Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

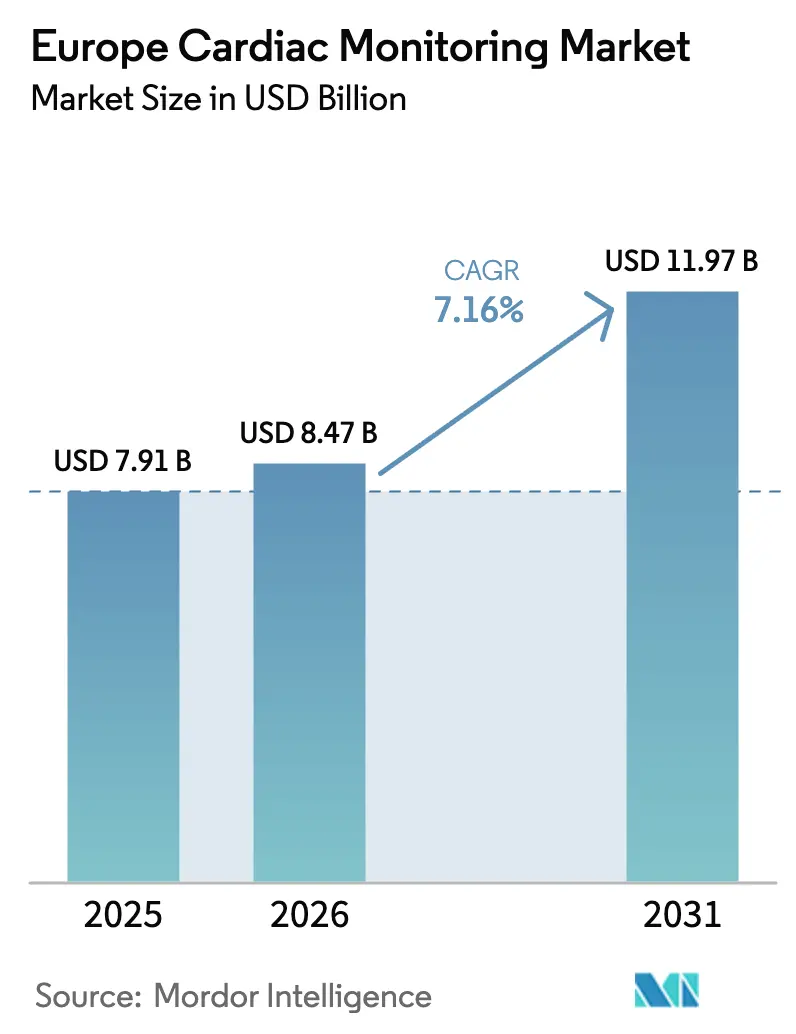

| Base Year Market Size (2025) | USD 7.91 Billion |

| Market Size (2026) | USD 8.47 Billion |

| Market Size (2031) | USD 11.97 Billion |

| Growth Rate (2026 - 2031) | 7.16% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Europe Cardiac Monitoring Market Analysis by ���ϲ�����

The Europe Cardiac Monitoring Market size is projected to expand from USD 7.91 billion in 2025 and USD 8.47 billion in 2026 to USD 11.97 billion by 2031, registering a CAGR of 7.16% between 2026 to 2031.

Demographic pressure remains intense cardiovascular disease caused 42.5% of all deaths in the WHO European Region in 2024 [1]World Health Organization, “Cardiovascular Diseases,” WHO.INT. Public-policy momentum is equally strong; the European Commission’s Safe Hearts Plan earmarked EUR 1.2 billion for prevention and early detection from 2025 to 2030. Reimbursement reforms are also catalyzing the European cardiac monitoring market: Germany’s 2026 DRG catalogue created code F41Z for bundled AMI care, while the NHS Payment Scheme 2025/26 funds ambulatory blood-pressure monitoring machines.

Key Report Takeaways

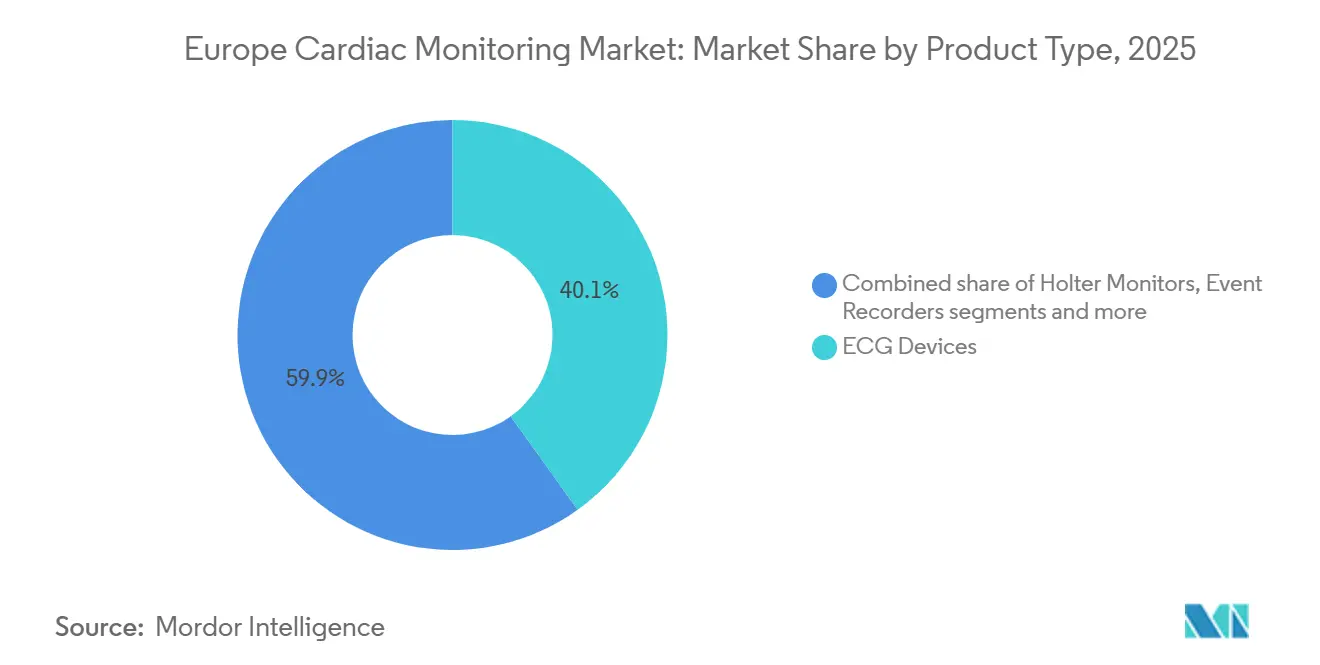

- By product type, ECG devices led with 40.1% of Europe cardiac monitoring market share in 2025. Smart wearable monitors are forecast to expand at a 7.81% CAGR through 2031, the fastest among product categories.

- By end user, hospitals held 49.12% share of the European cardiac monitoring market size in 2025. Home-care settings are advancing at an 8.11% CAGR to 2031, the highest end-user growth rate.

- By geography, Germany captured 35.34% revenue share in 2025. The United Kingdom is projected to post the quickest regional expansion at a 7.37% CAGR through 2031

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Cardiac Monitoring Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of CVD among Europe’s ageing population | +1.8% | Pan-European, acute in Germany, Italy, Spain | Long term (≥ 4 years) |

| Shift toward ambulatory and remote cardiac monitoring | +2.1% | Germany, UK, Nordics; nascent in CEE | Medium term (2-4 years) |

| Technological advances in wearable ECG devices | +1.5% | Western Europe core, spillover to urban CEE | Short term (≤ 2 years) |

| Favorable DRG and national tariff reimbursement updates | +1.3% | Germany, UK, France; pilots in Poland, Czech Republic | Medium term (2-4 years) |

| AI-driven predictive analytics in Holter datasets | +0.9% | Early adoption in Germany, UK, Netherlands | Medium term (2-4 years) |

| Emergence of tele-cardiology hubs in Central & Eastern Europe | +0.7% | Poland, Romania, Hungary, Czech Republic | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Rising Prevalence of CVD Among Europe’s Ageing Population

Cardiovascular disease claimed 1.7 million European lives in 2024, equal to 42.5% of all regional deaths. The Safe Hearts Plan mandates risk screening for adults over 40 by 2028, expanding the candidate pool for continuous rhythm surveillance. Hypertension control rates stand at only 38% across the EU, revealing an unmet need that wearable and patch-based ECG can address. Eurostat projects seniors (≥ 65 years) will rise to 24.8% of the EU population by 2030 concentrating demand in Germany, Italy, and Spain [2]Eurostat, “Population Structure and Ageing,” EUROSTAT.EC.EUROPA.EU. Vendors that position devices as chronic-disease-management tools rather than episodic diagnostics are poised to benefit from capitated payment models that reward outcomes.

Shift Toward Ambulatory and Remote Cardiac Monitoring

Payment incentives are migrating from inpatient to outpatient settings. Germany’s Hospital Reform Act moved select cardiac procedures into flat-rate bundles that financially encourage early discharge [3]Bundesministerium für Gesundheit, “Hospital Reform Act 2025,” BMG.BUND.DE. In the United Kingdom, the 2025/26 Payment Scheme set separate tariffs for ambulatory BP monitoring and Pro-BNP testing, formally recognizing diagnostics performed outside hospital walls. France’s August 2025 intra-DRG update now pays higher rates when remote telemetry triggers clinical action. These changes redirect purchasing power toward mobile cardiac telemetry and event recorders, forcing manufacturers to cultivate payer relationships and validate cost-per-diagnosis advantages.

Technological Advances in Wearable ECG Devices

Regulatory clearances for consumer wearables with medical-grade ECG functions accelerated after 2024. Apple Watch Series 10 received FDA approval for atrial-fibrillation detection and sleep-apnea notifications in September 2024. Samsung Galaxy Watch 7 followed in July 2024, while Garmin’s ECG app cleared in February 2024. Installed bases now exceed 45 million units across Europe, blurring the boundary between wellness and diagnosis. Clinical credibility is solidifying; Corsano’s wrist PPG monitor delivered 94.2% sensitivity for continuous AF detection in a 2025 study. As general practitioners increasingly prescribe smartwatches for first-line screening, traditional 24-hour Holter demand is likely to shift toward confirmatory testing only.

Favorable DRG and National Tariff Updates

Germany’s 2026 DRG catalogue introduced code F41Z bundling AMI treatment with mandatory 30-day post-discharge monitoring. The Hybrid-DRG expansion to 575 mixed inpatient-outpatient codes now reimburses event-recorder placement and implantable loop recorder insertion. In France, telemetry now carries severity modifiers that reward providers when data lead to interventions. The UK has carved out Clinical Decision-Making tariffs for out-of-hospital diagnostics, ending the historic lump-sum approach. These reforms unlock budgets yet impose stricter documentation, nudging smaller clinics toward integrated IT platforms.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent EU-MDR compliance costs | -1.2% | Pan-European, the highest pressure on SMEs | Medium term (2-4 years) |

| Data-privacy hurdles under GDPR | -0.8% | EU-wide, enforcement variability by member state | Short term (≤ 2 years) |

| Shortage of trained electrophysiologists | -0.6% | Central & Eastern Europe; rural Western Europe | Long term (≥ 4 years) |

| Specialty lithium-battery supply constraints | -0.5% | Global impacts on implantable device production | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Stringent EU-MDR Compliance Costs

EU-MDR transitional deadlines converged in 2024-2025, forcing legacy devices through costly re-certification. Article 10a obliges firms to warn regulators of any supply interruption within 48 hours, elevating compliance risk. Post-market surveillance burdens intensified after MDCG 2024-1 guidance, which mandates quarterly safety summaries for high-risk cardiac products. Notified-body scarcity stretches audit queues to 18-24 months, delaying launches and increasing costs beyond EUR 500,000 for a Class IIb monitor—barriers that disproportionately hurt small manufacturers.

Data-Privacy Hurdles Under GDPR

Cardiac telemetry qualifies as special-category data under Article 9, requiring explicit multi-step consent. The European Data Protection Board’s 2024 guidelines invalidated bundled consents and mandated end-to-end encryption. Enforcement actions are mounting: Germany issued EUR 3.2 million in fines against telehealth providers in 2024, while France’s CNIL levied EUR 1.5 million for inadequate ECG encryption. To comply, vendors must invest in pseudonymization architectures and regional data centers, raising per-patient service costs and slowing adoption in resource-constrained systems.

Segment Analysis

By Product Type: Wearables Disrupt Traditional Holter Dominance

ECG devices accounted for 40.1% of Europe's cardiac monitoring market share in 2025, underpinned by hospital demand for 12-lead systems. . Yet smart wearable monitors are projected to post a 7.81% CAGR to 2031, outpacing every other category. This surge reflects FDA-cleared consumer devices such as Apple Watch Series 10 and Samsung Galaxy Watch 7 that push diagnostics closer to the patient. Holter monitors remain relevant for 24- to 48-hour studies, but extended-wear patches offering 14-day recordings are eroding demand. Mobile cardiac telemetry, which delivers real-time data over 30 days, bridges the gap between ambulatory patches and implantable loop recorders, the latter commanding premium pricing above USD 3,000 per unit. Boston Scientific’s Bluetooth-enabled LUX-Dx II+ extends battery life to 4.5 years, reducing replacement procedures and aligning with value-based quotas.

The Europe cardiac monitoring market size for implantable solutions is poised to expand as regulatory guidance now treats AI algorithms as Class IIb devices, permitting software-only vendors to partner with hardware OEMs. Cardiologs, for example, licensed its arrhythmia-detection engine to three manufacturers in 2024, embedding predictive analytics natively and shrinking post-processing times. Competitive differentiation is therefore shifting from hardware ergonomics to cloud interoperability and analytic accuracy.

By End User: Home-Care Settings Outpace Hospital Growth

Hospitals controlled 49.12% of Europe cardiac monitoring market size in 2025, but bundled-payment reforms are redirecting patients toward lower-acuity venues. Home-care settings, supported by insurer reimbursement for remote patient monitoring, are forecast to grow at 8.11% CAGR through 2031. Germany’s DRG bundles now include 30-day telemetry post-AMI, an incentive for mobile monitoring devices. The NHS Long Term Plan targets 30% of outpatient cardiology visits to be delivered virtually by 2027, explicitly funding in-home ECG transmission.

Cardiac centers and clinics, currently holding a significant portion of market revenue, benefit from rapid Holter turnaround and specialist interpretation without hospital overhead. Ambulatory surgical centers (ASCs) are gaining share for implantable loop recorder insertions, cutting procedure costs by up to 50% compared with inpatient settings. Retail health pilots by CVS and Walgreens demonstrate emerging demand for opportunistic AF screening, though reimbursement remains embryonic.

Geography Analysis

Germany represented 35.34% of Europe cardiac monitoring market share in 2025, thanks to Hybrid-DRG expansion and a decentralized network of 1,893 acute-care hospitals. Reimbursement uniformity across statutory insurers reduces regional pricing volatility, sustaining equipment refresh cycles. The Europe cardiac monitoring market size in Germany is also buoyed by early AI adoption; university hospitals in Munich and Berlin integrated algorithmic arrhythmia triage into routine workflows during 2025.

The United Kingdom is the fastest-growing geography at a projected 7.37% CAGR through 2031. Clinical Decision-Making tariffs separated out-of-hospital diagnostics from general cardiology consults, freeing GBP 250 million for virtual pathway expansion. Tele-cardiology hubs launched across integrated care systems cut wait times for rhythm interpretation in underserved regions such as Cornwall and Cumbria, demonstrating scalable demand beyond metropolitan areas.

France, Italy, and Spain collectively account for a notable share of Europe cardiac monitoring market size. France’s intra-DRG severity modifiers reward telemetry that triggers clinical action, aligning financial incentives with outcome-based care. Italy’s National Recovery and Resilience Plan committed EUR 1.67 billion to digital health infrastructure but faces procurement delays at regional levels.

Spain’s Catalonia pilot reduced cardiology referrals by significantly, validating cloud-based ECG triage yet awaiting national rollout. Rest of Europe (Nordics, Central and Eastern Europe, Benelux, and smaller Western nations) makes up the remaining share. Poland is investing PLN 800 million (USD 200 million) in 15 tele-cardiology hubs, while the Czech Republic links rural hospitals to Prague’s IKEM center for real-time ECG reviews. Workforce shortages, particularly electrophysiologists, remain a binding constraint in many CEE regions.

Competitive Landscape

The Europe cardiac monitoring market is moderately concentrated: the top five players, Medtronic, GE HealthCare, Koninklijke Philips, Abbott, and Boston Scientific, control the majority of revenue. These incumbents leverage installed bases and proprietary cloud ecosystems that lock in customers through multi-year service contracts. GE HealthCare’s MUSE NX and Philips’ IntelliSpace platforms aggregate multi-modality data, creating switching costs for hospitals that have harmonized workflows around single-vendor ecosystems.

Disruptors target software margins rather than hardware volume. Cardiologs reported that algorithm licensing rose from 12% to 38% of its revenue between 2022 and 2024, signaling decoupling of value from physical devices. Patent filings echo this shift: Boston Scientific filed 14 applications in 2024 covering miniaturized sensors and wireless power transfer, while iRhythm lodged nine patents for skin-friendly adhesive electrodes.

White-space opportunities focus on heart-failure hemodynamics and pre-symptomatic arrhythmia prediction. Vectorious’ V-LAP left-atrial pressure sensor gained CE mark and is undergoing post-market surveillance in Germany and the Netherlands. Nordic specialist Bittium retains dominance in research-grade ECG among Scandinavian universities, while Swiss-based Schiller defends its niche in portable 12-lead systems for physician offices.

Europe Cardiac Monitoring Industry Leaders

Abbott Laboratories

Medtronic

Boston Scientific Corporation

GE Healthcare

Koninklijke Philips N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Biotronik launched the world's first CRT-D systems specifically approved for conduction system pacing.

- January 2026: Medtronic Plc announced the CE Mark for the Sphere-360 PFA catheter, a "single-shot" pulsed field ablation system for treating atrial fibrillation.

- May 2025: Philips launched the first commercial AI-ECG platform. They also introduced the VeriSight Pro 3D intracardiac echo catheter in Europe to provide higher-precision imaging during cardiac procedures.

Europe Cardiac Monitoring Market Report Scope

As per the scope of the report, cardiac monitoring devices are essential medical tools used to track the heart's electrical activity, heart rate, and rhythm to diagnose and manage various cardiovascular conditions

The Europe Cardiac Monitoring Market is segmented by product, end-user, and geography. By product, it is segmented into ECG devices, Holter monitors, event recorders, mobile cardiac telemetry, implantable loop recorders, and smart wearable monitors. By End users, the market is segmented into hospitals, cardiac centers & clinics, home-care settings, ambulatory surgical centers, and others. Geographically, the market is segmented across Germany, the United Kingdom, France, Italy, Spain, and the rest of Europe. For each segment, the market size and forecast are provided in terms of value (USD).

By Product Type

| ECG Devices |

| Holter Monitors |

| Event Recorders |

| Mobile Cardiac Telemetry |

| Implantable Loop Recorders |

| Smart Wearable Monitors |

By End User

| Hospitals |

| Cardiac Centres & Clinics |

| Home-Care Settings |

| Ambulatory Surgical Centres |

| Others |

By Country

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Product Type | ECG Devices |

| Holter Monitors | |

| Event Recorders | |

| Mobile Cardiac Telemetry | |

| Implantable Loop Recorders | |

| Smart Wearable Monitors | |

| By End User | Hospitals |

| Cardiac Centres & Clinics | |

| Home-Care Settings | |

| Ambulatory Surgical Centres | |

| Others | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe cardiac monitoring market in 2026?

It is expected to reach USD 8.47 billion, on track to reach USD 11.97 billion by 2031.

Which product category is growing fastest?

Smart wearable monitors are advancing at a 7.81% CAGR through 2031.

Why is home-care monitoring accelerating?

Bundled-payment reforms and payer reimbursement for remote telemetry are driving 8.11% CAGR growth in home settings.

Which country leads in revenue?

Germany held 35.34% of 2025 revenue, supported by Hybrid-DRG expansion.

What is the main regulatory hurdle for manufacturers?

EU-MDR compliance, particularly Article 10a supply-interruption rules and stringent post-market surveillance.

Page last updated on: