Dialyzer Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.11 Billion |

| Market Size (2031) | USD 7.04 Billion |

| Growth Rate (2026 - 2031) | 6.62% CAGR |

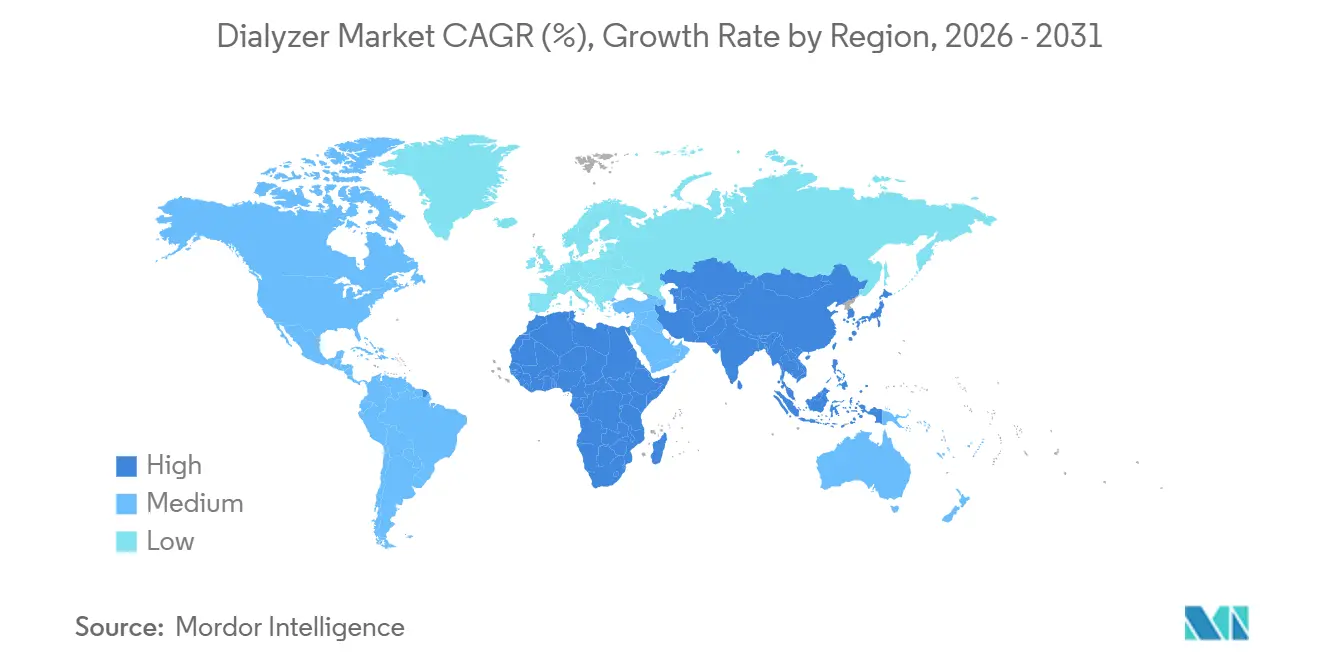

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

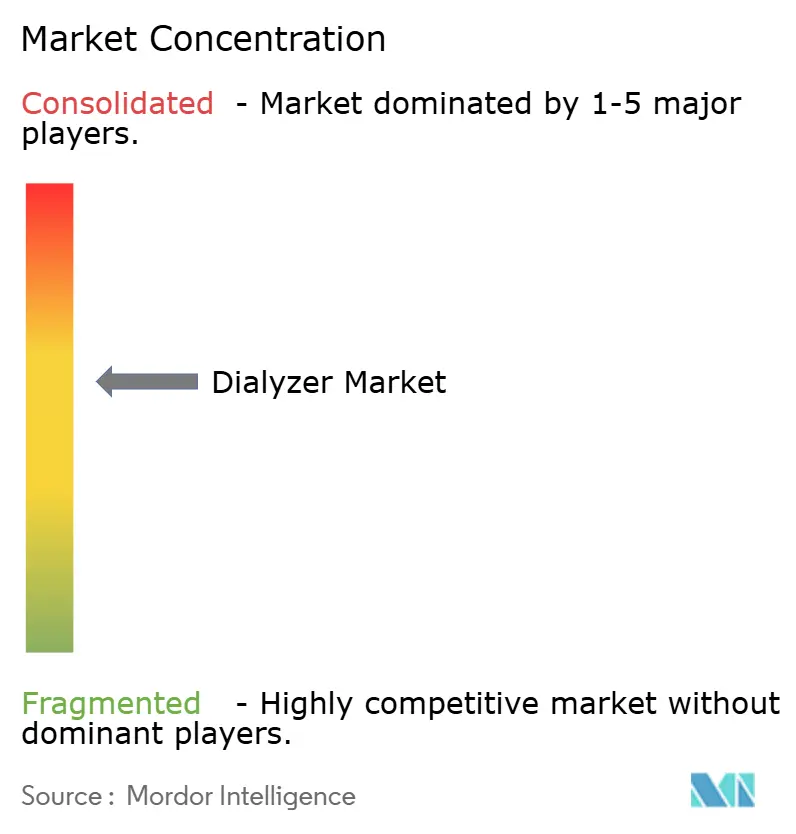

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Dialyzer Market Analysis by ���ϲ�����

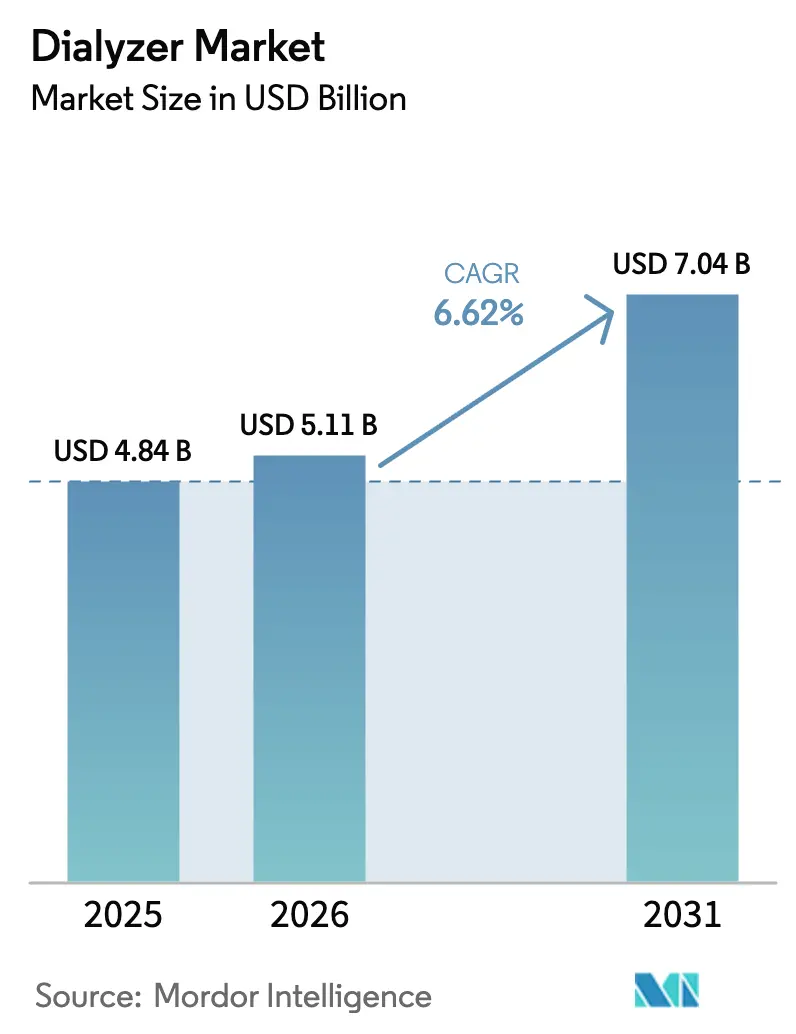

The Dialyzer Market size is expected to increase from USD 4.84 billion in 2025 to USD 5.11 billion in 2026 and reach USD 7.04 billion by 2031, growing at a CAGR of 6.62% over 2026-2031.

Demand is shifting toward high-flux and medium cut-off products as nephrologists prioritize larger middle-molecule clearance to curb cardiovascular mortality, while infection-control mandates sustain the rise of disposable single-use formats.[1]Centers for Disease Control and Prevention, “Infection Control Recommendations for Hemodialysis Facilities,” Centers for Disease Control and Prevention, cdc.gov Asia-Pacific is set to outpace developed regions on the back of insurance expansion in China and India that unlocks rural treatment capacity.[2]National Health Commission of the People’s Republic of China, “Annual Report on Dialysis Reimbursement Expansion 2025,” National Health Commission, nhc.gov.cn Cost advantages from localized polysulfone resin and vertical integration are helping regional manufacturers underbid multinationals without sacrificing ISO 13485 compliance. At the same time, European guidelines now favor online hemodiafiltration, prompting dialysis centers to upgrade to membranes compatible with higher convective volumes.

Key Report Takeaways

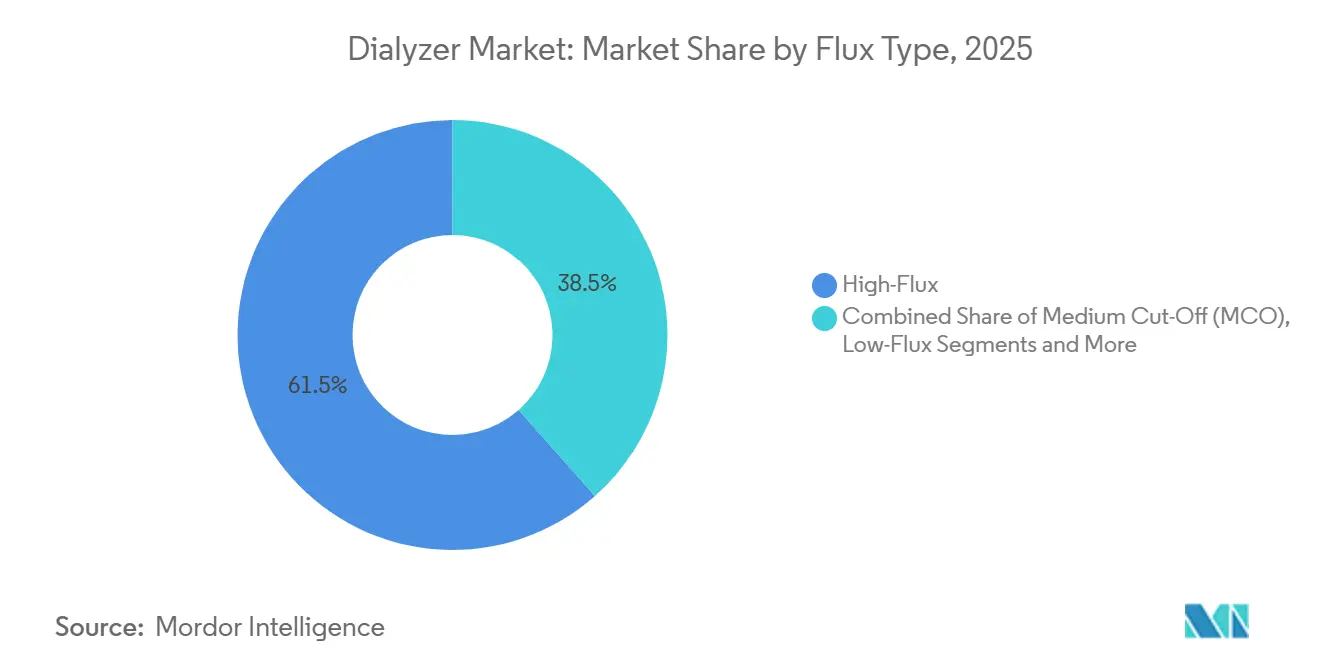

- By flux type, high-flux units led with 61.53% of the dialyzer market share in 2025, while medium cut-off membranes are projected to expand at a 10.74% CAGR through 2031.

- By usage type, disposable dialyzers captured 68.92% of global volume in 2025; the category is expected to grow at a 9.45% CAGR to 2031.

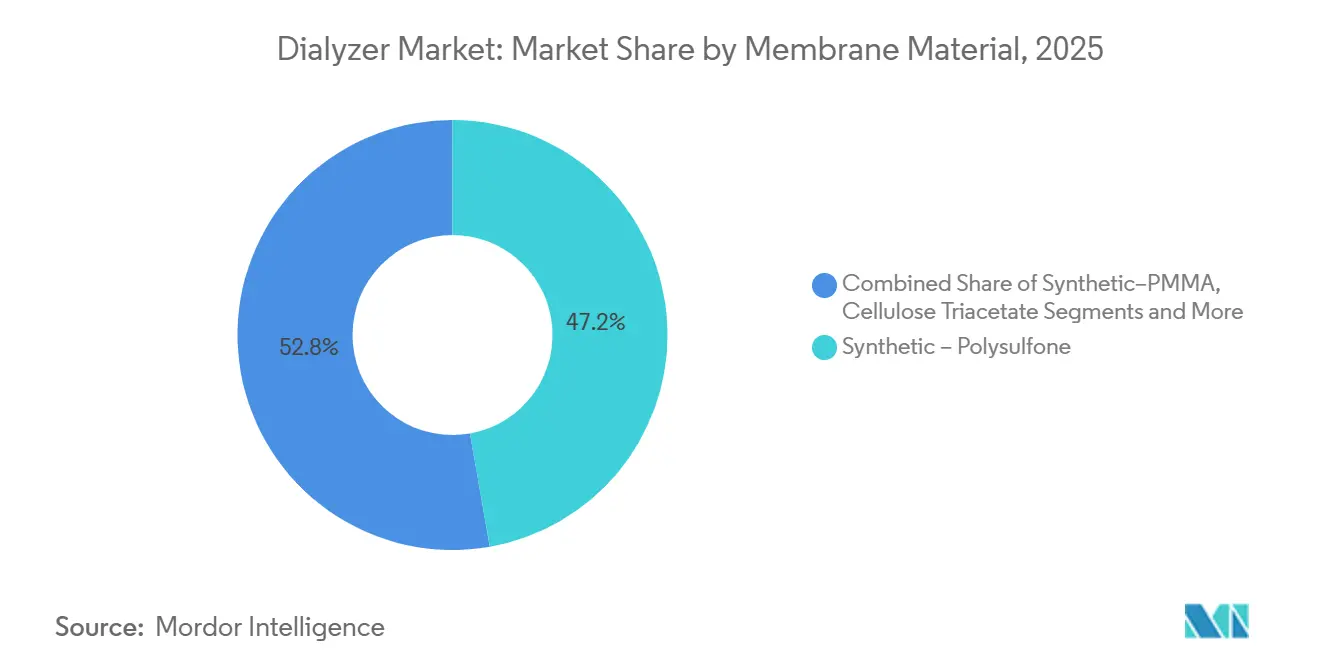

- By membrane material, polysulfone held 47.22% of the dialyzer market size in 2025, whereas PMMA membranes register the fastest forecast growth at 9.68% CAGR.

- By end user, in-center facilities accounted for 76.33% of demand in 2025, while home dialysis is advancing at an 8.46% CAGR to 2031.

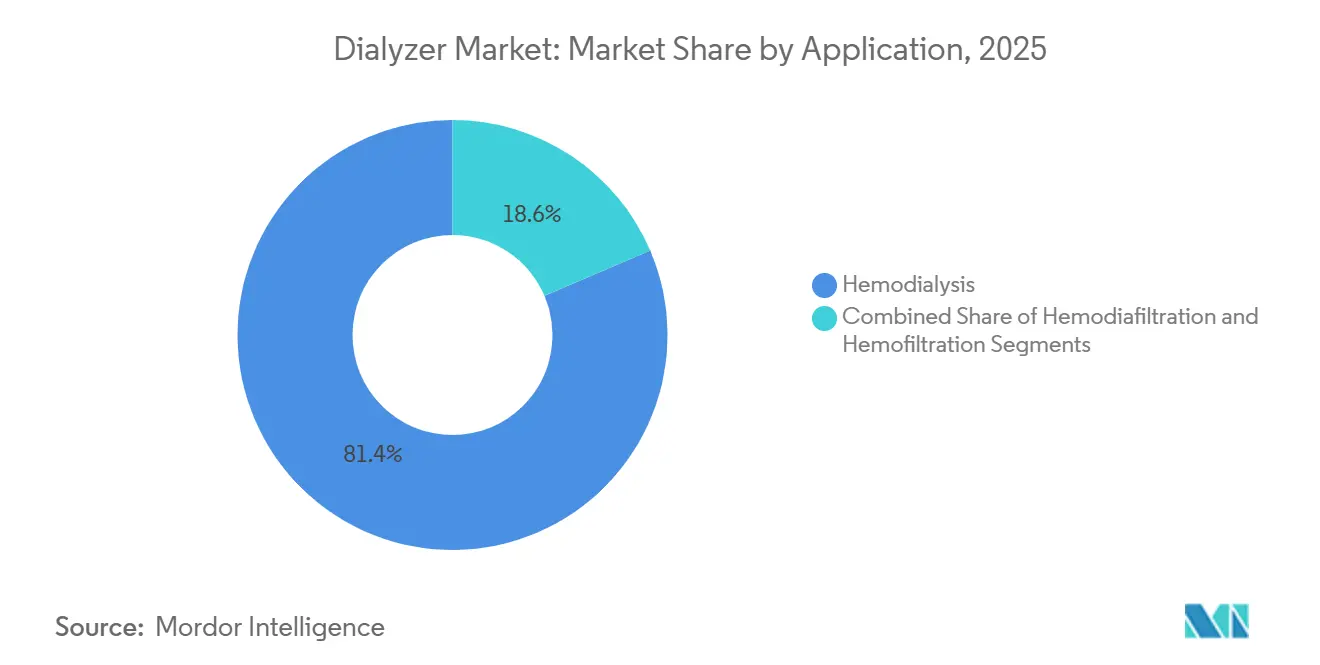

- By application, hemodialysis dominated with 81.43% share in 2025; hemodiafiltration is set to accelerate at a 10.62% CAGR through 2031.

- By patient group, adults represented 76.24% of 2025 volume, yet geriatric demand is growing faster at an 8.52% CAGR over the forecast period.

- By geography, North America held 36.82% revenue share in 2025, while Asia-Pacific is forecast to rise at an 8.93% CAGR toward 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dialyzer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising CKD & ESRD Prevalence | +1.8% | Global, with highest absolute growth in APAC and MEA | Long term (≥ 4 years) |

| Rapid Adoption of High-Flux & MCO Dialyzers | +1.2% | North America, Europe, Japan; emerging uptake in urban China and India | Medium term (2-4 years) |

| Healthcare-Infrastructure Expansion in APAC | +1.0% | APAC core (China, India, Indonesia), spill-over to Southeast Asia | Medium term (2-4 years) |

| Localized Polysulfone Supply Chains Lower Costs | +0.7% | China, India, South Korea; indirect benefits in MEA and South America | Short term (≤ 2 years) |

| Hv-HDF Clinical Evidence Drives Dialyzer Upgrades | +0.6% | Europe, select centers in North America and Australia | Medium term (2-4 years) |

| Expansion of Heparin-Free Dialyzers Broadens Patient Eligibility | +0.4% | Global, with early adoption in North America and Western Europe | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Rising CKD & ESRD Prevalence

Chronic kidney disease now affects about 850 million people worldwide, and the end-stage form is climbing fastest in low-income nations where late diagnosis is common.[3]International Society of Nephrology, “Chronic Kidney Disease,” isn-online.org China recorded more than 900,000 maintenance-dialysis patients in 2025 after rural insurance started covering 80% of treatment costs in tier-3 cities. India added 1,200 public dialysis centers under its national program by 2025, yet fewer than 15% of new ESRD cases secure regular therapy within six months. Diabetes and hypertension account for over 70% of new Asian cases, a share that has risen eight points since 2020. Public payers are shifting toward bundled contracts that reward lower hospitalization rates, pushing manufacturers to invest in membranes that improve survival.

Rapid Adoption of High-Flux & MCO Dialyzers

High-flux units held 61.53% share in 2025 because they clear beta-2 microglobulin better than low-flux models, cutting dialysis-related amyloidosis. Medium cut-off membranes remove even larger toxins without losing much albumin, which standard high-flux designs cannot match. Germany introduced an EUR 8 per-session add-on for MCO therapy in 2025, spurring uptake. Fresenius reported 35% shipment growth for MCO dialyzers in 2025 compared with 7% overall volume growth. Japan added middle-molecule clearance targets to its quality framework in 2024, accelerating the phase-out of low-flux products.

Healthcare-Infrastructure Expansion in APAC

Regional governments pledged more than USD 8 billion for dialysis capacity during 2024-2025. China allocated CNY 12 billion (USD 1.7 billion) to county-level hospitals in 2025. India’s Ayushman Bharat scheme began covering home-hemodialysis consumables in 2024, expected to lift dialyzer demand 12% a year. Indonesia signed a deal in 2025 with Nipro to build 50 satellite centers across Java and Sumatra. South Korea raised reimbursement for high-flux membranes by 8% in 2025, aligning payment with higher input costs. These projects enlarge the addressable base but strain supply chains for ultrapure water systems that high-performance therapy requires.

Localized Polysulfone Supply Chains Lower Costs

China added about 40,000 tons of polysulfone resin capacity between 2024 and 2025, cutting landed membrane costs 15-20% for Asian dialyzer makers. Weigao trimmed raw-material expenses 18% in 2025 and lifted gross margin four points without raising prices. Browndove opened an integrated extrusion line in India in late 2024, halving lead times to six weeks. South Korea’s resin imports fell 25% in 2025 even as dialyzer exports rose 12%, signaling substitution of local supply. Cheaper input boosts competitiveness in tenders for single-use products where resin accounts for around 30% of material cost.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Therapy & Device Cost Barriers | -1.1% | Low- and middle-income countries in APAC, MEA, and South America | Long term (≥ 4 years) |

| Stringent Sterilization/Biocompatibility Regulation | -0.6% | Global, with most acute impact in North America and Europe | Medium term (2-4 years) |

| PVP-Leachate Safety Concerns Affecting Tenders | -0.5% | Europe, Japan, and select North American health systems | Short term (≤ 2 years) |

| Heightened Regulatory Focus on Single-Use Plastic Waste | -0.4% | Europe, with emerging adoption in APAC and North America | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

High Therapy & Device Cost Barriers

Out-of-pocket dialysis expenses range from USD 12,000 to USD 30,000 a year in markets without broad insurance, a level that excludes many ESRD patients. India’s rural households spend roughly 150% of median income to finance dialysis, causing high dropout in the first 12 months. Brazil’s public insurance reimburses BRL 180 (USD 36) per session, about 40% below estimated operating cost, which is forcing center closures in underserved areas. Manufacturers must choose between lowering prices and protecting R&D budgets, a trade-off that slows innovation in low-income regions. Tiered-pricing pilots offer stripped-down dialyzers with smaller surface areas, yet these models lack the performance needed for high-flux or HDF therapy.

Stringent Sterilization / Biocompatibility Regulation

Revised ISO and EU Medical Device Regulation rules now require broader cytotoxicity, endotoxin, and leachate testing, adding six to nine months to European product launches and raising compliance costs about 10%. The U.S. FDA has intensified post-market surveillance, mandating real-time adverse-event reporting through electronic Medical Device Reporting portals. Many dialysis providers delay switching to new membranes until manufacturers clear the expanded tests, slowing adoption of incremental upgrades. Smaller Asian suppliers face higher relative burdens because each new lot must be validated in accredited labs, stretching working capital. Heightened scrutiny benefits large incumbents with in-house sterilization capacity but narrows the funnel for emerging brands.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Flux Type: MCO Membranes Capture HDF Demand

High-flux units accounted for 61.53% of 2025 volume in the dialyzer market, reflecting their seamless fit with existing machines and bundled-payment models that reward middle-molecule clearance. Medium cut-off membranes are projected to expand 10.74% a year through 2031, the fastest track inside the dialyzer market, because they deliver near-HDF toxin removal without the cost of online substitution infrastructure. Low-flux designs persist in cost-constrained centers that cannot maintain dialysate endotoxin below 0.03 EU/mL, while high cut-off products retain a niche for paraproteinemia management. Comparative trials show MCO therapy lowers C-reactive protein and improves itch scores, outcomes that influence payer formularies in Germany and Japan. Upgrades gather pace when reimbursement schemes add small per-session supplements that offset membrane premiums.

Clinical uptake is uneven: German outpatient chains migrated more than 35% of annual caseloads to MCO by late 2025 after an EUR 8 add-on took effect, yet U.S. centers await broader Medicare coverage. Japanese clinics are shifting directly from low-flux to online HDF, limiting MCO headroom in that country. Latin American groups trialed MCO dialyzers but postponed rollouts when currency swings hit import budgets. Suppliers seek to broaden acceptance by publishing head-to-head data against high-volume HDF while lobbying regulators to recognize middle-molecule benchmarks in quality audits. The marketing narrative stresses that MCO avoids albumin loss, a concern that once stalled early adoption of high-cut-off devices.

By Usage Type: Disposable Dialyzers Dominate Amid Infection-Control Rules

Disposable single-use units represented 68.92% of total shipments in 2025, and this slice of the dialyzer market is forecast to grow 9.45% annually through 2031 as hospital groups retire labor-intensive reuse programs. Updated guidelines in 17 U.S. states now recommend single-use products for hepatitis B or C positive patients, undercutting the reuse cost argument. In Europe, environmental taxes on peracetic acid disposal shaved margins on reprocessing services, pushing chains toward disposables even in value-driven tenders. North American integrated providers also prefer disposables for home dialysis because households lack validated cleaning equipment. Asia’s public insurers are making similar moves; India’s Ayushman Bharat added INR 350 per session to cover single-use dialyzer cost in 2025.

Reuse still holds ground where wage levels are low and consumable imports carry steep tariffs. Some U.S. large dialysis organizations combine reuse for stable patients and single-use for higher-risk cases, a hybrid that smooths operating budgets while meeting infection metrics. Reprocessing volumes slid 12% in North America during 2025 after two national hospital systems closed standalone disinfection centers. Sub-Saharan Africa continues to rely on reuse because per-patient dialyzer spending already strains limited renal budgets. Manufacturers see residual demand for robust housings and thicker membrane walls that withstand 20 sterilization cycles, yet R&D budgets overwhelmingly favor high-performance single-use designs.

By Membrane Material: Polysulfone Leads, PMMA Gains in Inflammatory Cohorts

Polysulfone retained a 47.22% foothold in 2025, cementing its place as the workhorse polymer inside the dialyzer market because it balances permeability and biocompatibility at scale. Local resin capacity added in China and India trimmed costs up to 20%, allowing regional brands to match multinationals on ISO 8637 performance at lower price points. Polyethersulfone occupies premium MCO and HDF niches where higher tensile strength prevents fiber collapse under convective loads. PAN and AN69 membranes stay confined to sepsis indications given their negative surface charge and cytokine adsorption properties. Cellulose triacetate hangs on in pediatric and hypersensitivity segments, particularly after PVP concerns resurfaced in 2024.

PMMA is the fastest riser, projected at 9.68% CAGR, because its hydrophobic surface adsorbs beta-2 microglobulin and interleukin-6—markers linked to cardiovascular risk—and appeals to nephrologists treating inflammatory complications. Asahi Kasei expanded PMMA output 15% in early 2025, betting that hospitals will pay a 25% premium for better cytokine clearance. Toray’s PMMA Filtryzer gained China’s NMPA nod at the end of 2024, opening a runway to an estimated 200,000 inflammatory-dialysis patients. Regulators now demand cytokine-adsorption validation under revised ISO 10993, a change that favors synthetic polymers over legacy cellulose. The competitive dynamic revolves around proprietary surface treatments—vitamin E bonding, zwitterionic grafts, or polyethylene-glycol layers—that differentiate brands on oxidative stress and clotting time.

By End User: Home Dialysis Expands on Remote-Monitoring Support

In-center facilities consumed 76.33% of 2025 units, yet home therapies are climbing at an 8.46% CAGR through 2031 as insurers reimburse patient training and telehealth check-ins. Compact cyclers with on-board water purification now fit apartments lacking dedicated plumbing, lowering practical barriers to adoption. North America leads with 18% of prevalent patients dialyzing at home, while Australia crossed the 20% mark after its Pharmaceutical Benefits Scheme extended consumable coverage in 2024. Europe trails because many urban flats lack space for storage, though Scandinavian countries buck the trend thanks to strong home-nursing networks. Asia-Pacific growth hinges on mobile connectivity; India’s Renalyx RxT 21 smart machine streams session data to cloud dashboards so physicians can intervene early.

Hospital-based dialysis remains essential for acute kidney injury in cardiac and transplant wards. Critical-care units favor dialyzers engineered for high blood-flow rates and low resistance to manage septic shock or post-surgical fluid overload. Manufacturers that bundle device sales with remote-monitoring software gain stickiness, as switching would require retraining both nurses and patients. Reimbursement frameworks increasingly tie home-therapy payments to monthly adherence scores captured by Bluetooth scales and automated BP cuffs. Providers still cite vascular-access complications and emergency response logistics as hurdles to scaling beyond early adopters.

By Application / Therapy: Hemodiafiltration Moves Mainstream

Conventional hemodialysis delivered 81.43% of 2025 procedures, but hemodiafiltration is forecast to gain 10.62% annually on mounting survival evidence, particularly in Europe where online HDF penetration already tops 40%. Dialysis chains swap in high-flux or MCO dialyzers compatible with convective volumes exceeding 23 L per session when reverse-osmosis plants can guarantee ultrapure water. High-volume HDF reduces cardiovascular events 19% compared with high-flux HD, according to a 2025 JAMA meta-analysis, and payers are starting to factor those savings into bundled rates. Hemofiltration remains a specialty protocol for intensive-care settings where cytokine storm management trumps urea clearance, limiting its share but sustaining premium pricing for low-resistance dialyzers.

Barriers revolve around infrastructure: many centers in emerging economies cannot maintain endotoxin below 0.03 EU/mL, so they stick with standard HD despite clinical guidance. Japan achieved parity reimbursement between HDF and HD in 2024, accelerating a 22% jump in HDF sessions by 2025. Australia and Canada followed with modest add-on payments to offset capital retrofits. Suppliers court medical directors with helical fiber-bundle geometries that raise convection without boosting transmembrane pressure. Marketing emphasizes shorter recovery times and better phosphate control, two patient-reported outcomes linked to adherence.

By Patient Group: Geriatric Growth Outpaces Adult Cohort

Adults aged 18-64 absorbed 76.24% of 2025 volumes, but geriatric demand is climbing at 8.52% a year as rising life expectancy and metabolic disease increase late-stage renal failure among seniors. Older patients often present frailty and cardiovascular comorbidities that necessitate dialyzers with softer ultrafiltration profiles to avoid intradialytic hypotension. Vitamin E-bonded membranes that curb oxidative stress resonate with this cohort, helping Asahi Kasei log 20% domestic growth for its Rexeed Evolution line in 2025. Incremental dialysis—two sessions per week at initiation—gained traction after a 2025 NIH study showed preserved quality of life without higher mortality. That protocol creates steady demand for small-surface-area dialyzers purpose-built for lower flow rates.

Pediatrics remains a thin but strategic segment. Small-diameter fiber bundles prevent hemodynamic swings in children under 20 kg, and the dialyzer market rewards suppliers with premium pricing for such specialized SKUs. Reimbursement gaps persist because many health systems lack discrete payment codes for pediatric disposables, leaving hospitals to absorb price differentials. Manufacturers keep pediatric programs alive to cement relationships with academic centers that influence adult product bids. In emerging Asia, pediatric ESRD care is limited by late referral and travel distance; home peritoneal dialysis often substitutes, but governments aim to lift pediatric HD penetration through subsidy schemes.

Geography Analysis

North America retained 36.82% of global revenue in 2025 because the United States funds more than 500,000 beneficiaries through Medicare’s bundled end-stage renal disease program, which pays for both dialyzer and ancillary supplies. Dialyzer market growth in the region is slowing as incidence levels off among non-Hispanic Whites, yet the prevalence of diabetes and hypertension above 15% in Hispanic and African American populations keeps absolute treatment numbers rising. Canada is testing value-based procurement pilots that link dialyzer reimbursements to hospitalization days saved, a step that encourages clinics to migrate to high-flux and MCO membranes that demonstrate better cardiovascular outcomes. Mexico extended federal coverage to another 12,000 patients in 2025, but the dialyzer market size remains constrained in the south where out-of-pocket costs deter therapy uptake. Private U.S. integrated delivery networks are channeling patients into home programs, which lifts volume for disposable products compatible with at-home machines. Across North America, the dialyzer market still benefits from strong aftermarket sales of vitamin E-bonded variants aimed at older cohorts, yet formulary committees are pressing suppliers for price freezes that offset biosimilar anemia-drug savings.

In Europe, led by Germany, France, and the United Kingdom, where comprehensive public insurance and online-HDF penetration above 40% make convective therapies mainstream. Germany’s Federal Joint Committee granted an EUR 8 per-session premium for MCO membranes in 2025, widening the dialyzer market share gap between premium and basic products. The EU Medical Device Regulation that took effect in mid-2025 lengthened launch timelines by up to nine months and raised compliance cost about 10%, squeezing small entrants. Eastern European governments use structural funds to add stations, yet reimbursements can be 50% lower than Western averages, keeping the dialyzer market price sensitive in Poland, Romania, and Bulgaria. Southern Europe is adopting hospital carbon-budget targets that penalize plastic waste, nudging centers toward lighter housings and potential limited reuse. Nordic countries keep stable demand with aging populations, but clinics there renew contracts largely on environmental metrics that now weigh 20% in tender scoring.

Asia-Pacific is projected to grow at an 8.93% CAGR through 2031, the fastest regional pace in the dialyzer market, as China, India, and Indonesia scale treatment capacity under expanded insurance umbrellas. China’s maintenance-dialysis population rose to more than 900,000 in 2025 after rural schemes began covering 80% of facility costs in tier-3 cities, moving the dialyzer market size toward parity with North America. India’s Pradhan Mantri National Dialysis Programme added 1,200 centers between 2024 and 2025, yet fewer than 15% of new ESRD patients reach therapy within six months, leaving headroom for future dialyzer market expansion. Japan is replacing low-flux products with HDF-ready membranes at a rapid clip after reimbursement parity arrived in 2024, while South Korea’s 8% fee uplift on high-flux units in 2025 offset higher polysulfone costs. Australia raised home-dialysis subsidies in 2024, lifting household adoption above 18% of national caseload and favoring compact disposables. Southeast Asia remains under-penetrated; Indonesia’s memorandum with Nipro to build 50 satellite centers should raise installed stations more than 30% by 2028. Across the region, local polysulfone capacity cuts resin cost up to 20%, intensifying competition as regional firms chase dialyzer market share from multinationals.

Competitive Landscape

The dialyzer market exhibits moderate concentration, yet regional Chinese and Indian specialists are eroding that hold by pricing 20-30% lower on comparable ISO-certified products. Fresenius leverages ownership of more than 4,000 clinics to pilot next-generation membranes in house before broader launch, speeding feedback loops and protecting dialyzer market share with proprietary helical fiber bundles that raise convective flux. Baxter differentiates with its Theranova MCO range, which commands 15-20% premiums in Germany and the Netherlands after winning an evidence-based add-on in 2025; that lift contributed to mid-single-digit dialyzer revenue growth despite flat total HD sessions. Asahi Kasei expanded PMMA capacity by 15% in early 2025 to serve inflammatory-patient niches, and the new line filled within six months thanks to vitamin E and cytokine-adsorption performance advantages.

Low-cost challengers such as Weigao Group, Browndove Healthcare, and Guangdong ZhongAi Medical vertically integrated polysulfone resin and extrusion in 2024-2025, shaving raw-material cost 18% and accelerating quotation cycles for public tenders. Shanghai Peony Medical and OCI Medical secured ISO 13485 certification and are now seeking FDA 510(k) clearance to enter the U.S. dialyzer market by 2027 with products priced 25-35% below incumbent brands. Established multinationals respond with dual-sourcing agreements that lock up clinical key accounts for five-year periods, bundling dialyzers with machines, concentrates, and service contracts. Strategic M&A remains likely; multiple private equity funds signal interest in mid-tier Asian membrane producers that hold domestic tenders but lack global distribution.

Innovation centers on surface engineering to enable heparin-free dialysis, asymmetric fiber geometry to push convective volumes, and lighter housings that cut plastic by 15%. Toray filed patents for polyethylene-glycol grafting that extends clotting time without systemic anticoagulation, and Fresenius disclosed 14 dialyzer-related patents in 2025 covering helical fiber and dual-layer asymmetric pores. Many suppliers partner with 3M or other materials companies to test bio-based polycarbonate caps that comply with EU plastic-tax rules. Sustainability credentials increasingly influence tenders; Baxter published a life-cycle assessment in 2025 showing a 22% carbon reduction per treatment after switching to recyclable packaging, helping secure NHS contracts in the United Kingdom. Competitive positioning therefore hinges as much on ESG metrics and telehealth integration as on pure membrane performance, keeping rivalry intense yet disciplined.

Dialyzer Industry Leaders

Asahi Kasei Corporation

B. Braun Melsungen AG

Fresenius Medical Care AG

Baxter International

Nipro Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Simergent gained FDA 510(k) clearance for the Archimedes automated peritoneal-dialysis system intended for home and clinical settings.

- June 2025: Renalyx Health Systems launched the RENALYX RxT 21, India’s first fully indigenous, AI-enabled smart hemodialysis machine, priced at INR 6.70 lakh.

- June 2025: Fresenius Medical Care obtained FDA clearance for its 5008X CAREsystem capable of high-volume hemodiafiltration, paving the way for a full U.S. launch in 2026.

Global Dialyzer Market Report Scope

A dialyzer, or "artificial kidney," is a medical device used in hemodialysis to filter waste, toxins, and excess water from the blood when the kidneys fail.

The Dialyzer Market Report is segmented by Flux Type, Usage Type, Membrane Material, End User, Application/Therapy, Patient Group, and Geography. By Flux Type, the market is segmented into High‑Flux, MCO, Low‑Flux, and HCO dialyzers. By Usage Type, the market is segmented into Disposable and Reusable dialyzers. By Membrane Material, the market is segmented into Polysulfone, Polyethersulfone, PAN/AN69, PMMA, and Cellulose Triacetate. By End User, the market is segmented into Hospitals, In‑Center Dialysis Facilities, and Home settings. By Application/Therapy, the market is segmented into Hemodialysis, Hemodiafiltration, and Hemofiltration. By Patient Group, the market is segmented into Adult, Geriatric, and Pediatric patients. By Geography, the market is segmented into North America, Europe, Asia‑Pacific, MEA, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD) for the above segments.

| High-Flux |

| Medium Cut-Off (MCO) |

| Low-Flux |

| High-Cut-Off (HCO) |

| Disposable / Single-use |

| Reusable |

| Synthetic – Polysulfone |

| Synthetic – Polyethersulfone |

| Synthetic – PAN / AN69 |

| Synthetic – PMMA |

| Cellulose Triacetate |

| Hospitals |

| In-Center Dialysis |

| Home Dialysis |

| Hemodialysis |

| Hemodiafiltration |

| Hemofiltration |

| Adult |

| Geriatric |

| Pediatric |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Flux Type | High-Flux | |

| Medium Cut-Off (MCO) | ||

| Low-Flux | ||

| High-Cut-Off (HCO) | ||

| By Usage Type | Disposable / Single-use | |

| Reusable | ||

| By Membrane Material | Synthetic – Polysulfone | |

| Synthetic – Polyethersulfone | ||

| Synthetic – PAN / AN69 | ||

| Synthetic – PMMA | ||

| Cellulose Triacetate | ||

| By End User | Hospitals | |

| In-Center Dialysis | ||

| Home Dialysis | ||

| By Application / Therapy | Hemodialysis | |

| Hemodiafiltration | ||

| Hemofiltration | ||

| By Patient Group | Adult | |

| Geriatric | ||

| Pediatric | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What CAGR is forecast for the dialyzer market from 2026 to 2031?

The dialyzer market is projected to grow at a 6.62% CAGR between 2026 and 2031 based on ���ϲ����� data.

Which flux type is expected to expand fastest through 2031?

Medium cut-off dialyzers are forecast to advance 10.74% annually, outpacing all other flux categories.

How large is disposable dialyzer demand versus reusable units?

Disposable single-use products held 68.92% volume share in 2025 and are still growing thanks to infection-control mandates.

Why is Asia-Pacific the fastest-growing region for dialyzers?

National insurance expansions in China, India, and Indonesia fund new dialysis centers and make therapy affordable for rural populations.

What regulatory issue currently affects tender decisions in Europe?

Concerns over PVP leachate have led several procurement agencies to set tighter residual limits, favoring suppliers with alternative coatings.

Page last updated on: