Digital Diabetes Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

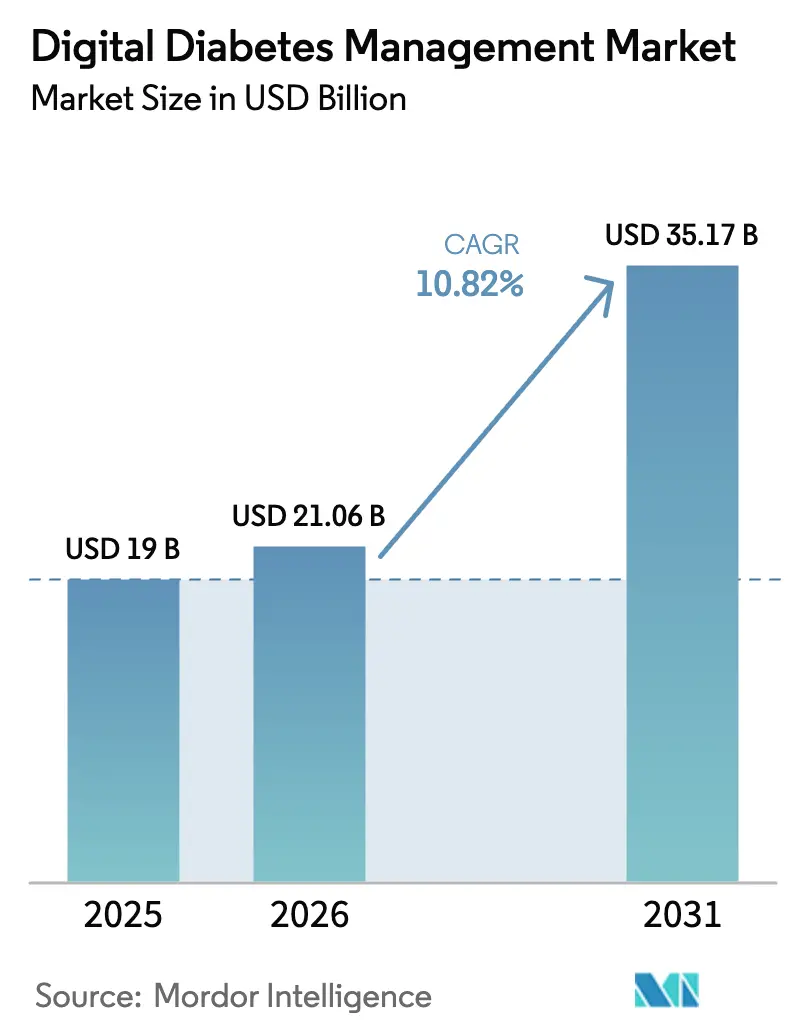

| Market Size (2026) | USD 21.06 Billion |

| Market Size (2031) | USD 35.17 Billion |

| Growth Rate (2026 - 2031) | 10.82% CAGR |

| Fastest Growing Market | North America |

| Largest Market | North America |

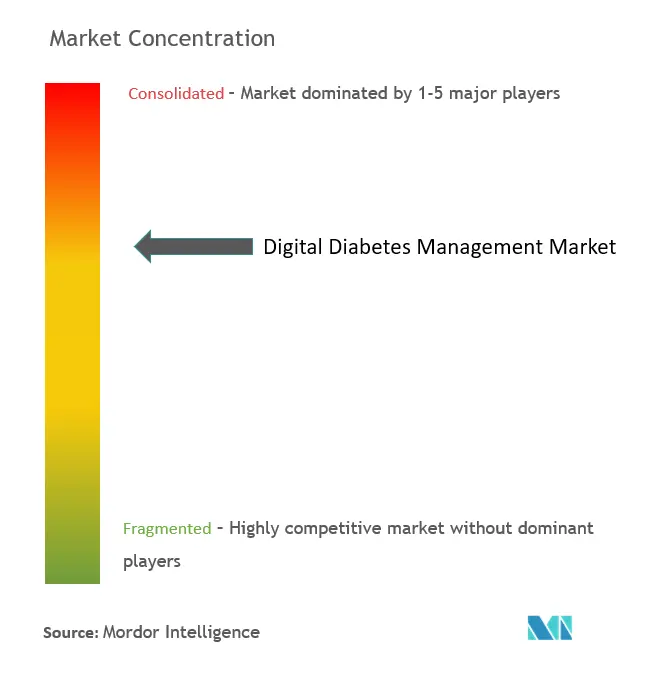

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Digital Diabetes Management Market Analysis by ���ϲ�����

Digital diabetes management market size in 2026 is estimated at USD 21.06 billion, growing from 2025 value of USD 19.00 billion with 2031 projections showing USD 35.17 billion, growing at 10.82% CAGR over 2026-2031. This growth reflects the convergence of continuous glucose monitoring (CGM), artificial-intelligence-driven dosing algorithms, and value-based reimbursement that is pushing diabetes care from reactive monitoring toward predictive, precision intervention. Regulatory agility—exemplified by the FDA’s streamlined over-the-counter (OTC) CGM approvals—removes prescription hurdles and broadens consumer access. Partnerships between medical-device incumbents and software innovators are collapsing traditional innovation cycles, while remote-monitoring reimbursement codes reward providers for demonstrable outcome improvements in glycemic control. At the same time, patient demand for self-care tools is rising as smartphone penetration and digital literacy expand worldwide, especially across Asia-Pacific. Competitive intensity is increasing as device makers embed AI to personalize insulin delivery, even as privacy-compliance costs and emergent GLP-1 pharmacotherapies create countervailing market headwinds.

Key Report Takeaways

- By product category, continuous glucose monitoring systems led with 47.68% revenue share of the digital diabetes management market in 2025; smart insulin pumps are projected to expand at a 11.74% CAGR to 2031.

- By type, wearables captured 54.90% of the digital diabetes management market share in 2025, while handheld devices are forecast to grow at an 11.42% CAGR through 2031.

- By end user, self/home healthcare accounted for 64.05% share of the digital diabetes management market size in 2025, whereas hospitals & specialty diabetes clinics are advancing at an 11.55% CAGR through 2031.

- By geography, North America maintained 41.95% share of the digital diabetes management market in 2025; Asia-Pacific is the fastest-growing region at a 11.98% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Digital Diabetes Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid uptake of CGM & hybrid closed-loop systems | +2.5% | Global, led by North America & Europe | Medium term (2-4 years) |

| Smartphone-driven diabetes apps integrated with EHRs | +1.8% | Global, accelerated in Asia-Pacific | Short term (≤ 2 years) |

| Shift to value-based care & reimbursement for remote monitoring | +1.2% | North America & Europe | Long term (≥ 4 years) |

| AI-powered predictive dosing & digital twins | +0.9% | Global, early adoption in developed markets | Medium term (2-4 years) |

| OTC CGM approvals targeting the T2D mass market | +0.7% | North America, expanding to Europe | Short term (≤ 2 years) |

| Employer-funded digital therapeutics in wellness plans | +0.6% | North America, emerging in Europe | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Rapid Uptake of CGM & Hybrid Closed-Loop Systems

Hybrid closed-loop ecosystems that fuse CGM data with automated insulin delivery are elevating time-in-range performance by 15-20 percentage points versus legacy pump therapy, resulting in lower long-term complication rates [1]Journal of Diabetes Science and Technology, “Hybrid Closed-Loop Systems Improve Time-in-Range,” sagepub.com. The FDA’s predetermined change-control plans for software updates are compressing iteration cycles from years to months, letting vendors refine algorithms continuously without new submissions. New CGM sensors are adding real-time ketone tracking, reducing diabetic ketoacidosis events during acute illness. Despite clinical gains, insurance coverage gaps persist; only 40% of eligible patients receive reimbursement for hybrid systems, capping penetration in key markets. As more longitudinal evidence emerges, payers are expected to recognize total-cost-of-care savings, supporting the digital diabetes management market’s broader expansion.

Smartphone-Driven Diabetes Apps Integrated With EHRs

Prescription-grade apps now deliver algorithmic insulin recommendations that combine CGM, meal logs, and step counts, transforming episodic clinical visits into data-rich tele-consultations. Fast Healthcare Interoperability Resources (FHIR) APIs ease bidirectional data flow between apps and hospital systems, though many providers still lack the IT bandwidth to act on streaming glucose feeds. Randomized studies show 0.5-0.8% HbA1c reductions when smartphone-integrated tools augment standard care. Engagement levels typically drop after six months, pushing developers to embed social-support nudges and gamification to sustain usage. Ecosystem platforms such as Glooko and mySugr are scaling by bundling medication tracking, nutrition coaching, and remote consultations, reinforcing stickiness within the digital diabetes management market.

Shift to Value-Based Care & Reimbursement for Remote Monitoring

New remote-patient-monitoring (RPM) CPT codes reimburse physicians for reviewing CGM data, creating predictable revenue streams that offset device costs. Medicare Advantage plans are pioneering outcome-based contracts that tie vendor payments to time-in-range metrics and hospitalisation reductions, aligning economic incentives across stakeholders. Providers that embed RPM into care pathways report 20-30% declines in emergency-department visits over 12-18 months. Standardising outcome measures beyond HbA1c remains challenging, but early metrics show meaningful cost savings, bolstering the digital diabetes management market.

AI-Powered Predictive Dosing & Digital Twins

Machine-learning models mine years of sensor readings, meal diaries, and exercise trends to forecast glucose trajectories and suggest micro-bolus adjustments minutes ahead of excursions. Digital-twin simulations let clinicians test therapy changes in silico before real-world application, compressing titration cycles from weeks to hours. Regulatory frameworks for software as a medical device (SaMD) now accommodate continuous-learning algorithms, though documentation burdens still challenge smaller developers. Early trials show AI-guided dosing achieves glycemic outcomes comparable to endocrinologist input while reducing clinician workload. Wider adoption will hinge on diverse training datasets that prevent algorithmic bias across ethnic and age cohorts, a critical factor for equitable growth of the digital diabetes management market.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy compliance costs | −1.4% | Global, stricter in Europe (GDPR) | Short term (≤ 2 years) |

| Unequal broadband/smartphone penetration in emerging markets | −0.8% | Asia-Pacific, MEA, Latin America | Long term (≥ 4 years) |

| Regulatory lag for AI-as-SaMD risk classification | −0.6% | Global, varying by jurisdiction | Medium term (2-4 years) |

| GLP-1 drug momentum cannibalizing device adoption | −0.5% | North America & Europe | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Data-Privacy Compliance Costs

Health systems deploying connected CGM and dosing apps shoulder annual privacy-program outlays that can top USD 2.8 million, with GDPR penalties amplifying risk for non-compliance [2]European Commission, “GDPR Compliance Costs in Health IT,” commission.europa.eu. Emerging vendors often allocate 15-25% of operating budgets to encryption, audit logging, and breach-notification infrastructure, slowing market entry. Multidevice consent management is complex because CGM sensors, pumps, smartphone apps, and EHR portals all share personal data. As cybersecurity insurance premiums rise, small practices hesitate to onboard new platforms, tempering near-term growth in the digital diabetes management market.

GLP-1 Drug Momentum Cannibalizing Device Adoption

GLP-1 receptor agonists flatten post-prandial glucose curves, leading many type 2 patients to test glucose 40-60% less often. Insurers frequently prioritise GLP-1 coverage over devices, assuming tablet therapy offsets the need for hardware. Device makers are repositioning CGM as a complementary bio-feedback loop that enhances drug adherence and dietary choices. However, monthly drug costs of USD 800–1,200 and emerging evidence that CGM can optimise GLP-1 titration suggest a mixed long-term impact rather than total substitution, preserving medium-range expansion of the digital diabetes management market.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Wearables Drive Seamless Integration

Wearable devices accounted for 54.90% revenue share of the digital diabetes management market in 2025, reflecting consumer preference for discreet patch sensors and tubeless pumps that wirelessly sync to smartphones. Segment-level digital diabetes management market size for wearables is projected to reach USD 18.63 billion by 2031 at a CAGR of 10.18%, outpacing handheld adoption. Patch CGM eliminates fingerstick calibration, improving adherence, while smartwatches are beginning to display real-time glucose alerts, fostering instant behavioural tweaks.

Handheld devices, though smaller in absolute value, are rising at an 11.42% CAGR, driven by Bluetooth glucose meters that auto-upload readings to cloud portals. AI-enhanced meters now recommend insulin dose ranges based on trend analytics, narrowing the feature gap with pump systems. As cost-sensitive markets in Latin America and parts of Asia seek affordable entry points, connected meters keep the digital diabetes management market diversified and accessible.

By Product: CGM Systems Lead Innovation

Continuous glucose monitoring systems dominated with 47.68% market share in 2025, translating into a segment digital diabetes management market size of USD 9.06 billion. OTC clearance of Dexcom Stelo and Abbott Libre Rio opens a vast type 2 population who previously faced prescription barriers, reinforcing scale advantages.

Smart insulin pumps are set to log the fastest 11.74% CAGR through 2031 as closed-loop automation gains traction. Smart pens and connected caps serve injection-based regimens, feeding dose data into analytics dashboards that integrate with CGM. Data-management and analytics platforms aggregate multidevice feeds, offering clinicians population-level dashboards; this interoperability keeps the digital diabetes management industry firmly positioned as a data-centric ecosystem.

By End User: Home Healthcare Transformation

Self/home healthcare accounted for 64.05% of demand in 2025 as pandemic-era telehealth normalised virtual diabetes coaching and remote CGM sharing. Time-in-range progress and lower hypo episodes are fostering long-term user loyalty, further boosting the digital diabetes management market.

Hospitals and specialty clinics are forecast to grow 11.55% annually as inpatient-glycemic-control protocols adopt real-time CGM streams to reduce DKA admissions. Academic sites increasingly use research-grade CGM datasets for metabolic-phenotyping studies, expanding procurement of high-resolution sensors. Employer-sponsored wellness programmes reinforce home-based monitoring, blurring traditional care-site boundaries.

Geography Analysis

North America held 41.95% market share in 2025 on the back of broad insurance coverage for CGM and RPM, and the FDA’s Digital Health Centre of Excellence that accelerates SaMD approvals. Regional digital diabetes management market size is projected to reach USD 14.21 billion by 2031, driven by ageing cohorts with rising type 2 incidence. Telehealth reimbursement parity laws enacted across 38 states improve rural access, and employer-sponsored digital therapeutics continue to scale among self-insured corporations.

Europe remains a mature but opportunity-rich arena. Stringent data-protection rules elevate trust, yet lengthen device-approval timelines under the Medical Device Regulation. Germany’s DiGA fast-track app reimbursement proves a template for integrating prescription digital therapeutics. France and the Nordics are piloting national CGM procurement for paediatric type 1 cohorts, ensuring that the digital diabetes management market sustains moderate but stable growth.

Asia-Pacific is the fastest-growing region at 11.98% CAGR, fuelled by 5G rollout, smartphone affordability, and national e-health missions in China, India, and Indonesia. Governments subsidise domestic CGM manufacturing, lowering entry price points. However, broadband gaps in rural provinces and diverse regulatory frameworks pose execution risks. Middle East & Africa and South America register single-digit growth as infrastructure builds out, with corporate wellness programmes and cash-pay segments leading early uptake.

Competitive Landscape

The digital diabetes management market remains moderately concentrated. Abbott and Medtronic’s alliance integrates FreeStyle Libre sensors with Medtronic insulin-delivery algorithms, pooling complementary strengths and locking in formularies at payers and IDNs. Dexcom focuses on software-driven ecosystem expansion, adding meal-logging AI and predictive-alert upgrades across its G-series lineage. Insulet’s Omnipod GO targets type 2 basal-only users, widening addressable demographics without tubing complexity.

Emerging players such as Bigfoot Biomedical, One Drop, and Glooko leverage cloud architectures and direct-to-consumer app distribution to undercut legacy channel costs. Many license sensor data under analytics-as-a-service models, positioning themselves as population-health enablers rather than hardware sellers. Partnerships with pharmacy chains and employers amplify reach.

Strategic M&A remains active: Tandem acquired algorithm specialist Sugarmate for its real-time data engine, and Ascensia partnered with Senseonics for implantable CGM, illustrating the race to differentiate through advanced data layers. Vendor roadmaps emphasise AI-enabled decision support, multi-parameter wearable fusion, and region-specific affordability strategies—collectively sustaining competitive dynamism within the digital diabetes management market.

Digital Diabetes Management Industry Leaders

Abbott

F. Hoffmann-La Roche Ltd.

Insulet Corporation

Dexcom

Medtronic

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Medtronic plc secured FDA clearance for its InPen app’s missed-meal dose-detection feature, paving the way for its Smart MDI system with Simplera CGM integration.

- January 2024: Abbott and Tandem Diabetes Care launched U.S. availability of Control-IQ-enabled t:slim X2 pumps integrated with FreeStyle Libre 2 Plus sensors.

- April 2023: Insulet Corporation received FDA clearance for Omnipod GO, a tubeless insulin-delivery device for adults with type 2 diabetes requiring daily basal insulin.

- March 2023: Becton Dickinson introduced the BD Diabetes Care App to deliver curriculum-based guidance for patients, caregivers, and educators.

Global Digital Diabetes Management Market Report Scope

Digital health management includes devices, services, and platforms that play an important role in the care of individuals with diabetes and simplify self-management.

The digital diabetes management market is segmented by type (wearable devices and handheld devices), product (smart glucose meters, continuous glucose monitoring systems, smart insulin pens, smart insulin pumps, apps), and geography (North America, Europe, Asia-Pacific, the Middle East and Africa, and Latin America).

The report offers the values (in USD) and volume (in units) for the above segments.

| Wearable Devices | Patch CGM |

| Smart Insulin Pumps | |

| Handheld Devices | Smart Glucose Meters |

| Continuous Glucose Monitoring Systems |

| Smart Glucose Meters |

| Smart Insulin Pumps |

| Smart Insulin Pens |

| Diabetes Management Apps |

| Data-Management & Analytics Platforms |

| Self / Home Healthcare |

| Hospitals & Specialty Diabetes Clinics |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Wearable Devices | Patch CGM |

| Smart Insulin Pumps | ||

| Handheld Devices | Smart Glucose Meters | |

| By Product | Continuous Glucose Monitoring Systems | |

| Smart Glucose Meters | ||

| Smart Insulin Pumps | ||

| Smart Insulin Pens | ||

| Diabetes Management Apps | ||

| Data-Management & Analytics Platforms | ||

| By End User | Self / Home Healthcare | |

| Hospitals & Specialty Diabetes Clinics | ||

| Academic & Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big is the Digital Diabetes Management Market?

The Digital Diabetes Management Market size is expected to reach USD 21.06 billion in 2026 and grow at a CAGR of 10.82% to reach USD 35.17 billion by 2031.

Which product segment leads the market today?

Continuous glucose monitoring systems hold 47.68% of 2025 revenue, making them the largest product category.

Who are the key players in Digital Diabetes Management Market?

Abbott, F. Hoffmann-La Roche Ltd., Insulet Corporation, Dexcom and Medtronic are the major companies operating in the Digital Diabetes Management Market.

Which is the fastest growing region in Digital Diabetes Management Market?

Asia-Pacific is the fastest-growing region, advancing at a 11.98% CAGR through 2031.

Which region has the biggest share in Digital Diabetes Management Market?

In 2025, the North America accounts for the largest market share in Digital Diabetes Management Market.

Page last updated on: