Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

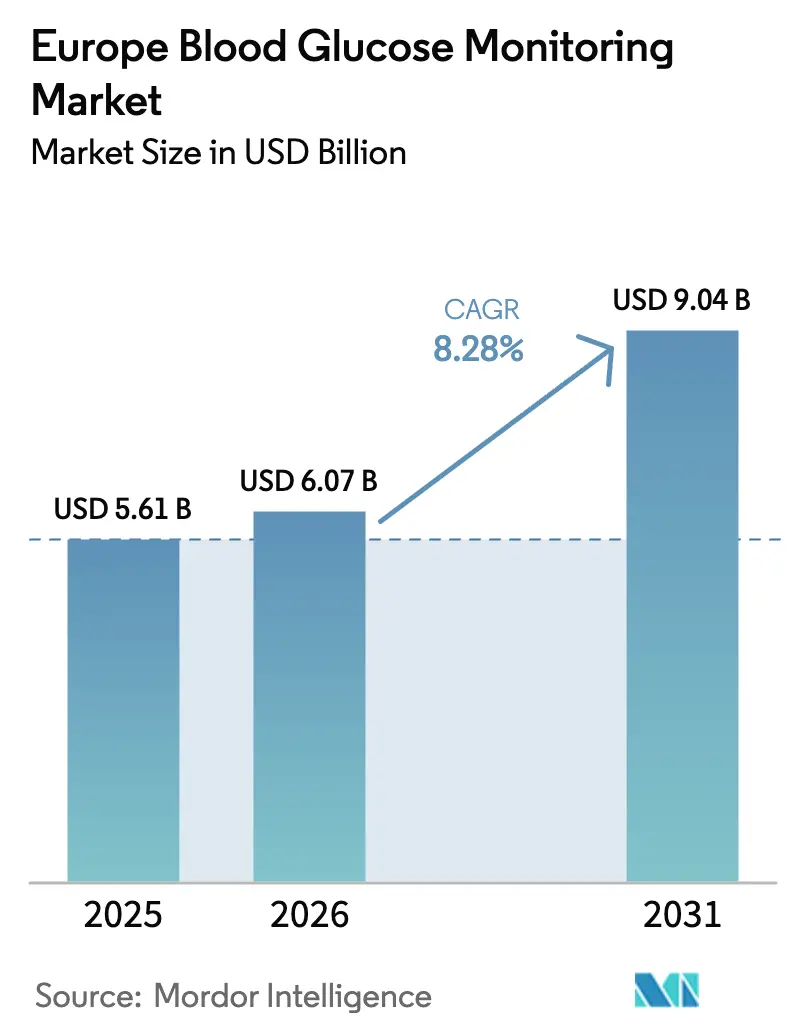

| Base Year Market Size (2025) | USD 5.61 Billion |

| Market Size (2026) | USD 6.07 Billion |

| Market Size (2031) | USD 9.04 Billion |

| Growth Rate (2026 - 2031) | 8.28% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Europe Blood Glucose Monitoring Market Analysis by ���ϲ�����

The Europe Blood Glucose Monitoring Market size is expected to grow from USD 5.61 billion in 2025 to USD 6.07 billion in 2026 and is forecast to reach USD 9.04 billion by 2031 at 8.28% CAGR over 2026-2031.

Spurring this climb are statutory payor decisions that now underwrite continuous glucose monitoring (CGM) for virtually every insulin-treated patient in Germany and the United Kingdom, rising uptake of hybrid closed-loop insulin delivery systems that require sensor data every five minutes, and an aging population that pushes diabetes prevalence higher each year across the EU-27. Competitive pricing for CGM sensors has narrowed the historic cost gap with self-monitoring blood glucose (SMBG) strips, allowing CGM to penetrate non-intensively treated Type-2 cohorts in France, Italy, and Spain. At the same time, national tele-diabetes programs in the Nordic region have normalised virtual follow-ups, shifting device purchasing power from hospitals to consumers and helping homecare emerge as the dominant end-user channel. Finally, regulatory pressure to reduce single-use plastics is accelerating design changes toward reusable transmitters, giving incumbents a fresh differentiator while dissuading low-cost SMBG entrants.

Key Report Takeaways

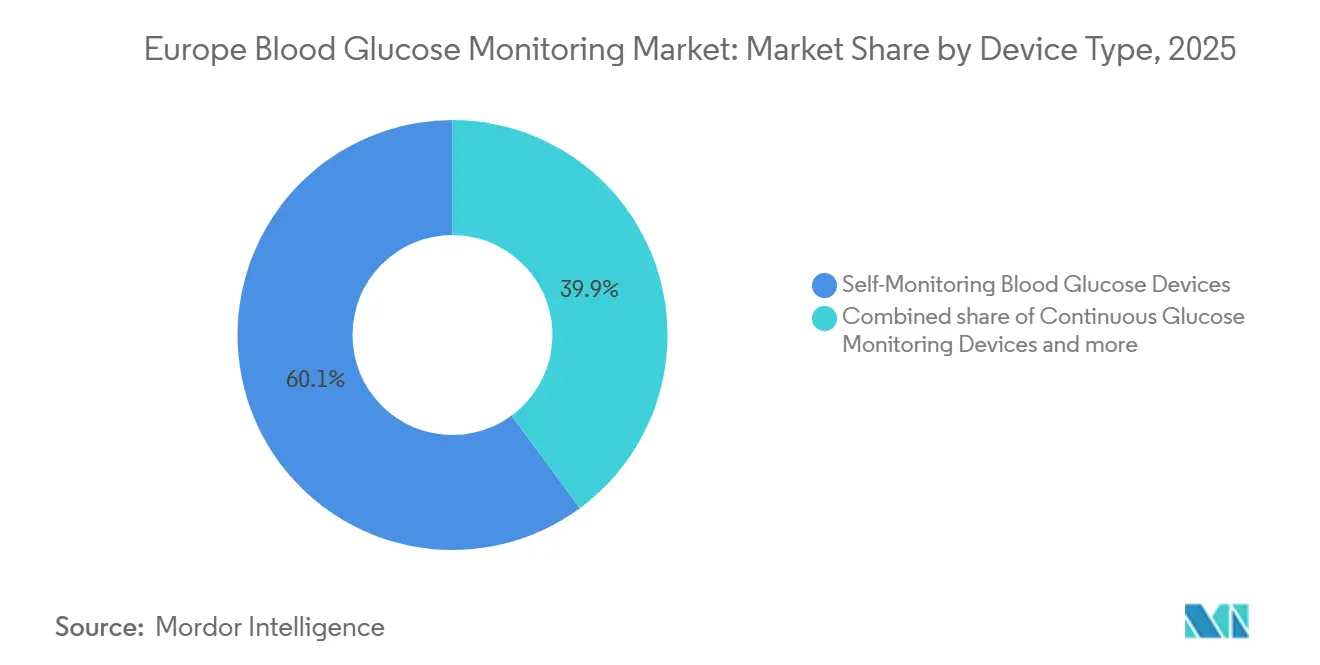

- By device type, SMBG retained 60.1% of Europe blood glucose monitoring market share in 2025, while CGM leads future growth at a 10.23% CAGR through 2031.

- By diabetes type, Type-2 diabetes commanded a 73.21% share of the European blood glucose monitoring market in 2025; Type-1 diabetes is projected to advance at a 13.5% CAGR to 2031.

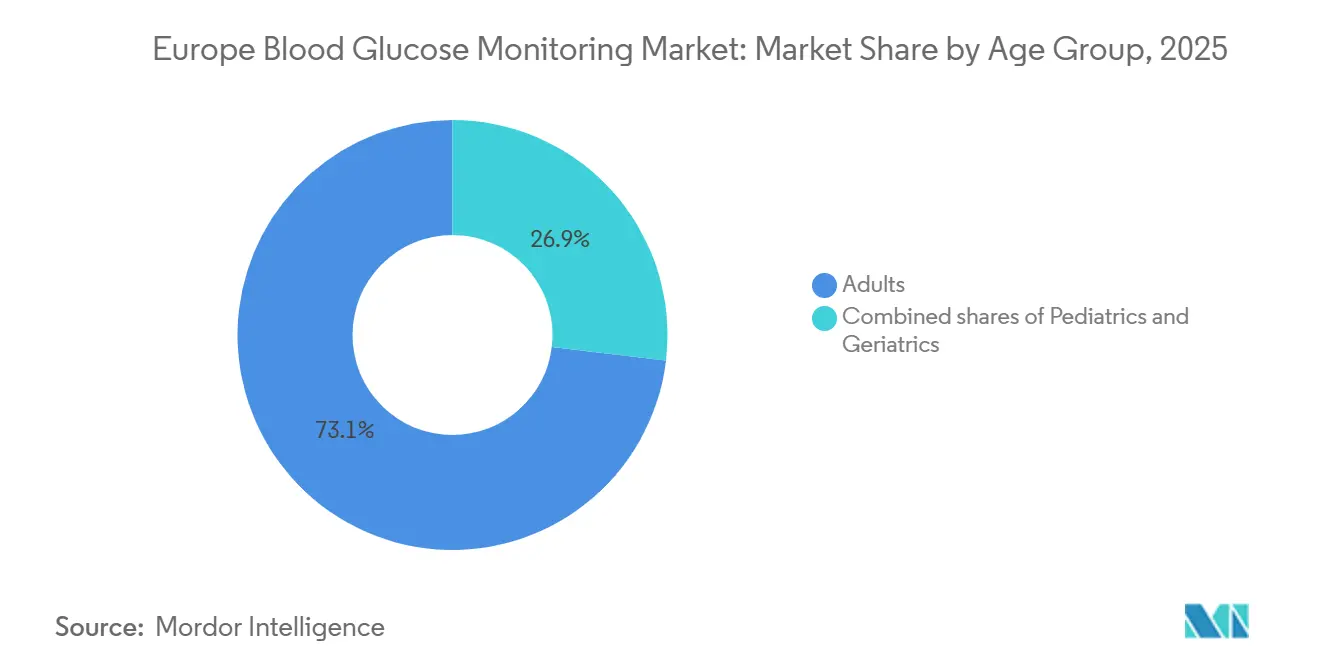

- By age group, adults held 73.1% share in 2025, whereas the pediatric cohort is poised to grow at 14.31% CAGR through 2031.

- By test type, invasive methods accounted for 59.12% of the European blood glucose monitoring market size in 2025; non-invasive platforms are forecast to expand at 10.78% CAGR over the same period.

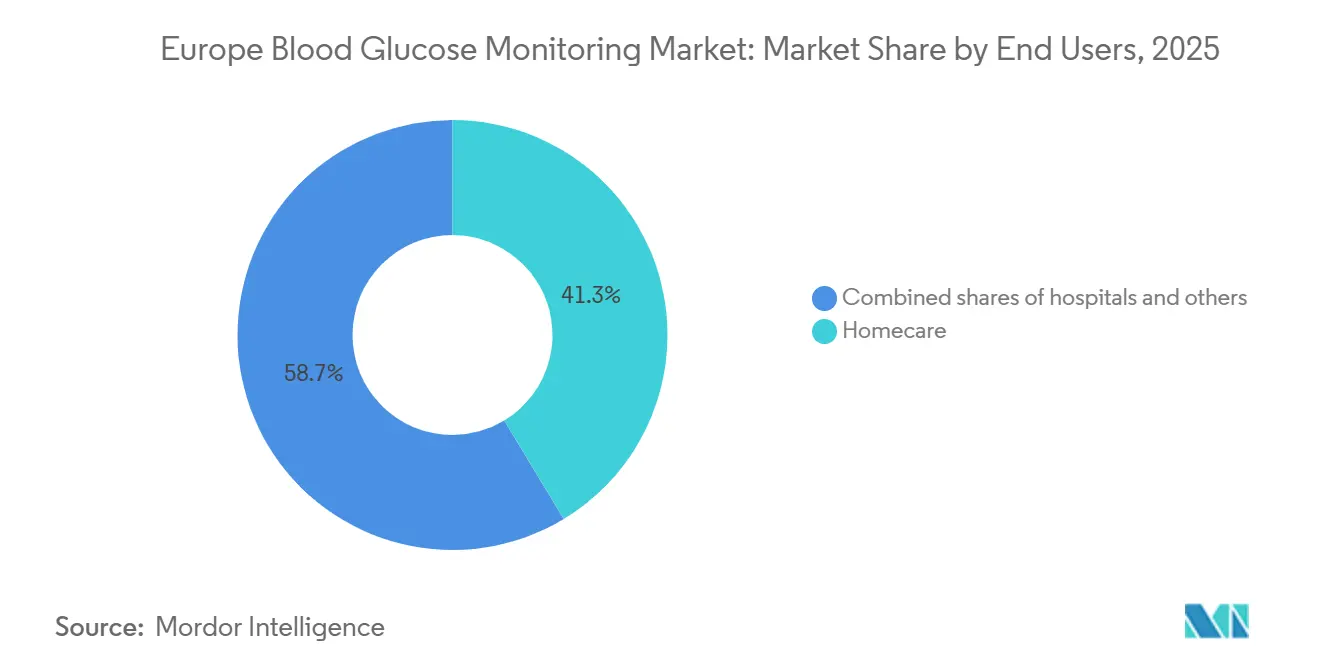

- By end user, the homecare segment captured 41.34% share in 2025 and is on track for a 9.87% CAGR to 2031.

- By geography, Germany led with 26.76% share in 2025, while the United Kingdom posts the fastest trajectory at 11.23% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Blood Glucose Monitoring Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising diabetes prevalence & ageing population | +2.1% | EU-5, Poland, Austria, Switzerland | Long term (≥ 4 years) |

| CGM–SMBG accuracy convergence & hybrid data platforms | +1.8% | Germany, UK, France, Netherlands, Sweden | Medium term (2-4 years) |

| Expanded public reimbursement for CGM across EU-5 | +1.5% | Germany, UK, France, Italy, Spain | Short term (≤ 2 years) |

| Digital-health integration enabling virtual diabetes clinics | +1.3% | Nordic countries, Netherlands, Belgium, UK | Medium term (2-4 years) |

| Value-based procurement & outcomes-linked tenders | +0.9% | Germany, France, Netherlands | Medium term (2-4 years) |

| ESG-driven demand for eco-designed reusable sensors | +0.6% | Germany, France, Netherlands, Sweden | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Understand The Key Trends Shaping This Market

Download PDF

Rising Diabetes Prevalence & Ageing Population

Europe counted 61 million adults living with diabetes in 2025, and the International Diabetes Federation projects this figure will reach 68 million by 2030. Germany documented 8.5 million diagnosed cases in 2025, a 9% rise from 2020, while Poland’s prevalence hit 7.2% amid rural diagnostic gaps [1]International Diabetes Federation, “IDF Diabetes Atlas 2025,” diabetesatlas.org. People aged 65-plus, whose diabetes incidence is 3.2-times higher than the working-age group, are expanding fastest in Italy, Spain, and Portugal, prompting suppliers to design CGMs with larger displays and voice prompts to suit dexterity or cognitive limitations. These demographics underpin sustained unit demand for both sensors and test strips. Consequently, the Europe blood glucose monitoring market continues to see stable baseline volumes even as per-patient strip consumption falls.

CGM–SMBG Accuracy Convergence & Hybrid Data Platforms

Peer-reviewed trials in The Lancet Diabetes & Endocrinology showed leading CGM systems achieving mean absolute relative difference (MARD) values below 9%, effectively matching laboratory standards and removing the calibration rationale for SMBG. Abbott FreeStyle Libre 3 and Dexcom G7 both secured ISO 15197:2013 certification without finger-stick validation, triggering Germany’s G-BA to reimburse CGM for basal-insulin Type-2 users from July 2025 [2]G-BA Germany, “Press Release July 2025,” g-ba.de. Hybrid data platforms now merge CGM feeds with insulin-pump algorithms and electronic health records, elevating closed-loop accuracy and squeezing the EUR 0.45 per-test price edge that SMBG once held. As decision makers weigh the total cost of care, strip-based economics alone can no longer shield SMBG from share erosion.

Expanded Public Reimbursement for CGM Across EU-5

NHS England committed GBP 350 million annually in April 2024 to provide flash and real-time CGM to every insulin-treated patient. France’s Haute Autorité de Santé followed in September 2024, extending coverage to poorly controlled Type-2 patients on multiple daily injections. Italy and Spain enacted similar, though regionally nuanced, funding schemes in 2025 that tie payment to hypoglycemia reduction metrics. These actions collectively expand the reimbursable universe by more than 1.2 million European users within two years, giving CGM its strongest demand shock in a decade.

Digital-Health Integration Enabling Virtual Diabetes Clinics

Post-pandemic, 42% of diabetes follow-ups in the Nordics occurred virtually in 2025, up from 18% in 2020, thanks to cloud dashboards that let clinicians titrate insulin remotely. Stockholm’s CGM data hub shortened waiting lists by 30% and improved HbA1c by 0.4 percentage points. Danish pilots pairing CGM with AI coaching apps reached 78% engagement, showing that behavioral nudges can amplify sensor value. These gains embolden payors to shift routine care to home settings, amplifying sensor sales through direct-to-consumer channels.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of CGM devices & consumables | –1.2% | Southern & Eastern Europe | Short term (≤ 2 years) |

| Semiconductor-grade MEMS supply-chain constraints | –0.8% | Germany, France, UK | Short term (≤ 2 years) |

| GLP-1-driven insulin volume decline dampening sensor demand | –1.0% | Germany, UK, France | Medium term (2-4 years) |

| EU MDR / IVDR bottlenecks & limited Notified-Body capacity | –0.7% | Pan-Europe | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

High Cost of CGM Devices & Consumables

Out-of-pocket spending remains a hurdle where reimbursement is partial or absent. Italian users paid EUR 120-160 per month for Libre sensors in 2025, 12% of the median disposable income in the south [3]Italian Diabetes Society, “Access Report 2025,” siditalia.it. Spain’s autonomous regions showed 70% coverage in Catalonia but only 18% in Extremadura, fuelling legal challenges from patient groups. Poland funds CGM solely for children, leaving 280,000 adult insulin users on SMBG strips that cost EUR 35 monthly, reinforcing health inequities.

Semiconductor-Grade MEMS Supply-Chain Constraints

CGM sensors use electrochemical electrodes built on silicon wafers, competing for foundry slots also serving automotive chips. During the 2024-2025 shortage, Dexcom faced 38-week ASIC lead times and prepaid EUR 45 million in wafer inventory. Abbott dual-sourced platinum-iridium electrodes to buffer risk, stockpiling 60 days of safety inventory. Any renewed silicon crunch could again expose the market to short-term stock-outs.

Segment Analysis

By Device Type: CGM Gains as SMBG Defends Legacy Base

SMBG still accounted for 60.1% of Europe's blood glucose monitoring market share in 2025, buoyed by entrenched reimbursement for Type-2 patients on oral agents and the 12 million-unit installed base of finger-stick users. Roche Accu-Chek Guide and LifeScan OneTouch Verio Reflect anchor pharmacy contracts, though their test-strip volumes slipped 4-6% in 2025 as CGM accelerated among insulin users. The European blood glucose monitoring market size linked to CGM is forecast to expand at 10.23% CAGR, propelled by accuracy parity, ISO certification without calibration, and interoperability with closed-loop pumps.

Emerging non-invasive wearables—Biolinq’s microneedle patch and Nemaura’s sugarBEAT—entered limited pilots in 2025, courting the 8 million pre-diabetics who refuse finger pricks. Medtronic’s Guardian 4 sensor reached 18% of new CGM starts in Germany within six months of its March 2025 launch, underscoring the momentum behind fully integrated systems. To blunt share loss, SMBG vendors now bundle Bluetooth meters with analytics portals, seeking to shift dialogue from “device” to “data” even as per-test economics erode.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Diabetes Type: Type-1 Intensity Meets Type-2 Volume

Type-2 cases delivered 73.21% of revenue in 2025, confirming their numeric dominance, yet Type-1 drives disproportionate growth and technology mix. The Europe blood glucose monitoring market size earned from Type-1 users is projected to climb 13.5% CAGR, as pediatric guidelines prescribe CGM as standard of care and closed-loop systems proliferate. Germany leads with 78% CGM penetration among Type-1 patients.

Type-1 patients also spend 4.2-times more per capita on sensors and pump supplies than Type-2 SMBG users, concentrating manufacturer margins. Expanded reimbursement for Type-2 CGM now hinges on clinical demonstration of hypoglycemia reduction rather than glycemic averages alone, a hurdle that vendors are actively studying. Broader inclusion of pre-diabetes monitoring could unlock 18 million additional users, but supportive cost-effectiveness dossiers remain a prerequisite.

By Age Group: Pediatrics Surge, Geriatrics Lag

Adults represented 73.1% of 2025 revenue, yet pediatrics outpaces every cohort with a forecast 14.31% CAGR. Sweden’s school-based program put CGM in 92% of Type-1 children by 2025, cutting emergency admissions by 44%.

Geriatric uptake sits at 19% despite accounting for 28% of diabetic Europeans, constrained by manual dexterity hurdles and skepticism toward new tech. Abbott’s caregiver-view feature lifted German and Dutch senior adoption 18% year-on-year. Italy’s pilot that couples CGM with weekly tele-consults achieved 72% adherence, signalling that wrap-around services, rather than hardware alone, can unlock this conservative segment.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Test Type: Invasive Dominance Faces Non-Invasive Challenge

Invasive modalities, spanning SMBG and minimally invasive CGM, held 59.12% share in 2025, supported by pump integration requirements. Non-invasive technologies are projected to grow at 10.78% CAGR through 2031 as patients gravitate toward pain-free options. Nemaura’s sugarBEAT registered 12.3% MARD in trials, good enough for private-pay segments, though still shy of public-funding thresholds.

Biolinq’s intradermal patch, now in CE-mark review, positions itself as “virtually non-invasive,” offering 14-day wear with no skin breach and targeting launch in 2026. For pump-dependent users, however, invasive CGM retains an accuracy and real-time advantage, especially for automated insulin delivery algorithms that adjust every five minutes. As such, invasive systems will dominate high-acuity segments even while non-invasive gains share among lifestyle-managed Type-2 and pre-diabetic populations.

By End User: Homecare Ascends, Hospitals Retreat

Homecare settings delivered 41.34% of revenue in 2025 and are projected to climb 9.87% CAGR, reflecting enduring patient preference for remote monitoring. German sickness funds reported 68% of endocrinology consults were virtual by 2025, trimming per-patient costs by EUR 340.

Hospitals accounted for a significant share but face slower growth as reimbursement rarely covers inpatient sensor use. Abbott’s Libre Pro addresses staff workload with retrospective reporting, but adoption remains low. Direct-to-consumer e-commerce, classified under “Others,” surged significantly in 2025 after Dexcom and Abbott launched subscription delivery, underscoring a retail-health tilt that reshapes channel strategy.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Germany commanded 26.76% of the Europe blood glucose monitoring market share in 2025, backed by statutory coverage that funds CGM for all Type-1 and select high-risk Type-2 patients. CGM penetration among German insulin users reached 78%, and sickness funds have started outcome-based contracts that further reward sensor adherence.

The United Kingdom is the fastest-growing territory with an 11.23% CAGR forecast to 2031, thanks to NHS England’s GBP 350 million program that extends flash and real-time CGM to 400,000 insulin-treated individuals. Suppliers set up direct distribution to support home delivery, bypassing pharmacy margin drag and enabling swift scale-up. France follows, with HAS expanding reimbursement to Type-2 multiple-daily-injection patients, though roll-out speed is uneven across rural départements.

Spain and Italy exhibit regionally fragmented access. Catalonia hit major CGM coverage. Italy’s pay-for-performance scheme links reimbursement to hypoglycemia reduction, shifting risk to vendors yet catalyzing adoption among cash-strapped health authorities. The Netherlands reaches 64% Type-1 penetration under a time-in-range payment model. Nordic nations collectively hold notable market share, but punch above their weight in virtual-clinic innovation and pediatric adoption. Eastern Europe remains SMBG-centric due to budget constraints, although Poland has signalled adult CGM funding from 2027.

Competitive Landscape

Four multinationals Abbott, Dexcom, Medtronic, and Roche collectively occupied the majority of Europe blood glucose monitoring market revenue in 2025. Abbott’s FreeStyle Libre franchise generated EUR 1.8 billion in sales, strengthened by a low-profile sensor, Bluetooth alerts, and growing integration with insulin pumps. Dexcom’s G7 seized a 22% share of new CGM starts in Germany and the UK within six months of its 2025 launch, leveraging 30-minute warm-up and 10-day wear.

Medtronic differentiates through vertical integration; its MiniMed 780G bundles Guardian 4 sensors with algorithmic insulin dosing and captured 18% of new German Type-1 starts in 2025. Roche continues to dominate SMBG via pharmacy contracts but is pivoting toward digital therapeutics as strip volumes decay. White-space opportunities such as pre-diabetes monitoring and geriatric-friendly interfaces attract newcomers like Biolinq and Nemaura, though capital and regulatory hurdles remain formidable.

AI-enhanced analytics form the next battleground. Abbott’s LibreLink app and Medtronic’s Meal Detection algorithm already predict glucose excursions, raising the stakes for sensor-agnostic software providers. Outcomes-linked tenders in Germany, France, and the Netherlands favor incumbents with extensive data, yet also encourage partnerships between device makers and AI startups to meet pay-for-performance thresholds.

Europe Blood Glucose Monitoring Industry Leaders

F. Hoffmann-La Roche AG

Abbott Laboratories

Dexcom Inc.

Medtronic plc

Ascensia Diabetes Care

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- January 2026: Dexcom unveiled a EUR 120 million expansion of its Letterkenny, Ireland, plant, adding 400 jobs and boosting G7 output 40% to serve NHS England demand.

- November 2025: Abbott secured CE-Mark for FreeStyle Libre 4, extending wear to 15 days and cutting warm-up to five minutes

- September 2025: Medtronic and Novo Nordisk launched a EUR 50 million collaboration to integrate Guardian 4 CGM data with GLP-1 dosing algorithms in Denmark and Sweden.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the European blood glucose monitoring market as every CE-marked, patient-operated device that reads capillary or interstitial glucose, namely glucometers, single-use test strips, lancets, and continuous glucose monitoring (CGM) systems whose sensors transmit to reusable handheld or wearable readers. We keep country coverage broad, spanning all 27 EU states plus the U.K., Switzerland, and Norway.

Scope exclusion: Central laboratory chemistry analyzers and still-experimental non-invasive wearables are left outside the frame, so our figures stay anchored to commercially proven, patient-centric hardware.

Segmentation Overview

- By Device Type

- Self-Monitoring Blood Glucose (SMBG)

- Continuous Glucose Monitoring (CGM)

- Emerging Non-Invasive Wearables

- By Diabetes Type

- Type-1 Diabetes

- Type-2 Diabetes

- By Age Group

- Pediatrics

- Adults

- Geriatrics

- By Test Type

- Invasive

- Non-Invasive

- By End User

- Hospitals

- Homecare

- Others

- By Country

- Germany

- France

- United Kingdom

- Italy

- Spain

- Rest of Europe

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed endocrinologists, diabetes nurse educators, hospital buyers, home-care pharmacists, and regional distributors in Germany, France, Italy, Spain, and the United Kingdom, which let us refine testing-frequency assumptions, sensor replacement cycles, and imminent payer policy changes. These conversations also validated early model outputs before sign-off.

Desk Research

We started by mapping diabetes prevalence, reimbursement ceilings, and import flows using open sources such as the International Diabetes Federation Atlas, Eurostat customs data, OECD Health Statistics, and national HTA portals like NICE and IQWiG. Regulatory listings in the European Database on Medical Devices helped the team align active product codes with customs HS lines across 30 markets. Company 10-Ks, investor decks, public tenders, and curated news from D&B Hoovers and Dow Jones Factiva guided blended selling-price and installed-base assumptions. This list is illustrative; many additional public records were reviewed to cross-check and clarify data points.

Market-Sizing & Forecasting

Our top-down model starts with diagnosed plus estimated undiagnosed diabetes pools, applies SMBG and CGM penetration ratios, and multiplies by testing frequency or sensor turnover to obtain unit volumes, which we then value with blended average selling prices. Select bottom-up cross-checks from distributor interviews and shipment snapshots stress-test totals. Key variables inside the multivariate regression forecast include population aging, obesity prevalence, reimbursement expansion timelines, CGM price erosion, and sensor replacement-cycle length. Scenario analysis brackets upside from factory-calibrated sensors and downside from emerging non-invasive devices.

Data Validation & Update Cycle

Before release, a second analyst compares outputs with historic trade data and independent diabetes-expenditure series. Models refresh each year, with interim updates triggered by material events such as reimbursement shifts or major product recalls, ensuring clients always receive our latest view.

Why Mordor's Europe Blood Glucose Monitoring Baseline Commands Reliability

Published estimates often differ because device baskets, price anchors, and refresh rhythms rarely align.

Gaps widen when consumables are omitted, list rather than transaction prices are used, or mid-cycle payer changes pass unnoticed.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.61 B (2025) | ���ϲ����� | - |

| USD 8.23 B (2024) | Regional Consultancy A | Includes insulin delivery disposables; relies on list prices |

| USD 4.13 B (2023) | Global Consultancy B | Excludes CGM durables; updates biennially |

Together, the comparison shows that Mordor's disciplined scope definition, current prevalence baseline, and yearly refresh cadence give decision-makers a balanced, transparent figure they can trust for planning.

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How fast is the Europe blood glucose monitoring market expected to grow?

The market is forecast to expand at an 8.28% CAGR from 2026 to 2031, rising from USD 6.07 million to USD 9.04 million.

Which device type is gaining the most ground in Europe?

Continuous glucose monitoring is the fastest-growing category, projected at a 10.23% CAGR as reimbursement broadens and accuracy now rivals laboratory standards

Why is the United Kingdom the fastest-growing country for glucose monitoring devices?

A GBP 350 million NHS England program funds CGM for all insulin-treated patients, driving an 11.23% CAGR through 2031 and encouraging direct-to-consumer distribution models

What challenges could slow market expansion?

High sensor prices in regions with partial reimbursement, semiconductor supply-chain constraints, and a shift toward GLP-1 therapy that reduces insulin use are the leading headwinds.