Epoxy Coatings Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 39.51 Billion |

| Market Size (2031) | USD 46.49 Billion |

| Growth Rate (2026 - 2031) | 3.31% CAGR |

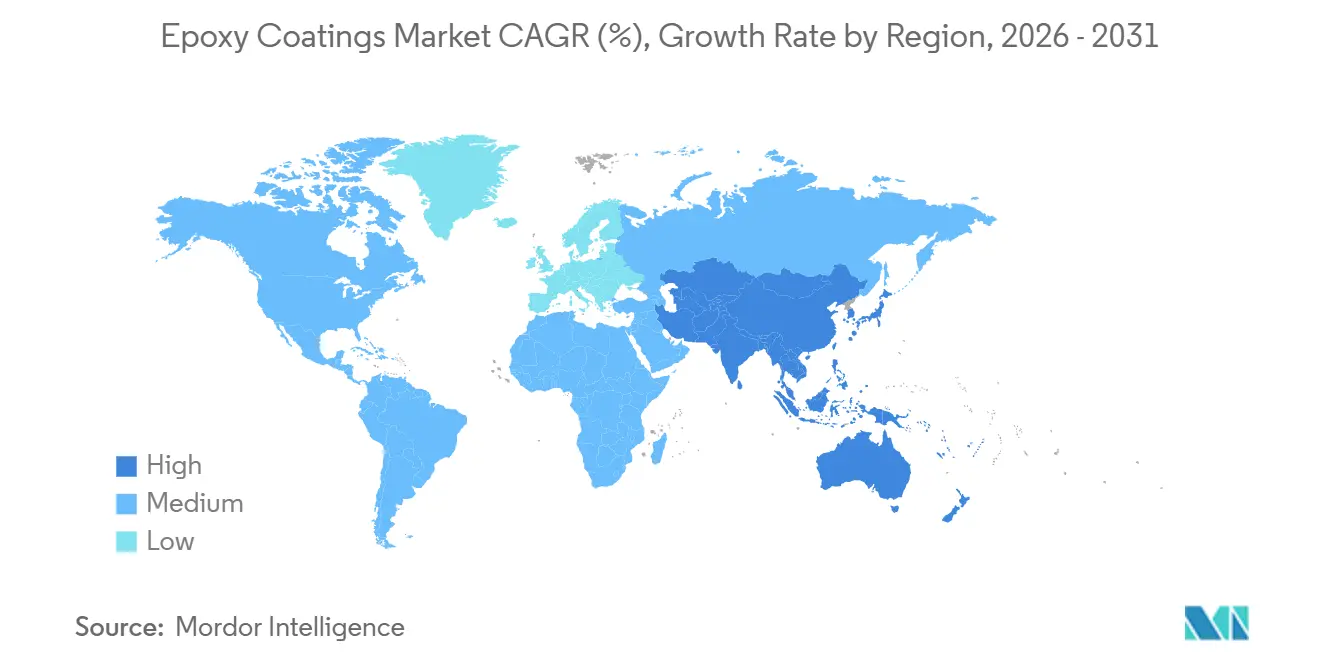

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

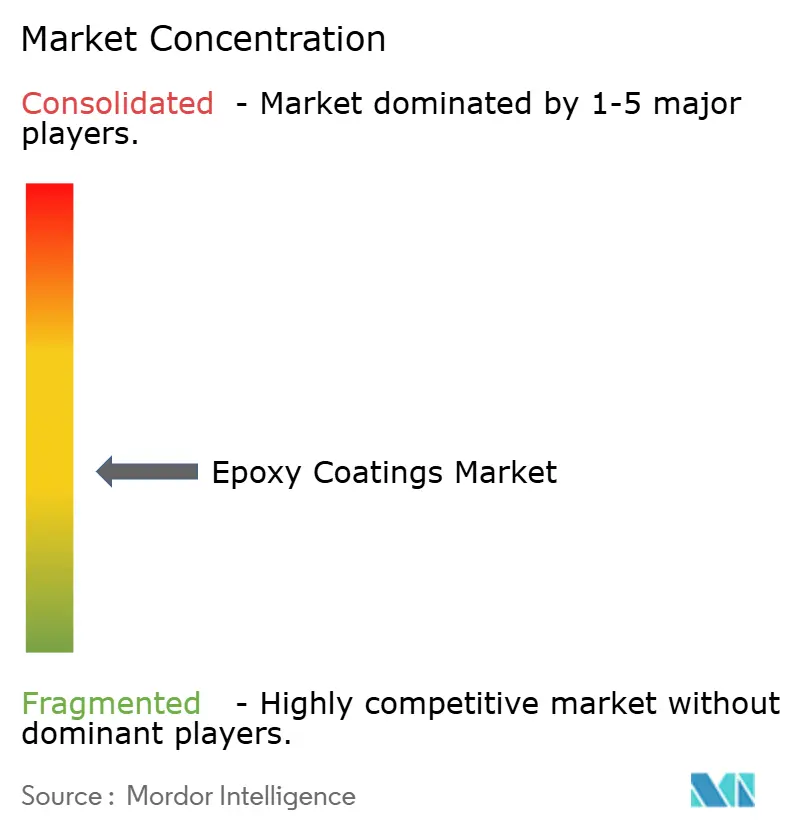

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Epoxy Coatings Market Analysis by ���ϲ�����

The Epoxy Coatings Market size is expected to grow from USD 38.24 billion in 2025 to USD 39.51 billion in 2026 and is forecast to reach USD 46.49 billion by 2031 at 3.31% CAGR over 2026-2031. Demand is shifting toward low-VOC products as water-based systems already command 41.81% of 2025 technology revenue and are expanding at 4.38% CAGR because REACH Annex XVII caps solvent content in protective finishes. Asia-Pacific remains the primary growth engine due to India’s USD 1.3 trillion National Infrastructure Pipeline and ASEAN’s sizeable infrastructure gap that governments aim to close by 2030. Industrial retrofits in food and beverage plants, spurred by updated USDA sanitation standards, are pulling through higher-margin floor coatings. Automotive OEMs are installing UV and LED-curable epoxy lines that cut energy use by 70%, which is helping producers protect margins despite raw-material cost swings.

Key Report Takeaways

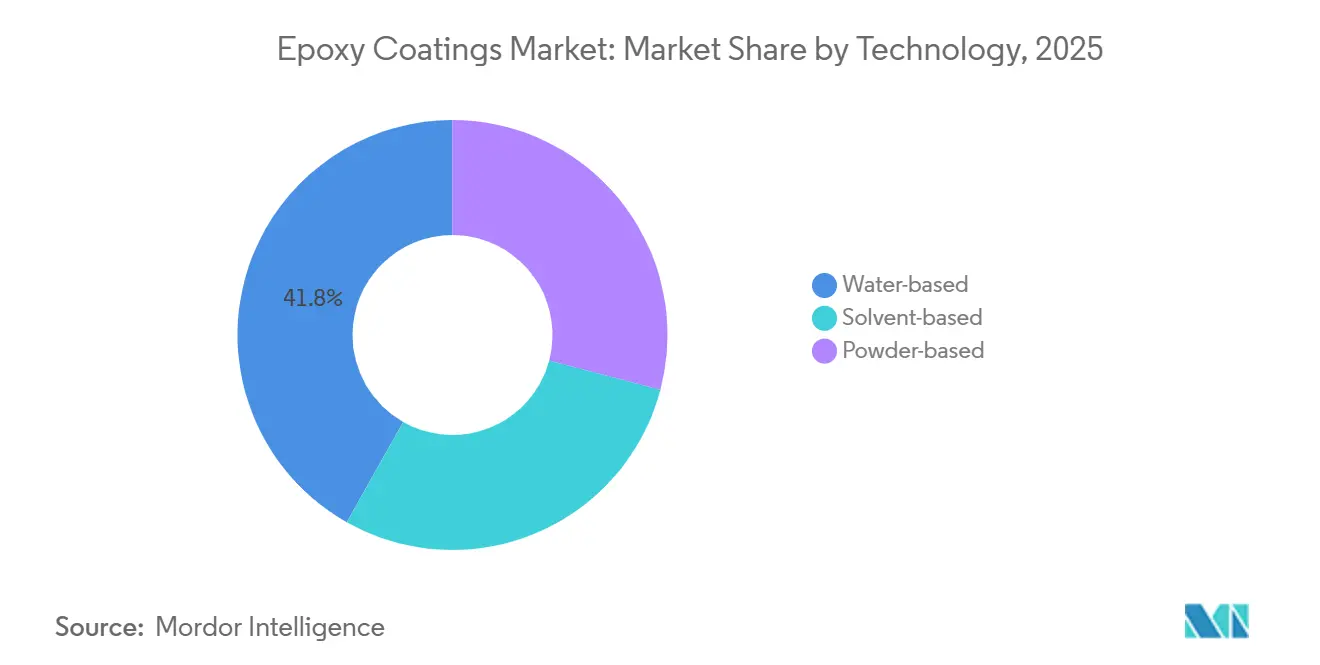

- By technology, water-based systems led with 41.81% of 2025 revenue and expanding at a 4.38% CAGR to 203.

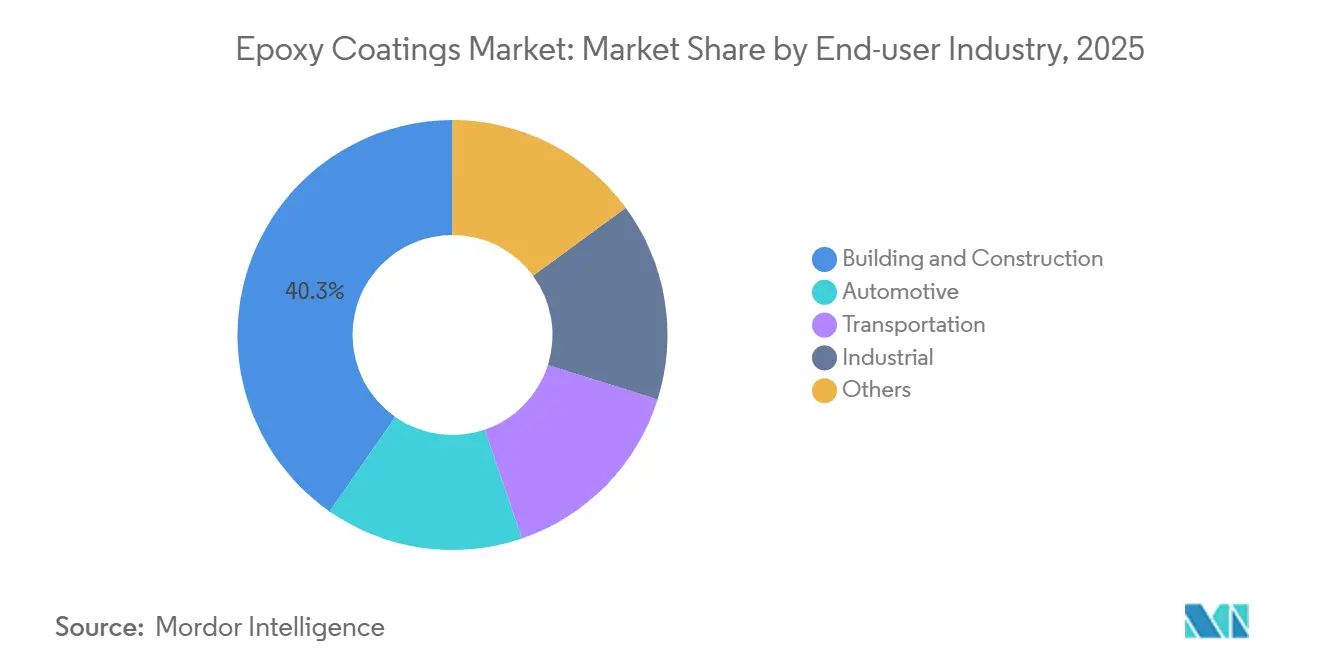

- By end-user, building and construction held 40.31% epoxy coatings market share in 2025; industrial applications are the fastest expanding segment at 3.61% CAGR through 2031.

- By geography, Asia-Pacific contributed 46.55% of 2025 revenue and is on track for a 3.68% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Epoxy Coatings Market Trends and Insights

Driver Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Waterborne Epoxy Penetration Rising in Industrial Protective Coatings | +1.2% | Global, strongest in EU and North America | Medium term (2-4 years) |

| Construction Sector Expansion in Asia-Pacific and Africa | +0.9% | India, ASEAN, Saudi Arabia, South Africa | Long term (≥ 4 years) |

| Industrial Flooring Upgrades in Food and Beverage Plants | +0.5% | North America, EU, ASEAN | Short term (≤ 2 years) |

| Rapid-Cure UV/LED-Curable Epoxy Technologies | +0.4% | Major automotive clusters | Medium term (2-4 years) |

| EV Battery Casings and Motor Housings | +0.3% | China, South Korea, United States, EU | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Waterborne Epoxy Penetration Rising in Industrial Protective Coatings

Two-component waterborne systems now deliver dry-film uniformity within ±5 µm, matching solvent grades while cutting VOCs by 80% to meet the 420 g/L REACH limit[1]European Chemicals Agency, “REACH Annex XVII Entries,” echa.europa.eu. Propylene-carbonate co-solvents keep 20-minute open times without breaching CARB rules, enabling full U.S. roll-out. Petro-chemical and wastewater firms value the zero-flash-point profile, which lowers insurance premiums by up to 15%. Germany recorded a 28% rise in waterborne tank-lining volumes during 2025. Price parity with solvent systems, reached in late 2024, removed the final barrier to mainstream adoption.

Construction Sector Expansion in Asia-Pacific and Africa

India’s pipeline dedicates USD 1.3 trillion to highways, metros, and airports that specify epoxy primers on steel rebar. ASEAN attracted USD 240 billion of FDI in 2025, and 42% funded factories and data centers needing chemical-resistant floors. Saudi Arabia’s USD 500 billion NEOM allocates marine-grade coatings for high-salinity zones. The African Development Bank pegs the continent’s infrastructure deficit at USD 100 billion per year, much of which will require corrosion-resistant epoxy systems. South Africa’s ports are also upgrading with epoxy layers that prolong steel life in coastal humidity.

Industrial Flooring Upgrades in Food and Beverage Plants

The Food Safety Modernization Act mandates seamless, non-porous floors, driving processors from vinyl tile toward epoxy terrazzo. USDA audits in 2025 cited 34% of plants for floor cracking, accelerating retrofit cycles[2]United States Department of Agriculture, “FSIS Compliance Data,” usda.gov. Silver-ion antimicrobial additives now cut microbial counts by 99.9% within 24 hours, allowing monthly deep-cleans. Rapid-cure mortars resurface 1,000 m² overnight, so downtime falls to eight hours. Thailand’s CP Foods alone invested USD 120 million to refit 22 facilities during 2025.

Rapid-Cure UV/LED-Curable Epoxy Technologies

UV-curable chemistries polymerize in 3–10 s under 395 nm lamps, removing ovens and cutting energy use by 70%. German OEMs trimmed coating cycles from 45 min to 12 min after LED line installation in 2025. New photoinitiators now enable through-cure of 200 µm films for electronics encapsulation. Japan saw a 41% jump in UV-line adoptions across electronics plants in 2025. LED lamp life beyond 50,000 h keeps operating costs below USD 0.02 per m² coated.

Restraint Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| BPA and Epichlorohydrin Price Volatility | –0.6% | EU and North America | Short term (≤ 2 years) |

| PFAS and Microplastic Rules Threatening Powder Epoxy | –0.4% | EU and California | Medium term (2-4 years) |

| Shortage of Skilled Robotics Applicators | –0.2% | North America, Western Europe, ASEAN | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

BPA and Epichlorohydrin Price Volatility Disrupting Cost Structures

Bisphenol A prices in Europe rose 22% during 2025 after provisional anti-dumping duties on Chinese epoxy imports. U.S. epichlorohydrin jumped 18% as Gulf Coast producers trimmed output on expensive natural gas. Indian vendors exploited duty-free feedstocks to undercut European suppliers by 12% in Middle East bids. Most formulators now favor quarterly instead of spot contracts, sacrificing flexibility. Raw materials consequently rose to 62% of finished-goods cost, squeezing mid-tier margins.

PFAS and Microplastic Rules Threatening Powder Epoxy Adoption

EU microplastics rules, effective January 2025, restrict powders that release particles under 5 mm unless overspray capture exceeds 95%. California placed fluorinated epoxy hardeners on its PFAS work plan, extending development cycles by up to two years. Anti-static additives help meet dust standards but add USD 0.40 per kg and lower gloss retention by 10% after 2,000 h QUV-A. Germany proposes extending similar limits to industrial coatings in 2026, forcing booth retrofits that cost up to USD 150,000 UBA.DE. Regulatory uncertainty is nudging automakers back toward low-VOC liquid grades despite powder’s 30% lower emissions.

Segment Analysis

By Technology: Waterborne Systems Outpace Solvent Alternatives

Water-based formulations seized 41.81% of 2025 revenue and are advancing at a 4.38% CAGR to 2031, owing to REACH caps of 420 g/L VOC for protective and 250 g/L for architectural coatings. Solvent-based blends cure faster below 10 °C and tolerate salt-contaminated steel, which offshore and winter jobs require. Powder grades face EU microplastics restrictions that push automakers toward low-VOC liquids. UV systems remain niche at under 1% yet deliver three-second cures for printed-circuit boards, offering future upside.

Waterborne chemistries have reached cost parity since late 2024 as scale economies emerged, and they achieve ISO 4624 adhesion above 3.5 MPa, matching solvent peers. Solvent-borne epoxies, however, still dominate marine tanks where surface salts up to 50 mg/m² exceed waterborne tolerance limits. Powder suppliers are trialing ultra-low-dust recipes with anti-static aids but accept a USD 0.40/kg cost penalty and 10% gloss fade after 2,000 h QUV-A. UV-curable grades gained traction in electronics because inline processing boosts board throughput to 120 units/h and slashes energy consumption.

Note: Segment shares of all individual segments available upon report purchase

By End-User Industry: Industrial Segments Accelerate Past Construction

Building and construction retained 40.31% of 2025 revenue on the back of mega-projects across India and ASEAN. Industrial users are the fastest expanding group at 3.61% CAGR because USDA sanitation audits trigger flooring retrofits. Automotive held an 18% share, driven by electric-vehicle battery casings that must survive aggressive thermal cycling. Transportation, including aerospace and rail, contributed 12% of revenue, fueled by Boeing and Airbus production ramps that specify corrosion-inhibiting primers.

Construction demand clusters in Asia-Pacific, where Belt and Road financed USD 28 billion of projects across 18 countries in 2025, each specifying epoxy protection on rebar. Industrial flooring upgrades accelerate in North America and Europe as processors shift to antimicrobial epoxies with silver ions that extend cleaning intervals. German automakers’ LED lines raised single-shift output to 180 vehicles, deepening reliance on fast-cure primers. Offshore wind growth in the North Sea and the South China Sea keeps marine-grade epoxies in demand for turbine towers enduring 5,000 h salt spray per ISO 9227.

Geography Analysis

Asia-Pacific contributed 46.55% of 2025 revenue and is expected to grow 3.68% CAGR to 2031, propelled by India’s infrastructure push and USD 240 billion of FDI into ASEAN factories. India’s epoxy coatings market size is rising fastest as domestic players leverage distribution density in tier-2 cities. The Chinese market is supported by semiconductor cleanrooms that need ISO Class 5 compliant floors. LG Energy Solution's scaled battery-coat capacity is driving the South Korean market.

North America’s market growth is anchored by the USD 110 billion U.S. infrastructure law that mandates epoxy deck sealers for freeze–thaw resilience. The United States delivered 78% of regional sales, followed by Canada at 14% where Toronto’s CAD 25 billion transit expansion relies on tunnel linings with moisture barriers. Mexico benefited from USD 35 billion of nearshoring investment in aerospace and auto plants that specify epoxy floors.

Europe accounted for significant revenue but faces margin pressure from VOC caps that require EUR 8–15 million reformulation outlays per product line. Germany led with 28% of regional sales thanks to automotive LED lines that sliced cure cycles to 12 min. The United Kingdom followed at 18%, boosted by GBP 44 billion of rail upgrades that need corrosion-proof steel coatings. France, Italy, and the Nordic zone round out the region with major metro, cruise, and offshore wind projects requiring epoxy protection.

Competitive Landscape

The epoxy coatings market is moderately consolidated. Bio-based epoxies from lignin and vegetable oils remain a white space with fewer than 50 active patents worldwide, offering startups fertile ground. Strategically, majors are deepening vertical integration and adding local production. Sherwin-Williams allotted USD 350 million to its Pune waterborne plant, shaving logistics costs by 18%.

Emerging disruptors such as Cardolite introduced cashew-shell-derived hardeners that meet USDA BioPreferred rules and command 12% price premiums in green buildings. Meanwhile, regional suppliers in Latin America and Africa gain share through fast service and private-label agreements with retailers. Despite rising raw-material volatility, mid-sized players prosper by tailoring niche formulations for local climate or regulatory quirks, keeping the epoxy coatings market competitive yet profitable.

Epoxy Coatings Industry Leaders

PPG Industries, Inc.

AkzoNobel N.V.

The Sherwin-Williams Company

Kansai Paint Co., Ltd.

Jotun

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: PPG invested USD 280 million to expand waterborne epoxy capacity in Sumaré, Brazil, adding 45,000 tons/year plus a research and development hub for low-VOC grades.

- November 2025: Asian Paints opened a USD 180 million epoxy plant in Visakhapatnam, India, integrating solvent-recovery systems that cut VOCs by 75%.

Global Epoxy Coatings Market Report Scope

Epoxy coating is a durable, protective substance used to prevent carbon steel tanks and other relatable materials from degrading on the outside. Epoxy coatings offer superior resistance to abrasion, turbulence, harsh chemicals, and severe temperatures.

The epoxy coatings market is segmented by technology type, end-user industry, and geography. By technology type, the market is segmented into water-based, solvent-based, and powder-based. By end-user industry, the market is segmented into building and construction, automotive, transportation, industrial, and other end-user industries. The report also covers the market size and forecasts for the epoxy coatings market in 17 countries across major regions. For each segment, the market sizing and forecasts have been done based on revenue (USD).

| Water-based |

| Solvent-based |

| Powder-based |

| Building and Construction |

| Automotive |

| Transportation |

| Industrial |

| Others |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Technology | Water-based | |

| Solvent-based | ||

| Powder-based | ||

| By End-user Industry | Building and Construction | |

| Automotive | ||

| Transportation | ||

| Industrial | ||

| Others | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large will epoxy coatings demand be by 2031?

The epoxy coatings market size is forecast to reach USD 46.49 billion by 2031, reflecting a 3.31% CAGR from 2026.

Which technology segment is expanding the fastest?

Water-based systems show the highest momentum at 4.38% CAGR because tightened VOC limits are accelerating their adoption.

Why are food plants replacing older floors?

Updated USDA sanitation audits found floor cracks in 34% of facilities in 2025, prompting a shift to seamless antimicrobial epoxy terrazzo that minimizes bacterial harborage.

How will European regulation affect suppliers?

REACH Annex XVII VOC caps force reformulation costs of EUR 8–15 million per product line, compressing margins and favoring firms with strong R&D funding.

What drives epoxy demand in electric vehicles?

Battery casings and motor housings require coatings that survive –40 °C to 85 °C cycling and resist dielectric breakdown above 10 kV/mm, needs met by cycloaliphatic epoxy chemistries.

Page last updated on: