Endometriosis Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.97 Billion |

| Market Size (2031) | USD 3.37 Billion |

| Growth Rate (2026 - 2031) | 11.31% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Endometriosis Treatment Market Analysis by ���ϲ�����

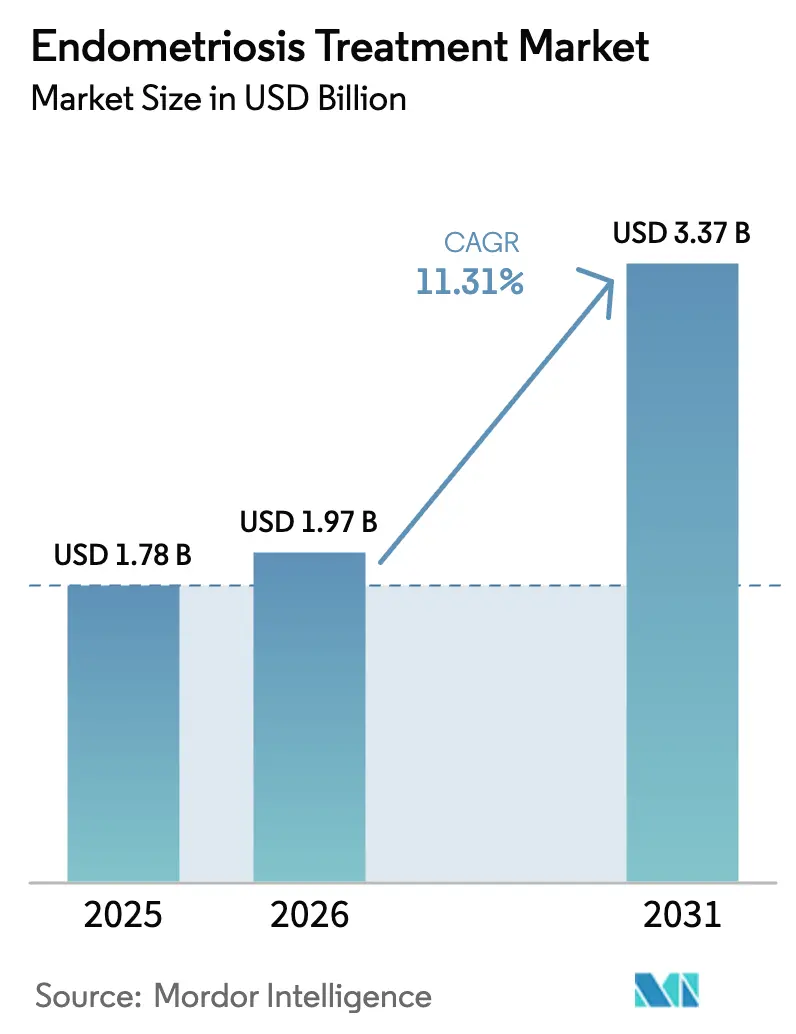

The Endometriosis Treatment Market size was valued at USD 1.78 billion in 2025 and is estimated to grow from USD 1.97 billion in 2026 to reach USD 3.37 billion by 2031, at a CAGR of 11.31% during the forecast period (2026-2031).

The uptake of oral gonadotropin-releasing hormone (GnRH) antagonists after favorable reimbursement decisions, broader screening initiatives, and accelerating venture funding is expanding the patient funnel. Long-acting delivery formats and online pharmacy fulfillment are reshaping adherence economics, while non-hormonal immunomodulators entering late-stage trials promise disease-modifying options. North America presently anchors demand on the back of high per-capita spending, but Asia-Pacific is closing the gap as China and India add laparoscopic capacity and fast-track innovative biologics. Competition remains moderate because five multinationals still capture more than half of commercial value, yet white space persists in regenerative therapies and digital diagnostics.

Key Report Takeaways

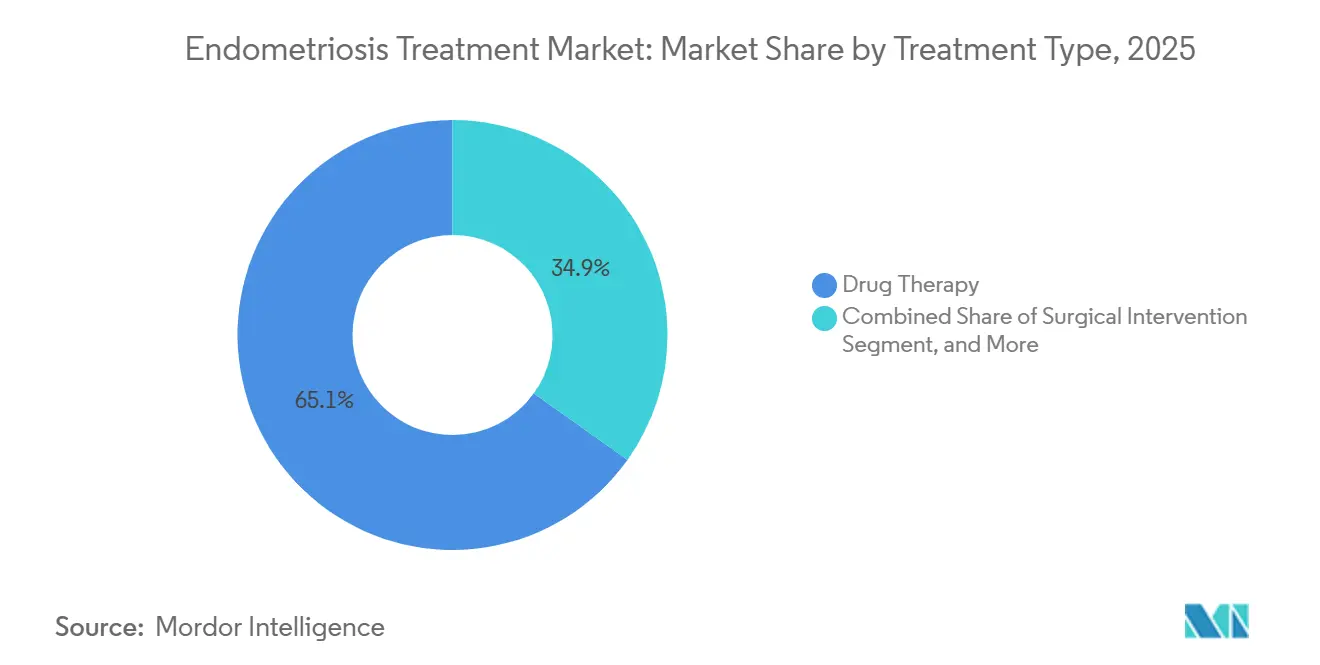

- By treatment type, drug therapy held 65.12 of % endometriosis treatment market share in 2025, and combined or multimodal protocols are the fastest-growing treatment type, advancing at a 12.17% CAGR to 2031.

- By drug class, GnRH agonists and antagonists led with a 42.07% share in 2025, while non-steroidal anti-inflammatory drugs are set to expand at a 13.59% CAGR through 2031.

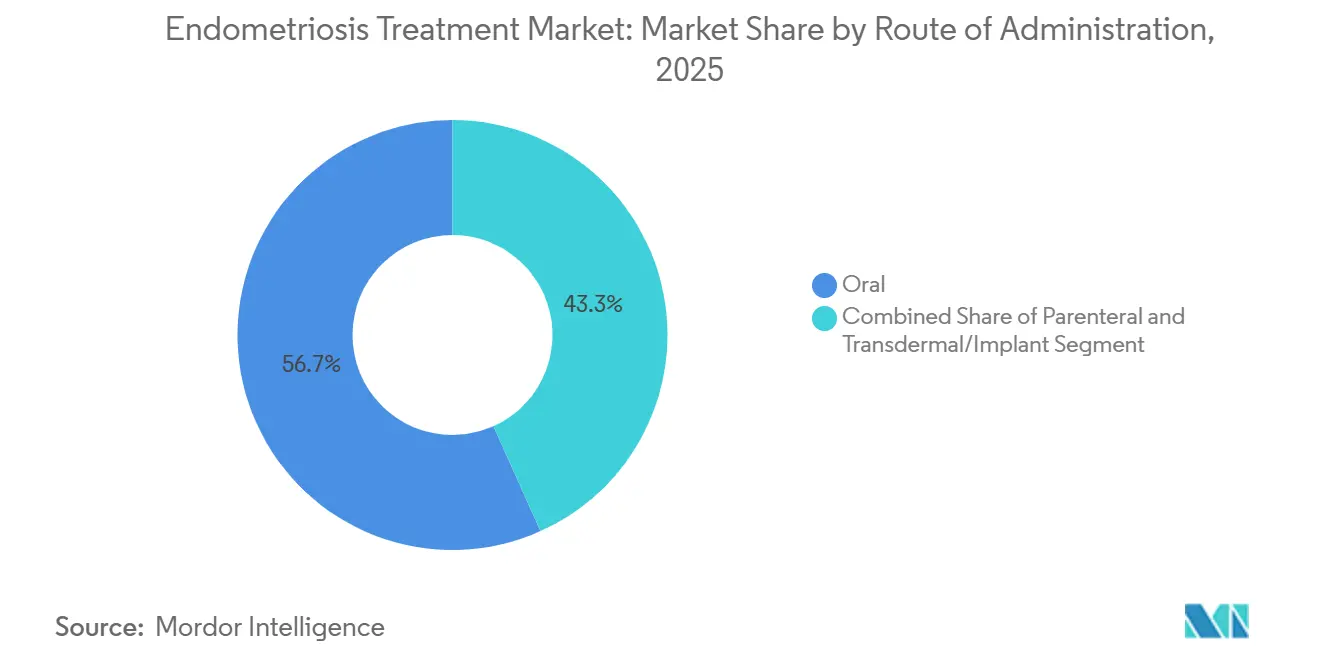

- By route of administration, oral formulations accounted for 56.72% of revenue in 2025, yet transdermal patches and subdermal implants are growing at a 14.09% CAGR.

- By end user, hospital pharmacies dispensed 47.28% of therapies in 2025, but online pharmacies are scaling at 14.91% CAGR on the strength of telehealth bundles.

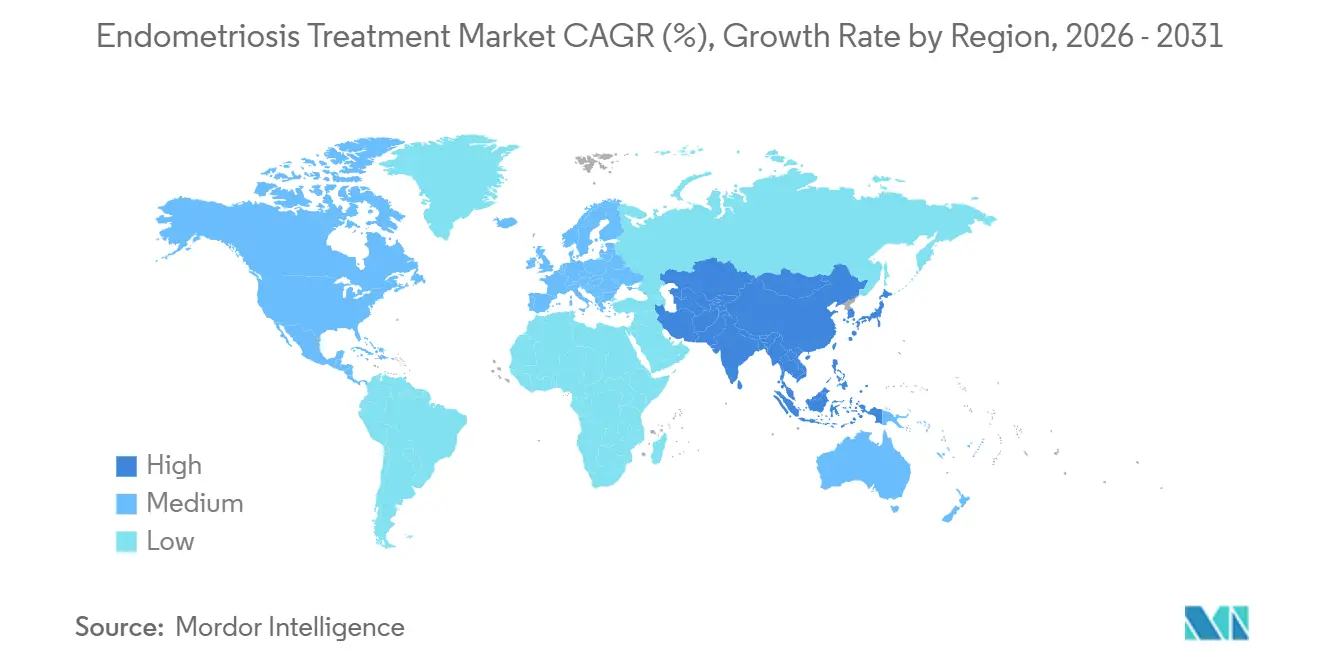

- By geography, North America accounted for 39.27% of 2025 sales, whereas Asia-Pacific is on track for a 13.42% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Endometriosis Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence Among Reproductive-Age Women | +2.1% | Global, acute in North America and Europe | Medium term (2-4 years) |

| Growing Awareness & Earlier Diagnosis | +1.8% | North America, Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| Advances in Minimally Invasive Hormonal Therapies | +1.5% | Global, led by North America and Europe | Medium term (2-4 years) |

| Emergence of Non-Hormonal Immunomodulators | +0.9% | Global, early adoption in North America | Long term (≥ 4 years) |

| Venture Capital Inflow into Regenerative Approaches | +0.7% | North America and Europe, spillover to Asia-Pacific | Long term (≥ 4 years) |

| AI-Based Early Detection & Digital Therapeutics | +0.6% | North America, Europe, select Asia-Pacific markets | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Rising Prevalence Among Reproductive-Age Women

Roughly 10% of women aged 15–49 now live with the condition, yet under-ascertainment in low-resource settings means the real figure is higher.[1]White House, “Action on Menstrual Health Report,” whitehouse.gov The 2024 White House report valued the annual U.S. economic burden at USD 78 billion, compelling several state Medicaid programs to extend coverage for laparoscopic diagnosis in 2025. Later childbearing amplifies risk by extending cumulative estrogen exposure, while China recorded a 12% jump in endometriosis-related infertility consultations between 2024 and 2025. These datapoints collectively expand the addressable endometriosis treatment market and support sustained double-digit growth prospects.

Growing Awareness & Earlier Diagnosis

Hashtags such as #EndoWarrior generated more than 50 million impressions during the 2025 awareness campaign, triggering self-referral surges. NICE guidelines issued in March 2025 reduced the diagnostic interval in England by over 2 years. France’s national pelvic-pain clinics lifted laparoscopic procedure volumes 23% year over year. AI-driven symptom-clustering pilots across Europe triaged high-risk patients for imaging, and patients presenting at earlier stages improve postoperative outcomes and reduce recurrence. Together, these shifts enlarge the treated population and accelerate revenue capture for the endometriosis treatment market.

Advances in Minimally Invasive Hormonal Therapies

Relugolix and linzagolix suppress pituitary signaling without the estrogen flare of injectable agonists, and once-daily dosing enhances adherence. Add-back estrogen-progestin formulations extend safe treatment windows beyond 12 months, mitigating concerns about bone density. Off-label uptake of etonogestrel implants delivered 40% dysmenorrhea relief in an Australian real-world study. Patches repurposed from contraception provide weekly dosing, appealing to patients who dislike pills. These innovations refresh the therapeutic arsenal and propel premium-priced drugs, expanding the endometriosis treatment market for hormonal care.

Emergence of Non-Hormonal Immunomodulators

HMI-115, a prolactin-receptor monoclonal antibody, reduced pelvic pain in Phase II without ablation of ovarian function and secured breakthrough status in China in 2025. TiumBio’s merigolix, a selective progesterone-receptor modulator, also achieved significant pain endpoints with minimal endometrial thinning. Because 20–30% of patients discontinue hormone therapy, these candidates address a clear unmet need. Regulatory agencies, however, call for biomarker-based endpoints, so sponsors must pair clinical readouts with translational assays. Successful launches would diversify mechanisms and dampen side-effect-driven churn that currently constrains the endometriosis treatment industry.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adverse Effects of Long-Term Hormone Use | -1.2% | Global | Short term (≤ 2 years) |

| High Treatment Cost & Patchy Insurance Coverage | -1.4% | North America, Europe, select Asia-Pacific markets | Medium term (2-4 years) |

| Clinical-Trial Recruitment Complexity | -0.5% | Global, acute in North America and Europe | Long term (≥ 4 years) |

| Social Stigma Delaying Care-Seeking | -0.8% | Global, pronounced in Asia-Pacific and Middle East | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Adverse Effects of Long-Term Hormone Use

Injectable GnRH agonists can lower trabecular bone density by more than 5% within six months, restricting duration without add-back estrogen.[2]American College of Obstetricians and Gynecologists, “Endometriosis Practice Bulletin,” acog.org Despite mitigation, 12% of relugolix patients in the U.K. surveillance reported breakthrough bleeding requiring adjustments. Irregular bleeding affects up to 40% of continuous progestin users and is linked to reduced adherence. A Swedish cohort also reported a 1.3-fold increase in insulin resistance markers after 2 years of norethindrone. These safety issues provoke therapy cycling, which raises cumulative costs and softens real-world effectiveness across the endometriosis treatment market.

High Treatment Cost & Patchy Insurance Coverage

Oral GnRH antagonists cost between USD 1,800 and USD 2,000 monthly in the United States, roughly the annual deductible of many high-deductible plans. Prior authorization typically insists on failed NSAID and oral contraceptive courses, delaying starts by up to six weeks. In Europe, England funds relugolix, but Scotland and Wales await local assessments. Japan reimburses injectable agonists yet excludes oral antagonists, while India seldom covers anything beyond generic NSAIDs. Laparoscopic excision can cost USD 10,000–50,000 and is sometimes classified as elective.[3]Healthcare Cost Institute, “Endometriosis Surgery Cost Analysis,” healthcostinstitute.org Such disparities depress uptake and constrain the size of the global endometriosis treatment market.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type: Multimodal Protocols Reshape Standard of Care

Combined approaches integrating surgery with postoperative hormonal suppression are expanding at a 12.17% CAGR and eroding monotherapy dominance. Surgery alone has a 5-year recurrence rate above 40%, whereas adjuvant hormones can extend remission by up to 2 years. Drug therapy still represented 65.12% of the endometriosis treatment market share in 2025, but high switching rates betray dissatisfaction. Robotic laparoscopy gained visibility, yet 2025 evidence found no superiority in pain relief over conventional techniques. Upfront combination care lowers lifetime revisions, steering payers toward bundled reimbursement models that enlarge the endometriosis treatment market.

Sequencing trends are emerging; pre-operative hormonal downsizing can cut intraoperative blood loss, though robust trials are scarce. Nerve-sparing excision techniques help preserve organ function, broadening candidate eligibility. Drug-only regimens remain first-line for women desiring fertility preservation, but payer focus on durability is nudging clinicians toward multimodal pathways. The paradigm shift aligns endometriosis management with other chronic inflammatory diseases, reinforcing recurring revenue streams.

Note: Segment shares of all individual segments available upon report purchase

By Drug Class: NSAIDs Gain Share Amid Affordability Pressures

GnRH modulators led with a 42.07% share in 2025, yet over-the-counter NSAIDs are on track for a 13.59% CAGR through 2031. Ibuprofen and naproxen cost as little as USD 10–20 monthly, anchoring first-line pain control. Real-world German data show 68% of newly diagnosed patients start on NSAID monotherapy, underscoring cost sensitivity. Oral contraceptives account for roughly 18% but cater to users seeking dual contraception. Innovation inside the class is minimal; growth stems chiefly from volume as diagnosis rates rise, adding fresh entrants to the endometriosis treatment market size baseline.

Combination NSAID products addressing bloat or gastroprotection broaden retail shelf space. Guideline bodies also endorse NSAID continuation post-surgery to temper residual dysmenorrhea. While premium biologics court the severe-pain segment, accessible analgesics continue to expand the overall patient pool, reinforcing their share in the endometriosis treatment market.

By Route of Administration: Long-Acting Delivery Gains Patient Preference

Oral formats still accounted for 56.72% of 2025 revenue, but transdermal patches and subdermal implants will grow fastest at a 14.09% CAGR. Non-adherence to daily dosing exceeds 30%, so weekly or multi-year delivery is attractive. The etonogestrel implant provided 40% pain reduction and a 28% drop in healthcare utilization in Australian cohorts. Depot injections retain a niche among patients who favor quarterly clinic visits, though bone-density-loss warnings on medroxyprogesterone temper demand. Oral GnRH agonist scripts already declined 8% between 2024 and 2025 as once-daily antagonists cannibalized volume. New long-acting rings and microspheres in development could expand modality options and amplify the endometriosis treatment market, driven by patient-centric delivery.

Adhesive reactions affect up to 15% of patch users, presenting a manageable but real deterrent. Intravaginal rings are under early investigation, promising localized hormone release with minimal systemic exposure. Collectively, delivery innovations elevate patient quality of life and support durable market expansion.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Online Pharmacies Disrupt Traditional Models

Hospital pharmacies dispensed 47.28% of units in 2025, anchored by peri-operative supply and specialty-drug coordination. Yet online pharmacies are forecast to expand at a 14.91% CAGR by bundling teleconsults, prescriptions, and home delivery. Treated.com undercuts retail pricing by up to 30%, while Sesame Care offers visits for USD 25 plus USD 10 for generics. Digital platforms attract younger consumers and those living in areas distant from specialist centers, putting competitive pressure on brick-and-mortar outlets. Draft U.K. rules now require surgical confirmation before online GnRH antagonist prescribing, a hurdle that may slow penetration for advanced cases. As oral antagonists become mainstream formulary items, volume should shift from hospitals to retail and e-commerce, reallocating market share in endometriosis treatment.

Hospital pharmacies will nevertheless defend their share in injectable depots and immediate post-surgical fills. Retail chains leverage in-store clinics to keep foot traffic, but convenience, confidentiality, and bundled chronic-care services favor digital dispensers for long-term hormonal suppression.

Geography Analysis

North America contributed 39.27% of 2025 revenue, supported by robust insurance coverage for novel hormones and direct-to-consumer marketing. U.S. Medicaid expansions in multiple states covered laparoscopic diagnosis and GnRH antagonists, decreasing out-of-pocket costs. Canada funds generic hormones, but provinces differ on reimbursement for oral antagonists; Ontario added relugolix in April 2025. Mexico’s private insurers now subsidize endometriosis procedures, yet public-sector uptake remains limited.

Asia-Pacific is projected to post the fastest CAGR of 13.42%. China’s breakthrough designation for HMI-115 and rapid rollout of laparoscopic suites across tier-2 cities shorten diagnosis delays. India holds one of the highest absolute patient counts, but stigma and clinician shortages hamper detection. Japan’s universal system reimburses injectable agonists while negotiations continue for orals, creating room for biosimilars and domestic generics. Australia’s inclusion of dienogest on the Pharmaceutical Benefits Scheme in 2024 reduced co-pays to AUD 6.60, driving a 35% surge in prescriptions.

NICE endorsements in March and May 2025 unlocked National Health Service funding for relugolix and linzagolix. France’s mandated pelvic-pain clinics lifted surgical volumes 23% year on year. Germany’s insurers lean toward cost-effective NSAID initiation, reflected in high first-line ibuprofen uptake. South America and the Middle East & Africa remain nascent but are beginning to incorporate dedicated women's health benefits in urban centers. Collectively, geographic diversification underpins the widening landscape of endometriosis treatment markets.

Competitive Landscape

Incumbents AbbVie, Bayer, Pfizer, Takeda, and Johnson & Johnson together account for a significant portion of revenue, indicating moderate concentration. Bayer’s January 2026 pledge to elevate women’s health redirects fresh R&D toward pelvic pain, while AbbVie defends Orilissa against once-daily rivals by emphasizing early launch experience. Patent expiries between 2027 and 2029 threaten legacy agonist margins, catalyzing a pivot to differentiated non-hormonal and regenerative assets.

Smaller innovators are seizing unmet-need niches. Cyclana Bio’s GBP 5 million raise backs extracellular-matrix drug discovery for fibrosis reversal. Metri Bio’s 3D organoids enable high-throughput screening tailored to individual phenotypes. Hope Medicine’s HMI-115 could deliver the first mechanism that leaves ovarian function intact, potentially reshaping treatment algorithms. Digital pharmacies like Treated.com and Wisp expand access and gather real-world adherence data valuable for post-marketing differentiation. Regulatory accelerators, such as NICE appraisals in the U.K. and breakthrough tags in China and the U.S., can reassign share virtually overnight. As generics erode pricing power and novel entrants mature, the competitive field will intensify, rewarding speed, safety, and patient-centric delivery.

Endometriosis Treatment Industry Leaders

Bayer AG

Pfizer Inc.

AbbVie Inc.

AstraZeneca

Teva Pharmaceutical Industries Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: NHS England approved once-daily relugolix–estradiol–norethisterone therapy, branded Ryeqo, for symptomatic treatment of endometriosis.

- May 2024: Gynica began Phase 1 trials for S-301 and S-302 cannabinoid formulations delivered via its IntraVag system at Careggi University Hospital.

- March 2024: Scotland launched the first clinical program evaluating dichloroacetate as a metabolic therapy for endometriosis.

- February 2024: Australia’s TGA cleared Ryeqo, the first oral therapy approved nationally for endometriosis pain.

Global Endometriosis Treatment Market Report Scope

As per the scope of the report, endometriosis is a medical condition in which tissues similar to the endometrium grow in ovaries and fallopian tubes. It can affect women of all ages, including teenagers, and cause pain or infertility.

The endometriosis treatment market is segmented by type, treatment type, drug class, route of administration, distribution channel, and geography. By treatment type, the market is segmented into drug therapy, surgical intervention, and combined/multimodal therapy. By drug class, the market is segmented into gonadotropin-releasing hormone (GnRH) agonists & antagonists, progestins, non-steroidal anti-inflammatory drugs (NSAIDs), and other drug classes. By route of administration, the market is segmented into oral, parenteral, and transdermal/implant. By distribution channel, the market is segmented into hospital pharmacies, retail pharmacies & drug stores, and online pharmacies.The report also covers the market sizes and forecasts for the endometriosis treatment market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Drug Therapy |

| Surgical Intervention |

| Combined / Multimodal Therapy |

| Gonadotropin-Releasing Hormone (GnRH) Agonists & Antagonists |

| Progestins |

| Non-Steroidal Anti-Inflammatory Drugs (NSAIDs) |

| Oral Contraceptives |

| Selective Estrogen Receptor Modulators (SERMs) |

| Oral |

| Parenteral |

| Transdermal / Implant |

| Hospital Pharmacies |

| Retail Pharmacies & Drug Stores |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Treatment Type | Drug Therapy | |

| Surgical Intervention | ||

| Combined / Multimodal Therapy | ||

| By Drug Class | Gonadotropin-Releasing Hormone (GnRH) Agonists & Antagonists | |

| Progestins | ||

| Non-Steroidal Anti-Inflammatory Drugs (NSAIDs) | ||

| Oral Contraceptives | ||

| Selective Estrogen Receptor Modulators (SERMs) | ||

| By Route of Administration | Oral | |

| Parenteral | ||

| Transdermal / Implant | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies & Drug Stores | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is global demand for endometriosis therapeutics growing?

Between 2026 and 2031 the endometriosis treatment market is expected to expand at an 11.31% CAGR, rising from USD 1.97 billion to USD 3.37 billion.

Which therapy approach is gaining the most momentum?

Combined surgery plus postoperative hormonal suppression is the fastest-growing pathway, advancing at 12.17% CAGR as evidence mounts that it halves five-year recurrence.

Why are NSAIDs still widely used despite new hormonal drugs?

Generic NSAIDs cost USD 10–20 per month and remain first-line pain control, especially for patients facing high deductibles or wishing to avoid hormonal side effects.

Which region will add the most new patients in the next five years?

Asia-Pacific will outpace all other regions with a 13.42% CAGR as China and India scale laparoscopic infrastructure and accelerate approvals for innovative biologics.

What pipeline innovation could change the treatment paradigm?

Non-hormonal biologics such as HMI-115, which reduces pain without shutting down ovarian function, may deliver disease modification and reshape long-term management strategies.