Constipation Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

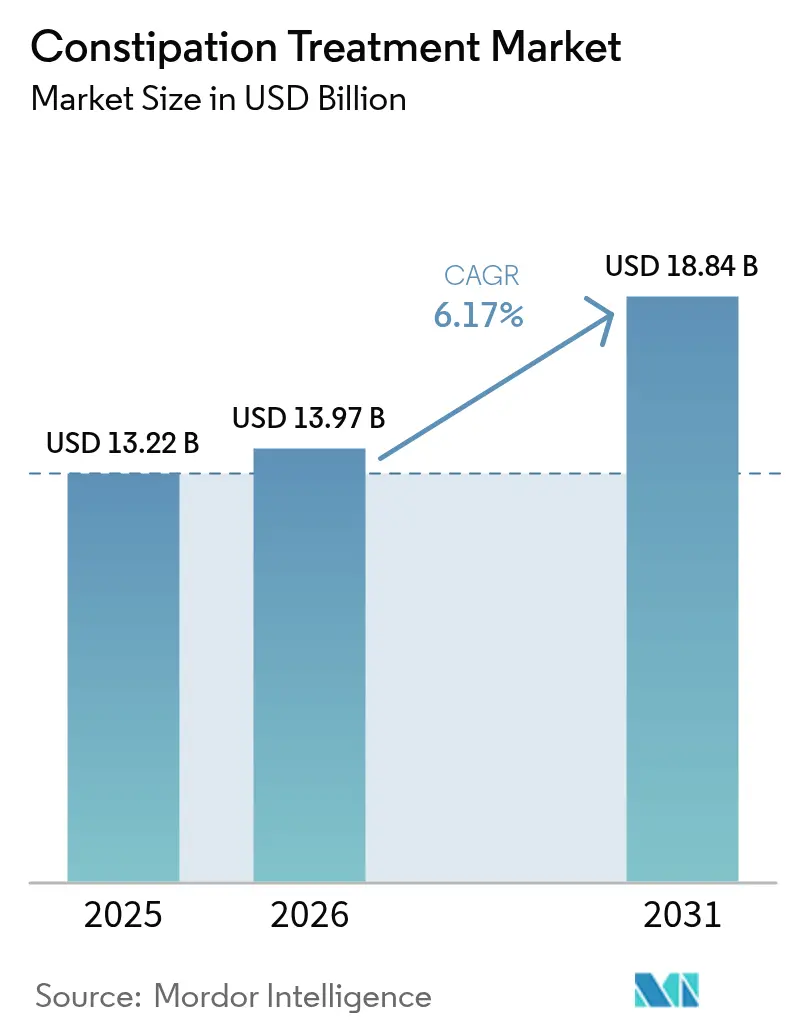

| Market Size (2026) | USD 13.97 Billion |

| Market Size (2031) | USD 18.84 Billion |

| Growth Rate (2026 - 2031) | 6.17% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

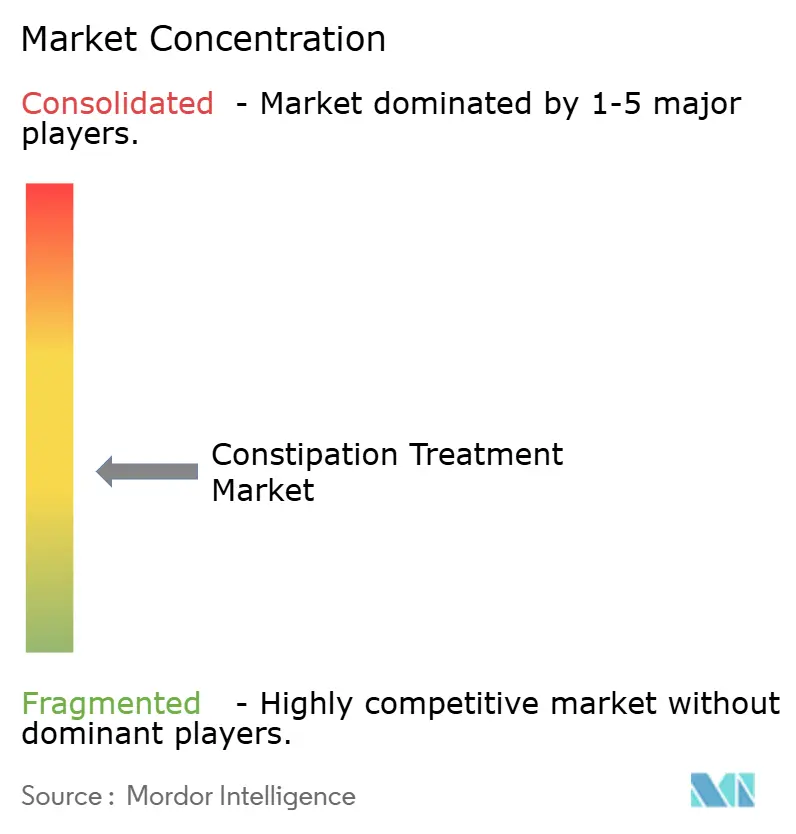

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Constipation Treatment Market Analysis by ���ϲ�����

The Constipation Treatment Market size is projected to expand from USD 13.22 billion in 2025 and USD 13.97 billion in 2026 to USD 18.84 billion by 2031, registering a CAGR of 6.17% between 2026 to 2031.

Prescription volumes for opioid analgesics remain high, locking many patients into chronic opioid-induced constipation regimens even as public-health campaigns attempt to reduce misuse. At the same time, e-commerce pharmacies shorten purchase paths and lift over-the-counter laxative penetration, especially among price-sensitive consumers. Secretagogues and other novel mechanisms win formulary access in irritable bowel syndrome with constipation, yet payers increasingly prefer lower-cost alternatives, nudging the product mix toward generic osmotics. Consolidation among branded manufacturers accelerates as patent cliffs loom, while digital biofeedback tools certified as software medical devices start to siphon volume from drug therapies.

Key Report Takeaways

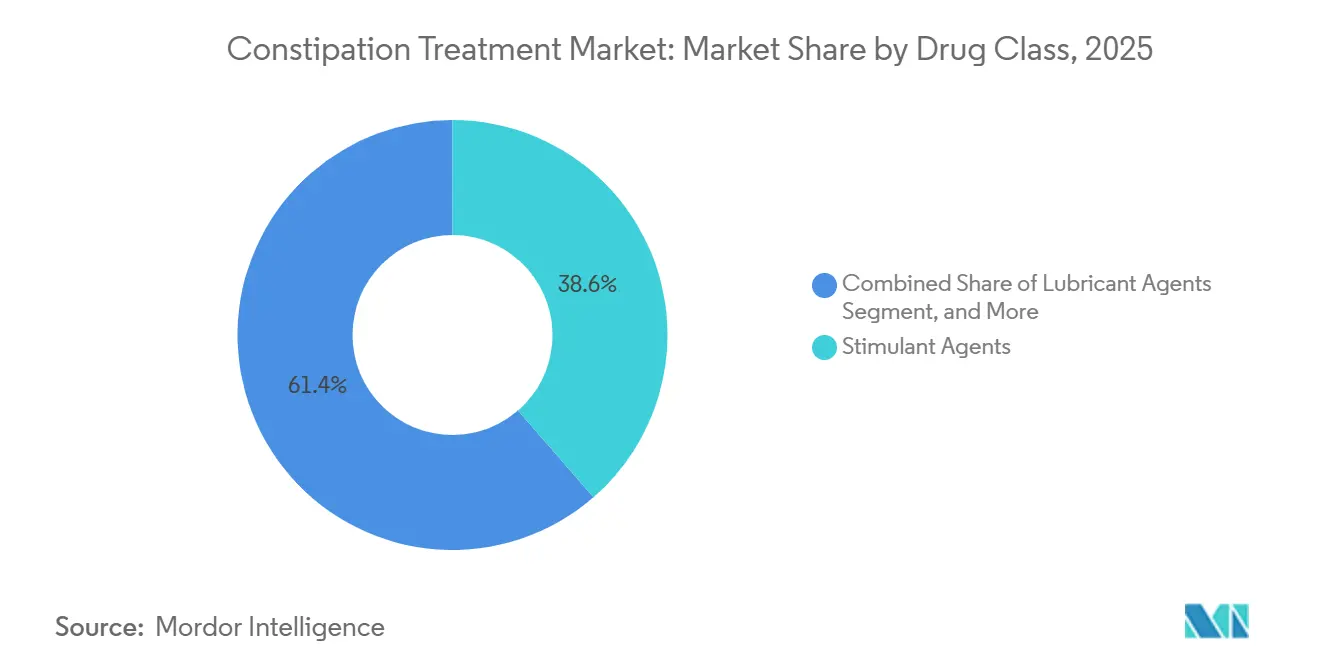

- By drug class, stimulant agents led with 38.62% of the constipation treatment market share in 2025, whereas lubricant agents are forecast to expand at a 7.06% CAGR through 2031.

- By disease type, opioid-induced constipation captured 34.07% of the value in 2025, while the irritable bowel syndrome with constipation sub-segment is expected to accelerate at a 9.63% CAGR to 2031.

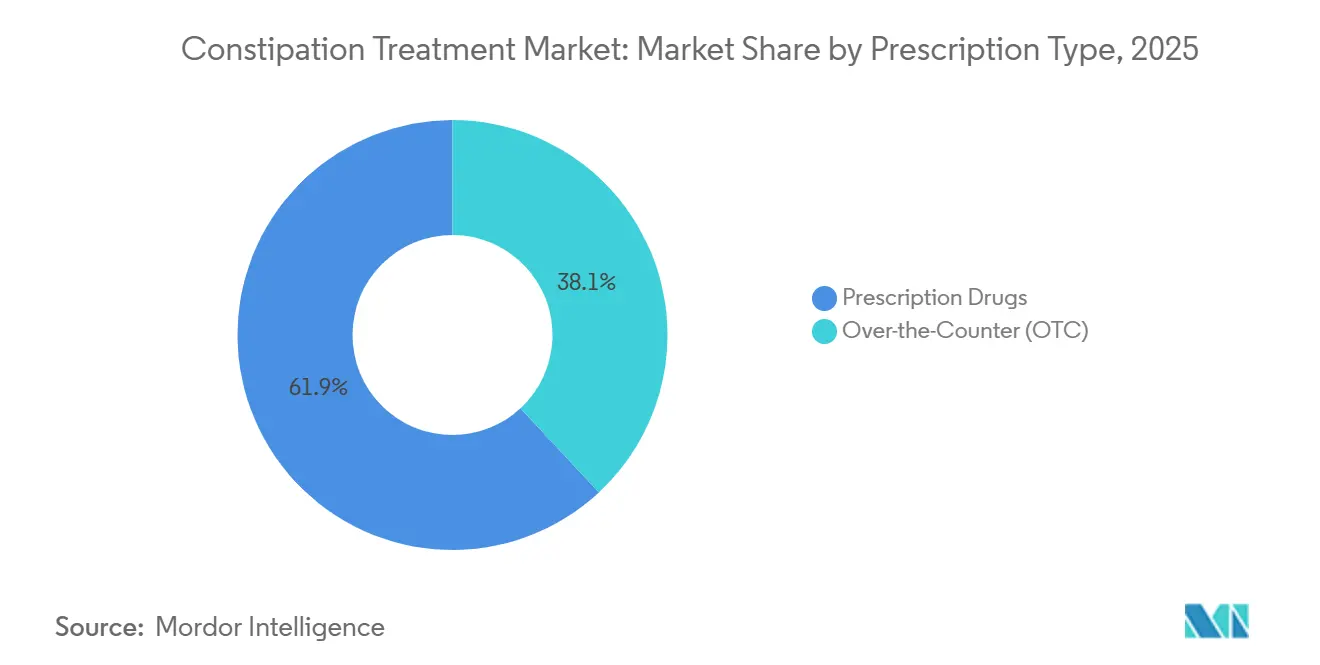

- By prescription type, prescription medicines accounted for 61.92% of revenue in 2025, yet over-the-counter formulations are projected to grow at an 8.08% CAGR during the same horizon.

- By route of administration, oral formulations accounted for 75.78% of sales in 2025, and the oral route is anticipated to grow at an 8.41% CAGR, outpacing rectal products.

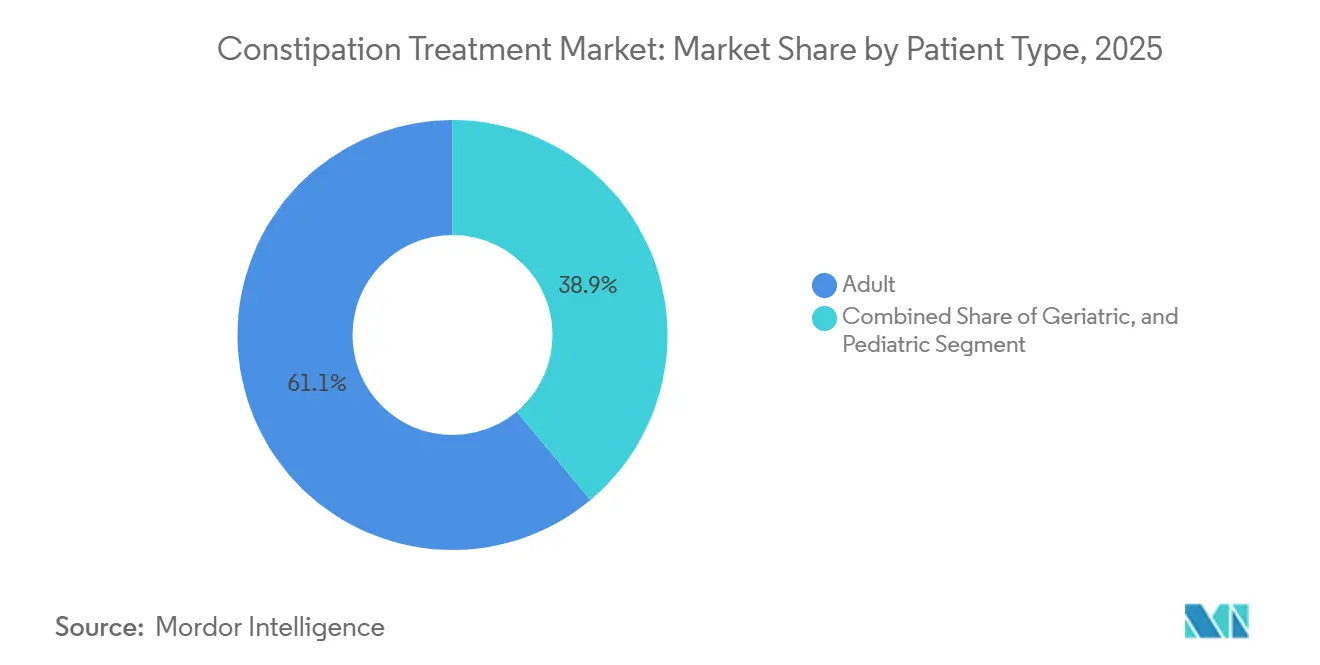

- By patient type, adults represented 61.08% of treated patients in 2025, although the geriatric cohort is advancing at an 8.82% CAGR, the fastest among all groups.

- By distribution channel, hospital pharmacies held 34.78% of distribution revenue in 2025, while online and direct-to-consumer channels are expanding at a 7.83% CAGR as telehealth bundles drive subscription refills.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Constipation Treatment Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging Population Boosts Chronic-Use Demand | +1.2% | Global, strongest in North America, Europe, Japan | Long term (≥ 4 years) |

| Opioid Prescription Surge Driving OIC | +1.5% | North America, Europe | Medium term (2-4 years) |

| E-Commerce Accelerates OTC Laxative Uptake | +0.9% | Global, early gains in North America, Asia-Pacific cities | Short term (≤ 2 years) |

| Mid-Stage Gut-Targeted Neuromodulators | +0.7% | North America, Europe | Long term (≥ 4 years) |

| Microbiome & Digital Adherence Innovations | +0.6% | North America, Western Europe, Australia | Medium term (2-4 years) |

| Approvals of New GC-C and 5-HT4 Agonists | +1.3% | Global, regulatory leads in US, EU, Japan | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Aging Population Boosts Chronic-Use Demand

People aged 65 and above numbered 761 million in 2025 and are projected to reach 994 million by 2030, a shift that raises baseline constipation prevalence to more than 26%.[1]United Nations DESA, “World Population Ageing 2025,” un.org Long-term care facilities mandate prophylactic osmotic or bulk-forming agents, turning these products into recurring, annuity-style prescriptions. Japan, where 29.1% of citizens are older than 65, reported a 14% rise in laxative scripts among those over 75 during 2025. Higher Parkinson’s and diabetes incidence further entrenches multi-year regimens. Manufacturers answer with low-sodium, palatable formulas aligned with the 2024 Beers Criteria update, which flags high-osmolarity products for deprescribing.

Opioid Prescription Surge Driving OIC Therapies

The United States dispensed 142.2 million opioid prescriptions in 2024, only 7% below 2023, sustaining a large cohort at risk for opioid-induced constipation.[2]Centers for Disease Control and Prevention, “U.S. Opioid Dispensing Rate Maps,” cdc.gov Up to 81% of chronic-opioid patients experience OIC, yet fewer than one-quarter receive a peripherally acting mu-opioid receptor antagonist, leaving an undertreated pool that often presents in emergency care for fecal impaction. European regulators widened methylnaltrexone labeling in 2024, enlarging the non-cancer pain segment. Physicians increasingly redirect to GC-C agonists like linaclotide off-label to bypass prior-authorization barriers, spurring interest in fixed-dose opioid–laxative combinations that minimize therapeutic gaps.

E-Commerce Accelerates OTC Laxative Penetration

Online sales of OTC laxatives in the United States jumped 34% year over year in 2025, compared with 4.2% in physical retail.[3]National Association of Chain Drug Stores, “2025 Pharmacy Market Trends Report,” nacds.org Direct-to-consumer subscription kits lower per-unit costs by 22% and deliver discreet packaging that reduces stigma, drawing first-time buyers who had avoided in-store purchases. Amazon Pharmacy’s algorithmic storefront funnels same-day delivery across 12 cities, pressuring competitors to match convenience or shed share. Regulatory oversight lags: the FDA issued 17 warning letters in 2025 for unapproved stimulant combinations. Yet private-label brands now command 29% of online category revenue, squeezing premium manufacturers’ pricing latitude.

Pipeline Gut-Targeted Neuromodulators Enter Mid-Stage Trials

Several Phase II neuromodulators showed 53% symptom relief versus 29% for placebo, earning FDA Breakthrough Therapy designation in 2025. These agents aim to normalize enteric nervous signaling without conventional pro-secretory effects, potentially redefining moderate-to-severe treatment algorithms. Venture funding gravitates toward start-ups that pair such molecules with digital adherence coaching to maximize real-world persistence. If successful, these entrants could compress demand for stimulant and osmotic agents that dominate current chronic protocols.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adverse-Effect & Dependency Fears | -0.8% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Stricter OTC Stimulant / Sodium-Phosphate Rules | -0.6% | North America, Europe, Australia | Short term (≤ 2 years) |

| Biofeedback Platforms Cannibalize Drug Spend | -0.5% | North America, Western Europe | Medium term (2-4 years) |

| Consumer Shift to Herbal & Home Remedies | -0.4% | Global, notable in Asia-Pacific and Latin America | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Adverse-Effect & Dependency Fears Curb Long-Term Use

A 2025 FDA surveillance review showed that 19% of chronic stimulant users developed hypokalemia serious enough to require hospitalization. Advocacy groups caution against more than 14 straight days of stimulant use, and cohort data reveal a 34% dose-escalation rate within 18 months, validating dependency concerns. Health Canada’s advisory linking high-dose polyethylene glycol to aspiration pneumonia in frail seniors has driven nursing homes toward fiber-based agents despite a slower onset.

Stricter OTC Stimulant / Sodium-Phosphate Regulations

The FDA shifted certain sodium phosphate laxatives to prescription-only status in 2024, erasing USD 87 million in annual OTC revenue. Australia capped bisacodyl pack sizes in early 2025, while the European Commission’s labeling harmonization proposal forces manufacturers to add dependency warnings well before the 2027 deadline. Compliance costs thin the field, granting scale players extra shelf space but limiting consumer choice.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Secretagogues Reshape Prescription Mix

Stimulant agents accounted for 38.62% of segment revenue in 2025, reflecting their low cost and rapid onset, yet lubricant formulas are projected to grow at a 7.06% CAGR as microencapsulation reduces aspiration risk among elders. Osmotic agents remain first-line in hospital protocols, though their 5.8% growth lags the 6.17% baseline of the constipation treatment market. Secretagogues already command premium pricing, and their patents expiring in 2027-2028 could invite biosimilars that compress margins.

Bulk-forming products enjoy a reputation for “natural” relief but require high fluid intake that deters frail patients. Stool softeners, chiefly docusate, slide after a Cochrane review showed no clear efficacy, leading the American College of Gastroenterology to downgrade them in 2025 guidance. Peripherally acting mu-opioid receptor antagonists occupy a specialized OIC niche but endure payer hurdles that limit uptake compared with off-label GC-C alternatives.

By Disease Type: IBS-C Outpaces Chronic Idiopathic Constipation

Opioid-induced constipation retained 34.07% of disease-type value in 2025, yet IBS-C is forecast to sprint ahead at a 9.63% CAGR, the fastest among all indications. Chronic idiopathic constipation remains the largest absolute pool but grows more slowly as patients experiment with diet, fiber supplements, and app-based biofeedback.

Rome IV criteria revisions in 2024 effectively expanded the IBS-C population by lowering the symptom-frequency threshold, enlarging the patient pool for GC-C and 5-HT4 agonists. Prucalopride prescriptions surged 27% in 2025 after pediatric European approval stimulated brand visibility. Neurologic constipation continues to be underserved, reflecting split care pathways between neurology and gastroenterology practices.

By Prescription Type: OTC Gains Traction Despite Regulation

Prescription drugs accounted for 61.92% of sales in 2025, but the OTC category is predicted to grow at an 8.08% CAGR as copayment burdens and prior-authorization delays frustrate patients. The anticipated 2028 generic entry for linaclotide could blur prescription-OTC boundaries, with manufacturers weighing lower-dose OTC switches.

Stronger enforcement against high-risk stimulant combinations modestly curbs OTC growth, yet e-commerce continues to expand its reach: 41% of Amazon Pharmacy laxative buyers in 2025 were first-time purchasers. Private-label products thrive online, capturing a larger slice of category spend than in physical outlets.

By Route of Administration: Oral Dominance Continues

Oral products represented 75.78% of 2025 revenue and are poised to expand at an 8.41% CAGR, faster than the overall constipation treatment market. Taste-masked powders, chewables, and orally disintegrating tablets target swallowing issues and sensory decline in older adults, reinforcing the route’s popularity.

Rectal options occupy acute rescue scenarios, and parenteral products such as subcutaneous methylnaltrexone remain confined to palliative care due to USD 37–42 per-dose costs. The constipation treatment market share for suppositories is inching upward within long-term care as caregivers prioritize predictable evacuation timings.

By Patient Type: Geriatric Growth Outpaces Other Cohorts

Adults accounted for 61.08% of users in 2025, but geriatric patients posted an 8.82% CAGR, eclipsing that of every other group. Institutional protocols often require routine laxatives, creating durable volume streams.

Manufacturers reformulate products with reduced sodium and improved taste to suit cardiovascular comorbidities and sensory decline. Pediatric needs receive renewed attention following the FDA’s 2024 label expansion of polyethylene glycol for infants over six months.

By Distribution Channel: Online Pharmacies Disrupt Traditional Models

Hospital pharmacies controlled 34.78% of 2025 value because of bundled inpatient protocols, yet online and direct-to-consumer services are advancing at a 7.83% CAGR. Retail drugstores, while holding the largest absolute slice, face margin compression and rising private-label penetration.

Price studies show average online OTC prices running 18% below in-store equivalents, intensifying traffic migration. Regulatory warning letters introduce compliance risk, but uneven enforcement allows numerous platforms to operate in a gray zone.

Geography Analysis

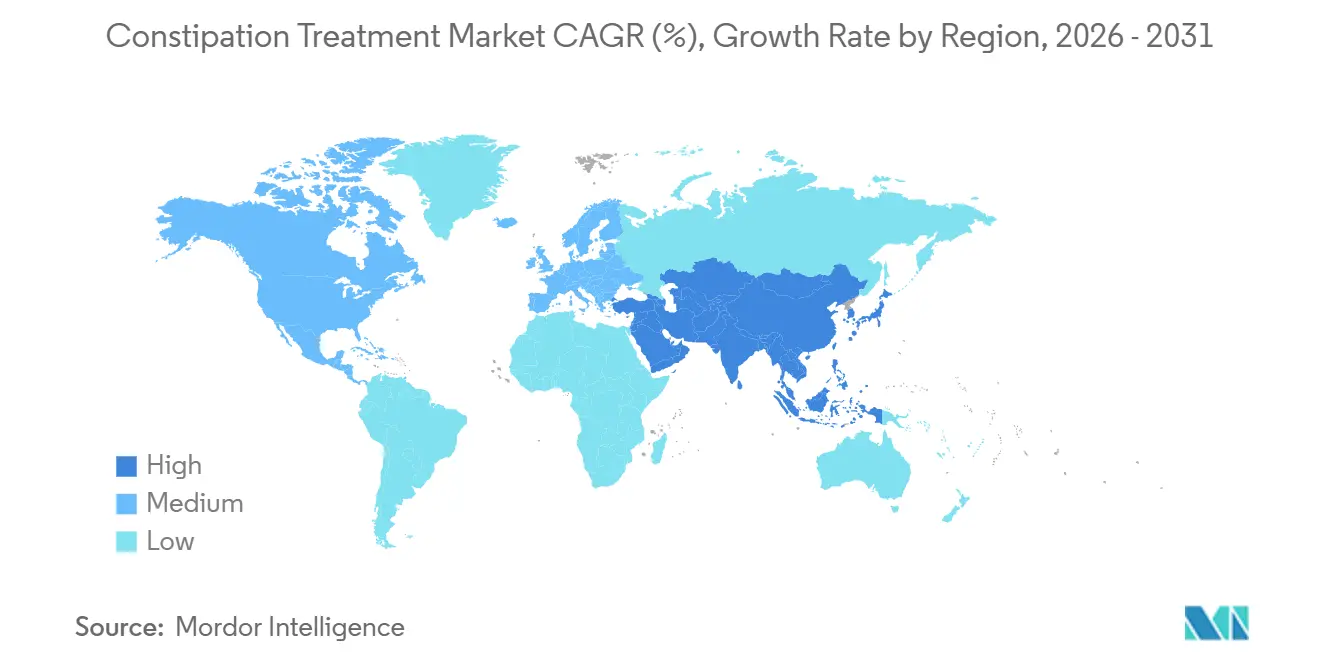

North America captured 39.43% of 2025 revenue on the back of high per-capita health spending and entrenched opioid prescribing that feeds the OIC segment. Canada expanded linaclotide coverage in its two largest provinces during 2024, prompting a 23% rise in prescriptions. Mexico remains bifurcated: metropolitan centers mirror U.S. treatment patterns, while rural areas lean on herbal senna, leaving prescription penetration at 34% of diagnosed cases.

Germany, the United Kingdom, and France supply 62% of regional turnover, but single-payer cost controls push clinicians toward generics. Takeda’s newly approved 5-HT4 agent still awaits favorable price agreements in Italy and Spain, delaying uptake. NICE guidance updates that emphasize fiber and lifestyle adjustment dampen prescription volume in the United Kingdom.

Asia-Pacific posts the fastest regional CAGR at 11.27%. China’s decision to add linaclotide to provincial reimbursement lists in 2024, India’s low-priced generic GC-C launches, and Japan’s super-aged demographic collectively propel growth. Australia’s stimulant pack-size caps inadvertently shift chronic users to prescription items, while South Korea leverages telemedicine to broaden specialist access.

Middle East and Africa together represent a modest 7% share but record steady expansion as Gulf states upgrade health infrastructure. South America grows at 6.9%; Brazil’s approval of plecanatide in 2024 and local generic launches keep prices accessible. Economic volatility in Argentina continues to push consumers toward locally made stimulants.

Competitive Landscape

The constipation treatment market remains fragmented. Mergers and divestitures intensify as patents expire: Grünenthal bought Movantik for USD 250 million in 2024, and Ipsen exited the category by selling Forlax for EUR 350 million in 2025. Multinationals focus on lifecycle management, extending exclusivity through pediatric labels and orally disintegrating formulations, whereas generic players rush bioequivalence filings to seize post-patent share.

Digital therapeutics emerge as non-drug competitors. FDA-cleared biofeedback apps reduce rescue-drug use, prompting incumbents to explore hybrid bundles; Ironwood piloted an adherence-coaching partnership for Linzess in 4 U.S. states in 2025. Patent data show AbbVie and Takeda staking claims in neuromodulators and microbiome modulators, signaling a pivot toward novel pathways with lower risk of electrolyte imbalance.

Smaller biotechs face steep commercialization hurdles. Ardelyx achieved only 12% U.S. formulary coverage for tenapanor by mid-2025, while Evoke Pharma’s asset changed hands for USD 28 million as part of a repositioning gamble. Private-label OTC growth online further erodes pricing power for traditional brands, hastening strategic portfolio pruning.

Constipation Treatment Industry Leaders

Takeda Pharmaceutical Company Ltd

Ironwood Pharmaceuticals, Inc.

AstraZeneca Plc

Sanofi S.A.

Bausch Health Companies Inc. (Salix Pharmaceuticals)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: ANI Pharmaceuticals launched the first generic prucalopride with 180-day exclusivity in the United States, immediately undercutting branded pricing

- June 2024: Nestlé Health Science acquired VOWST, the first oral fecal microbiota product, bolstering its GI portfolio

Global Constipation Treatment Market Report Scope

As per the scope of the report, constipation is a common medical condition that affects an individual's normal life, and prolonged constipation could be a symptom of more severe diseases and disorders. It is estimated to affect every individual once in a lifetime. Constipation may be occasional, lasting for a few weeks, or chronic, lasting longer and recurrent. Therefore, it may be associated with other conditions, such as irritable bowel syndrome or opioid consumption.

The constipation treatment market is segmented by drug class, disease type, prescription type, route of administration, patient type, distribution channel, and geography. By drug class, the market is segmented into bulk forming agents, osmotic agents, stimulant agents, and other drugs. By disease type, the market is segmented into chronic idiopathic constipation (CIC), irritable bowel syndrome with constipation (IBS-C), opioid-induced constipation (OIC), and post-surgical & neurologic Constipation. By patient type, the market is segmented into adult, geriatric, and pediatric. By prescription type, the market is segmented into over-the-counter and prescription drugs. By distribution channel, the market is segmented into hospitals, pharmacies, retail pharmacies, and online pharmacies. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (USD) for the above segments.

| Bulk-Forming Agents |

| Osmotic Agents |

| Stimulant Agents |

| Stool Softeners / Emollients |

| Lubricant Agents |

| Secretagogues (ClC-2, GC-C) |

| Other Drug Classes |

| Chronic Idiopathic Constipation (CIC) |

| Irritable Bowel Syndrome-C (IBS-C) |

| Opioid-Induced Constipation (OIC) |

| Post-surgical & Neurologic Constipation |

| Over-the-Counter (OTC) |

| Prescription Drugs |

| Oral |

| Rectal |

| Parenteral |

| Adult |

| Geriatric |

| Pediatric |

| Hospital Pharmacies |

| Retail / Drug Stores |

| Online Pharmacies & DTC Subscriptions |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Class | Bulk-Forming Agents | |

| Osmotic Agents | ||

| Stimulant Agents | ||

| Stool Softeners / Emollients | ||

| Lubricant Agents | ||

| Secretagogues (ClC-2, GC-C) | ||

| Other Drug Classes | ||

| By Disease Type | Chronic Idiopathic Constipation (CIC) | |

| Irritable Bowel Syndrome-C (IBS-C) | ||

| Opioid-Induced Constipation (OIC) | ||

| Post-surgical & Neurologic Constipation | ||

| By Prescription Type | Over-the-Counter (OTC) | |

| Prescription Drugs | ||

| By Route of Administration | Oral | |

| Rectal | ||

| Parenteral | ||

| By Patient Type | Adult | |

| Geriatric | ||

| Pediatric | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail / Drug Stores | ||

| Online Pharmacies & DTC Subscriptions | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is the constipation treatment market projected to grow to 2031?

It is expected to expand from USD 13.97 billion in 2026 to USD 18.84 billion by 2031 at a 6.17% CAGR.

Which therapy class currently leads revenue?

Stimulant agents held 38.62% of 2025 revenue, topping all other classes.

What drives the strong growth in Asia-Pacific?

Wider reimbursement in China, low-cost generics in India, and Japan’s aging society lift regional demand at an 11.27% CAGR.

Why are over-the-counter laxatives gaining share?

E-commerce pharmacies and subscription bundles lower prices and bypass prior-authorization barriers, pushing OTC volume ahead at an 8.08% CAGR.

Which patient group grows fastest?

Geriatric patients advance at 8.82% annually, fueled by polypharmacy and institutional laxative protocols.

Page last updated on: