

| Rest of Europe |

| By Product | Kitchen Cabinets | |

| Kitchen Chairs | ||

| Kitchen Tables | ||

| Other Products (trolley, cart, pantry shelves) | ||

| By Material | Wood | |

| Metal | ||

| Plastic & Polymer | ||

| Other Materials | ||

| By End-User | Residential | |

| Commercial | ||

| By Distribution Channel | B2C / Retail | Home Centers |

| Specialty Furniture Stores | ||

| Online | ||

| Other Distribution Channels | ||

| B2B / Project | ||

| By Geography | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the current Europe kitchen furniture market size and growth outlook to 2031?

The Europe kitchen furniture market size is USD 23.12 billion in 2026 and is projected to reach USD 27.97 billion by 2031 at a 3.88% CAGR, supported by renovation-driven demand and compliance-led retrofits.

Which product categories are leading, and which are growing fastest in Europe?

Cabinets lead with 58.64% share in 2025, while chairs are the fastest-growing product with a projected 4.08% CAGR through 2031 in the Europe kitchen furniture market.

Which materials are gaining traction in the Europe kitchen furniture market?

Wood remains dominant with a 65.85% share in 2025, while metal is the fastest-growing material, driven by durability and aesthetic trends in residential and light-commercial spaces.

How are distribution channels evolving for kitchen furniture in Europe?

B2C retail remains the largest channel at 69.72% in 2025, while B2B project channels are expanding at 5.05% as developers adopt turnkey modular kitchens and BIM-based specifications.

Which European countries are set to drive the fastest growth?

France is projected to post the fastest growth with a 4.62% CAGR through 2031, supported by renovation frameworks and urban densification policies.

What are the main headwinds for the Europe kitchen furniture market in the near term?

Short-term headwinds include higher borrowing costs affecting big-ticket purchases and the added compliance burden from EUDR traceability requirements for timber inputs.

Page last updated on: