Data As A Service Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

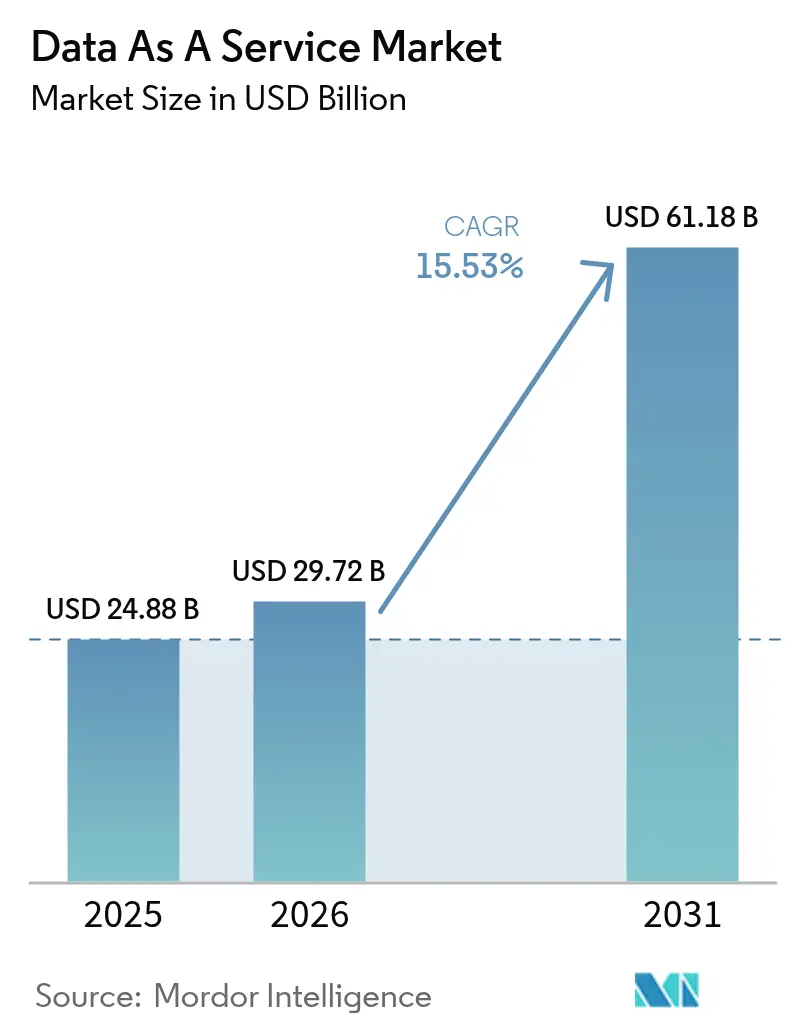

| Market Size (2026) | USD 29.72 Billion |

| Market Size (2031) | USD 61.18 Billion |

| Growth Rate (2026 - 2031) | 15.53% CAGR |

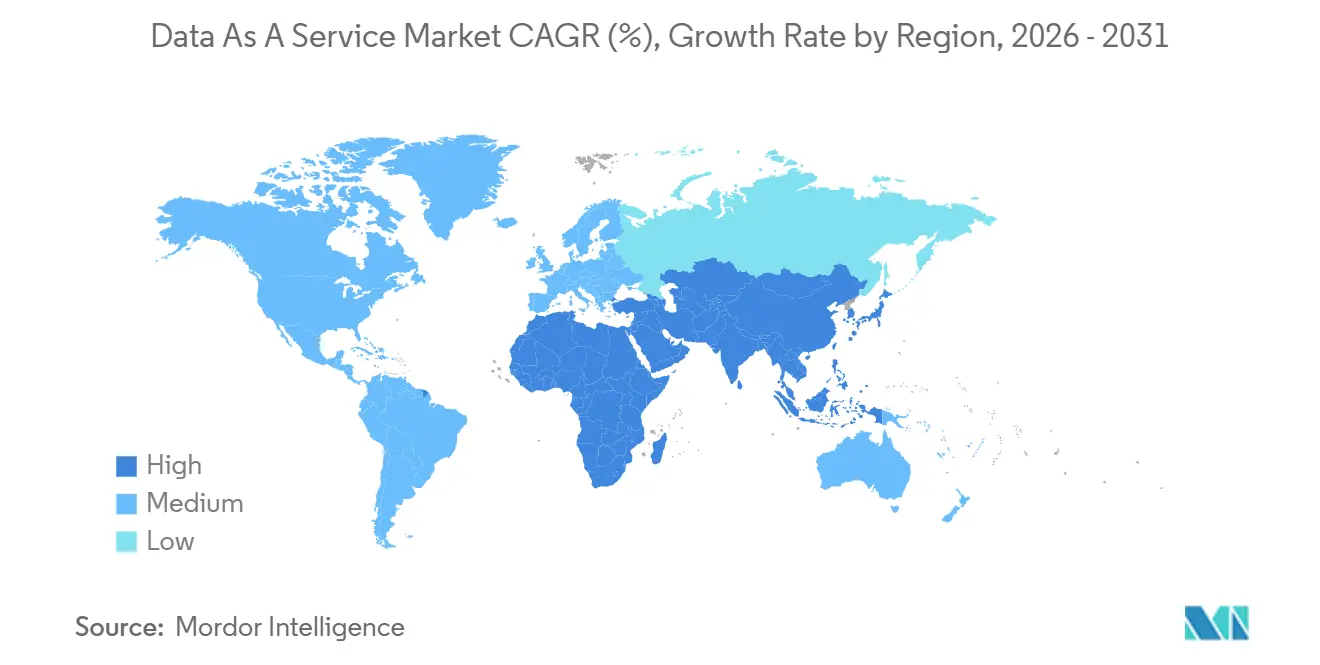

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

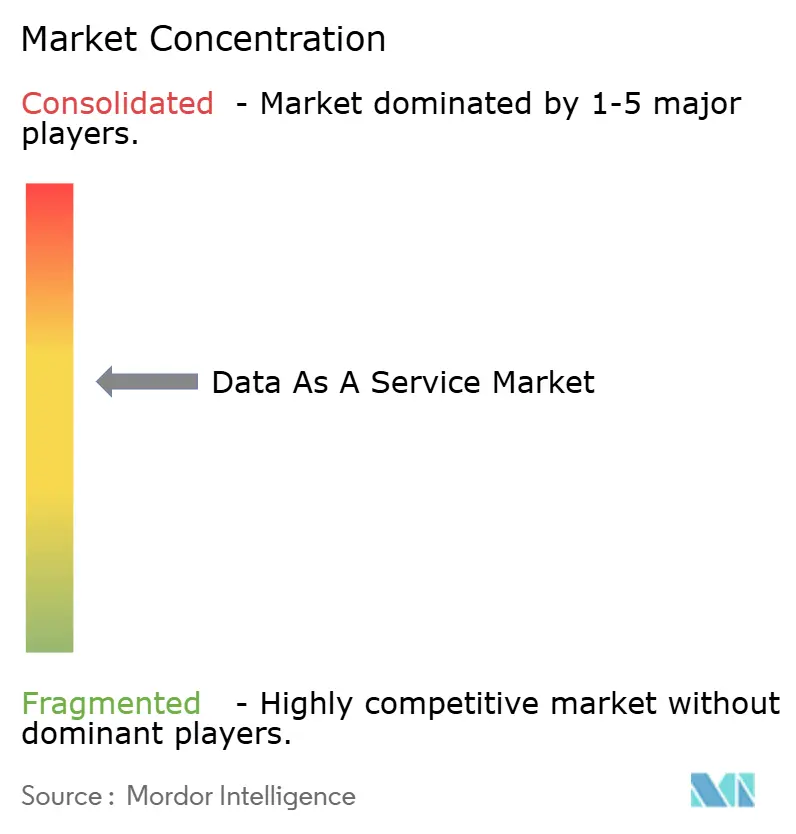

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Data As A Service Market Analysis by ���ϲ�����

The data as a service market size is projected to be USD 24.88 billion in 2025, USD 29.72 billion in 2026, and reach USD 61.18 billion by 2031, growing at a CAGR of 15.53% from 2026 to 2031. Enterprises are accelerating the shift from on-premise data warehouses to consumption-based platforms that separate storage, compute, and analytics. Public cloud elasticity shortens deployment timelines, while sovereign-cloud offerings ease data-localization barriers. AI-enabled retrieval-augmented generation (RAG) models spur demand for continuously refreshed external corpora. Competitive intensity is rising as hyperscalers integrate first-party data exchanges, forcing independent brokers to differentiate through coverage depth, refresh frequency, and privacy-enhancing computation.

Key Report Takeaways

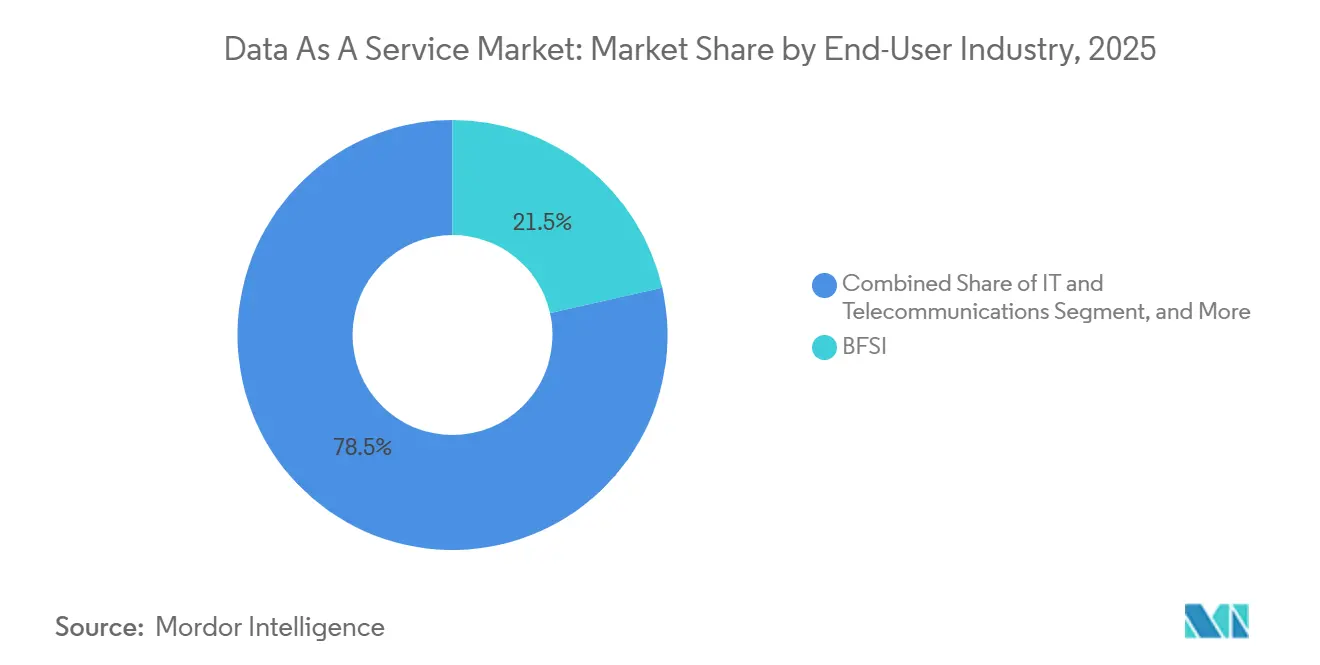

- By end-user industry, banking, financial services, and insurance held 21.47% of the data as a service market share in 2025, while healthcare and life sciences are forecast to expand at a 15.62% CAGR through 2031.

- By deployment model, public cloud captured 56.91% revenue share in 2025, whereas hybrid and multi-cloud configurations are advancing at a 15.69% CAGR to 2031.

- By data type, structured formats accounted for 48.73% of revenue in 2025, yet unstructured formats are projected to grow at a 15.71% CAGR during 2026-2031.

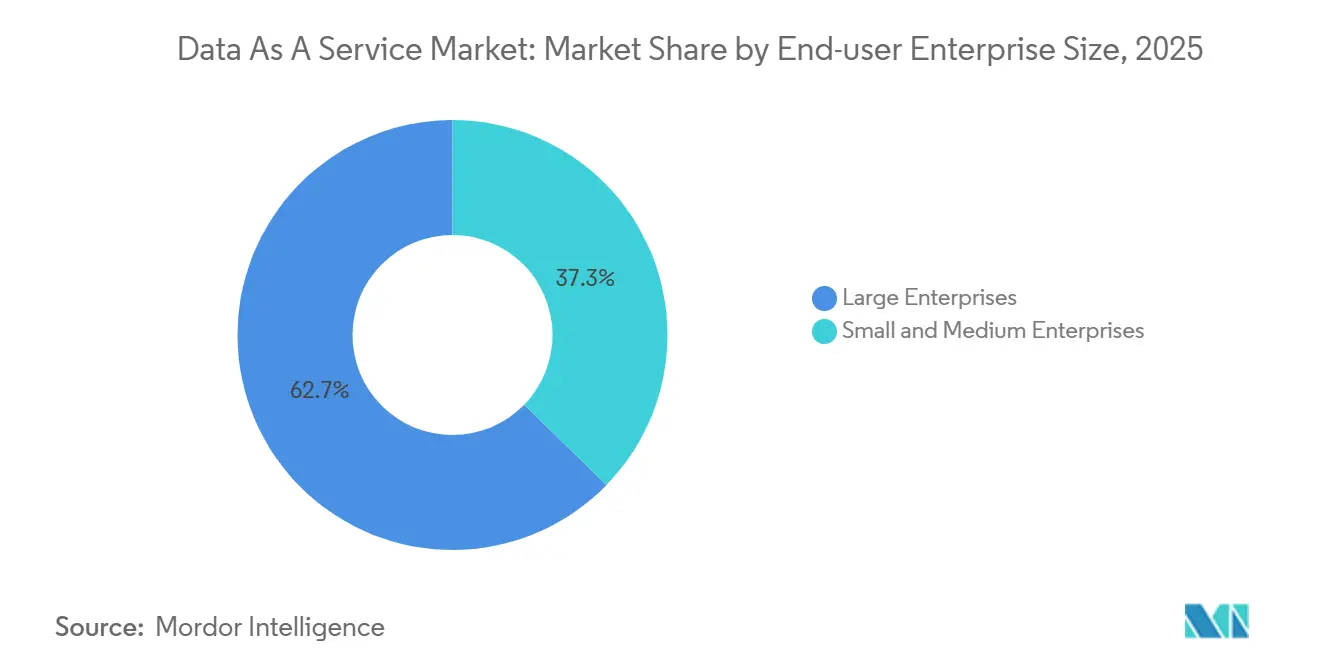

- By organization size, large enterprises commanded 62.71% spending in 2025, but small and medium enterprises are scaling at a 15.77% CAGR over the same period.

- By application, customer and marketing intelligence captured 29.63% share in 2025; real-time operational analytics is the fastest-growing use case at a 15.59% CAGR to 2031.

- By geography, North America generated 40.62% of global revenue in 2025, while Asia-Pacific is on track for a 15.84% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Data As A Service Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Enterprise Shift Toward Data-Driven Decision-Making | +4.2% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Explosion of Unstructured Data and Real-Time Analytics Demand | +3.8% | Global, APAC core with spill-over to Middle East and Africa | Long term (≥ 4 years) |

| AI RAG Frameworks' Appetite for Refreshable External Data | +3.1% | North America and Europe, emerging in APAC | Short term (≤ 2 years) |

| Falling Cloud Storage and Compute Costs | +2.4% | Global | Medium term (2-4 years) |

| Data-Localization Laws Fueling Regional Data Marketplaces | +1.3% | APAC core, Europe, select Middle East markets | Long term (≥ 4 years) |

| API-First "Nano-Datasets" Monetization Platforms | +0.9% | North America and Europe, early adoption in APAC | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Enterprise Shift Toward Data-Driven Decision-Making

Chief executive mandates now tether bonuses to data-informed key performance indicators, pushing demand for benchmarking feeds and alternative consumer-sentiment datasets. A 2025 survey of 1,200 executives showed 78% linking incentives to quantifiable metrics, up from 54% in 2023. Financial institutions embed satellite imagery and card-transaction aggregates into underwriting models, trimming default rates and slashing approval cycles.[1]JPMorgan Chase, “Investor Presentation 2025,” jpmorganchase.com Updated Regulation Fair Disclosure formats foster new revenue streams as filings become machine-readable.[2]U.S. Securities and Exchange Commission, “Regulation Fair Disclosure Amendments 2024,” sec.gov Early adopters gain competitive speed, compelling laggards to converge on data-centric cultures. The virtuous loop sustains double-digit spending regardless of cyclical IT headwinds.

Explosion of Unstructured Data and Real-Time Analytics Demand

Unstructured assets already represent more than 80% of enterprise data creation, yet legacy databases struggle to parse video, audio, and sensor telemetry. Object stores combined with serverless query engines now deliver SQL-like analytics on Parquet or JSON without extract-transform-load delays, cutting insight latency from days to minutes.[3]Amazon Web Services, “AWS re:Invent 2025 Data Analytics Keynote,” aws.amazon.com Manufacturers stream machine-vision frames to centralized lakehouses, reducing scrap by up to 14%. Retailers run dynamic shelf-price algorithms fueled by foot-traffic heatmaps and point-of-sale events, refreshing tags every 15 minutes. New regulations such as the EU Data Act mandate IoT interoperability, while China’s Personal Information Protection Law limits cross-border transfer of biometric data, forcing region-specific pipelines. Vendors that master multi-jurisdiction orchestration capture disproportionate share.

AI RAG Frameworks’ Appetite for Refreshable External Data

Retrieval-augmented generation overtakes static fine-tuning because it updates knowledge bases without retraining billion-parameter models. IBM recommends embedding regulatory filings and technical manuals into vector databases, lowering hallucinations by up to 60%. Pharmaceutical teams pipe real-world evidence into retrieval workflows, shaving 3-5 months from phase-two timelines. Legal firms ingest nightly case-law updates to draft merger documents aligned with fresh precedents. Consumption-based pricing shifts spend from bulk licensing to recurring API calls. Forthcoming ISO/IEC 42001 audits amplify demand for lineage-rich datasets.

Falling Cloud Storage and Compute Costs

Hyperscalers have cut object-storage rates by 31% since 2024 and now bill query engines in sub-second increments, trimming bursty workload invoices by up to 35%. ARM-based processors offer 40% better price-performance for transformation jobs, freeing budgets for broader dataset portfolios. Spot-instance markets discount compute by over 70%, though require interruption-tolerant orchestration. Deflation democratizes petabyte-scale analytics and allows startups to undercut incumbents on price and refresh cadence.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-Privacy and Cybersecurity Concerns | -2.1% | Global, acute in Europe and North America | Short term (≤ 2 years) |

| Data-Quality and Interoperability Gaps | -1.6% | Global | Medium term (2-4 years) |

| Rising Hyperscaler Egress Fees Compressing Margins | -0.8% | Global, concentrated in multi-cloud architectures | Short term (≤ 2 years) |

| ESG Scrutiny of Energy-Intensive Data Pipelines | -0.5% | Europe and North America, emerging in APAC | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Data-Privacy and Cybersecurity Concerns

Breaches such as the 2024 Change Healthcare ransomware incident, which exposed 100 million prescription records and cost USD 2.3 billion in remediation, fuel skepticism toward third-party brokers. European regulators issued 47 GDPR enforcement actions in 2025, averaging EUR 18 million (USD 19.7 million) per fine. India’s Digital Personal Data Protection Act adds seven-year audit-log mandates, inflating compliance overhead for offshore providers. Encryption-in-use remains computationally heavy, limiting adoption to niche workloads. Lengthening vendor-selection cycles curb near-term revenue growth.

Data-Quality and Interoperability Gaps

Buyers divert up to 40% of analytics budgets to cleanse inconsistent schemas and missing values. Proprietary encodings inside legacy ERP systems complicate mapping, delaying integrations. Lack of universal exchange standards entrenches incumbents despite slower refresh cadence. Metric redefinitions without versioning break downstream models, eroding trust. Blockchain provenance pilots remain stalled by scalability and governance uncertainties.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User Industry: BFSI Anchors Spending, Healthcare Gains Momentum

BFSI institutions contributed 21.47% of 2025 revenue, leveraging stringent stress-testing mandates that demand granular macroeconomic, transactional, and behavioral feeds. Asset managers subscribe to high-frequency market quotes, while insurers license telematics and socioeconomic indicators to price risk more precisely. The data as a service market size devoted to BFSI continues to expand as algorithmic trading and real-time underwriting accelerate dataset turnover. Healthcare and life sciences, though smaller today, are projected to grow 15.62% annually as pharmaceutical firms ingest real-world evidence and genomics repositories to meet regulatory surveillance needs. Public-sector adoption lags due to procurement cycles, yet smart-city pilots in Singapore and Dubai showcase federated exchanges that pool traffic, utility, and permitting data.

Pharma companies co-develop federated architectures that comply with privacy laws, reducing bulk transfers. Retailers and e-commerce players blend location intelligence with loyalty data to sharpen assortment planning. Manufacturing lines stream supply-chain visibility feeds that track port congestion and commodity futures, improving inventory resilience. Government agencies test open data hubs for labor, health, and environmental transparency. Telecommunications providers monetize anonymized network telemetry, offsetting voice revenue declines, while energy utilities ingest weather and load forecasts to optimize renewable dispatch. Education remains nascent, yet competency-based platforms begin ingesting labor-market signals, suggesting steady if slower growth.

By Deployment Model: Hybrid Strategies Balance Control and Scale

Public cloud held 56.91% revenue share in 2025, buoyed by turnkey analytics and elastic scaling. Financial firms keep sensitive customer records on-premise but route anonymized aggregates to the cloud, capturing cost and agility advantages. Hybrid and multi-cloud environments are forecast to grow 15.69% annually as firms seek residency compliance and avoid lock-in. The data as a service market size attached to hybrid workloads thus outpaces overall expansion.

Telecom operators deploy regional edge compute nodes for sub-second analytics, then mirror insights into central lakehouses. Private cloud persists in defense and critical infrastructure, yet container orchestration brings cloud-native tooling behind firewalls. Sovereign-cloud launches in Europe combine managed services with jurisdictional control, eroding traditional private installations. Multi-cloud fabrics cache popular datasets across hyperscalers to dodge egress fees, although cross-cloud bandwidth still costs up to USD 0.09 per gigabyte. Vendors that automate cost-aware routing gain favor among large enterprises.

By Data Type: Unstructured Assets Overtake Legacy Schemas

Structured data retained 48.73% share in 2025 through finance, CRM, and ERP workloads. However, unstructured formats—video, audio, free-text—are on a 15.71% CAGR trajectory. Computer-vision on shelf cameras boosts on-shelf availability by over 8 percentage points, while insurers exploit driver telematics to cut loss ratios. Semi-structured JSON and XML logs mirror broader market growth, feeding microservices and webhook streams.

Rising unstructured volumes inflate compute budgets for embedding generation and similarity search, pressuring providers to optimize inference. Regulations lag behind deep-learning explainability requirements, adding compliance ambiguity. Metadata standards such as Dublin Core extensions layer provenance, relevance, and usage rights, automating discovery and governance. Vendors that compress video intelligently or batch embeddings by similarity achieve margin advantages and reduce customer spend.

By Organization Size: SME Adoption Accelerates

Large enterprises represented 62.71% of 2025 spending, leveraging dedicated data-engineering teams and multi-year contracts. Yet SMEs are scaling usage at a 15.77% CAGR as API-first vendors eliminate heavy integration. The data as a service market share gap narrows as cloud marketplaces bundle dataset subscriptions with compute credits.

Vertical SaaS embeds benchmarking feeds directly into accounting, CRM, and HR modules, letting a 200-employee manufacturer access the same labor cost dashboards as a Fortune 500 peer. Low-code analytics platforms generate SQL from natural-language prompts, lowering the talent barrier. Managed governance services automate consent logs and breach notifications, offsetting compliance overhead. Cost-elastic serverless SQL allows SMEs to burst during campaign peaks and idle off-peak, aligning spend with value.

By Application: Operational Analytics Leads Growth Curve

Customer and marketing intelligence retained 29.63% of 2025 revenue, as brands enrich first-party IDs with demographic and intent signals. Yet real-time operational analytics is the fastest-growing use case at a 15.59% CAGR, propelled by edge sensors and sub-second event streaming. The data as a service market size attached to operational analytics benefits from manufacturing, logistics, and energy segments seeking predictive maintenance and dynamic routing.

Fraud detection models integrate utility-payment histories and social-graphs, extending credit to thin-file consumers while preserving risk thresholds. Risk and compliance workloads ingest sanctions lists and adverse-media feeds to slash false positives. Supply-chain optimization fuses shipping manifests, port congestion, and weather data, cutting dwell times and boosting on-time delivery. Product and pricing analytics adjust shelf prices every 15 minutes, raising gross margins. Emerging workloads in HR analytics, ESG reporting, and clinical-trial recruitment follow overall market pace.

Geography Analysis

North America generated 40.62% of 2025 revenue, anchored by tier-one data vendors and dense hyperscale infrastructure. Financial firms drive alternative-data demand, while state-level privacy laws require granular consent management. Canada pilots federated health exchanges, and Mexico’s nearshoring wave spurs cross-border freight visibility. Growth moderates as the region matures, pivoting from raw feeds to value-added analytics, yet product innovation still incubates here.

Asia-Pacific is the fastest-growing region at a 15.84% CAGR through 2031. Government-backed exchanges in China enable compliant monetization of industrial and consumer datasets, while India’s Open Network for Digital Commerce levels the playing field for small merchants. Japan’s Society 5.0 subsidizes industrial IoT and cross-company sharing. Australia and New Zealand promote cloud-first policies, and Southeast Asia invests in subsea fiber to support fintech. Fragmented regulations complicate integration, but scale and digital-transformation imperatives sustain double-digit expansion.

Europe’s stringent GDPR regime shapes market dynamics, raising compliance barriers but rewarding privacy-enhancing computation. Germany and the United Kingdom lead adoption through automotive telematics and financial market data, while France aggregates hospital and genomics records for federated research. Southern Europe and the Middle East expand from smaller bases; the United Arab Emirates and Saudi Arabia invest in smart-city platforms that require localized compute. South American growth is constrained by macro volatility, yet Brazil’s maturing data-protection law begins to catalyze customer-data platforms in agribusiness and retail.

Competitive Landscape

Roughly 45-50% of 2025 revenue accrues to the top ten vendors, indicating moderate fragmentation. Bloomberg, Thomson Reuters, and S&P Global protect entrenched franchises via proprietary data pipelines and integrated terminals. Cloud-native challengers such as Snowflake and Databricks unbundle storage and analytics, offering open sharing protocols and consumption pricing. Amazon Web Services Data Exchange now lists more than 3,500 third-party datasets, leveraging compute footprints for vertical integration.

Strategic activity centers on vertical depth and geographic expansion. Oracle’s 2026 acquisition of Datavant adds healthcare interoperability, while SAP and Google co-develop manufacturing data models. Sustainability data emerges as white space, driven by EU CSRD and impending SEC rules. Disruptors such as SafeGraph offer hourly-refreshed location intelligence, stealing share from quarterly update incumbents. Privacy-enhancing computation differentiates vendors that support federated learning or confidential computing.

Venture funding flows toward decentralized protocols like Ocean Protocol that promise peer-to-peer data monetization, though adoption remains pilot-stage. API-automation players Fivetran and Airbyte remove connector maintenance burdens, freeing engineers for modeling. Horizontal niches such as firmographic enrichment face price compression, whereas vertical specialties like clinical-trial recruitment sustain premium pricing. Private-equity roll-ups may accelerate, but antitrust bodies are likely to scrutinize any mega deals concentrating pivotal data assets.

Data As A Service Industry Leaders

Bloomberg Finance L.P.

Thomson Reuters Corporation

S&P Global Inc.

Snowflake Inc.

RELX PLC (LexisNexis Risk Solutions)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Snowflake partnered with Salesforce to embed Data Cloud into Sales Cloud and Service Cloud, targeting mid-market firms lacking dedicated data engineers.

- January 2026: Oracle acquired Datavant’s enterprise connectivity unit for USD 1.8 billion, bolstering real-world evidence and interoperability in Oracle Health.

- December 2025: Amazon Web Services launched AWS Clean Rooms for advertising, enabling privacy-preserving overlap analysis without sharing raw data.

- November 2025: Bloomberg released Data License 2.0, a sub-50-millisecond cloud API that replaces legacy FTP feeds.

Global Data As A Service Market Report Scope

Data as a Service is an information provision and distribution model in which data files are made available to customers over a network. DaaS is primarily a cloud strategy used to facilitate the accessibility of business-critical data in a protected and affordable manner.

The Data As a Service Market Report is Segmented by End-User Industry (BFSI, Healthcare, Retail, Manufacturing, Government, IT, Energy, Education, Others), Deployment (Public Cloud, Private Cloud, Hybrid), Data Type (Structured, Unstructured, Semi-Structured), Organization Size (Large Enterprises, SMEs), Application (Operational Analytics, Customer Intelligence, Risk Management, Supply-Chain, Fraud Detection, Pricing, Others), and Geography. Market Forecasts are in Value (USD).

| BFSI |

| IT and Telecommunications |

| Government and Public Sector |

| Retail and E-Commerce |

| Healthcare and Life Sciences |

| Manufacturing |

| Energy and Utilities |

| Education |

| Others End-User Industry |

| Public Cloud |

| Private Cloud |

| Hybrid / Multi-Cloud |

| Structured Data |

| Unstructured Data |

| Semi-Structured Data |

| Large Enterprises |

| Small and Medium Enterprises |

| Real-Time Operational Analytics |

| Customer and Marketing Intelligence |

| Risk and Compliance Management |

| Supply-Chain and Logistics Optimisation |

| Fraud Detection and Credit Scoring |

| Product and Pricing Analytics |

| Others Application |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By End-User Industry | BFSI | |

| IT and Telecommunications | ||

| Government and Public Sector | ||

| Retail and E-Commerce | ||

| Healthcare and Life Sciences | ||

| Manufacturing | ||

| Energy and Utilities | ||

| Education | ||

| Others End-User Industry | ||

| By Deployment Model | Public Cloud | |

| Private Cloud | ||

| Hybrid / Multi-Cloud | ||

| By Data Type | Structured Data | |

| Unstructured Data | ||

| Semi-Structured Data | ||

| By Organization Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| By Application | Real-Time Operational Analytics | |

| Customer and Marketing Intelligence | ||

| Risk and Compliance Management | ||

| Supply-Chain and Logistics Optimisation | ||

| Fraud Detection and Credit Scoring | ||

| Product and Pricing Analytics | ||

| Others Application | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How fast is the data as a service market expected to grow from 2026 to 2031?

It is projected to advance at a 15.53% CAGR, climbing from USD 29.72 billion in 2026 to USD 61.18 billion by 2031.

Which deployment model is gaining the most traction among enterprises?

Hybrid and multi-cloud architectures are expanding at a 15.69% CAGR as firms balance residency compliance with flexibility.

What drives the rapid uptake of unstructured data services?

Video, sensor, and text assets fuel real-time analytics and AI RAG models, pushing unstructured formats to the fastest growth rate, 15.71% annually through 2031.

Why are small and medium enterprises increasing their share of spending?

API-first platforms, serverless billing, and cloud marketplaces remove integration barriers and align costs with usage, letting SMEs scale gradually.

Which region will lead growth over the forecast horizon?

Asia-Pacific is forecast to expand at a 15.84% CAGR, supported by government-backed data exchanges and large-scale digital transformation programs.

What creates white-space opportunity for new vendors?

Emerging ESG and sustainability datasets linked to upcoming disclosure rules remain under-served, offering premium pricing potential for accurate, timely coverage.

Page last updated on: