Connected Healthcare Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

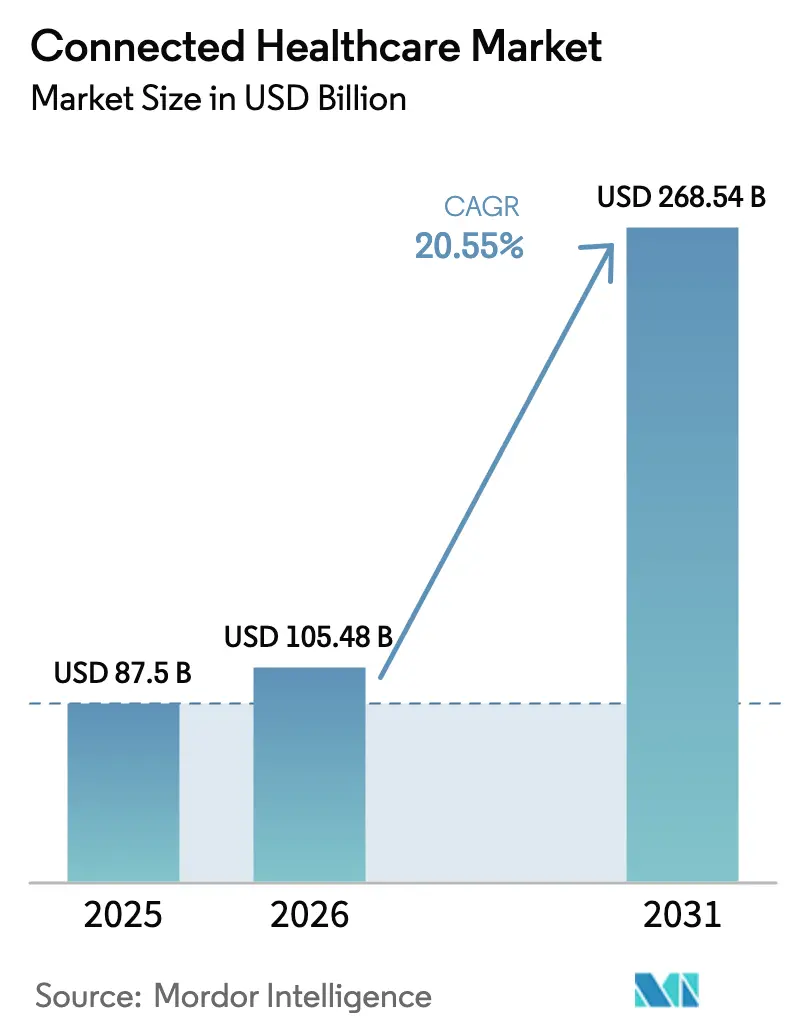

| Market Size (2026) | USD 105.48 Billion |

| Market Size (2031) | USD 268.54 Billion |

| Growth Rate (2026 - 2031) | 20.55% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Connected Healthcare Market Analysis by ���ϲ�����

The Connected Healthcare Market size is projected to be USD 87.5 billion in 2025, USD 105.48 billion in 2026, and reach USD 268.54 billion by 2031, growing at a CAGR of 20.55% from 2026 to 2031.

This rapid climb illustrates how digital care models have moved from niche pilots to system-wide standards, led by telehealth reimbursement and increasing use of artificial intelligence in clinical devices. Health systems now aim for continuous rather than episodic engagement, spurring demand for real-time monitoring platforms, predictive analytics, and interoperable data hubs. Regulatory support for remote patient monitoring, combined with edge-AI hardware innovations, is lowering adoption barriers, while consumer electronics brands keep shifting wellness tracking into clinical decision workflows. At the same time, cybersecurity readiness, clinician workflow redesign, and broadband availability remain gating factors that influence deployment timelines across geographies.

Key Report Takeaways

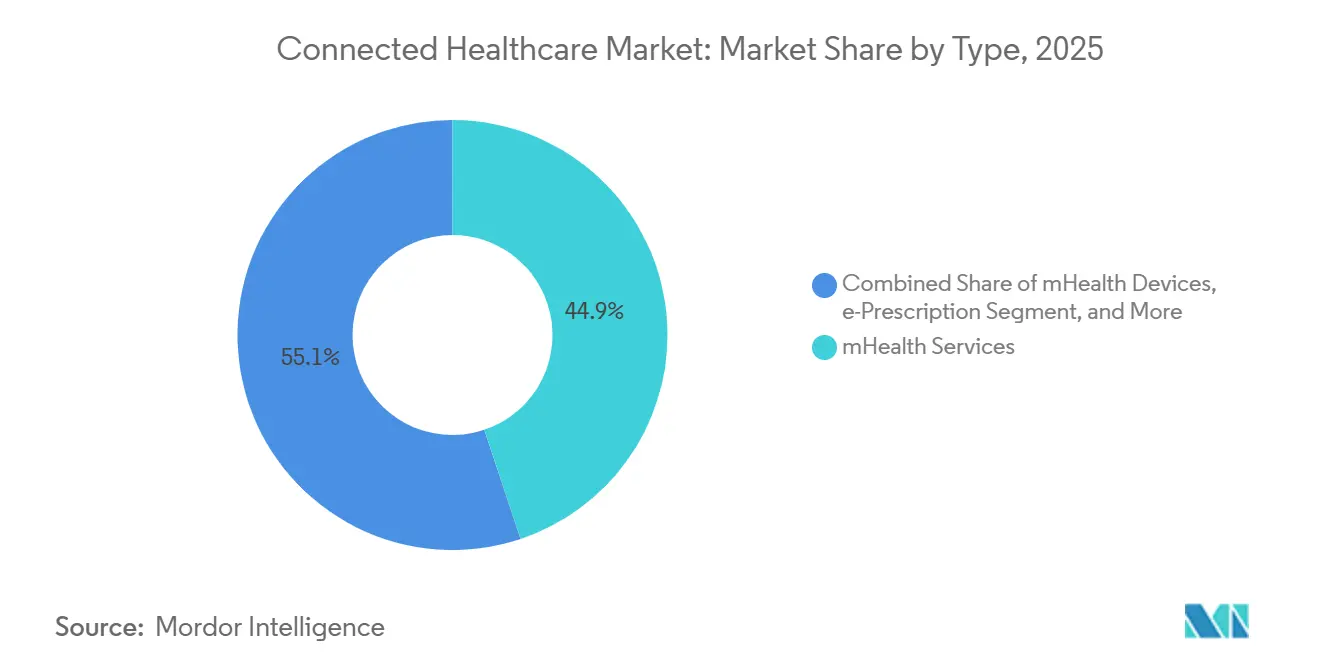

- By type, mHealth Services led the connected healthcare market with a 44.86% share in 2025, while e-prescription is projected to grow at the fastest rate, with a 23.31% CAGR through 2031.

- By function, remote patient monitoring dominated with a 34.78% share and also recorded the highest growth rate of 21.92% CAGR.

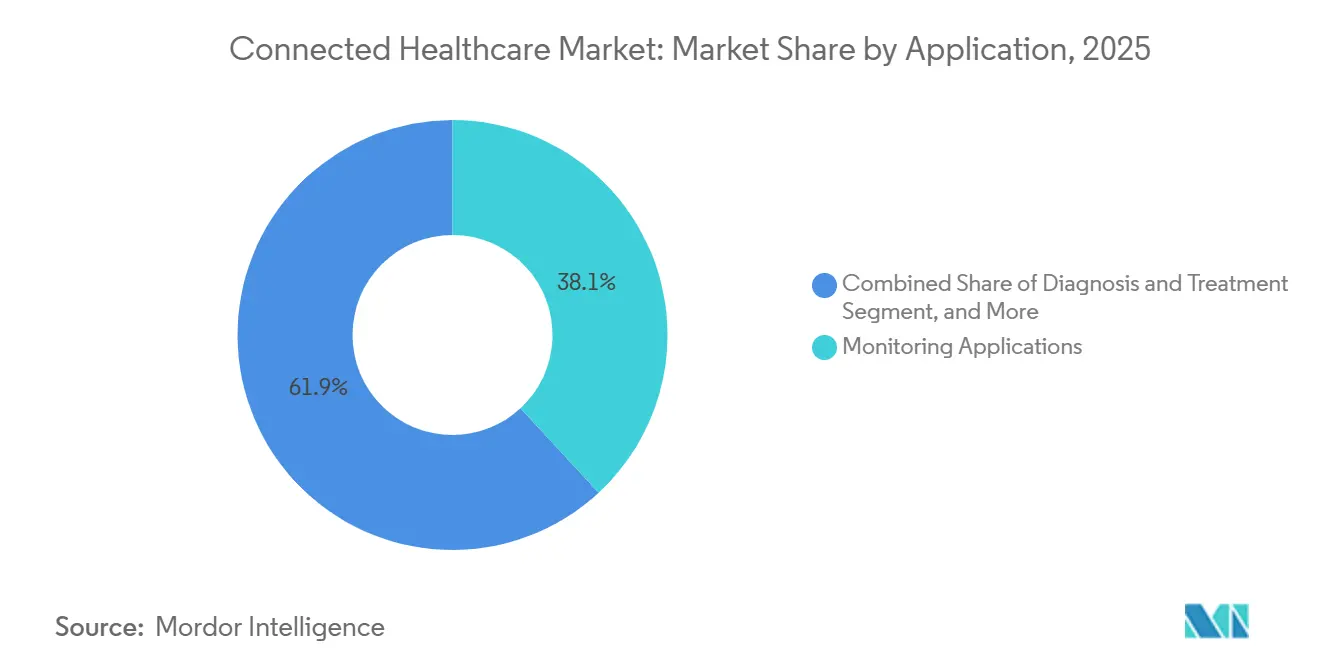

- By application, monitoring applications accounted for the largest share at 38.10%, whereas wellness & prevention is set to expand most rapidly at 22.05% CAGR.

- By end user, hospitals and clinics remained the top users with a 46.45% market share, while home monitoring is on the fastest trajectory with a 21.74% CAGR.

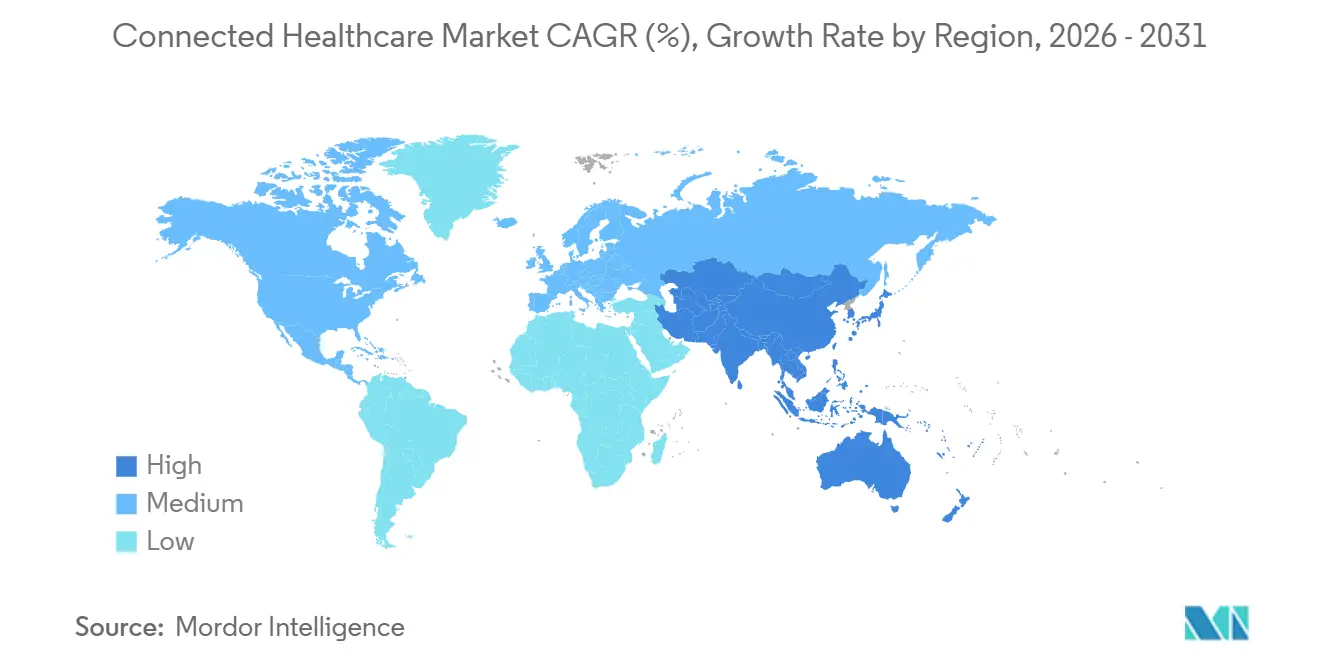

- By geography, North America contributed the highest revenue share of 41.31%, while Asia-Pacific is forecast to grow at the fastest pace of 22.98% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Connected Healthcare Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rapid telehealth adoption | +4.2% | Global, strongest in North America and Europe | Short term (≤ 2 years) |

| Rising chronic disease burden | +5.8% | Global, pronounced in aging populations in North America, Europe, and Asia-Pacific | Long term (≥ 4 years) |

| Government reimbursement push for RPM | +3.9% | North America and select European markets adhering to value-based care | Medium term (2-4 years) |

| Edge-AI chips enable on-device analytics | +3.1% | Asia-Pacific core, spillover to North America and Europe due to data-sovereignty mandates | Medium term (2-4 years) |

| Hospital Private 5G Networks Accelerate Imaging | +2.40% | North America & EU early adopters | Long term (≥ 4 years) |

| Consumer Tech APIs Spur Interoperability | +1.80% | Global, led by North America | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Rapid Telehealth Adoption

Pandemic-era virtual visit volumes soared by 766%, creating permanent patient expectations for on-demand consultations. Medicare has formalized audio-only and home-based telehealth coverage through March 2025, cementing virtual care as a standard benefit.[1]U.S. Department of Health and Human Services, “Telehealth Flexibilities for 2025,” hhs.gov Consequently, 70% of health systems in the AVIA Network now deploy remote patient monitoring solutions, mainly for chronic disease cohorts. Vendor ecosystems are expanding beyond video consults; Epic added ambient AI documentation to streamline visit notes and improve clinician productivity. The connected healthcare market benefits as providers integrate scalable, secure telehealth stacks to support longitudinal patient management.

Rising Chronic Disease Burden

Half of the U.S. population lives with at least one chronic condition, consuming 86% of national healthcare spending. Remote monitoring programs can save USD 5.2 million annually for every 500 high-risk Medicare beneficiaries through fewer readmissions. Kaiser Permanente’s program, which covers 45,000 members, illustrates the clinical and economic gains achievable through continuous monitoring.[2]Kaiser Permanente, “Remote Patient Monitoring Outcomes,” kaiserpermanente.org In Utah, home telemetry reduced average HbA1c from 9.73% to 7.81% and lowered systolic blood pressure from 130.7 mmHg to 122.9 mmHg, confirming improvements in outcomes.[3]Diabetes Technology & Therapeutics, “Utah Remote Monitoring Project,” diabetesjournals.org Asia-Pacific’s ageing demographics and rising diabetes prevalence are expanding the patient pool, aligning with USD 20 trillion in cumulative elderly-care spend projections to 2030.

Government Reimbursement Push for RPM

The Centers for Medicare & Medicaid Services added dedicated CPT codes that reimburse for at least 16 days of physiologic data capture within a 30-day cycle, providing providers with predictable revenue for remote monitoring. Rural Health Clinics and Federally Qualified Health Centers now receive separate RPM payments, which helps narrow access gaps in underserved regions. Europe is following with broader coverage for digital therapeutics, creating a synchronized global policy environment that accelerates vendor scaling across continents.

Edge-AI Chips Enable On-Device Analytics

Organic electrochemical transistors developed at the University of Hong Kong showcase medical-grade edge processors that analyze biosignals locally, improving latency and privacy. FDA clearance of LifeSignals’ wearable biosensor and Masimo’s medical watch highlights regulatory comfort with edge-AI devices. GE HealthCare’s foundation models optimized on NVIDIA platforms enable faster image assessment within scanners, reducing cloud load and reliance on the network. Neuromorphic processors such as BrainChip’s Akida and Microchip’s BioGAP-Ultra execute inference locally on milliwatt budgets, eliminating dependence on cloud GPUs and satisfying European and Chinese data-residency rules.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Cyber-Security & Data-Privacy Concerns | -2.80% | Global, with EU GDPR compliance | Short term (≤ 2 years) |

| High Integration & Capital Costs | -2.10% | Global, acute in emerging markets | Medium term (2-4 years) |

| Clinician Alarm Fatigue | -1.40% | North America & EU primary | Medium term (2-4 years) |

| Rural Bandwidth Inequality | -1.90% | Global, severe in rural areas | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Cyber-Security & Data-Privacy Concerns

Average breach costs climbed to USD 10.1 million in 2024 as 67% of providers reported at least one security event. India ranks among the top five most attacked healthcare systems, illustrating global exposure. The Biden administration plans substantial increases to the HHS cybersecurity budget, and the FDA now mandates security documentation for device clearance. In 2024, the healthcare industry recorded the highest breach costs, reaching USD 10.93 million per incident. A ransomware attack on Change Healthcare in February 2024 disrupted claims processing for 100 million patients and resulted in a financial impact of USD 2.3 billion for UnitedHealth. In May 2024, a cyberattack on Ascension Health forced 140 hospitals to operate on paper workflows for three weeks. Each connected bed supports 15 to 20 networked devices, significantly increasing potential attack vectors.

High Integration & Capital Costs

Replacing Electronic Health Record (EHR) systems costs USD 50,000 to USD 500,000 per provider and has a break-even period of approximately 7 years. This creates a significant barrier to adopting new platforms. Clinicians often navigate between three to five applications during a single patient encounter, underscoring the limited interoperability between monitoring feeds and core EHR systems. By the end of 2024, only 38% of U.S. hospitals had implemented patient-facing FHIR APIs, despite regulatory mandates under the 21st Century Cures Act. Integration backlogs are delaying the deployment of Remote Patient Monitoring (RPM) programs, which typically require 18 to 24 months to achieve cost savings sufficient to offset investments in devices and staffing. This extended timeline often exceeds the tenure of many Chief Financial Officers (CFOs). Furthermore, vendor lock-in increases switching costs, as proprietary data models make transitioning to interoperable alternatives difficult.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: E-Prescription Adoption Climbs

mHealth Services captured 44.86% connected healthcare market share in 2025, reflecting how enterprise telehealth suites and patient portals matured from pandemic triage tools into core clinical infrastructure. Integrated platforms like Epic MyChart now deliver secure messaging, photo triage, automated refill requests, and AI-driven care navigation inside a single workflow. Growth continues as health systems expand remote case management, device integration, and personalized engagement features to support at-home chronic care plans, solidifying the segment’s lead in the connected healthcare market.

The e-Prescription and mHealth Development category, while smaller, is set to grow at a 23.31% CAGR through 2031. Regulatory support for electronic prescribing, including controlled substances, and rising demand for API-based medication reconciliation underpin the momentum. Cloud development kits allow hospitals to add institution-specific apps that read or write EHR data, enhancing revenue diversification. Innovations such as real-time benefits checks and price-transparency tools make digital prescribing central to medication-adherence strategies.

By Function: RPM Leads in Share and Growth

Telemedicine maintained a 27.95% functional share in 2025 thanks to sustained virtual consult volumes, yet Remote Patient Monitoring is outpacing with a 21.92% CAGR. Cardiology and endocrinology programs illustrate the impact: devices transmit daily vitals and glucose metrics, while AI triage surfaces exceptions for nurse review, allowing clinicians to oversee larger populations without proportional staffing growth. FDA authorization of the Cordella Pulmonary Artery Sensor System for heart-failure home use expands the scope of physiological markers captured outside hospitals.

Clinical Monitoring and ancillary functions grow steadily as vendors bundle multi-parameter sensors with decision-support software. Philips and Mass General Brigham are building real-time data fabrics that pull ECG, capnography, and hemodynamic waveforms into a unified analytics layer, shortening alert-to-intervention windows. These integrations reinforce the trend in the connected healthcare market toward comprehensive, continuous oversight.

By Application: Wellness & Prevention Gains Pace

Monitoring Applications controlled 38.10% of revenue in 2025, owing to long-established disease-specific platforms for diabetes and cardiac care. However, Wellness and prevention are forecast to expand at a 22.05% CAGR as consumers adopt wearables that record sleep, activity, and metabolic signals, which clinicians increasingly accept as adjunct data. Google’s Personal Health Insights Agent analyzes multimodal wearable data to deliver personalized coaching, while Samsung’s noninvasive glucose technology positions consumer devices as early risk-screening tools.

Diagnosis & Treatment applications also benefit from AI advances. GE HealthCare’s partnership with NVIDIA yields autonomous imaging pipelines that automatically segment, label, and prioritize radiographs, shortening time-to-diagnosis in resource-constrained settings. Healthcare Management applications evolve as EHR vendors add staffing optimization, inventory analytics, and revenue-cycle AI modules, creating a continuum from operational to clinical intelligence within the connected healthcare market.

By End User: Home Settings Accelerate

Hospitals & Clinics contributed 46.45% revenue in 2025 as they remain the primary purchasers of regulated devices and enterprise software. Yet Home Monitoring shows the fastest path at 21.74% CAGR as payers adopt hospital-at-home reimbursement and the FDA promotes its Health Care at Home pathway. Continuous vital sign sensors, Bluetooth-enabled scales, and AI chatbots extend care teams into patient living rooms, shifting acute interventions toward earlier community-based management.

Ambulatory and specialty Clinics embrace digital-first visits, with Vizient projecting 15.4% outpatient volume growth through 2034 as the site of care shifts from inpatient wards to procedure-focused centers. Laboratories integrate remote sample collection, tracking, and device-generated physiologic data to offer diagnostic insights contextualized within longitudinal vital sign trends.

Geography Analysis

North America held a 41.30% share of the connected healthcare market in 2025, owing to Medicare’s broad telehealth coverage, the efficiency of FDA device clearance, and strong venture funding pipelines. The region benefits from widespread insurer alignment on remote monitoring reimbursement, high broadband penetration, and robust cybersecurity frameworks that encourage enterprise-level deployments. U.S. hospitals continue to expand hybrid care strategies combining virtual triage, home diagnostics, and AI-assisted imaging, which sustains regional revenue leadership.

Asia-Pacific is the fastest-expanding region, forecast to grow at 22.98% CAGR between 2026 and 2031. China anchors regional momentum with venture investment reaching USD 6.3 billion in 2018 and continued public–private support for digital health pilots, such as 5G-enabled surgical mentoring. India’s insurance-funded telehealth integration and digital health law rollouts support scalable care pathways reaching rural populations. Thailand’s Siriraj Hospital cut pathology turnaround from 15 minutes to 25 seconds via 5G-linked AI microscopes, illustrating leapfrog benefits where advanced networks combine with clinician shortages.

Europe shows moderate progress, with reimbursement varying by country, yet the European Health Data Space proposal promises unified governance that would boost cross-border telehealth and AI device adoption. Nordic nations already reimburse home spirometry in chronic obstructive pulmonary disease, while Germany’s DiGA program lists more than 50 prescribed digital therapeutics. The Middle East and Latin America expand slowly from pilot projects as bandwidth, security frameworks, and payer models mature.

���ϲ����� provides coverage of the connected healthcare market across other key regional markets. Detailed country-level analysis extends to Indonesia incorporating local coverage and market participation, as required.

Competitive Landscape

The connected healthcare market remains moderately fragmented. Traditional device leaders like Philips, GE HealthCare, and Medtronic couple sensor know-how with software-as-a-service business models to defend installed bases. Technology giants such as Apple, Google, and Samsung leverage consumer ecosystems to generate continuous data streams that feed into clinical APIs, eroding boundaries between wellness and medical applications. Their ruggedized consumer wearables increasingly hold FDA clearance, boosting credibility within hospital procurement cycles.

Strategic partnerships dominate. Medtronic joined Philips in integrating Nellcor oximetry and Microstream capnography into Philips bedside monitors, creating bundled value for multi-parameter surveillance. Samsung purchased Xealth to pipe third-party digital therapeutics into clinician workflows across more than 500 hospitals, illustrating platform-centric competitive tactics. GE HealthCare’s seven-year imaging alliance with Sutter Health targets statewide AI deployment, while its NVIDIA collaboration accelerates autonomous X-ray triage.

AI-native contenders raise significant capital, leading to USD 23 billion in healthcare AI funding during 2024, with nearly one-third earmarked for diagnostic imaging and clinical decision support. Incumbent EHR vendor Epic expands into enterprise resource planning and clinical AI modules to protect its share as cloud-first disruptors gain traction.

Connected Healthcare Industry Leaders

Koninklijke Philips NV

Medtronic Plc

GE HealthCare Technologies Inc.

International Business Machines Corporation

Cisco Systems, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: An AI-based home-monitoring platform launched in India, letting physicians track patients continuously outside hospitals.

- January 2026: LiverRight, the national virtual clinic for liver disease, introduced contactless RPM during telemedicine appointments.

- July 2025: Samsung Electronics acquired Xealth, integrating 70 digital-health solutions across 500 hospitals.

- March 2025: GE HealthCare unveiled the Genesis cloud-imaging suite and partnered with NVIDIA on autonomous scanning algorithms.

Global Connected Healthcare Market Report Scope

As per the scope of the report, connected healthcare (or connected health) is a patient-centered, technology-driven model that uses digital tools such as wearables, mobile apps, and sensors to connect patients with clinicians, enabling remote care, real-time monitoring, and data sharing. It moves care from reactive, in-person visits to proactive, continuous management.

The connected healthcare market is segmented by type, function, application, end user, and geography. By type, the market is segmented into mHealth Services, mHealth Devices, and e-Prescription. By function, the market is segmented into Remote Patient Monitoring, Clinical Monitoring, Telemedicine, and Others. By application, the market is segmented into Diagnosis & Treatment, Monitoring Applications, Wellness & Prevention, Healthcare Management, and Others. By end user, the market is segmented into Hospitals & Clinics, Home Monitoring, Ambulatory & Specialty Clinics, and Research & Diagnostic Laboratories. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle-East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers market size and forecasts in value (USD) for the above segments.

| mHealth Services |

| mHealth Devices |

| e-Prescription |

| Remote Patient Monitoring |

| Clinical Monitoring |

| Telemedicine |

| Others |

| Diagnosis & Treatment |

| Monitoring Applications |

| Wellness & Prevention |

| Healthcare Management |

| Others |

| Hospitals & Clinics |

| Home Monitoring |

| Ambulatory & Specialty Clinics |

| Research & Diagnostic Laboratories |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | mHealth Services | |

| mHealth Devices | ||

| e-Prescription | ||

| By Function | Remote Patient Monitoring | |

| Clinical Monitoring | ||

| Telemedicine | ||

| Others | ||

| By Application | Diagnosis & Treatment | |

| Monitoring Applications | ||

| Wellness & Prevention | ||

| Healthcare Management | ||

| Others | ||

| By End User | Hospitals & Clinics | |

| Home Monitoring | ||

| Ambulatory & Specialty Clinics | ||

| Research & Diagnostic Laboratories | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the connected healthcare market?

The connected healthcare market size is USD 105.48 billion in 2026.

How fast is the connected healthcare market expected to grow?

It is forecast to register a 20.55% CAGR, reaching USD 268.54 billion by 2031.

Which segment holds the largest connected healthcare market share?

MHealth Services accounted for 44.86% revenue share in 2025.

Which region is expanding the quickest in connected healthcare?

Asia-Pacific is projected to post a 22.98% CAGR between 2026 and 2031, the highest among all regions.

Why is remote patient monitoring gaining momentum?

RPM lowers readmissions and supports chronic care efficiencies, saving around USD 5.2 million per 500 high-risk Medicare patients annually.

What are the main challenges to wider connected healthcare adoption?

Cybersecurity risks and rural bandwidth limitations represent the most significant headwinds.

Page last updated on: