Date Syrup Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 444.61 Million |

| Market Size (2031) | USD 581.64 Million |

| Growth Rate (2026 - 2031) | 5.52% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Middle East and Africa |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. |

|

Date Syrup Market Analysis by ���ϲ�����

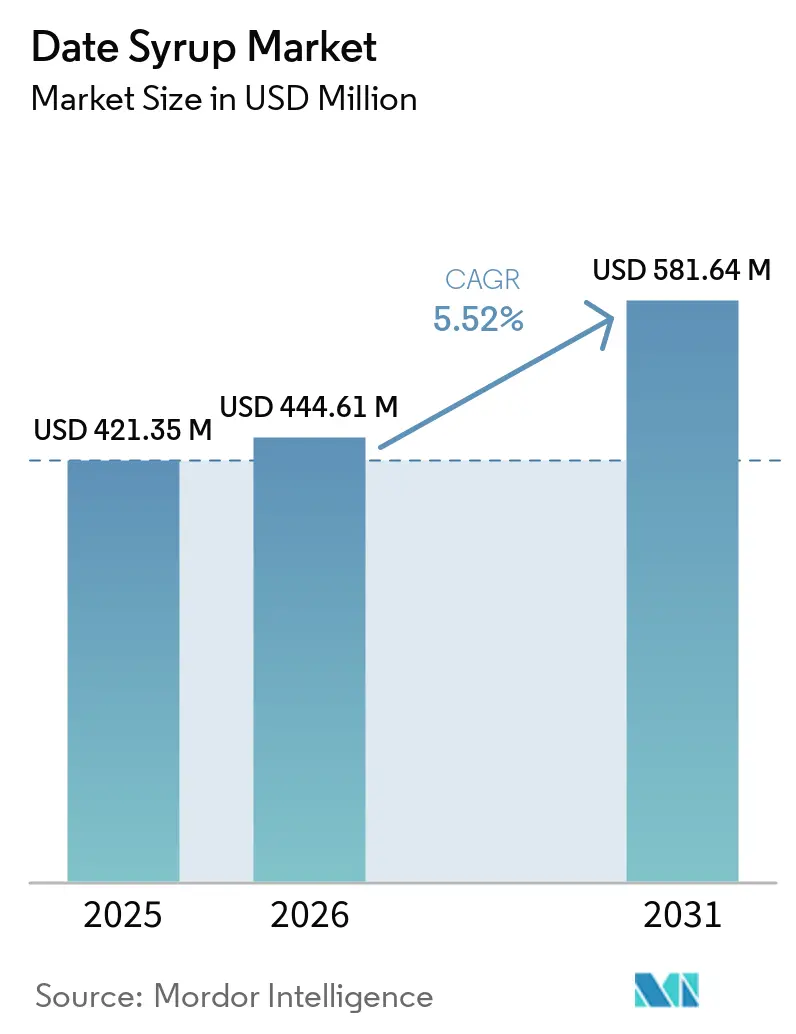

The date syrup market was valued at USD 421.35 million in 2025, stands at USD 444.61 million in 2026, and is projected to reach USD 581.64 million by 2031, growing at a CAGR of 5.52% from 2026 to 2031. The date syrup market is benefiting from a broad shift in sweetener demand, as consumers and food formulators move toward ingredients that look less processed and fit clean ingredient statements more easily. That shift is supported by a strong supply base of Arab countries, which keeps the Middle East and North Africa central to the availability of raw materials for the date syrup market. The date syrup market also benefits from a stronger functional profile than many competing syrups, as date syrup has a high monosaccharide content and antioxidant-linked phenolic compounds that support premium positioning in retail and foodservice. Export momentum is widening the commercial base, with Saudi Arabia reporting SAR 1.9 billion in date exports in 2025 across 125 countries and a 39% rise in shipments to China, which points to deeper international demand pipelines for processed date products, including syrup[1]Source: Saudi Press Agency, "Saudi Date Exports Hit Record SAR1.9 Billion in 2025, Up 14.3%," spa.gov.sa.

Key Report Takeaways

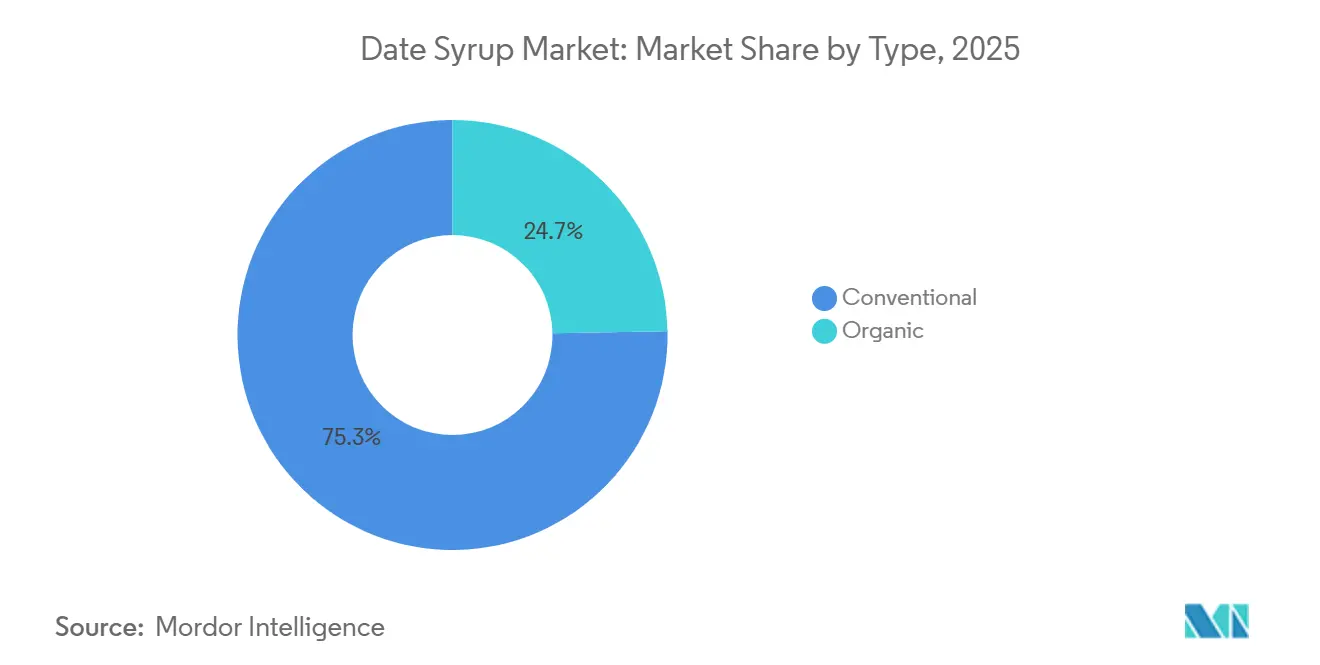

- By type, conventional syrups accounted for 75.27% of the market in 2025, whereas organic syrups are projected to grow at a 6.68% CAGR through 2031.

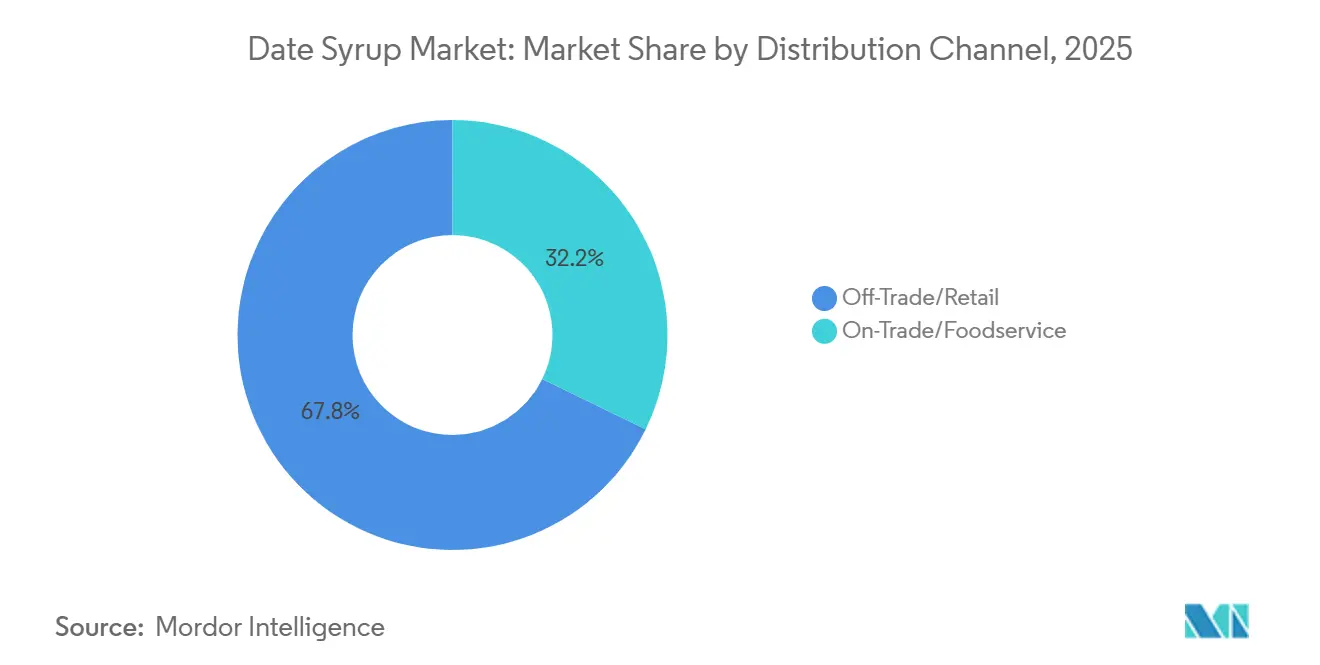

- By distribution channel, off-trade/retail held 67.77% of the market in 2025, while on-trade/foodservice is projected to grow at a 7.02% CAGR through 2031.

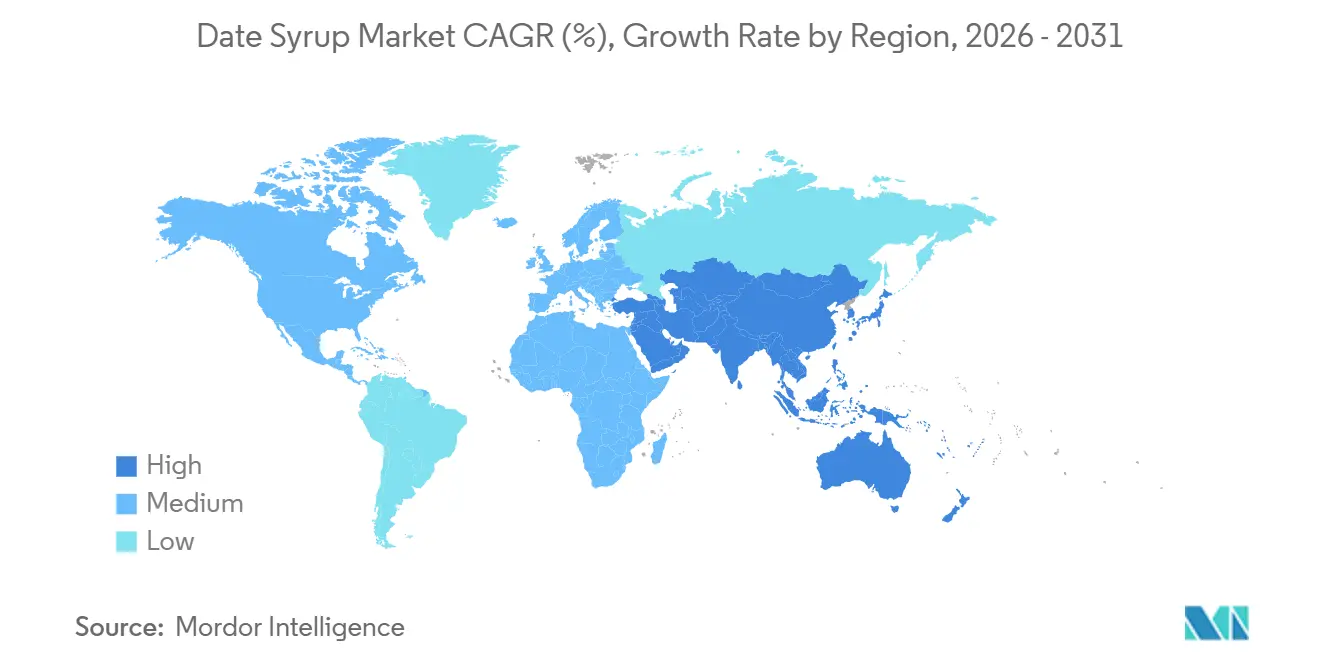

- By geography, Middle East and Africa accounted for 40.01% of the market in 2025, while Asia-Pacific is projected to grow at a CAGR at 6.52% through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Date Syrup Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for clean-label sugar replacements | +1.3% | Global, with concentrated traction in North America, Europe, and Asia-Pacific urban centers | Medium term (2-4 years) |

| Increased adoption of plant-based and vegan sweeteners | +1.0% | Global, particularly North America, Western Europe, and emerging Asia-Pacific markets | Medium term (2-4 years) |

| Foodservice uptake of Middle Eastern-inspired menus | +0.8% | Asia-Pacific, North America, and Europe | Short term (≤ 2 years) |

| Technological advancements in extraction and preservation improving shelf life and quality | +0.6% | Middle East and Africa supply base, with secondary benefits globally | Long term (≥ 4 years) |

| Functional performance in bakery, dairy, and snack reformulation | +0.8% | Global, with premium positioning in North America and Europe | Medium term (2-4 years) |

| Rising e-commerce and retail accessibility of niche products | +0.5% | North America, Europe, and Asia-Pacific, with early gains in Middle East and Africa and South America | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Growing demand for clean-label sugar replacements

The date syrup market is experiencing growth driven by a broader consumer shift away from high-fructose corn syrup and artificial sweeteners toward more natural and recognizable ingredients. This trend is significant because date syrup offers a minimally processed image, helping avoid the consumer hesitation often associated with unfamiliar sweetener names. In June 2024, the World Health Organization reinforced this reformulation trend by recommending fiscal measures on sugar-sweetened beverages within healthy diet policy frameworks, increasing pressure on food and beverage companies to reconsider their sweetener choices[2]Source: World Health Organization, “Fiscal Policies to Promote Healthy Diets: WHO Guideline,” World Health Organization, who.int. Date syrup aligns well with the demand for simple ingredient narratives, making it a versatile option across packaged foods, beverages, and foodservice menus. Additionally, the market benefits from clean-label positioning, which has transitioned from being a niche retail focus to a mainstream grocery priority, as ingredient clarity now serves as a practical selling point for a broader consumer base.

Increased adoption of plant-based and vegan sweeteners

The date syrup market is also being supported by growing attention to diet quality, metabolic health, and ingredient functionality at both household and industrial levels. Date syrup offers a stronger narrative for metabolic health than standard caloric sweeteners. Its low glycemic index and natural sugar composition make it an attractive alternative for consumers seeking healthier sweetening options. The functional benefits extend beyond glucose management, as research highlights the diverse phytochemical profile of Phoenix dactylifera, including carotenoids, zeaxanthin, minerals, and other bioactive compounds. These attributes are increasingly appealing to premium product developers aiming to cater to health-conscious consumers. Additionally, the rising demand for clean-label and natural products is driving innovation in the date syrup market. Buyers in health-oriented channels are requesting greater transparency into cultivar, processing stage, and origin, pushing the market toward more premium, traceable product tiers.

Foodservice uptake of Middle Eastern-inspired menus

Foodservice adoption of date syrup is expanding beyond specialty health cafés into mainstream hospitality and quick-service restaurant (QSR) channels. In India's HoReCa sector, cafés in Mumbai, Bengaluru, and Delhi have incorporated date syrup into cold brews, lattes, and detox beverages as part of "no added sugar" menu positioning, driven by increasing middle-class wellness spending. This trend reflects the growing use of date syrup in beverages, bakery items, desserts, and plant-based menu formats, where operators seek a natural sweetener that aligns with clean-label ingredient positioning. The date syrup market benefits further as commercial kitchens utilize it across multiple menu categories, increasing ingredient demand per outlet more effectively than single-bottle retail sales. Al Barakah Dates Factory, which processes over 100,000 tonnes annually, has identified the United States as its primary export market for date paste and date syrup. This serves as a strong supply-side indicator of significant B2B demand across food manufacturing and foodservice channels. The channel holds particular relevance in markets where dates already enjoy cultural familiarity, enabling smoother menu adoption with minimal consumer education and reduced risk for operators.

Rising e-commerce and retail accessibility of niche products

Online retail is significantly amplifying the reach of niche natural sweetener brands by removing geographic shelf-space constraints that previously limited date syrup to specialty health stores. Agthia Group (Al Foah) reported a 55% increase in e-commerce revenue in 2024, with the channel now accounting for 5.4% of total group revenues. This highlights how established Middle East and Africa producers are actively shifting toward digital-first distribution in international markets. The date syrup market is particularly benefiting from e-commerce as it enables brands to bypass traditional retail limitations, allowing smaller players to build awareness through search behavior, ingredient storytelling, and repeat purchase programs before securing mass retail listings. The growing visibility of health-ingredient keywords in e-commerce search results is creating a demand pull, reducing customer acquisition costs for emerging brands. This trend is accelerating category fragmentation at the value end of the market while simultaneously reinforcing premium positioning at the higher end.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from alternate natural sweeteners | -0.6% | Global, most intense in North America and Western Europe | Medium term (2-4 years) |

| Challenges posed by climate change and water scarcity in date-growing regions | -0.5% | Middle East and Africa supply base, with global downstream impact | Medium term (2-4 years) |

| Stringent regulatory requirements concerning labeling, certifications, and traceability | -0.4% | North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Supplier standardization and viscosity variability concerns | -0.3% | Global, most acute in emerging supply origins such as Pakistan, Sudan, and Iraq | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Competition from alternate natural sweeteners

Date syrup competes in a crowded natural sweetener field, where honey, maple syrup, agave, and rice malt syrup each hold strong consumer loyalty and well-established supply chains. Honey, in particular, dominates as a globally recognized category with centuries of consumption heritage, making it challenging for date syrup to achieve trial conversions in markets where it lacks cultural familiarity. This challenge is especially pronounced in North America and Western Europe, where premium shelf space is often dominated by sweeteners with longer mainstream retail histories and significant promotional investments. To gain a competitive edge, the date syrup market must focus on differentiation through its unique composition, origin, and functional benefits. For instance, date syrup's high antioxidant content and natural mineral profile can be emphasized to appeal to health-conscious consumers. Strategic marketing efforts, such as storytelling around its Middle Eastern heritage and sustainable production processes, can further enhance its appeal.

Supplier standardization and viscosity variability concerns

The fragmentation of date palm cultivation across smallholder farms in Egypt, Iraq, Pakistan, and Sudan, where post-harvest processing levels remain low compared to Gulf state competitors, creates significant variability in feedstock quality, complicating large-scale date syrup standardization. According to Egypt's Cabinet Information and Decision Support Center (IDSC), inheritance-driven land fragmentation and inadequate cold storage are structural constraints that limit value-added processing at the origin[3]Source: Egypt Cabinet Information and Decision Support Center, “Egypt Ranked World's Top Date Producer With 1.87 Million Tonnes Production,” Aldawla News, aldawlanews.com. The metabolomic profiles of commercial date syrups vary substantially depending on cultivar and processing methods. Additionally, the date syrup market faces challenges from volatility in raw materials, driven by climate-sensitive date palm cultivation, which can amplify pricing fluctuations and complicate long-term supply planning. Simultaneously, import markets are imposing stricter food safety, labeling, and traceability requirements, increasing costs for suppliers that do not already meet export-grade standards.

Segment Analysis

By Type: Organic Segment Gaining Ground on Conventional Base

Conventional date syrup held 75.27% of the date syrup market share in 2025, which shows how firmly the category still rests on price-sensitive commercial demand. The date syrup market continues to lean toward conventional volumes because large food manufacturers, bakeries, and institutional buyers prioritize broad availability and predictable cost structures. Conventional supply also benefits from wider raw material access across key producing countries and fewer certification costs, which helps keep procurement simple for mainstream users. These conditions make the conventional tier the operational backbone of the date syrup market even as premium retail narratives get more attention. The segment’s scale is therefore tied less to brand storytelling and more to dependable industrial movement across business-to-business (B2B) channels.

Organic date syrup represents the faster-growing segment within the date syrup market, with a projected CAGR of 6.68% through 2031. This growth is driven by an expanding consumer base willing to pay a premium for certified organic products, particularly in specialty retail, natural grocery, and direct-to-consumer channels. Bateel International’s vertically integrated model exemplifies this premium trajectory, as its certified Al Ghat farm in Saudi Arabia produces over 5,000 tonnes annually, supporting both upscale retail and hospitality markets. Notably, the growth in the organic segment is expanding the overall customer base of the date syrup market rather than significantly cannibalizing the conventional segment. It is successfully attracting consumers who might otherwise opt for honey, maple syrup, or other premium natural sweeteners.

By Distribution Channel: Retail Holds the Base, Foodservice Accelerates

Off-trade/retail accounted for 67.77% of the market in 2025. Supermarkets and hypermarkets dominate this channel, offering conventional products alongside an expanding range of premium organic options. Within retail, the date syrup market has gained momentum online, as digital platforms enable smaller brands to build consumer trial without relying on extensive physical distribution. This trend has allowed several brands to transition from niche awareness to broader availability in large-format grocery stores. Consequently, the retail channel remains the primary volume driver, even as its composition shifts toward premium and digital offerings. Online discovery often facilitates in-store expansion, creating a synergistic growth pathway. Smaller specialty stores and convenience formats, which are less saturated, present further opportunities for shelf space as consumer awareness continues to grow.

On-trade or foodservice is projected to grow at a 7.02% CAGR through 2031, making it the fastest-expanding distribution channel in the date syrup market size outlook. Its momentum comes from ingredient adoption across café beverages, desserts, bakery items, and premium restaurant menus, where natural sweetening plays well with clean-label positioning. The date syrup market is especially well placed in foodservice because chefs and operators can introduce the ingredient without asking consumers to commit to a full retail purchase first. Once the ingredient becomes familiar on menus, retail pull often follows, which supports a useful two-step demand pattern. That dynamic gives foodservice an influence on the broader category that goes beyond its direct value share. The channel also tends to support premium pricing more comfortably than mass grocery because menu value is tied to the overall eating experience rather than only to pack price.

Geography Analysis

Middle East and Africa held 40.01% of the date syrup market share in 2025, which kept the region firmly in the lead. The region’s position reflects deep cultural familiarity with date syrup, close proximity to major cultivation zones, and a more mature supply chain for date-based products. The export breadth matters for the date syrup market because it shows that processors in the region are building commercial reach well beyond traditional consumption markets. The regional base is also strengthened by certification capability, including BRCGS, Halal, Kosher, and organic standards, which global buyers increasingly expect for large-scale procurement. Egypt adds another layer of supply depth within the region. Date exports from Egypt reached USD 105.6 million in 2024, up 19.3% year over year, supported by investment in processing and refrigerated storage infrastructure.

Asia-Pacific is the fastest-growing region, with the date syrup market size projected to rise at a 6.52% CAGR through 2031. Growth is being driven by higher disposable incomes, wider access to health-oriented retail, and existing familiarity with dates across parts of South and Southeast Asia. India stands out as the most immediate volume opportunity because it is the world’s largest date importer, with trade value of USD 266.7 million based on the user-supplied FAO reference. Bateel’s Singapore entry in 2025, completed with Bluebell Group, also shows how premium date-based products are being positioned in affluent urban retail environments before wider regional rollout. China also presents a promising market, with increasing Saudi shipments indicating growing consumer exposure and stronger state-backed export channels that could support processed date products over time.

North America and Europe remain attractive because they offer stronger monetization per unit even with smaller volume shares than Middle East and Africa. In North America, premium organic brands and direct-to-consumer players have shown that the date syrup market can scale through a mix of digital awareness and national retail expansion. In Europe, Germany, the Netherlands, and the United Kingdom remain key entry points, and European date imports reached EUR 383.4 million in 2025 with Tunisia, Iran, and Israel among the main suppliers. South America is still at an early stage, with Brazil and Argentina showing limited but visible natural sweetener substitution, so the date syrup market is likely to remain smaller there through the forecast period.

Competitive Landscape

The date syrup market remains moderately fragmented, with no single producer exerting significant influence over pricing across the category. This structure reflects the coexistence of large Gulf processors, organic and specialty brands in the United States and Europe, and a wide field of regional suppliers across the Middle East and South Asia. At the upper end of the volume spectrum, companies such as Agthia Group and Al Barakah Dates Factory compete on processing scale, export readiness, and comprehensive certification capabilities. At the premium end, brands including Just Date, Date Lady, D’vash Organics, and Joolies focus on organic positioning, consumer trust, and retail agility. The date syrup market, therefore, operates within two distinct competitive layers: one driven by scale and compliance, and the other by brand equity and differentiated product narratives.

This dual structure explains the slow pace of consolidation within the market. Large processors in the date syrup market excel in B2B supply, where buyers prioritize traceability, consistency, and certification over consumer-facing brand recognition. Premium specialists, on the other hand, thrive in markets where shoppers are willing to pay for origin control, cleaner formulations, or organic status. The practical divide between these models creates opportunities for partnerships and selective investments rather than immediate large-scale consolidation. For instance, Just Date’s February 2026 partnership with Contour Ridge highlights how capital is being directed toward brands that can bridge premium positioning with broader channel expansion. Similarly, Bateel has leveraged boutique expansion and vertically integrated farming to strengthen its luxury market presence, distinct from industrial volume strategies.

Technology and operational credentials are becoming increasingly critical across the date syrup market as buyer expectations evolve. Al Barakah’s solar-powered processing model exemplifies this trend, as sustainability credentials are gaining importance, particularly among European buyers. Additionally, there is growing potential for specialized product formats, such as cultivar-specific syrups and transparent functional positioning tied to minerals and phenolic content. Smaller exporters with robust agricultural systems, including Israeli and Lebanese suppliers, may challenge larger incumbents in specialty retail by combining certified supply with targeted distribution strategies.

Date Syrup Industry Leaders

-

Agthia Group PJSC (Al Foah)

-

Al Barakah Dates Factory LLC

-

Bateel International LLC

-

Just Date

-

Lion Dates Impex Pvt. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Just Date secured a strategic partnership with Contour Ridge, a San Antonio-based private equity, to scale its organic date syrup, organic date sugar, and date-sweetened chocolate chip product portfolio across retail, foodservice, and grocery channels, with new product pipeline acceleration as a stated capital deployment priority.

- February 2025: Bateel International opened its first Southeast Asian boutique in Singapore at Takashimaya, Orchard Road, in partnership with Bluebell Group, offering premium organic dates, date syrups, and gourmet spreads, part of the brand's strategy to triple revenue and expand to approximately 500 locations globally by 2029, with targeted market entries in Japan, Indonesia, and Malaysia.

- November 2024: Global Foods unveiled its latest innovation: Clear Date Syrup in November 2024. This groundbreaking product redefines natural sweeteners, presenting all the advantages of traditional date syrup in a clear and versatile format, poised to transform the landscape of food manufacturing.

Global Date Syrup Market Report Scope

Date syrup is a thick, dark brown sweet syrup made from dates that's commonly used in Middle Eastern and Arab cooking as well as a natural sweetener.

The breakfast food market is segmented by type, distribution channel, and geography. Based on type, the market is segmented into conventional and organic. By distribution channels, the market has been segmented into on-trade/foodservice and off-trade/retail. Based on off-trade/retail, the market has been segmented into hypermarkets/supermarkets, convenience stores/grocery stores, online retail stores, and other distribution channels. By geography, the market has been segmented into North America, Europe, Asia-Pacific, South America, and Middle East and Africa. For each segment, the market sizing and forecasts have been done based on value (USD).

| Conventional |

| Organic |

| On-Trade/Foodservice | |

| Off-Trade/Retail | Supermarkets/Hypermarkets |

| Convenience Stores/Grocery Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Conventional | |

| Organic | ||

| By Distribution Channel | On-Trade/Foodservice | |

| Off-Trade/Retail | Supermarkets/Hypermarkets | |

| Convenience Stores/Grocery Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

Which type is growing faster through the forecast period?

Organic is the fastest-growing type, with a projected 6.68% CAGR through 2031, supported by certification-led premium demand and stronger specialty retail pull.

How large is the date syrup space expected to become by 2031?

The date syrup market is expected to reach USD 581.64 million by 2031, rising from USD 444.61 million in 2026 at a 5.52% CAGR.

Which sales channel is expanding the fastest?

On-Trade/Foodservice is the fastest-growing channel at a 7.02% CAGR, helped by adoption in café beverages, desserts, and clean-label menu formats.

Which region is the largest, and which one is growing the fastest?

Middle East and Africa was the largest region with 40.01% share in 2025, while Asia-Pacific is projected to grow the fastest at a 6.52% CAGR through 2031.

Page last updated on: