Emergency Stop Switches Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 11.29 Billion |

| Market Size (2031) | USD 19 Billion |

| Growth Rate (2026 - 2031) | 10.98% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

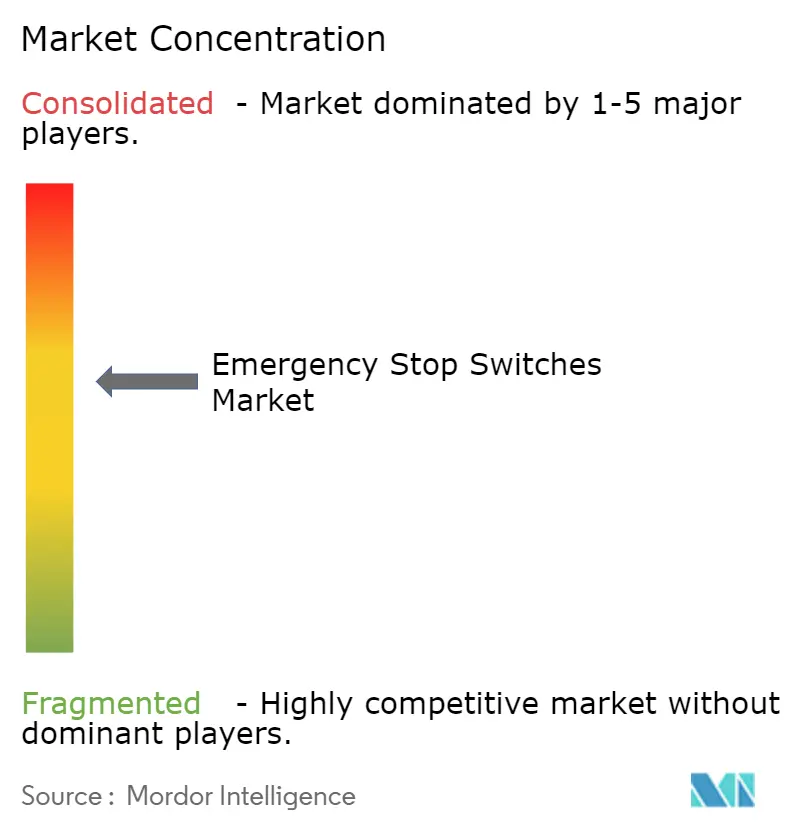

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Emergency Stop Switches Market Analysis by ���ϲ�����

The emergency stop switches market size is expected to increase from USD 10.17 billion in 2025, USD 11.29 billion in 2026 and reach USD 19 billion by 2031, growing at a CAGR of 10.98% over 2026-2031. Tighter machinery safety rules, stronger functional safety validation requirements, and a broader shift from isolated hardwired devices to integrated safety architectures across industrial sectors are driving growth in the emergency stop switches market. A major 2026 change came from the updated IEC 60947-5-5 standard, which pushed manufacturers to refresh latch testing, illuminated device behavior, and conformity files, while the EU Machinery Regulation is already shaping early compliance spending ahead of its January 2027 implementation.[1]European Agency for Safety and Health at Work, “Regulation 2023/1230/EU - Machinery,” EU-OSHA, osha.europa.eu The emergency stop switches market is also gaining support from higher automation density in robotics, warehouse systems, and flexible manufacturing cells, where redundant channels, higher diagnostic integrity, and faster restart logic are becoming standard design choices. Competitive activity remains balanced rather than highly concentrated, since European specialists still hold an edge in certified, high-specification applications, while Asian OEMs and value-tier suppliers continue to pressure pricing in more cost-sensitive use cases. Through 2031, demand should stay broad-based as reshoring in North America, gigafactory construction in Europe, and factory build-outs across Asia create sustained openings for certified product upgrades, retrofit programs, and application-specific safety solutions.

Key Report Takeaways

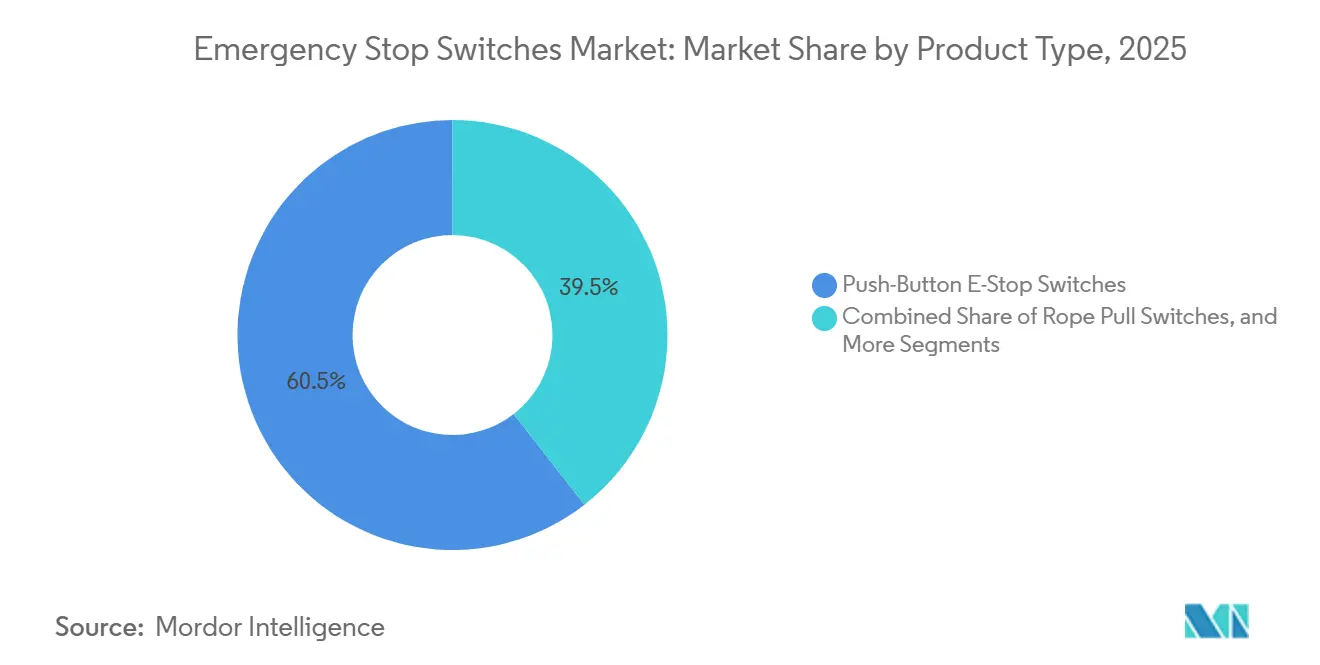

- By product type, push-button e-stop switches held 60.51% share of the emergency stop switches market in 2025, while safety interlock-integrated e-stops are forecast to expand at an 11.11% CAGR through 2031.

- By reset mechanism, push-pull configurations accounted for 47.54% share of the emergency stop switches market in 2025, while automatic and electronic reset variants are projected to grow at the fastest pace, at an 11.02% CAGR through 2031.

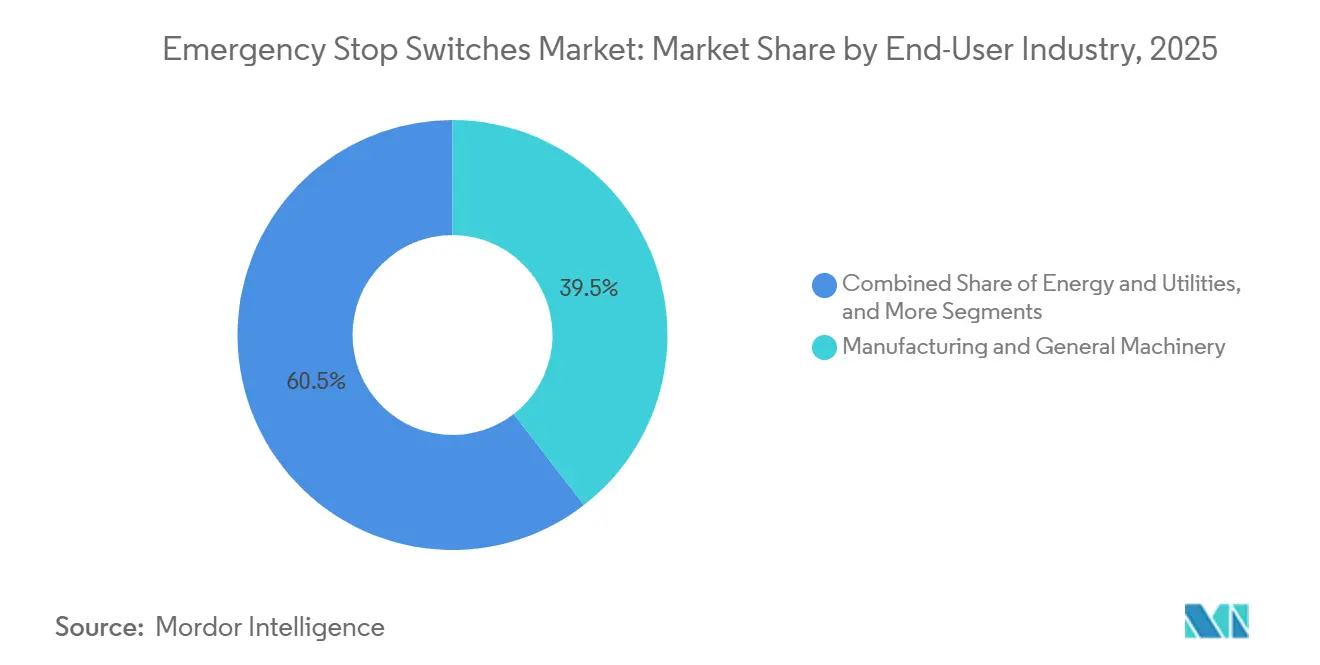

- By end-user industry, manufacturing and general machinery held a 39.52% share of the emergency stop switches market in 2025, while energy and utilities is set to record the highest growth, at an 11.38% CAGR through 2031.

- By contact configuration, 1 NC configurations led with a 37.83% share of the emergency stop switches market in 2025, while multi-contact configurations with more than 2 NC contacts are projected to grow the fastest, at a 12.12% CAGR through 2031.

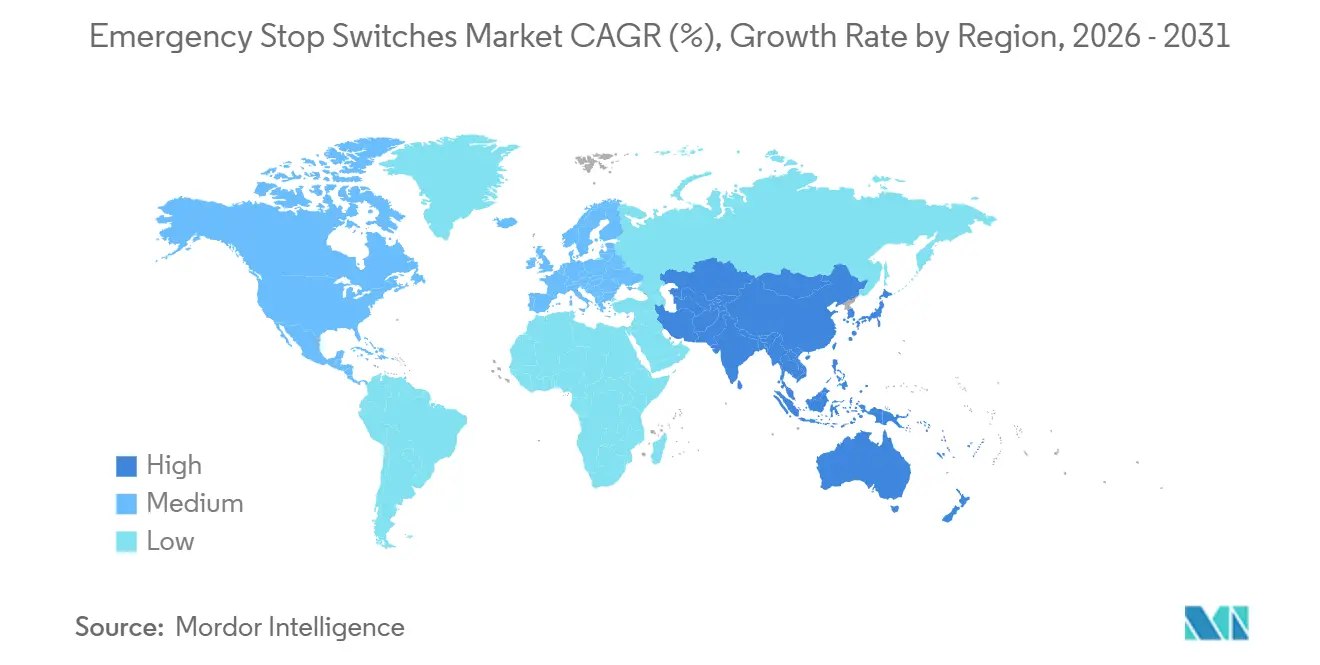

- By geography, Asia-Pacific held 42.80% share of the emergency stop switches market in 2025 and also recorded the highest projected regional CAGR, at 11.64% through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Emergency Stop Switches Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tighter Machinery Safety Enforcement And Functional Safety Compliance | +3.5% | Global, with early-mover intensity in EU, North America, and APAC core | Short term (≤ 2 years) |

| Higher Automation And Robotics Density In Discrete Manufacturing | +2.8% | APAC core, China, Japan, South Korea, Europe, North America | Medium term (2-4 years) |

| Conveyor And Warehouse Automation Expansion | +1.9% | North America and EU, with spill-over to India and Southeast Asia | Medium term (2-4 years) |

| Safety Retrofits In Process Industries And Heavy Machinery | +1.5% | Middle East, Europe, North America | Medium term (2-4 years) |

| Battery, Power Electronics, And High-Energy Assembly Line Build-Out | +1.1% | Europe, Germany, North America, APAC, China, South Korea | Medium term (2-4 years) |

| Hygiene-Grade And High-IP Emergency Stop Adoption In Food And Pharma Lines | +0.7% | Europe, North America, APAC, Japan, South Korea | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Tighter Machinery Safety Enforcement And Functional Safety Compliance

The emergency stop switches market is receiving its strongest near-term lift from changing machinery safety rules, because each new revision forces OEMs and machine builders to revisit approved designs and technical files. The February 2026 release of IEC 60947-5-5:2026 introduced new latch-mechanism test protocols and added Annex B for illuminated emergency stop devices that indicate active and inactive states, pushing product redesign and recertification work across vendor portfolios. ISO 13849:2023 and IEC 62061:2021/A1:2024 continue to support higher performance expectations for emergency stop functions, and high-automation settings often move beyond baseline compliance toward PLe or SIL 3 design targets.[2]ZVEI, “Safety of Machinery, Information on the Application and Delimitation of the Standards EN 62061 and EN ISO 13849 Version 1.1,” ZVEI, zvei.org The revised EU Machinery Regulation 2023/1230 widens the compliance lens to cover autonomous mobile machinery, connected equipment, and AI-based safety functions, which is raising the value of certified safety components before the rule becomes effective in January 2027. That shift means emergency stop devices are now treated less as simple accessories and more as fixed bill-of-materials items that must withstand both mechanical and system-level review. The emergency stop switches market, therefore, benefits not only from replacement demand but also from a broader shift toward higher-specification devices that enhance audit readiness and reduce conformity risk.

Higher Automation And Robotics Density In Discrete Manufacturing

The emergency stop switches market is also supported by rising robot density, as each industrial robot cell, cobot station, or automated module adds certified stop points to the machine safety layout. IFR reported that Western Europe reached 267 robots per 10,000 manufacturing employees in 2024, while the United States reached 307, which kept North America and Europe among the highest-density regions for safety-device content per installed machine. China reached 166 robots per 10,000 manufacturing employees in 2024 and held the largest operational stock worldwide, keeping unit demand high even as certified device content per machine still trails that of the most regulated factories. IFR also recorded 64,542 cobot installations worldwide in 2024 and 199,000 professional service robot installations, both of which matter because collaborative settings and mobile automation require more distributed safety functions and clearer human-access emergency stop access. IDEC’s Emergency Stop Assist System showed how this need is spreading into AGV and AMR environments, where wireless remote actuation becomes useful when operators cannot reach a fixed button fast enough. The emergency stop switches market gains from this trend because higher automation density does not just increase unit counts; it also raises demand for multi-contact, interlock-integrated, and remotely accessible designs.

Conveyor And Warehouse Automation Expansion

The emergency stop switches market is seeing a wider installed base in warehouses and conveyor-heavy logistics sites, where device demand rises with each protected zone rather than with each standalone machine. Long conveyor runs continue to favor rope-pull devices because a single actuator can protect extended spans and allow local shutdown at the point of risk without stopping the entire line. Modular fulfillment layouts are also increasing the number of shared spaces where people, sortation equipment, and mobile robots interact, which pushes designers toward more distributed emergency stop points and more granular safety logic. In these environments, the value shifts from a single-panel device to a network of access points that can isolate one zone while keeping adjacent sections available for controlled operation. Schmersal’s ZQ901 pull-wire emergency stop switch, shown for harsh ambient conditions in bulky goods and conveyor applications, reflects this response to longer belt runs and rougher industrial handling settings. As warehouse investment spreads into India and Southeast Asia, the emergency stop switches market should continue to benefit from the simple fact that larger automated footprints need more stop nodes, more zone boundaries, and stronger field-level safety integration.

Safety Retrofits In Process Industries And Heavy Machinery

The emergency stop switches market is also supported by retrofit demand, which follows a different spending cycle from new equipment, as operators often replace devices while modernizing entire safety architectures. New Frontier Technologies documented an emergency shutdown upgrade in natural gas processing that included field-level safety push-button monitoring and area-specific protection bypass, demonstrating how older installations are moving toward safety-rated PLC systems. A 2025 Scientific Reports study on petrochemical emergency shutdown system management identified equipment and infrastructure age as one of the confirmed factors that weaken inspection, testing, and maintenance quality, which strengthens the case for planned replacement cycles. Pohlann Maschinensicherheit also showed that hydraulic press retrofits are now moving from single-channel circuits toward dual-channel Category 4 and PLe arrangements, with validation and documentation accounting for a large share of total engineering effort. This makes retrofits commercially important because the switch itself is only one line item inside a much larger compliance package, yet the certified device remains non-negotiable. The emergency stop switches market benefits from that structure because every brownfield upgrade tends to lock buyers into validated, traceable, and application-matched components rather than the cheapest available substitute.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy Retrofit Downtime And Validation Costs | -1.5% | Global, elevated in South America, Middle East, Africa | Medium term (2-4 years) |

| Price Pressure From Low-Cost, Non-Certified Products | -1.0% | APAC, Southeast Asia, South America, Middle East and Africa | Long term (≥ 4 years) |

| Cyber-Validation Burden For Diagnostic And Networked Emergency Stop Nodes | -0.6% | Europe, North America, APAC tech hubs | Short term (≤ 2 years) |

| Human-Factors Failures From Poor Placement And Guarding | -0.3% | Global, with elevated frequency in South Asia and South America | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Legacy Retrofit Downtime And Validation Costs

The largest commercial friction point in the emergency stop switches market is still the system engineering effort around a retrofit, not the price of the switch itself. Revere Control Systems noted that machine downtime, functional testing, and compliance documentation can consume 30-40% of retrofit engineering hours, and that burden is especially hard to justify in continuous-process operations, where even planned outages can incur major production losses.[3]Revere Control Systems, “A Practical Approach to Paper Mill Safety Upgrades,” Revere Control Systems, reverecontrol.com Pohlann’s 600-ton hydraulic press retrofit in Germany required a full safety control system replacement, new guard-door interlocks, stopping-time measurements, and audit-ready documentation before restart, which illustrates why smaller operators often delay projects. Many legacy-plant operators therefore postpone emergency-stop upgrades until an audit, insurance review, or major overhaul forces action, compressing procurement into shorter windows and increasing price sensitivity. PowerSafe Automation’s phased upgrade approach shows that the cost problem can be managed across 90-day, 3-12-month, and 12-24-month stages, but it also fragments order timing and complicates distributor planning. The emergency stop switches market, therefore, grows more slowly than the compliance need alone would suggest, because retrofit timing is often determined by outage economics rather than device urgency.

Price Pressure From Low-Cost, Non-Certified Products

The emergency stop switches market also faces a persistent pricing drag from low-cost and poorly documented products that mimic certified devices in appearance. Flexa Systems highlighted the growing risk of counterfeit industrial parts and noted that safety-related components remain attractive targets due to their high unit value and long replacement cycles. This pressure is strongest in Southeast Asia, South America, and parts of the Middle East and Africa, where online procurement channels make it easier for buyers to compare visually similar parts while missing differences in traceability, direct-opening action, positive-guided contacts, and rated life. Some lower-tier products may carry marking for general industrial use, but that does not mean they satisfy the emergency stop function requirements expected under IEC 60947-5-5 and ISO 13850. That creates a two-tier structure in which premium vendors defend certified applications while price-led suppliers pull down average selling prices in less-regulated use cases. The emergency stop switches market is therefore shaped by both real demand growth and ongoing revenue leakage, especially where enforcement is weak, and buyers focus first on upfront cost.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Safety Integration Is Reshaping The Push-Button Paradigm

Push-button e-stop switches held a 60.51% share in 2025, making them the largest product pool in the emergency stop switches market, as they remain the default choice for operator panels, controller enclosures, and general machine workstations. Their position is tied to low installed cost, clear familiarity among operators, and a straightforward conformity path under the main emergency stop standards. ISO 13850 and IEC 60947-5-5 still serve as the visual and functional baseline for these devices through requirements for red actuators, yellow backgrounds, and direct-opening normally closed contacts. In practice, many machine builders still begin a design review with a push-button architecture and shift to a more complex device only if the hazard analysis calls for additional functions. That default behavior matters because it protects volume demand even as higher-specification alternatives grow faster. The emergency stop switches market, therefore, continues to rely on the push-button category as its broadest and most stable installed base.

Premium vendors still find room to differentiate within this mature segment by focusing on failure behavior, compact packaging, and easier machine-level certification. IDEC’s XW and XA series demonstrated this clearly through a short-body form and a reverse-energy structure that ensures normally closed contacts open even if the block is damaged or separated. At the same time, safety interlock-integrated e-stops are forecast to grow at a 11.11% CAGR through 2031, marking the fastest pace among product types and pointing to a different design logic. These devices combine emergency stop actuation, guard monitoring, and locking functions in a single housing, reducing wiring complexity and supporting higher diagnostic expectations in compact machine cells. Euchener's CTP is a live example of that shift, combining RFID guard locking, pushbutton controls, and emergency stop functionality in a PL e and Category 4 housing. Rope-pull switches remain essential in conveyor-heavy layouts, while foot-operated and palm- or mushroom-style variants retain their role in machine-tool, press, and retrofit applications, so the emergency stop switches industry is not replacing the push-button paradigm so much as building integrated safety layers around it.

By Reset Mechanism: Electronic Reset Enters Safety-Critical Applications

Push-pull reset mechanisms accounted for 47.54% of the market in 2025, making them the leading reset type in the emergency stop switches market, as they still offer the clearest physical confirmation that the hazard has been cleared before a restart request. Their wide use reflects both simplicity and a large North American installed base, where pull-reset has remained familiar in many machine categories. ISO 13850 does not favor pull-reset over twist-reset, but actual practice still varies by region and operator preference.[4]IDEC EMEA, “ISO 13850 | IDEC EMEA,” IDEC, idec.com Twist-release holds the next-largest share because European machinery designers often view the rotational action as a more deliberate human gesture, reducing the risk of accidental release. The emergency stop switches market keeps both formats active because neither one has displaced the other across all applications.

Automatic and electronic reset variants are projected to expand at a 11.02% CAGR through 2031, making them the fastest-growing reset type as flexible manufacturing cells move more restart logic into certified controllers. In these settings, the reset decision is not limited to an operator walking to a panel and releasing a button. Instead, the safety controller checks whether the emergency stop circuit is clear, whether the machine axes are in a safe state, and whether the validated logic has authorized the restart condition. That architecture fits collaborative robot cells, AGV interfaces, and compact automated modules where manual reset would slow operations or create access issues. Key-release and lockable versions are also gaining relevance in lockout and tagout procedures, especially where maintenance staff must control access to a machine while work is underway. IDEC’s padlock-capable offering, which accepts up to 12 personal locks on one device, shows how the emergency stop switches industry is adapting reset hardware to operational control needs rather than to stop function alone.

By End-User Industry: Energy And Utilities Overtakes Legacy Sectors In Growth Rate

Manufacturing and general machinery held a 39.52% share in 2025, keeping this category the largest end-use segment in the emergency stop switches market, as nearly every industrial machine with hazardous movement requires at least one certified stop device. This segment spans metalworking, plastics, packaging, printing, textiles, and other machinery, so its scale is supported by breadth rather than by one narrow application cycle. That wide base makes demand more stable, even when individual machinery categories slow down at different times. It also means that changes in factory architecture can shift product mix without removing the underlying need for emergency stop coverage. Revere Control Systems demonstrated this in a paper mill safety retrofit, combining safety PLCs, interlocked gates, scanners, and emergency stop circuits to reduce downtime and support zone-specific access. In that sense, the emergency stop switches market size for manufacturing and general machinery remains tied to its role as the baseline volume engine across industrial automation.

Energy and utilities are expected to grow at a 11.38% CAGR through 2031, making it the fastest-growing end-use segment, as high-energy systems place greater emphasis on validated stop functions and higher SIL expectations. Hydrogen electrolysis plants, battery energy storage systems, and wind-related substation infrastructure all operate in environments where uncontrolled stop failure carries serious operational consequences. That requirement pushes emergency stop design deeper into the functional safety loop rather than leaving it as a simple operator control. Conveyors and material handling are also expanding quickly because rope-pull devices scale with belt length, which raises switch content per site in mining and logistics facilities. Elevators and escalators remain steady amid replacement demand driven by modernization and code-driven maintenance panels. The emergency stop switches market size in energy and utilities is therefore growing faster than legacy machinery, as its projects combine capacity build-out with stricter functional safety thresholds in new infrastructure.

By ���ϲ����� Configuration: Multi-���ϲ����� Demand Reflects Diagnostic Architecture Shifts

1 NC configurations held a 37.83% share in 2025, making them the largest contact type in the emergency stop switches market, as they still meet the minimum interruption requirement in simpler safety relay applications. Their strength comes from installed-base logic, lower wiring complexity, and suitability for Category 1 or Category 2 settings where a normally closed contact can still support the intended loop function. Even so, revenue weight is shifting away from this format as safety controllers increasingly monitor multiple input channels and demand clearer fault detection. The 2 NC segment has benefited from that move because it offers dual-channel confirmation without the added packaging complexity of larger contact blocks. This creates a transition path for builders who need stronger diagnostics but do not yet need the highest redundancy level. The emergency stop switches market has therefore begun to shift from minimum-viable contact arrangements toward architectures that embed fault visibility into the device value.

Multi-contact configurations with more than 2 NC contacts are projected to grow at a 12.12% CAGR through 2031, making them the fastest-growing contact type in the report. Their rise is closely linked to robot cells, autonomous vehicle docks, and power-electronics assembly environments, where a single emergency-stop command may need to cut power, confirm braking, and maintain redundant safety outputs simultaneously. In these layouts, a switch is valued for how well it supports the diagnostic architecture, not just how quickly it opens the circuit. The 1 NO plus 1 NC arrangement still serves a useful niche: the normally open contact feeds machine status or supervisory signaling, while the normally closed contact handles the safety action. That is common in applications such as elevator door interlocks and conveyor zone signaling, where operational visibility matters alongside the protective stop. The emergency stop switches industry is therefore rewarding contact configurations that fit controller-based safety logic and multi-function safety tasks, rather than the simplest electromechanical format alone.

Geography Analysis

Asia-Pacific accounted for 42.80% of the emergency stop switches market share in 2025 and is also projected to expand at an 11.64% CAGR through 2031, which makes it both the largest and fastest-growing regional market in the report. The region combines mature high-automation economies such as Japan and South Korea with large expansion markets such as China and India, so it carries both installed-base depth and new-build momentum. IFR reported that China reached 166 robots per 10,000 manufacturing employees in 2024, leaving room for further growth in safety devices as factories move closer to export-grade compliance standards.[5]International Federation of Robotics, “World Robotics 2025,” International Federation of Robotics, ifr.org India’s greenfield manufacturing projects in electronics, semiconductors, and pharmaceuticals are also driving new demand for certified stop devices in facilities designed to meet multinational safety standards. South Korea and Japan continue to drive premium demand for interlock-integrated and communication-ready devices in semiconductor, display, and automotive manufacturing, and Schmersal’s March 2025 subsidiary launch in South Korea directly reflects that opportunity.

North America held the second-largest share in 2025, and the emergency stop switches market there is being shaped by reshoring, EV production, semiconductor investment, and warehouse automation build-out. IFR reported that North America reached 204 robots per 10,000 manufacturing employees in 2024, while the United States ranked among the world’s highest-density robot markets at 307 robots per 10,000 manufacturing employees. That operating base supports stronger safety-device content per machine, especially on high-voltage battery and power-electronics lines, where stop functions must meet more demanding safety logic. The region also has a sizeable legacy equipment base, which keeps retrofit demand active in presses, stamping systems, and injection molding lines. Europe remains the most compliance-intensive regional market, and the emergency stop switches market size there is being supported by Germany, the United Kingdom, France, and Italy as OEMs pre-qualify parts ahead of the EU Machinery Regulation implementation in January 2027.

South America, the Middle East, and Africa together make up a smaller share, but the emergency stop switches market is still expanding there through mining, oil and gas, utilities, and selective industrial modernization. Brazil leads South America through mining safety upgrades and agri-food processing expansion, where rope-pull devices and high-IP emergency stop units are well-suited for washdown and harsh-duty environments. The Middle East is supported by Saudi Arabia and the UAE, where energy projects and industrial free zones are increasing the adoption of internationally certified safety systems aligned with IEC and ISO standards. Africa remains nascent, with South Africa and Egypt accounting for much of the regional demand through mining, utilities, and food manufacturing.

Competitive Landscape

The emergency stop switches market remains moderately concentrated, with the top 5 suppliers holding a notable share of global revenue, while a long tail of regional specialists, component suppliers, and niche safety players compete below them. That structure gives leading firms scale advantages in certification, engineering support, and channel reach, but it does not eliminate competition because customers still compare delivery times, customization, and application fit at the project level. European suppliers such as Schmersal, Pilz, and EUCHNER are strongest in the highest-specification settings, where TÜV, UL, DGUV, or similar approvals are contractually required and where customers value functional safety support alongside the hardware. The emergency stop switches market, therefore, behaves like a technical selection market in its premium tiers and a price-sensitive component market in its lower tiers. Asian OEMs and value-tier manufacturers continue to exert pressure in less critical or more cost-driven applications, especially where enforcement is lighter, and buyers focus on immediate procurement cost.

Several strategic moves show how leading companies are trying to protect their position while expanding into faster-growth applications. Schmersal launched a global webshop in May 2026, which widened digital self-service procurement for OEMs and end users and supports broader volume capture across regions.[6]K.A. Schmersal GmbH and Co. KG, “IO-Link Safety, Schmersal Presents New Safety Solutions for the Smart Factory,” Schmersal, schmersal.com Schmersal also expanded its Asia-Pacific footprint through subsidiaries in South Korea and Vietnam, thereby strengthening local engineering support in electronics- and automation-heavy manufacturing hubs. EUCHNER has continued to push integrated guard-locking and emergency-stop designs that combine RFID monitoring, locking force, and stop functionality into a single compact node, supporting higher-value machine architectures. IDEC’s product and control solutions also show how vendors are linking the stop device more closely with safety-controller logic, remote actuation, and restart management rather than selling the button as a standalone part.

Open opportunities remain strongest in wireless and detachable emergency stop stations for AGV and AMR environments, hygiene-grade stainless steel devices for food and pharmaceutical lines, and ultra-compact devices for small machines, medical equipment, and charging hardware. Those gaps matter because the emergency stop switches market is shifting toward applications where space, washdown resistance, or mobile access changes the value of the device more than its base stopping function. Smaller European specialists such as COMEPI, Pizzato Elettrica, and Giovenzana still compete well in OEM niches by offering rapid customization and shorter lead times. ONPOW, despite its visible presence in general pushbutton volumes, has limited overlap with certified-safety-grade specifications that define the core scope of this market.

Emergency Stop Switches Industry Leaders

IDEC Corporation

K.A. Schmersal GmbH & Co. KG

EAO AG

Pilz GmbH & Co. KG

Bernstein AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: K.A. Schmersal GmbH and Co. KG launched a fully responsive global webshop, providing customers worldwide with simplified digital access to its complete safety-switch and safety-system product portfolio. The platform supports self-service procurement for OEM integrators and end-user buyers across all major regions.

- April 2026: ONPOW unveiled its latest innovation: the Ultra-Thin IP68 Push Button Switch. Designed for compact devices and demanding environments, this switch seamlessly blends smart design, robust durability, and precise functionality, setting a new benchmark for industrial components.

- January 2026: The International Electrotechnical Commission published IEC 60947-5-5:2026, the second edition of the standard governing emergency stop devices with mechanical latching functions, introducing new test methods for latch mechanisms, adding Annex B for illuminated emergency stop devices distinguishing active and inactive states, and revising structural alignment with the broader IEC 60947 series. The update compels device manufacturers to refresh product designs and conformity documentation.

- January 2026: ANDRITZ Schuler's 1.5-GW battery cell mass formation line entered operation at a leading battery manufacturer in southern Germany, featuring over 50,000 formation channels across 200 chambers, integrated power electronics, and fully automated loading and unloading. The deployment illustrates the scale of the safety-critical assembly-line infrastructure now commissioned in EV battery manufacturing.

Global Emergency Stop Switches Market Report Scope

The Emergency Stop Switches Market is Segmented by Product Type (Push-Button, Rope Pull, Foot-Operated, Palm/Mushroom, and Interlock-Integrated), Reset Mechanism (Push-Pull, Twist-Release, Key-Release, Lever, and Auto/Electronic), End-User Industry (Manufacturing, Elevators, Conveyors, Energy and Utilities, and Others), ���ϲ����� Configuration (1 NC, 2 NC, 1 NO+1 NC, and Multi-contact), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Push-Button E-Stop Switches |

| Rope Pull Switches |

| Foot-Operated E-Stop Switches |

| Palm / Mushroom Switches |

| Safety Interlock-Integrated E-Stops |

| Push-Pull |

| Twist-Release |

| Key-Release / Lockable |

| Lever / Mechanical Reset |

| Automatic / Electronic Reset |

| Manufacturing and General Machinery |

| Elevators and Escalators |

| Conveyors and Material Handling |

| Energy and Utilities |

| Other End-user Industries |

| 1 NC |

| 2 NC |

| 1 NO + 1 NC |

| Multi-contact (More than 2 NC) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Israel | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Product Type | Push-Button E-Stop Switches | |

| Rope Pull Switches | ||

| Foot-Operated E-Stop Switches | ||

| Palm / Mushroom Switches | ||

| Safety Interlock-Integrated E-Stops | ||

| By Reset Mechanism | Push-Pull | |

| Twist-Release | ||

| Key-Release / Lockable | ||

| Lever / Mechanical Reset | ||

| Automatic / Electronic Reset | ||

| By End-user Industry | Manufacturing and General Machinery | |

| Elevators and Escalators | ||

| Conveyors and Material Handling | ||

| Energy and Utilities | ||

| Other End-user Industries | ||

| By ���ϲ����� Configuration | 1 NC | |

| 2 NC | ||

| 1 NO + 1 NC | ||

| Multi-contact (More than 2 NC) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the 2026 value and 2031 forecast for emergency stop switches?

The market stands at USD 11.29 billion in 2026 and is forecast to reach USD 19 billion by 2031, which reflects an 10.98% CAGR over 2026-2031.

Which region leads global demand for emergency stop switches?

Asia-Pacific led in 2025 with 42.80% share and is also the fastest-growing region, supported by high robot installations, factory build-outs, and strong electronics manufacturing activity.

Which product category is the largest in emergency stop switches?

Push-button e-stop switches remained the largest product category in 2025 with 60.51% share because they stay standard across machine panels, robot enclosures, and operator stations.

Which product area is growing the fastest through 2031?

Safety interlock-integrated e-stops are forecast to grow the fastest at 11.11% CAGR because more machine designs now combine stopping, guard monitoring, and locking in one device node.

Why is energy and utilities growing faster than traditional machinery uses?

Energy and utilities is projected to grow at 11.38% CAGR through 2031 because hydrogen, battery storage, and high-voltage power systems require more demanding functional safety loops and validated stop functions.

What is the main commercial barrier for suppliers in this space?

Retrofit downtime and validation cost remain the biggest hurdle, since compliance work, testing, and documentation often weigh more heavily on project budgets than the device price itself.

Page last updated on: