Dairy Cream Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 11.37 Billion |

| Market Size (2031) | USD 13.67 Billion |

| Growth Rate (2026 - 2031) | 3.76% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. |

|

Dairy Cream Market Analysis by ���ϲ�����

The dairy cream market size was valued at USD 11.02 billion in 2025, increased to USD 11.37 billion in 2026, and is projected to reach USD 13.67 billion by 2031, growing at a compound annual growth rate (CAGR) of 3.76% during the forecast period. This steady growth is primarily driven by the rising demand for premium, natural, and versatile dairy ingredients that enhance texture, flavor, and sensory appeal in food and beverages. The increasing consumption of convenience foods, the expansion of the foodservice and café culture, and a growing preference for indulgent culinary experiences are key factors supporting cream utilization across various end-use applications. Additionally, sustainability initiatives, clean-label trends, and animal welfare considerations are influencing purchasing behavior, prompting manufacturers to develop ethically sourced and environmentally responsible products.

Key Report Takeaways

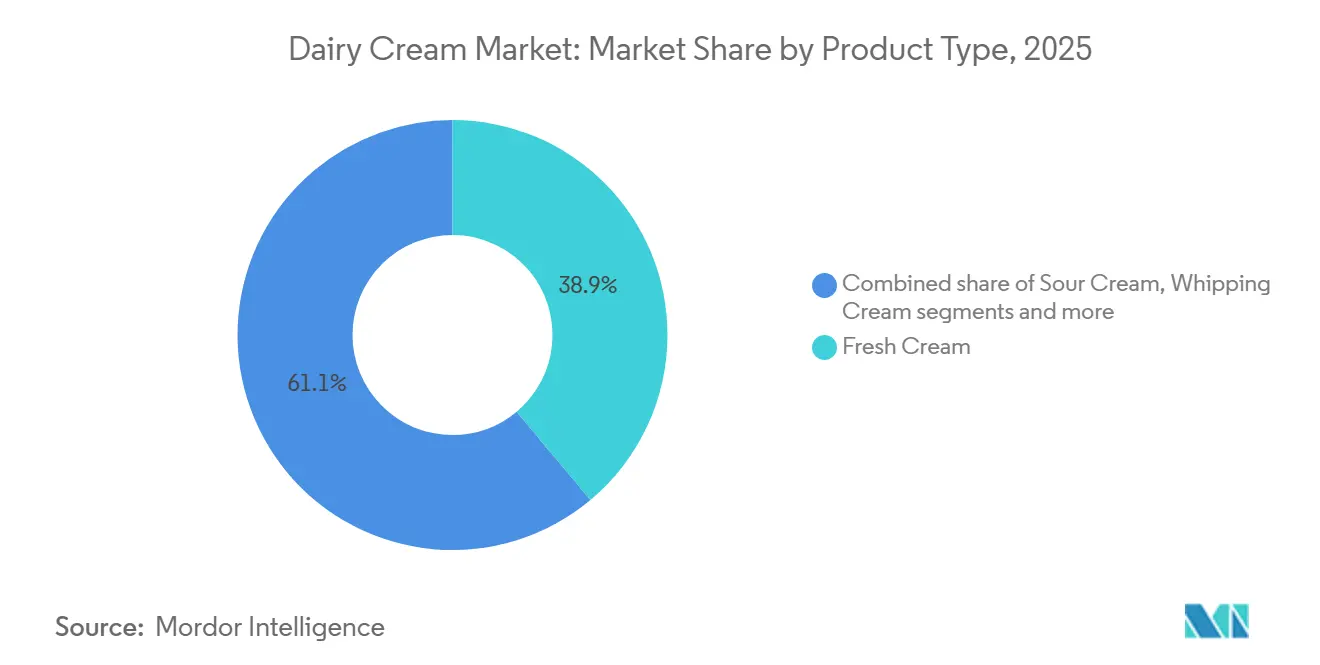

- By product type, Fresh Cream led with 38.92% of the dairy cream market share in 2025, while Whipping Cream is forecast to expand at a 6.63% CAGR to 2031, buoyed by bakery and café uptake.

- By packaging, Cartons accounted for 43.23% of 2025 sales, whereas Glass Jars show the fastest projected growth at 6.54% through 2031 as premium brands chase circular-economy mandates.

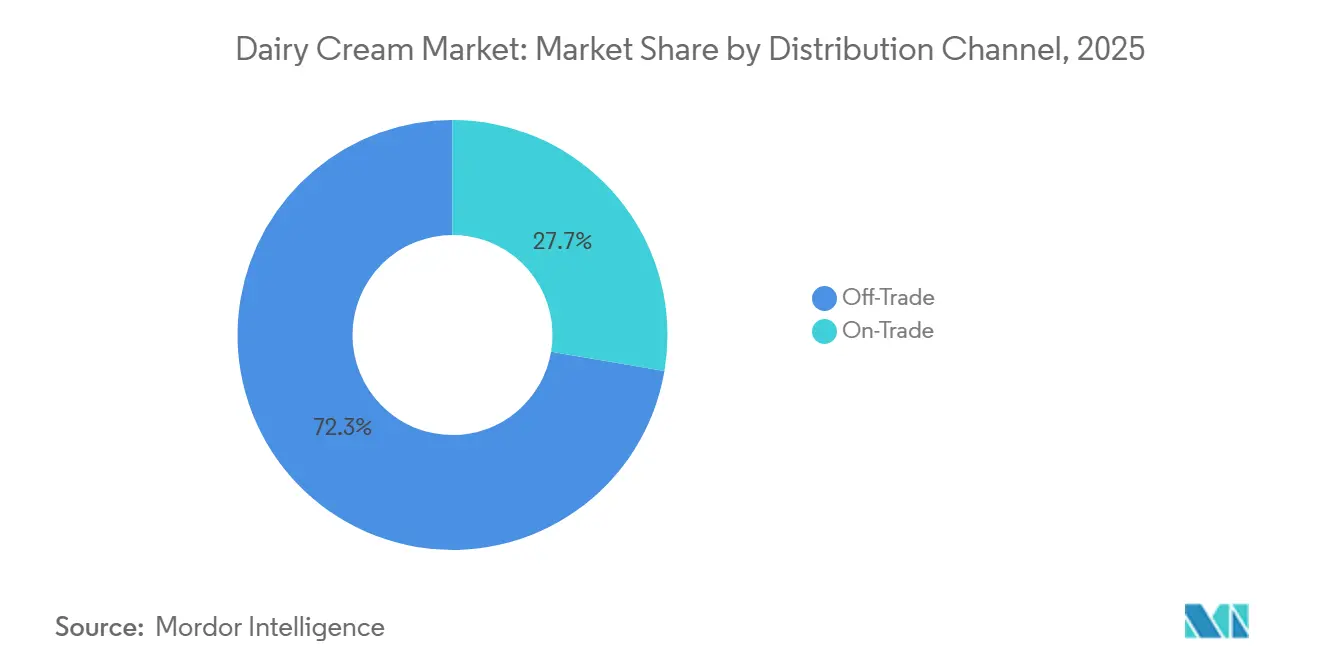

- By distribution channel, Off-Trade represented 72.32% of value in 2025; however, On-Trade is set to rise at 5.81% annually with hotels and restaurants rebuilding post-pandemic menus.

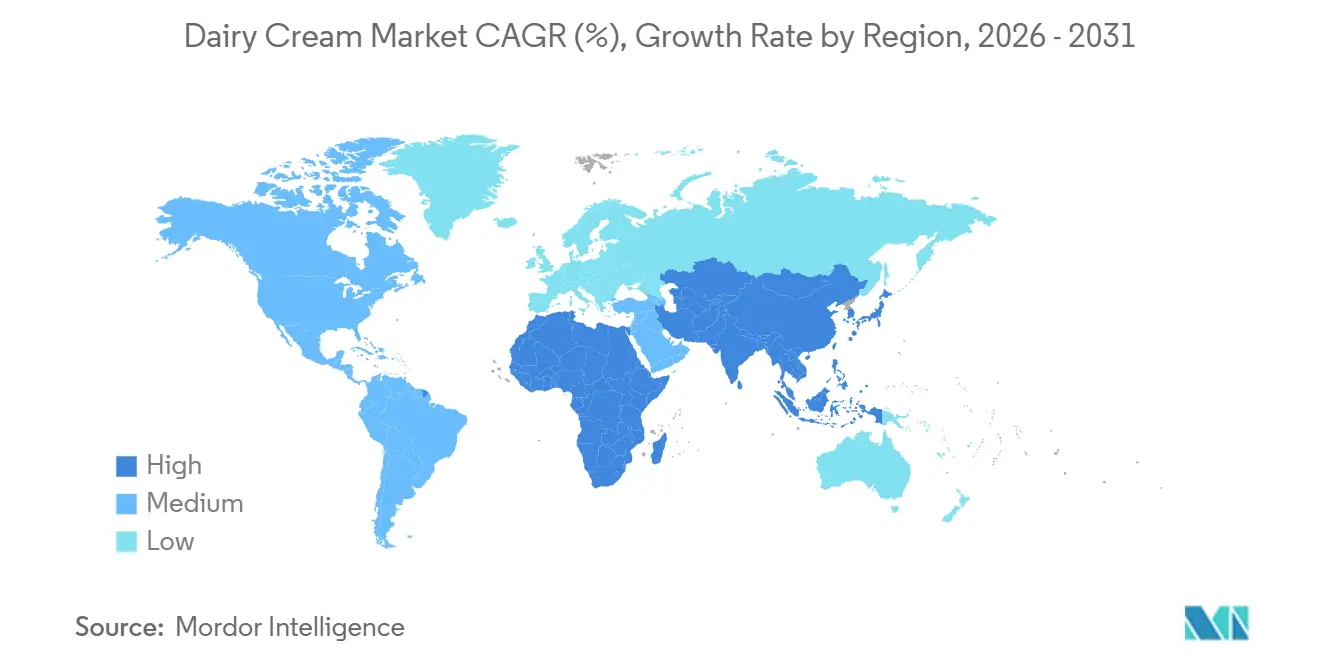

- By geography, Europe held 32.11% of the value in 2025, but Asia-Pacific is projected to grow quickest at 7.12% a year on the back of China’s self-sufficiency push and India’s cooperative distribution strength.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dairy Cream Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for convenience foods | +0.8% | Global, with concentration in North America, Western Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Sustainability and animal welfare initiatives | +0.5% | Europe and North America core, expanding to Australia and New Zealand | Long term (≥ 4 years) |

| Innovation in product formulations | +0.7% | Global, led by Europe and North America; spillover to Asia-Pacific premium segments | Long term (≥ 4 years) |

| Growth of foodservice and cafe culture | +0.8% | Asia-Pacific core, expanding in Middle East and South America urban centers | Medium term (2-4 years) |

| Technological advancements in cream processing | +0.6% | Global, with early adoption in Europe, North America, and developed Asia-Pacific markets | Medium term (2-4 years) |

| Premiumization of dairy products | +0.6% | Europe, North America, and affluent Asia-Pacific metros (Shanghai, Tokyo, Singapore) | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Rising demand for convenience foods

The increasing demand for convenience foods is driving growth in the global dairy cream market, as consumers prioritize time-efficient meal solutions without sacrificing taste or quality. Factors such as fast-paced urban lifestyles, dual-income households, and changing dietary preferences have boosted the consumption of ready-to-eat (RTE), ready-to-cook (RTC), and packaged meal options, which often utilize dairy cream for its ability to enhance texture, richness, and flavor stability. Dairy cream serves a vital functional role in processed food formulations by improving mouthfeel, emulsification, and consistency, making it a key ingredient in the development of convenience-focused products. Furthermore, the growth of chilled and frozen food categories, along with advancements in UHT and long-shelf-life cream processing technologies, has allowed manufacturers to incorporate cream into packaged foods while ensuring product safety and stability. Food producers are increasingly using cream in sauces, meal kits, instant mixes, and dessert bases to enhance sensory appeal and provide indulgent eating experiences in convenient formats.

Sustainability and animal welfare initiatives

Sustainability and animal welfare initiatives are becoming significant growth drivers in the global dairy cream market, influencing both consumer purchasing patterns and corporate strategies. Growing awareness of environmental concerns, including carbon emissions, water usage, and livestock treatment, has led consumers to prefer dairy products that adhere to responsible sourcing and ethical production practices. In response, dairy cream manufacturers are adopting regenerative agriculture methods, methane-reduction technologies, improved feed efficiency, and certified humane farming systems to enhance supply chain transparency and minimize environmental impact. Certifications such as organic, grass-fed, pasture-raised, and animal-welfare-approved labels are gaining importance, enabling brands to differentiate their cream products and support premium pricing strategies. Additionally, companies are incorporating sustainability commitments into packaging innovations by using recyclable cartons, reduced-plastic formats, and lower-emission processing technologies.

Innovation in Product Formulations

Innovation in product formulations remains a significant driver in the global dairy cream market, as manufacturers respond to evolving consumer expectations regarding quality, ethics, and functionality. Companies are increasingly launching differentiated cream variants to meet demands for better taste, enhanced performance, adherence to animal welfare standards, and clean-label attributes. Reformulation efforts focus on fat optimization, improved whipping stability, heat resistance, and extended shelf life, while incorporating ethical sourcing and sustainability claims to enhance brand appeal. For example, in August 2024, Waitrose introduced ‘free-range’ cream across its own-label range, including single, double, whipping, and extra thick cream. This initiative highlights the growing importance of animal welfare and transparent sourcing practices, which are becoming key factors influencing consumer purchasing decisions. Such innovations not only foster differentiation in a moderately concentrated market but also enable brands to achieve premium positioning and build stronger consumer loyalty.

Growth of foodservice and cafe Culture

The global dairy cream market is driven by the rapid expansion of foodservice outlets, specialty cafés, bakeries, and hospitality chains. Professional kitchens increasingly depend on high-performance cream products to enhance menu quality and maintain consistency. The growing popularity of café culture, premium dessert chains, and experiential dining concepts has further boosted the demand for cream with superior whipping stability, smooth texture, and visual appeal. As consumers dine out more frequently and seek indulgent, visually appealing food and beverages, foodservice operators are emphasizing the use of premium dairy ingredients that perform reliably under high-volume operations. For example, in October 2024, at FHA HoReca 2024, Anchor Food Professionals introduced the Infiniti Whipping Cream, designed to meet the evolving performance requirements of professional chefs and pâtissiers. Such product launches demonstrate how manufacturers are innovating to address foodservice needs, focusing on improved aeration, stability, and operational efficiency.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising competition from plant-based cream alternatives | -0.5% | North America, Western Europe, and urban Asia-Pacific (Australia, Japan, South Korea) | Medium term (2-4 years) |

| Short shelf life of fresh dairy cream | -0.4% | Global, with acute impact in regions lacking cold-chain infrastructure (Sub-Saharan Africa, South Asia, Southeast Asia) | Short term (≤ 2 years) |

| Volatility in raw milk quality and supply | -0.3% | Global, with seasonal peaks in temperate regions (Europe, North America, Southern South America) | Short term (≤ 2 years) |

| Stringent food safety and quality regulations | -0.2% | Global, with highest compliance costs in Europe, North America, and developed Asia-Pacific markets | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Rising competition from plant-based cream alternatives

The growing competition from plant-based cream alternatives is a notable restraint on the dairy cream market, driven by shifting consumer preferences toward vegan, lactose-free, and environmentally perceived lower-impact options. Plant-based creams made from oat, almond, soy, coconut, and other botanical sources are achieving significant retail penetration. These products offer comparable texture and whipping functionality while appealing to flexitarian and dairy-averse consumers. Additionally, they are often promoted with claims of lower saturated fat content, sustainability, and ethical sourcing, which strongly attract younger and health-conscious demographics. For example, the Good Food Institute (GFI) reported that consumers in the United Kingdom purchased an average of 9.1 million plant-based products per week from major supermarkets during the early part of 2024 [1]Source: Good Food Institute (GFI), "Plant-based meat and milk are now mainstream choices for British consumers", gfieurope.org. This increasing adoption underscores a structural shift toward alternative dairy solutions, heightening competitive pressure on traditional cream manufacturers.

Short shelf life of fresh dairy cream

The short shelf life of fresh dairy cream poses a significant challenge in the global dairy cream market, as it necessitates stringent storage, transportation, and inventory management throughout the supply chain. Due to its high moisture and fat content, fresh cream is highly perishable and prone to microbial growth, spoilage, and quality deterioration if not consistently refrigerated. This reliance on an uninterrupted cold chain increases logistical complexity and operational costs for manufacturers, distributors, and retailers. Temperature fluctuations during storage or transit can result in product spoilage, financial losses, and reputational damage for brands. Additionally, the limited shelf life hinders geographic expansion into regions lacking developed refrigeration infrastructure, thereby restricting market penetration. Retailers must carefully manage stock rotation to minimize waste, which can reduce profit margins and limit opportunities for promotional activities.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Fresh Cream Dominance Masks Whipping Cream Surge

Fresh cream accounted for 38.92% of the dairy cream market in 2025, emerging as the leading product type due to strong consumer preference, its natural positioning, and superior functional performance. Its dominance is largely attributed to its perception as an authentic, minimally processed dairy product that aligns with clean-label and premium food trends. Consumers increasingly associate fresh cream with higher quality, richer taste, and better texture compared to processed or non-dairy alternatives, driving repeat purchases and fostering brand loyalty. Furthermore, advancements in pasteurization, packaging, and refrigerated distribution have improved product stability and availability across both developed and emerging markets, enhancing its market penetration.

Whipping cream is projected to grow at a CAGR of 6.63% through 2031, making it the fastest-growing segment within the dairy cream market. This growth is primarily driven by increasing demand for premium dairy ingredients that provide superior aeration, volume stability, and texture enhancement. Whipping cream offers functional benefits such as high overrun capacity, stable foam formation, and consistent structural performance, making it highly preferred in both professional and retail applications. Additionally, the growing consumer preference for visually appealing and indulgent food experiences is boosting its demand, as whipping cream enhances product aesthetics and sensory appeal.

By Packaging Type: Carton Efficiency Versus Glass Premiumization

Cartons accounted for 43.23% of the dairy cream packaging market share in 2025, establishing themselves as the leading packaging format. This dominance is attributed to their effective balance of product protection, convenience, and cost efficiency. Their widespread adoption is driven by their ability to preserve freshness and extend shelf life through advanced aseptic and multilayer barrier technologies, which are essential for maintaining cream quality. Cartons are lightweight, easy to store, and stackable, making them efficient for transportation and retail shelf management, thereby reducing handling complexities across supply chains. Additionally, cartons facilitate clear labeling, enhance branding visibility, and offer portion-controlled formats, improving consumer convenience and product differentiation. Sustainability considerations further bolster their position, as paper-based carton materials are increasingly viewed as more environmentally responsible compared to rigid plastic alternatives.

Glass jars are projected to grow at a CAGR of 6.54% through 2031, primarily driven by the rising premiumization trends within the dairy cream market. Glass packaging is widely regarded as a high-end, traditional, and purity-preserving format, enhancing product positioning in premium and artisanal segments. Consumers increasingly associate glass jars with superior quality, freshness retention, and minimal chemical interaction, which reinforces trust and brand credibility. This perception aligns closely with the clean-label movement and the demand for minimally processed, authentic dairy products. Glass provides excellent barrier properties, protecting cream from moisture, oxygen, and external contaminants without compromising taste or texture. Its reusability and recyclability further enhance its appeal among environmentally conscious consumers, supporting sustainability-focused purchasing decisions.

By Distribution Channel: Off-Trade Maturity Versus On-Trade Recovery

Off-trade channels accounted for 72.32% of the global dairy cream distribution share in 2025, maintaining their leading position due to extensive retail reach, product accessibility, and frequent consumer purchases. Supermarkets, hypermarkets, convenience stores, and online grocery platforms collectively ensure widespread availability of dairy cream products, providing consistent access for consumers in urban and semi-urban areas. The structured retail environment supports proper refrigeration and cold-chain management, which are critical for maintaining product quality and shelf life, thereby fostering consumer trust. Off-trade channels also enhance brand visibility, facilitate promotional campaigns, and offer diversified packaging formats catering to both household and bulk purchasers. The growth of organized retail networks and e-commerce grocery platforms has further strengthened this segment by offering convenience, doorstep delivery, and subscription-based purchasing options.

The on-trade segment is projected to grow at a CAGR of 5.81% through 2031, driven by the steady increase in food-away-from-home consumption and the recovery of the hospitality and foodservice industries globally. Restaurants, cafés, hotels, bakeries, and quick-service outlets are incorporating dairy cream into premium menu offerings, reflecting growing demand for indulgent and high-quality dining experiences. According to the United States Department of Agriculture (USDA), per capita food-away-from-home (FAFH) purchases reached a record high of USD 4,275 in 2024, underscoring the structural shift toward dining and beverage consumption outside the home [2]Source: United States Department of Agriculture (USDA), "Food Service Industry", usda.gov. This trend directly supports dairy cream demand within on-trade establishments, as cream-based ingredients enhance menu differentiation, product richness, and presentation appeal. Additionally, the rapid expansion of specialty cafés, dessert chains, and premium beverage outlets has increased institutional procurement of whipping and fresh cream in bulk formats.

Geography Analysis

Europe is projected to retain 32.11% of the global dairy cream market share in 2025, maintaining its leadership position due to its well-established dairy infrastructure, strong milk production base, and deep-rooted dairy consumption culture. The region's dominance is primarily driven by Germany, which, according to the German Federal Statistical Office, produced approximately 32.1 million tons of cow’s milk in 2024, making it the largest milk producer in Europe [3]Source: German Federal Statistical Office, "Germany largest EU milk producer" destatis.de. This substantial raw milk availability ensures stable cream extraction capacity and supports large-scale processing operations. Additionally, key markets such as the United Kingdom, France, Italy, and Spain significantly contribute to regional demand, supported by strong culinary traditions, advanced dairy processing technologies, and premium dairy product consumption patterns.

Asia-Pacific is forecast to grow at a CAGR of 7.12% through 2031, emerging as the fastest-growing regional market. The region's growth is driven by the rapid modernization of dairy supply chains, increasing cold-chain penetration, and the rising adoption of Western-style bakery and café culture. Expanding organized retail networks and improvements in domestic milk processing capacities are further enhancing market accessibility. Additionally, the growing middle-class population, increasing disposable incomes, and changing dietary preferences are fueling demand for dairy cream products. Innovation in Ultra-High Temperature (UHT) and long-shelf-life cream products has enabled broader distribution across diverse climatic conditions, ensuring product availability in remote areas and further accelerating the region's growth momentum.

North America, South America, and the Middle East & Africa collectively account for the remaining share of global dairy cream demand, each driven by distinct structural factors. North America benefits from advanced dairy technology, strong foodservice integration, and stable milk production systems. The region also sees increasing demand for specialty cream products driven by evolving consumer preferences and the growth of the premium food segment. South America leverages its expanding dairy farming sector and growing processing capabilities to strengthen regional supply. Rising investments in modern dairy infrastructure and government initiatives to support the dairy industry are further boosting the market. Meanwhile, the Middle East and Africa region is experiencing gradual growth, supported by improving cold-chain infrastructure, the expansion of the hospitality sector, and increasing reliance on imported and locally processed dairy cream products.

Competitive Landscape

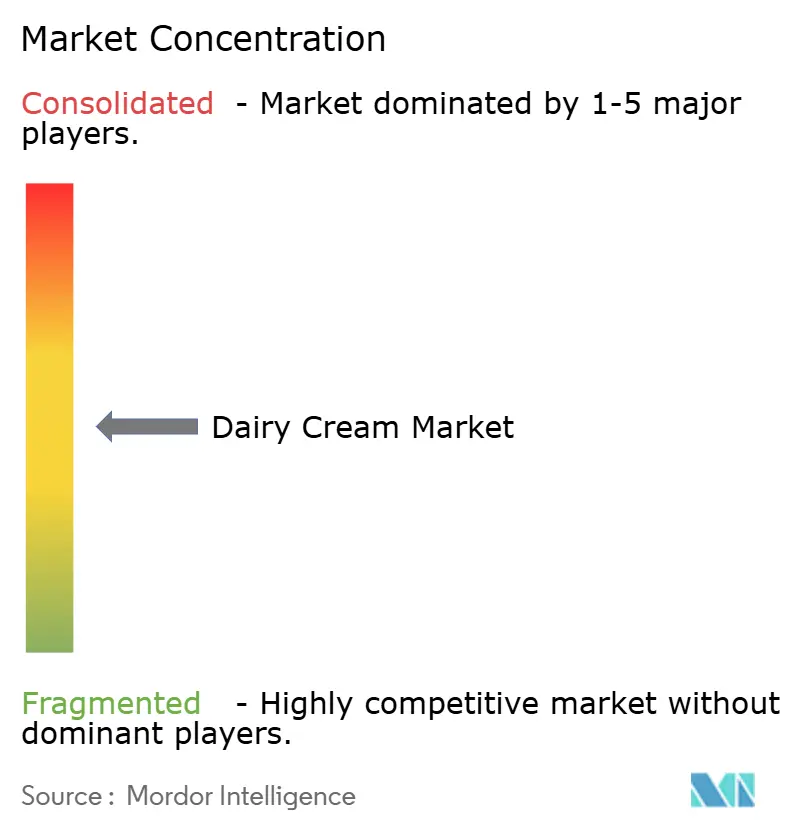

The global dairy cream market is moderately concentrated, featuring a combination of multinational dairy corporations and prominent regional cooperatives competing across retail and foodservice channels. Key players in the market include Groupe Lactalis S.A., Danone S.A., Nestlé S.A., Arla Foods amba, and Dairy Farmers of America Inc. These companies utilize vertically integrated supply chains, extensive milk procurement networks, and robust brand portfolios to sustain their competitive edge. Their global reach, advanced processing capabilities, and diverse product ranges enable them to serve both premium and mass-market segments, contributing to market stability while maintaining competitive dynamics.

Strategic differentiation in the dairy cream market increasingly focuses on product innovation and format diversification. Leading companies are introducing ambient-stable and UHT cream formats to expand into regions with limited cold-chain infrastructure, thereby broadening their distribution networks. Additionally, there is a rising focus on organic, grass-fed, and regenerative-agriculture-certified cream products aimed at affluent and environmentally conscious consumers. Hybrid dairy-plant formulations are also gaining traction, allowing manufacturers to cater to flexitarian consumers seeking reduced dairy content while preserving functional performance and sensory quality. These innovations are reshaping competitive strategies and enabling companies to address shifting consumer preferences effectively.

Sustainability and technological advancements remain integral to competitive strategies in the market. Leading players are prioritizing initiatives such as reducing carbon footprints, mitigating methane emissions in dairy farming, adopting recyclable and low-impact packaging, and implementing traceable sourcing systems to enhance brand credibility. Furthermore, the digitalization of supply chains, automation in cream separation and fat standardization processes, and the use of AI-driven quality monitoring systems are improving operational efficiency and ensuring product consistency.

Dairy Cream Industry Leaders

-

Groupe Lactalis S.A.

-

Danone S.A.

-

Nestlé S.A.

-

Arla Foods amba

-

Dairy Farmers of America Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Elle & Vire has introduced its "Finesse Light Whipping Cream" (Crème Finesse) in Macau, featuring a reduced fat content of 25% to cater to the growing consumer preference for healthier products.

- November 2025: Trewithen Dairy introduced a new double cream product in time for Christmas. This thick double cream is made from 100% Cornish milk sourced from grazing cows and is available in a 300 ml pack.

- December 2024: Fonterra introduced its new Anchor Easy Bakery Cream at the China International Import Expo (CIIE) in Shanghai. The Anchor Easy Bakery Cream is made using 100% New Zealand dairy.

- August 2024: Whipped cream brand Whipnotic has introduced its festive line-up, featuring two new flavors: Peppermint Mocha and Apple Crisp. These join the brand's existing varieties, which include Peach Mango, Strawberry Swirl, Vanilla Salted Caramel, and Brownie Batter.

Global Dairy Cream Market Report Scope

The cream is a dairy product prepared from milk and has a certain level of saturated fat content. It can be used in a variety of recipes and dishes, such as spicy, sweet, and salty sauces, ice cream, and others. The dairy cream market is segmented into product type, packaging type, distribution channels, and geography. Based on product type, the market is segmented into fresh cream, thickened cream/heavy cream, whipping cream, sour cream, and other cream types. Based on packaging type, the market is segmented into cartons, plastic tubs, glass jars, and other packaging types. Based on the distribution channel, the market is segmented into on-trade and off-trade. The off-trade segment is further segmented into supermarkets/hypermarkets, convenience stores, online retail stores, and other distribution channels. Based on geography, the market is segmented into North America, Europe, Asia-Pacific, South America, the Middle East, and Africa. For each segment, market sizing and forecasts have been prepared based on Value (USD) and Volume (Units).

| Fresh Cream |

| Thickened Cream/Heavy Cream |

| Whipping Cream |

| Sour Cream |

| Other Cream Types |

| Cartons |

| Plastic Tubs |

| Glass Jars |

| Others |

| On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Fresh Cream | |

| Thickened Cream/Heavy Cream | ||

| Whipping Cream | ||

| Sour Cream | ||

| Other Cream Types | ||

| By Packaging Type | Cartons | |

| Plastic Tubs | ||

| Glass Jars | ||

| Others | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big will the dairy cream market be by 2031?

It is projected to reach USD 13.67 billion by 2031, growing at a 3.76% CAGR from 2026.

Which product type is growing quickest?

Whipping Cream is forecast to expand at 6.63% annually through 2031 as artisanal bakeries and cafés scale in Asia and the Middle East.

Why are glass jars gaining share?

Premium brands adopt glass to signal quality and comply with European deposit-return mandates, driving a 6.54% CAGR for the format.

Which region offers the fastest growth?

Asia-Pacific leads with a projected 7.12% CAGR as China ramps up self-sufficient UHT cream output and India expands cooperative distribution.

Page last updated on: