Engineered Foam Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

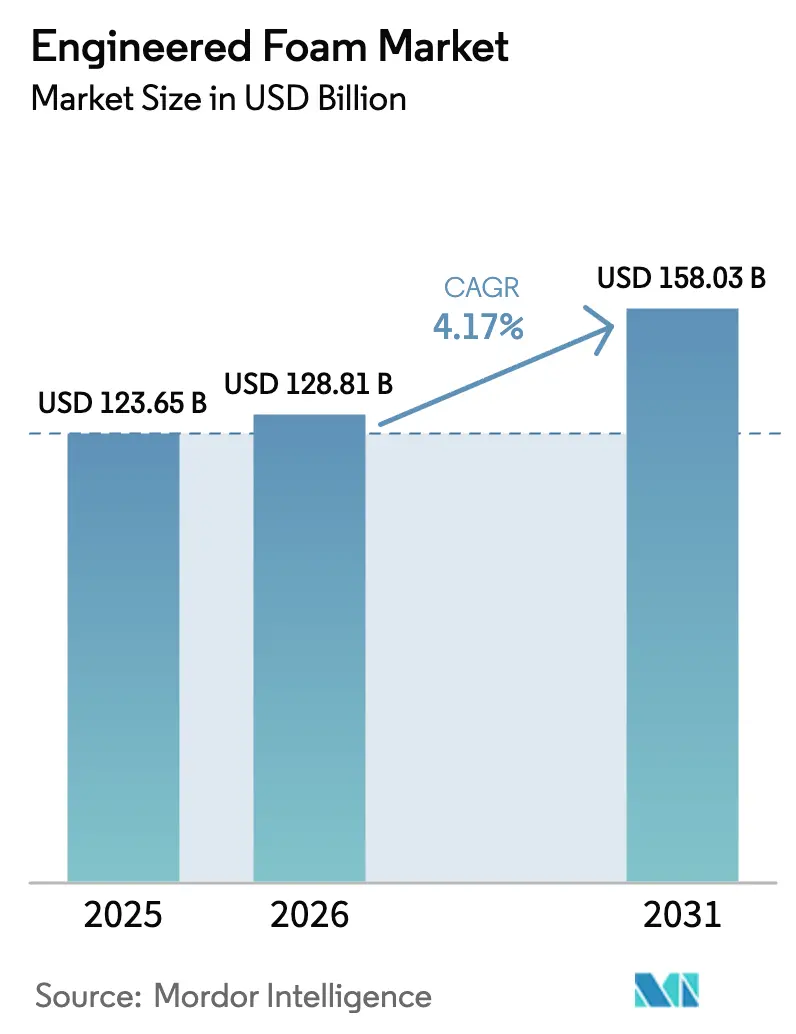

| Market Size (2026) | USD 128.81 Billion |

| Market Size (2031) | USD 158.03 Billion |

| Growth Rate (2026 - 2031) | 4.17% CAGR |

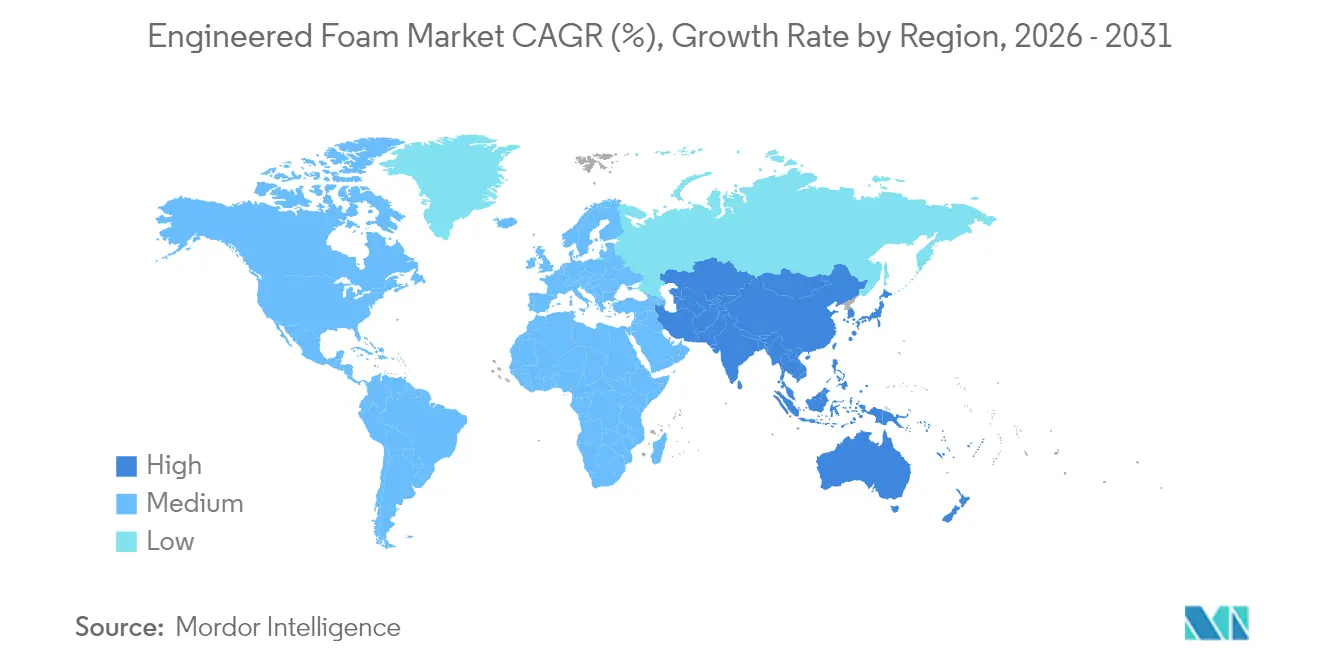

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Engineered Foam Market Analysis by ���ϲ�����

Engineered Foam Market market size in 2026 is estimated at USD 128.81 billion, growing from 2025 value of USD 123.65 billion with 2031 projections showing USD 158.03 billion, growing at 4.17% CAGR over 2026-2031. Regulations that raise building-envelope R-values, automakers’ appetite for lighter and quieter electric vehicles, and the phase-down of high-GWP blowing agents collectively accelerate volume growth. Producers are also benefiting from e-commerce packaging demand and from early hydrogen-infrastructure pilots that require cryogenic foams. Asia-Pacific anchors supply and demand thanks to new TPU capacity in China and large-scale civil-engineering projects, while North America acts as a regulatory bellwether for low-GWP spray systems. Short-term margin pressure stems from isocyanate and polyol price swings, but integrated suppliers that lock in raw-material streams and commercialize bio-based polyols are positioned to defend profitability.

Key Report Takeaways

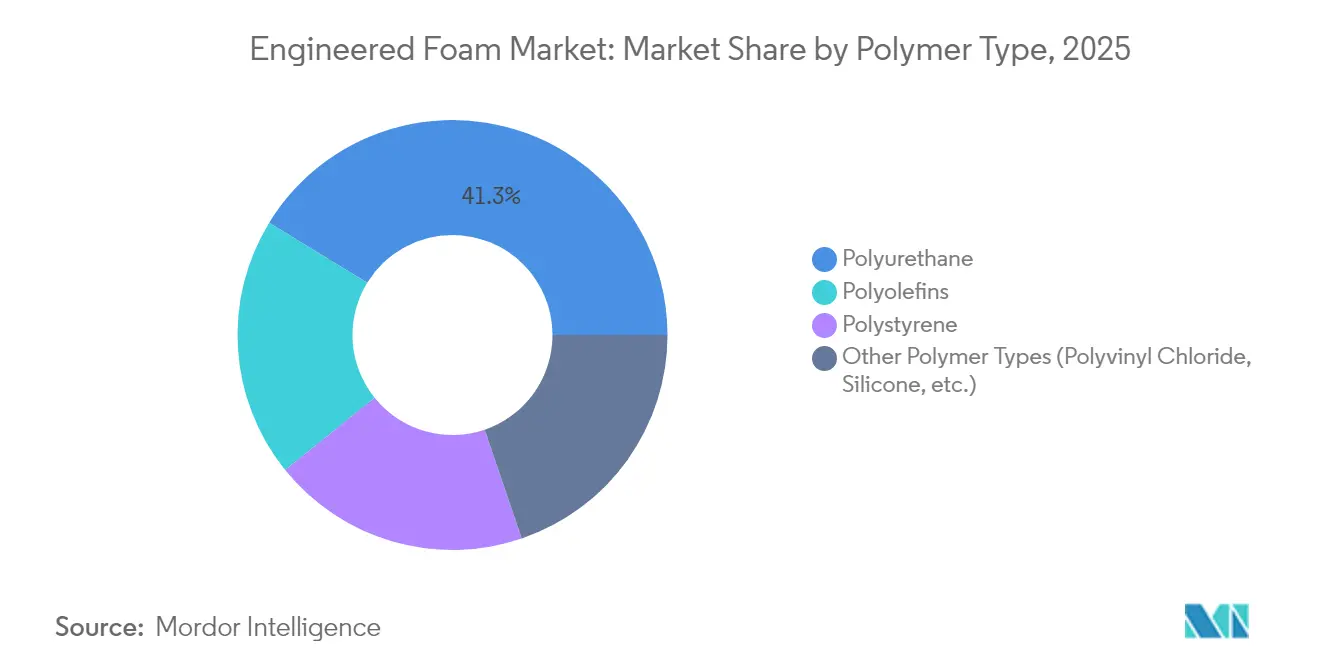

- By polymer type, polyurethane led with 41.25% engineered foam market share in 2025, whereas the Other Polymer Types segment is projected to widen at a 5.06% CAGR through 2031.

- By foam type, flexible foams accounted for 52.30% revenue in 2025; spray foams are forecast to post the fastest expansion at 5.03% CAGR to 2031.

- By function, thermal-insulation applications held 39.55% of the engineered foam market size in 2025 and structural core and lightweighting foams are advancing at a 4.85% CAGR through 2031.

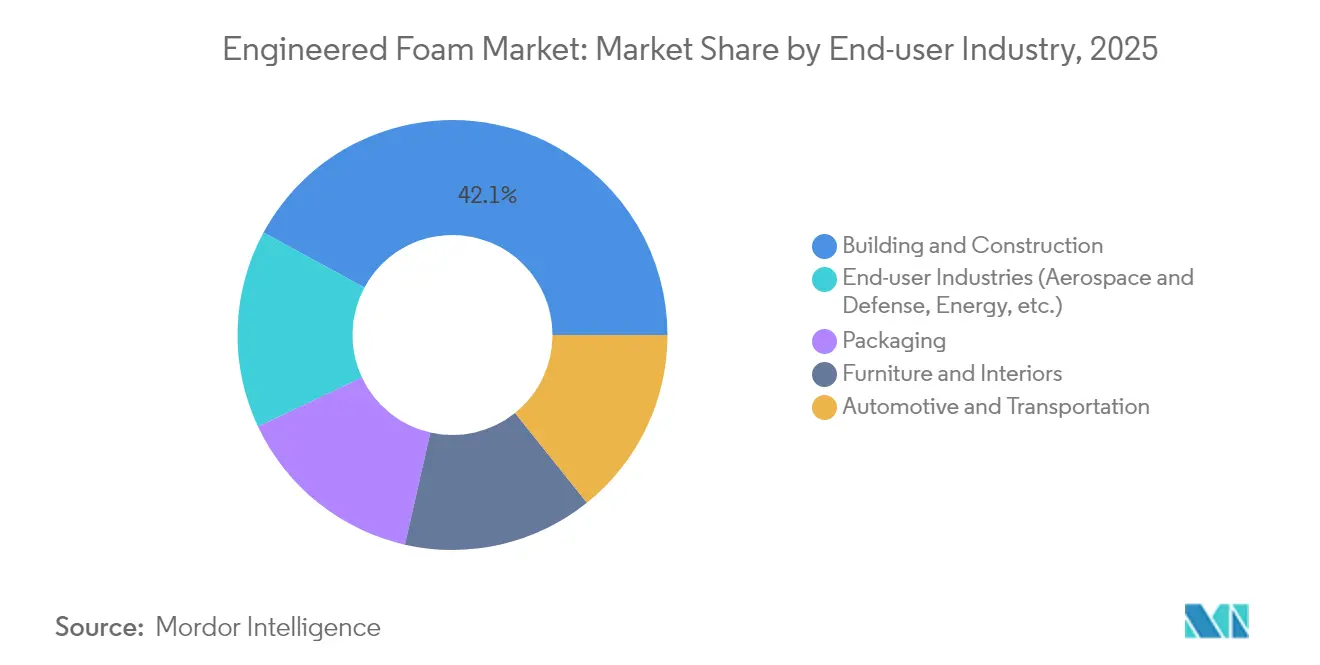

- By end-user industry, building and construction commanded 42.10% revenue in 2025, while the aggregate of aerospace, energy, and other niche industries is expected to climb at a 5.12% CAGR, through 2031.

- By geography, Asia-Pacific captured 44.30% of global demand in 2025 and is simultaneously slated to grow at 4.90% CAGR through 2031

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Engineered Foam Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Demand for Lightweight, Fuel-Efficient Materials in Automotive | +0.8% | Global, with concentration in Asia-Pacific and North America | Medium term (2-4 years) |

| Stringent Building Energy Codes Driving Demand for Engineered Insulation Foams | +0.7% | North America s EU, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Expanding E-Commerce Boosting Protective Foam Packaging | +0.5% | Global, led by North America and Asia-Pacific | Short term (≤ 2 years) |

| Rapid Adoption of Acoustic Metamaterial Foams in EV Cabins | +0.4% | Asia-Pacific core, spill-over to North America and EU | Medium term (2-4 years) |

| Growing Demand for Cryogenic-Capable Foams for Hydrogen Infrastructure Insulation | +0.3% | EU and North America, early adoption in Japan | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Surging demand for lightweight, fuel-efficient materials in automotive

Automakers target weight savings to shore up EV driving range and meet fleet-average CO₂ limits. Polyurethane systems such as Huntsman’s SHOKLESS™ provide density windows that secure battery modules while cutting mass Life-cycle analyses show natural-fiber composites cut energy demand versus metals, reinforcing the appeal of hybrid foam–composite architectures. Mexico’s 13% output surge and its rise to fourth-largest polyurethane market underline the regional pull created by near-shoring strategies. As EV skateboard platforms proliferate, foams that fuse structural support, thermal management, and NVH damping shift from optional to critical components in the engineered foam market.

Stringent building energy codes driving demand for engineered insulation foams

The 2021 IECC mandates exterior continuous insulation in climate zones 4 and 5, cementing closed-cell spray polyurethane foam’s R-7 per inch profile. Federal adoption lifts new-home efficiency by 34.4% compared with 2009 baselines, even after a USD 7 229 incremental build cost[1]Federal Register, “Adoption of Energy Efficiency Standards for New Construction of HUD- and USDA-Financed Housing,” federalregister.gov. Huntsman estimates that insulating the existing US housing stock could save 648 billion kWh a year—power equivalent to taking 38.9 million cars off the road. Commercial builders seeking LEED points specify rigid panels blown with greater than 10 GWP agents, accelerating the conversion away from HFC-141b. Consequently, code pressure channels the bulk of insulation volume toward higher-performance foams in the engineered foam market.

Expanding e-commerce boosting protective foam packaging

Online order volumes keep rising, forcing brand owners to trim damage rates without inflating dimensional weight. Sealed Air’s closed-cell polyethylene profiles achieve that balance, replacing bulkier corrugated designs while protecting delicate items. The firm’s Cellu-Pro™ range embeds 95% recycled content, meeting EU recycled-material quotas. Patent filings around starch-derived biodegradable cushions reinforce momentum toward circular packaging. These shifts translate into continuous order books for converters and bolster the engineered foam market.

Rapid adoption of acoustic metamaterial foams in EV cabins

With ICE noise gone, EV interiors expose occupants to wind and tire frequencies. Research shows aerogel-loaded non-wovens achieve a 0.33 average absorption coefficient at 500–1 600 Hz while retaining 0.026 W/mK thermal conductivity. Covestro’s Bayfit® cavity fillers shave 3–5 dB from cabin noise without appreciable weight gain. Similar metamaterial logic now migrates into 100% recyclable aircraft seat foams, evidencing cross-sector pull. NVH performance therefore ranks among the most bankable growth levers inside the engineered foam market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Isocyanate and Polyol Prices | -0.6% | Global, particularly impacting North America and Asia-Pacific | Short term (≤ 2 years) |

| Tightening VOC Blowing-Agent Regulations | -0.4% | North America and EU, expanding globally | Medium term (2-4 years) |

| Scarcity of Certified Bio-Based Polyol Feedstock | -0.3% | Global, with acute shortages in developed markets | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Volatility in isocyanate and polyol prices

MDI spot indices swung double-digit in 2024, lifting polyurethane resin quotes even as automotive demand dipped 25% BASF’s buy-out of the Alsachimie PA 6.6 joint venture secures adipic-acid and HMD streams, illustrating how backward integration hedges cost risk. Mid-tier converters rely on multi-source contracts, yet price lags still compress margins across the engineered foam market.

Tightening VOC blowing-agent regulations

The US EPA bans HFC-blown spray foams with GWPs above 150 from January 2025, obliging formulators to switch to HFOs and hydrocarbons[2]American Chemistry Council, “State Phase-Down of HFCs in the Spray Foam Industry,” americanchemistry.com . Europe’s F-gas overhaul follows suit. Low-GWP agents impose higher raw-material bills and flammability-handling costs, thinning out smaller applicators. Compliance complexity thus tempers near-term volume in pockets of the engineered foam market even as long-run sustainability arcs favor compliant suppliers.

Segment Analysis

By Polymer Type: Portfolio diversification gathers pace

Polyurethane retained the largest engineered foam market share at 41.25% in 2025, rooted in closed-cell systems that deliver R-7 per inch and dominate cold-chain and roofing builds. Nonetheless, bio-based routes, non-isocyanate chemistries, and CO₂-modified backbones fuel a 5.06% CAGR for the Other Polymer Types segment. BASF’s Ludwigshafen EPS expansion targets appliance and packaging niches, while Covestro’s prototype rigid foam with 20% captured CO₂ hits spec parity with petro-based incumbents.

Second-generation polyolefins improve recyclability, giving e-commerce shippers a low-density option that meets circular pledges. Specialty silicones penetrate rolling-stock interiors thanks to intrinsic flame-smoke-toxicity compliance. As feedstock diversification deepens, polyurethane’s revenue dominance will narrow slightly, yet it will still anchor engineered foam market size in 2030 because of unmatched insulation efficiency and mature supply chains.

Note: Segment shares of all individual segments available upon report purchase

By Foam Type: Spray systems capture code-driven upside

Flexible foams accounted for 52.30% revenue in 2025, buoyed by bedding, furniture, and seat applications. Rigid boards preserved food-retail cold lanes, and elastomeric foams served HVAC gasket needs. Spray foams, however, are slated for a 5.03% CAGR—fastest in class—because they meet air-sealing and insulation codes in one pass, raising their engineered foam market size share year-over-year. Huntsman Building Solutions’ Icynene Series reaches 7.4 per-inch R-value and rolls out in low-pressure kits for remodelers.

HFO-blown chemistry now dominates new launches, while roofing contractors exploit high-lift closed-cell variants to curb labor hours. As insurers tighten energy-loss clauses, spray foam penetration could top 20% of North American wall-and-roof insulation by 2030, further enlarging the engineered foam market.

By Function: Insulation leads; lightweighting accelerates

Thermal-insulation duties held 39.55% of 2025 revenue, the largest slice of the engineered foam market size, because codes and cold-chain logistics value low λ materials. Structural core and lightweighting foams log a 4.85% CAGR, helped by sandwich-panel use in battery enclosures and 3D-printed lattice cores that shed 35% weight versus honeycombs.

Acoustic and vibration foams ride EV demand, while energy-absorption cushions expand with omnichannel retail. Buoyancy foams hold steady in marine energy and recreation. Function-level diversity shelters producers from sector cyclicality and enlarges participation in the engineered foam market.

By End-user Industry: Construction still rules, niche sectors outpace

Building and construction contributed 42.10% of revenue in 2025, underpinned by code-mandated exterior insulation. Yet aerospace, hydrogen energy, and medical devices cluster into the Other End-user Industries segment, which is expanding at 5.12% CAGR. Aircraft seat makers adopt fully recyclable foams to cut turnaround emissions, and cryogenic insulation systems guard liquid-hydrogen tanks at –253 °C. These higher-value niches diversify the engineered foam market revenue stream beyond cyclical housing trends.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia-Pacific’s 44.30% share and 4.90% CAGR reflect a full-spectrum industrial ecosystem that spans civil construction, auto assembly, and consumer electronics. China’s renewable-powered TPU complex in Zhanjiang underscores commitment to local value chains. Japan refines NVH foams for premium EVs, and India’s construction boom absorbs rigid boards and spray systems in new urban housing. South Korea contributes advanced resins for memory-chip packaging, whereas ASEAN factories gain share by offering cost-competitive conversion. Together these dynamics sustain the engineered foam market’s highest regional momentum.

North America combines strict building codes with capital access, supporting leadership in low-GWP spray-foam capacity. Huntsman’s Icynene Series and regionwide installer training push open-cell products deeper into retrofit attic jobs. Mexico’s near-shoring wave powers automotive PU usage, and Canada’s cold climate bolsters insulation demand. Upside persists, yet feedstock volatility remains a cost wild card for engineered foam market players across the region.

Europe plays sustainability spearhead, mainstreaming CO₂-based polyols and bio-circular attributions. Covestro’s rigid-foam prototypes with 20% captured CO₂ set new life-cycle benchmarks. Nordic housing stimuli amplify demand for high-R SIP panels, whereas Germany’s automotive tier system pilots flame-retardant lightweight cores for EV battery trays. Regulatory certainty around F-gas and VOC ceilings helps long-term investment planning, anchoring the engineered foam market’s European strategy.

Competitive Landscape

Moderate fragmentation defines the engineered foam market. Carpenter’s purchase of Recticel’s Engineered Foams Division for EUR 656 million vaults it to the largest vertically integrated flexible-foam supplier. Armacell’s full buy-out of AJA boosts aerogel-based high-temperature insulation capacity beyond 700 t/y, opening LNG and district-heating applications. BASF’s Alsachimie acquisition fortifies upstream control over polyamide precursors, illustrating vertical-integration logic.

Technology differentiation now trumps volume. Covestro markets Bayfit® NVH fillers that deliver 3 dB attenuation at equal mass, earning premium placements in EV platforms. Huntsman’s SHOKLESS™ resists thermal runaway in battery packs, tapping the EV safety up-cycle. Dow’s bio-based NORDEL™ REN EPDM signals a push to renewable elastomer matrices. Companies with R&D heft, captive monomer streams, and regulatory-affairs expertise therefore hold strategic high ground.

Mid-tier converters hedge raw-material risk via tolling agreements and localized recycling, but margin resilience still trails that of integrated peers. Private-equity funds remain active buyers, targeting specialty formulators with aerospace and medical access where price realizations are higher. Overall, intellectual-property breadth, low-carbon credentials, and M&A scale will dictate share gains inside the engineered foam market.

Engineered Foam Industry Leaders

BASF SE

Dow Inc.

Huntsman Corporation

Armacell International SA

Carpenter Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: BASF has unveiled biomass balance grades of its Elastoflex® polyurethane foam, broadening its offerings for the furniture sector. This newly formulated foam is designed for diverse furniture uses, such as seating, headrests, and armrests.

- July 2023: Carpenter acquired Recticel NV's Engineered Foams Division, which included the former Foam Partner and Otto Bock operations. This acquisition established Carpenter as the world's largest vertically integrated manufacturer of polyurethane foams and specialty polymer products.

Global Engineered Foam Market Report Scope

The engineered foam market report includes:

| Polyurethane |

| Polyolefins |

| Polystyrene |

| Other Polymer Types (Polyvinyl Chloride, Silicone, etc.) |

| Flexible |

| Rigid |

| Spray |

| Other Foam Types (Elastomeric, etc.) |

| Thermal Insulation |

| Acoustic and Vibration Control |

| Energy Absorption and Cushioning |

| Buoyancy and Floatation |

| Structural Core and Lightweighting |

| Building and Construction |

| Packaging |

| Furniture and Interiors |

| Automotive and Transportation |

| End-user Industries (Aerospace and Defense, Energy, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Polymer Type | Polyurethane | |

| Polyolefins | ||

| Polystyrene | ||

| Other Polymer Types (Polyvinyl Chloride, Silicone, etc.) | ||

| By Foam Type | Flexible | |

| Rigid | ||

| Spray | ||

| Other Foam Types (Elastomeric, etc.) | ||

| By Function | Thermal Insulation | |

| Acoustic and Vibration Control | ||

| Energy Absorption and Cushioning | ||

| Buoyancy and Floatation | ||

| Structural Core and Lightweighting | ||

| By End-user Industry | Building and Construction | |

| Packaging | ||

| Furniture and Interiors | ||

| Automotive and Transportation | ||

| End-user Industries (Aerospace and Defense, Energy, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current engineered foam market size and growth outlook?

The engineered foam market size stands at USD 128.81 billion in 2026 and is expected to reach USD 158.03 billion by 2031, growing at a 4.17% CAGR.

Which polymer type leads the engineered foam market?

Polyurethane holds the top position with 41.25% engineered foam market share in 2025, owing to its superior insulation and structural versatility.

Why is Asia-Pacific the fastest-growing region?

China’s renewable-powered TPU capacity, large infrastructure spending, and rapid EV adoption give Asia-Pacific both the largest share and the fastest 4.90% CAGR through 2031.

How are regulations influencing spray foam demand?

The 2021 IECC and the EPA’s low-GWP mandates are pushing builders toward closed-cell spray polyurethane foam that offers R-7 per inch and air-sealing in one pass.

What innovations are most disruptive in the engineered foam market?

CO₂-based polyols, aerogel-enhanced cryogenic foams, and metamaterial acoustic fillers are reshaping product portfolios and commanding premium pricing.