Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

| Market Size (2026) | USD 64.18 Billion |

| Market Size (2031) | USD 92.44 Billion |

| Growth Rate (2026 - 2031) | 6.90% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Mexico Commercial Real Estate Market Analysis by ���ϲ�����

The Mexico commercial real estate market size is USD 64.18 billion in 2026 and is projected to reach USD 92.44 billion by 2031, registering a 6.9% CAGR. The Mexico commercial real estate market is pivoting from greenfield development to asset recycling as global firms favor portfolio acquisitions and turnkey capacity over new builds, despite headline FDI highs. New greenfield capital commitments fell to USD 3.17 billion in 2024, even as total FDI reached USD 36.87 billion, a mismatch that pushes demand toward pre-certified facilities and away from raw land. Logistics leads on both scale and growth as e-commerce penetration surpasses 84% and last‑mile fulfillment reshapes specifications in dense metro corridors. Occupancies near 98% in organized industrial parks and elongated permitting windows in top corridors increase the pricing power of developers who banked inventory during 2022 to 2024 and raise barriers for late entrants. Demand patterns also show a tilt to rentals as financing tightens and affordability strains persist, with households emerging as the fastest-growing end‑user while corporates and SMEs continue to dominate absorption.[1]https://www.imf.org/en/home

Key Report Takeaways

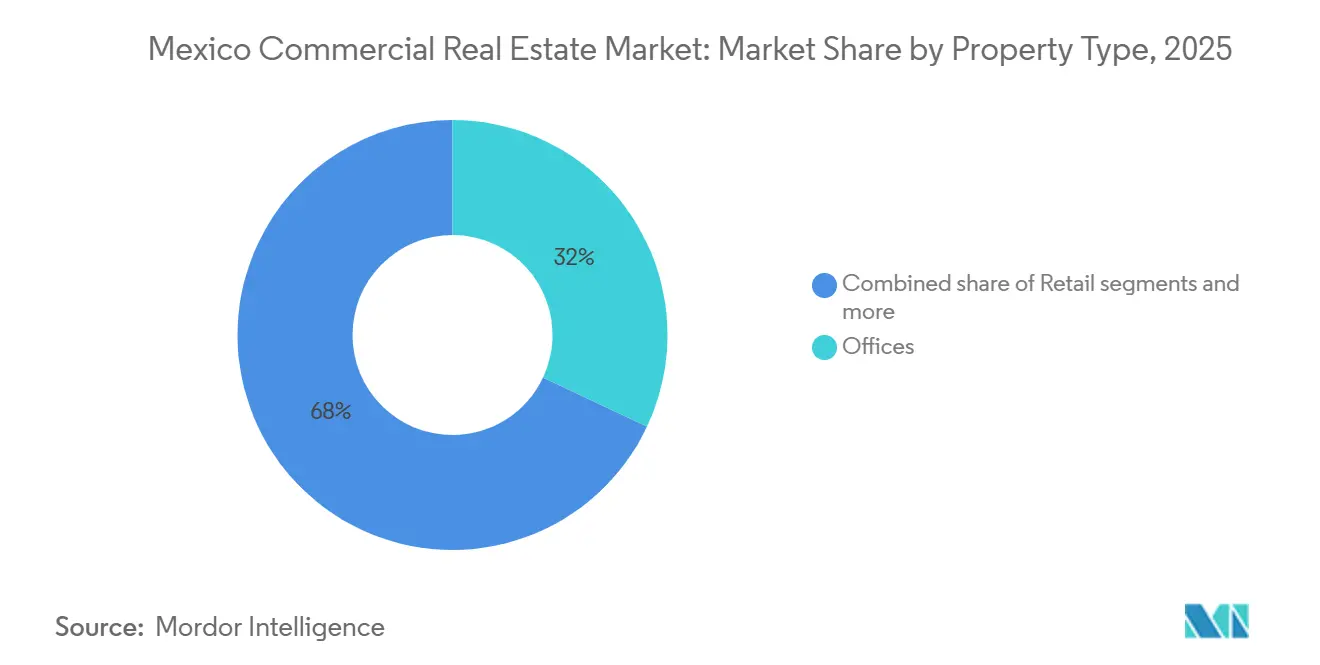

- By property type, logistics led with a 33.22% revenue share in 2025, and logistics is forecast to expand at an 8.1% CAGR to 2031.

- By business model, the sales segment held 68.44% of the Mexico commercial real estate market share in 2025, while rental posted the highest projected CAGR at 7.55% through 2031.

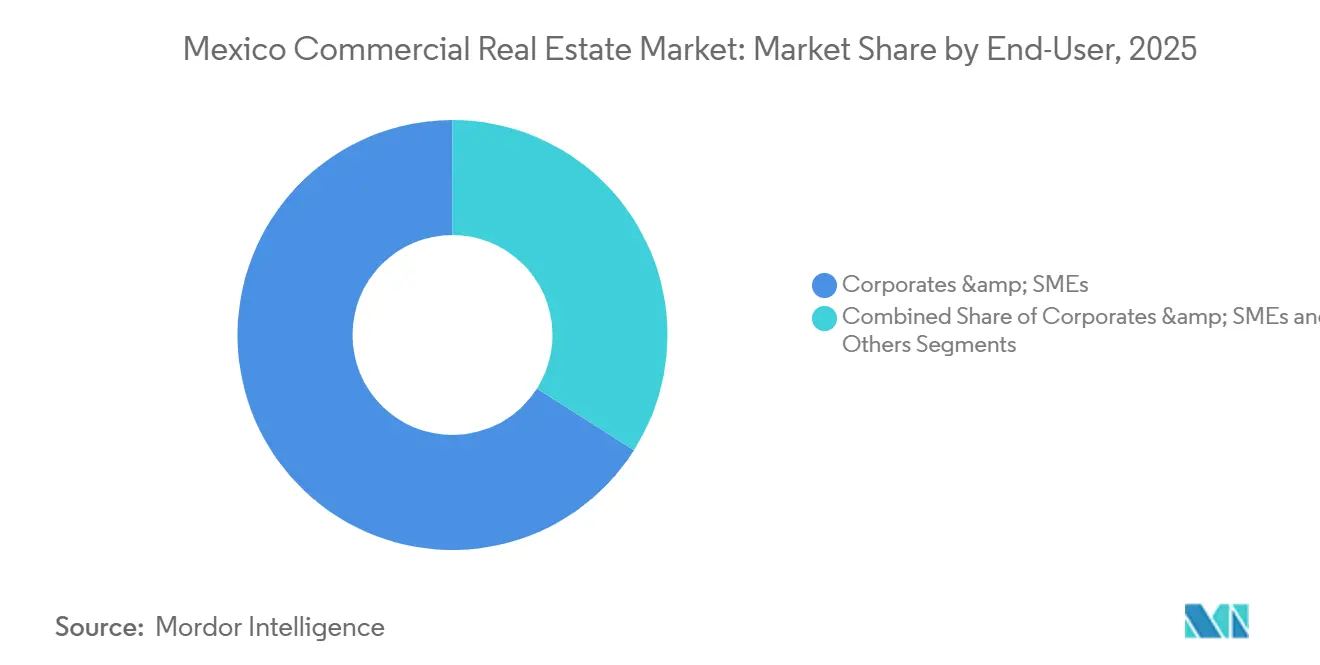

- By end‑user, corporates and SMEs accounted for a 71.45% share of the Mexico commercial real estate market size in 2025, and individuals and households are advancing at a 7.77% CAGR through 2031.

- By geography, Mexico City captured 24.33% in 2025, while Querétaro is forecast to expand at a 7.33% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Mexico Commercial Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Nearshoring‑Induced Industrial Demand Along The US–Mexico Border | +2.1% | Nuevo León, Baja California, Chihuahua, Coahuila, Tamaulipas | Medium term (2-4 years) |

| Expansion Of Data‑Centre Investments Fuelled by Fiber Upgrades | +1.8% | Querétaro, Monterrey, Guadalajara | Medium term (2-4 years) |

| E‑Commerce Growth Boosting Last‑Mile Logistics Space | +1.3% | Mexico City, Guadalajara, Monterrey, national metro corridors | Short term (≤ 2 years) |

| Peso Stability Attracting Foreign Institutional Investors to Offices | +0.9% | Mexico City CBD, Monterrey | Long term (≥ 4 years) |

| Rapid Urbanization of The Bajío Region Driving Mixed-Use Developments | +0.8% | Querétaro, Aguascalientes, Guanajuato, San Luis Potosí | Medium term (2-4 years) |

| PPP Transportation Corridors Lifting Retail Footfall in Secondary Cities | +0.5% | Bajío region, Mérida, Cancún | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Nearshoring Induced Industrial Demand along the US–Mexico Border

Mexico sustains top‑tier trade integration with the United States through 2025, and manufacturers seeking North American proximity prioritize turnkey capacity that accelerates time to operation. Greenfield flows lag, with new capital commitments at USD 3.17 billion in 2024 versus a record USD 36.87 billion total FDI, which channels leasing and acquisition demand into existing parks. Surveys indicate electricity and water shortfalls across organized industrial sites, so the Mexico commercial real estate market rewards developers who secured power and permits in advance. In Nuevo León, large announced projects face grid and permitting hurdles, reinforcing pre‑certified parks as the default landing zone for incoming tenants. The pending 2026 USMCA review tempers construction starts as firms seek clarity on rules of origin and tariff risks before locking capital, yet inquiry pipelines along border states remain strong for build‑to‑suit and ready‑to‑occupy products.[2]https://practiceguides.chambers.com/practice-guides/real-estate-2025/mexico/trends-and-developments

Expansion of Data‑Centre Investments Fuelled by Fiber Upgrades

Querétaro concentrates an estimated 65% of Mexico’s installed data‑center capacity, with multi‑billion‑dollar commitments from hyperscalers shaping power and connectivity buildouts. New routes like a diverse DWDM path between Querétaro and Monterrey improve redundancy, while private substations and regulatory fast‑tracking aim to ease grid constraints. AI workloads magnify energy intensity, so developers hedge with power‑adjacent sites and scalable interconnection in Monterrey as an overflow. The Mexico commercial real estate market now prices a digital‑adjacency premium for industrial land near these clusters. Pre‑leasing patterns and campus expansions show that data infrastructure is a durable, cross‑cycle driver of industrial and logistics valuations.[3]https://www.mdcdatacenters.com/

E‑Commerce Growth Boosting Last‑Mile Logistics Space

Online retail adoption crossed 84% in 2024, and parcel volumes during national promotions stress last‑mile capacity, pushing tenants to seek automation‑ready urban‑edge warehouses. The Mexico commercial real estate market sees higher premiums for facilities with high clear heights, heavy floor loads, and pre‑installed automation rails that shorten commissioning times. Operators scaling nationwide coverage demonstrate that self‑operated hubs paired with franchise logistics can lift service quality and reduce delivery times. These performance targets shift leasing from pure square‑meter metrics to technology readiness and energy resilience, such as solar‑ready roofs and smart inventory systems. Landlords that deliver plug‑and‑play layouts with embedded intelligence capture lease spreads over conventional stock.

Peso Stability Attracting Foreign Institutional Investors to Offices

Currency stabilization through mid‑2025 improves visibility for dollar‑denominated capital, supporting renewed interest in Mexico City’s Class A assets. Office absorption reached 175,000 square meters during the first three quarters of 2025, with technology, transport, and media tenants driving activity and a three‑days‑in workweek gaining traction. Premium towers with ESG credentials, wellness amenities, and flexible floorplates capture the bulk of demand while secondary submarkets trail. Pre‑leasing in key corridors tightens future availability and yields in the 7% to 8% range remain attractive against regional benchmarks. This bifurcation repositions trophy assets as core allocations for cross‑border investors within the Mexico commercial real estate market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Banxico’s Tight Monetary Stance Raising Borrowing Costs | -1.4% | National, acute in Mexico City and Monterrey | Short term (≤ 2 years) |

| Prolonged Zoning Approval Timelines in Mexico City Metro Area | -0.8% | Mexico City, Estado de México and adjacent municipalities | Medium term (2-4 years) |

| Construction‑Input Inflation Compressing Development Margins | -0.7% | National, steepest in Mexico City | Short term (≤ 2 years) |

| Security Concerns in Northern States Deterring International Tenants | -0.6% | Chihuahua, Sinaloa, Tamaulipas logistics routes | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Banxico’s Tight Monetary Stance Raising Borrowing Costs

Policy rates have moved lower since 2024, yet lending conditions remain tight, and spreads stay elevated, which constrains new development starts. Construction credit contracted in 2024 even as headline monetary easing progressed, reflecting bank risk repricing after large federal project cycles rolled off. Mortgage rates around 10.3% through mid‑2025 signal a wide gap from policy rates and caution lenders maintain in underwriting. For developers, all‑in debt costs near high single digits compress project returns and shift the Mexico commercial real estate market toward stabilized, income‑producing assets. ESG‑linked facilities offer modest funding advantages, favoring platforms with certified portfolios and scale.

Prolonged Zoning Approval Timelines in Mexico City Metro Area

Permitting in the capital region often takes 12 to 18 months, which doubles the wait relative to faster jurisdictions and adds soft costs that erode returns. New environmental and circularity compliance requirements scheduled for enforcement in 2025 introduce added documentation and certification fees. Smaller developers bear disproportionate burdens, which pushes some activity to neighboring municipalities where approvals move faster but tenant demand is thinner. The result is a spatial mismatch as occupiers prefer core submarkets while buildable sites cluster on the periphery. This friction keeps the Mexico commercial real estate market tight in core corridors and supports rent premiums for ready‑to‑occupy assets.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Type: Logistics Anchors Portfolio Velocity, Data Centers Redefine Industrial

Logistics held 33.22% of the Mexico commercial real estate market share in 2025 and is forecast to expand at an 8.1% CAGR through 2031, the strongest pace among property types. The Mexico commercial real estate market benefits from e‑commerce penetration above 84%, which moves tenant demand toward urban‑edge micro‑fulfillment and high‑throughput hubs. Specifications such as 12‑meter clear heights, heavy floor loads, and pre‑installed automation rails shorten commissioning and support light assembly, labeling, and quality control. Querétaro’s concentration of data centers adds a power‑intensive category of “digital warehouses,” altering rent and cap‑rate benchmarks for nearby industrial corridors. Occupancies near 98% in organized industrial parks and 12 to 18‑month permitting windows tilt pricing power to owners who banked inventory from 2022 to 2024, while late entrants face high land costs and delayed approvals. The Mexico commercial real estate market size for logistics is projected to expand at an 8.1% CAGR between 2026 and 2031, driven by last‑mile density needs and pre‑leased hyperscale campuses that anchor broader industrial ecosystems.

Data‑center activity reinforces the logistics‑industrial continuum as power and fiber drive site selection and pre‑leasing decisions. A second fully diverse DWDM route linking Querétaro and Monterrey improves redundancy and positions Monterrey as an overflow node if power constraints bind in Querétaro. Developers that secure private substations and long‑term power agreements gain a leasing edge with cloud and AI tenants, while traditional warehouses command premiums when they are solar‑ready and automation‑ready. Office and retail trails logistics on growth but show signs of stabilization in core corridors, with amenity‑rich, ESG‑certified towers in Mexico City enjoying high occupancy and stronger rent resilience. The Mexico commercial real estate industry, in turn, adopts mixed‑use integration where campus amenities, wellness, and flexible workspaces support diversified cash flows for landlords.

By Business Model: Rental Gains Share as Affordability Crisis Redirects Capital

Sales accounted for 68.44% of market value in 2025, but its growth outlook at 6.9% CAGR trails rental, which is set to grow at 7.55% annually through 2031. Elevated spreads between policy rates and mortgage rates, tighter underwriting, and high transaction costs encourage occupiers to lease longer and defer purchases. Office landlords in Mexico City shift to longer tenures with inflation‑linked escalators and higher tenant improvement packages to lower entry costs and attract fast‑growing tech and services tenants. Industrial developers add power‑purchase agreements and rooftop solar to leases, bundling energy with space to secure longer commitments and stabilize cash flows. The Mexico commercial real estate market reflects this rotation as institutional investors favor platforms with recurring rental income and scaled property management capabilities.

Three reinforcing effects sustain rental’s lead on growth near term. First, developers who can no longer pencil attractive unlevered returns under higher input costs prefer to build‑to‑lease for credit tenants rather than build‑to‑sell. Second, fractional and exchange‑traded vehicles continue to attract retail capital into listed structures instead of direct acquisitions, enhancing liquidity and lowering minimums for investors. Third, city‑level rental reforms standardize lease terms and encourage formalization, which reduces default risk and draws more institutional landlords. The Mexico commercial real estate industry responds with portfolio strategies that prioritize stabilized occupancy, ESG credentials, and tenant retention in core submarkets.

By End‑User: Corporates Dominate Absorption, Households Post Steepest Growth

Corporates and SMEs captured 71.45% of end‑user demand in 2025 as industrial parks operated near full occupancy, and Mexico City’s core submarkets led office absorption. Tenants with export mandates prioritize certified parks that align with customs and tax programs, which favors professional developers with regulatory expertise and scale. Technology firms drive a large share of office take‑up and require fiber‑rich buildings, flexible floorplates, and building‑level ESG adherence. The Mexico commercial real estate market sees concentrated activity in trophy corridors where these specifications are standard, while secondary submarkets lag. Occupier decisions emphasize energy reliability and compliance, which sustains the premium for certified campuses and lowers churn.

Individuals and households post the fastest CAGR at 7.77% through 2031 as affordability constraints redirect demand into formal rental. Social‑leasing initiatives and urban migration to industrial corridors add momentum in major metros and fast‑growing Bajío cities. Renters favor smaller units near employment centers, and new stock attempts to balance yield with accessibility in submarkets with improved transit or proximity to large parks. The Mexico commercial real estate industry adapts by layering co‑living, serviced apartments, and mixed‑use formats to serve this demand without diluting asset quality. Policy and incentive zones along the borders keep corporate demand anchored, which indirectly supports rental housing in surrounding municipalities.

Geography Analysis

Mexico City accounts for 24.33% of the market value in 2025 and concentrates the largest tech workforce in Latin America, which supports office absorption and mixed‑use strength. Class A towers with ESG credentials and wellness amenities maintain near‑full occupancy even as citywide vacancy remains higher due to obsolescence in secondary stock. New supply under construction shows meaningful pre‑leasing, and return‑to‑office norms at three or more days per week stabilize tenant footprints. High permitting friction keeps the Mexico commercial real estate market tight in core corridors, which sustains pricing power for ready‑to‑occupy assets. Developers enhance building value with amenities and flexible workspaces that support community and retention in the Central Business District.

Border‑adjacent Nuevo León leads in industrial construction and is a prime gateway for nearshoring tenants, though energy and water constraints limit the pace of delivery. Very high park occupancy and rail enhancements strengthen the state’s connectivity and positioning for logistics and manufacturing. Guadalajara benefits as a secondary tech hub with lower office vacancy than the capital and a more balanced supply pipeline. The Mexico commercial real estate market distributes demand across these metros as tenants calibrate rent, power availability, and labor pools. Estado de México absorbs overflow from the capital but trades lower land costs against longer approvals and weaker transit links.

Querétaro records the fastest growth with a 7.33% CAGR on the back of hyperscale data‑center campuses and a dense fiber backbone. The state’s installed base shapes industrial land valuations as sites near existing campuses command digital‑adjacency premiums. Power constraints are the key systemic risk and could redistribute future investments to Monterrey or Guadalajara if grid expansion lags workload growth. The Mexico commercial real estate market size attribution reflects this concentration as Querétaro captures a growing slice of new industrial commitments while Mexico City remains the largest node by value. Secondary Bajío cities advance as improved corridors expand catchment areas for retail and mixed‑use developments.

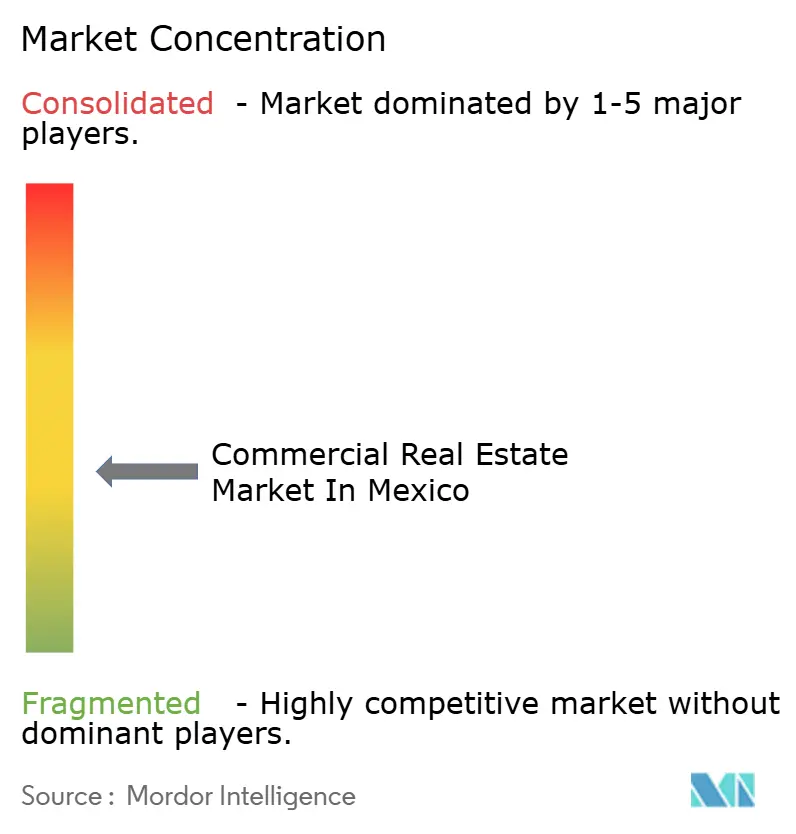

Competitive Landscape

The Mexico commercial real estate market is fragmented. Industrial and logistics exhibit moderate concentration among institutional landlords, with scale vehicles expanding through consolidation and selective development. A landmark transaction integrated Terrafina into FIBRA Prologis, creating a national leader with large‑tenant reach and improved capital markets access. Vesta’s sustainability‑linked financing and certification targets highlight an ESG‑led differentiation strategy that aligns with global capital mandates. FIBRA Uno pivots toward development yield capture through a specialized platform while navigating a stricter credit backdrop. The Mexico commercial real estate market rewards platforms that control shovel‑ready land, utility connections, and leasing pipelines with high-credit tenants.

Office and retail remain fragmented, which limits scale efficiencies but enables niche positioning and amenity‑driven strategies. Mexico City’s trophy towers lead on occupancy and pricing, while secondary stock in outer submarkets lags. Mixed‑use flagships that integrate retail, office, and residential demonstrate stronger resilience and leasing velocity. The Mexico commercial real estate market sees owners deepen property management capabilities and focus on wellness, ESG, and flexible layouts to defend cash flows. Retail strategies emphasize sales per square meter and hybrid tenant mixes, with health and experience anchors stabilizing traffic.

Developers compress delivery timelines by internalizing design, construction, and leasing and by pre‑leasing a portion of GLA before breaking ground. New fiber routes and private substations around data‑center clusters shape land acquisition and forward leasing in key states. Capital recycling remains active as listed vehicles dispose of non‑core assets and fund projects in high‑demand corridors. The Mexico commercial real estate market is increasingly differentiating on certifications and compliance as export‑oriented occupiers demand audited standards. Platforms that align regulatory readiness, ESG, and infrastructure access hold an advantage in tenant selection and pricing.

Mexico Commercial Real Estate Industry Leaders

Fibra Uno (FUNO)

FIBRA Prologis (FIBRAPL)

FIBRA Macquarie México (FIBRAMQ)

FIBRA Monterrey (FMTY)

FIBRA Danhos (DANHOS)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Kio Data Centers inaugurated its QRO2 facility in Parque Industrial El Marqués, Querétaro, adding 12 MW of IT capacity and bringing the company's total Querétaro campus to 19 MW.

- November 2025: FIBRA Prologis concluded its public acquisition offer for 100% of Terrafina's CBFIs, achieving 99.82% ownership and triggering a delisting from the Mexican Stock Exchange effective December 1, 2025.

- November 2025: FIBRA Prologis issued USD 500 Million in senior unsecured bonds over 10 years (maturity November 26, 2035) with a yield of 145 basis points over U.S. Treasury bonds. Proceeds are allocated to general corporate purposes, including partial debt repayment and potential acquisitions.

- October 2025: The Mexican federal government, via the Secretaría de Economía, announced CloudHQ's USD 4.8 Billion commitment for six data centers in Querétaro, with President Claudia Sheinbaum Pardo and Economy Secretary Marcelo Ebrard Casaubon emphasizing the project's role in Mexico's Plan México strategy to enhance AI and digital-infrastructure capacity.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines Mexico's commercial real estate market as income-generating non-residential property, office, retail, logistics/industrial, hospitality, and mixed-use assets, valued at prevailing capital-market prices and tracked through transactions, completions, and stabilized stock. According to ���ϲ�����, leasing-only fees, construction services, and purely residential assets lie outside this frame.

Scope Exclusion (clarity first): bare land trading that lacks development permits is not counted.

Segmentation Overview

- By Property Type

- Offices

- Retail

- Logistics

- Others (Industrial, Hospitality, etc.)

- By End-User

- Individuals / Households

- Corporates & SMEs

- Others

- By States

- Mexico City (CDMX)

- Nuevo Leon

- Jalisco

- Queretaro

- Mexico State (Edomex)

- Rest of Mexico

Detailed Research Methodology and Data Validation

Primary Research

Fortnightly calls and surveys with developers, FIBRA managers, brokers, building-tech vendors, and credit officers across Mexico City, Monterrey, Guadalajara, Tijuana, and Queretaro let us verify achievable rents, fit-out costs, and nearshoring tailwinds that secondary data hinted at but did not quantify. Inputs from these interviews guided vacancy-take-up lags and cap-rate spreads used in the model.

Desk Research

We gathered macro and property-level signals from tier-one public sources such as Banco de Mexico rate releases, INEGI construction output, Secretaria de Economia FDI dashboards, AMPIP industrial-park directories, SAT trade statistics, and CBRE/SiiLA vacancy bulletins. Company 10-Ks, REIT filings, and reputable press helped us gauge pipeline funding and rent benchmarks. To enrich gaps, our analysts tapped Dow Jones Factiva for deal news and D&B Hoovers for issuer financials. This list is illustrative; many additional publications underpinned data checks.

A second pass linked freight flows from Aduanas, e-commerce turnover from Asociacion de Internet MX, and highway concession awards to sub-sector uptake, thereby validating demand curves for last-mile warehouses and border sheds. Historical absorption figures were reconciled with permits held in the Registro Unico de Vivienda to filter speculative announcements.

Market-Sizing & Forecasting

We begin with a top-down stock reconstruction. Certified floor space and transaction logs are multiplied by average realized prices, then adjusted for shadow inventory and currency conversion. Results are sense-checked through selective bottom-up rollups of major FIBRA portfolios and sampled sales-price-per-square-meter evidence. Key variables like industrial absorption, peso lending rates, e-commerce parcel volume, foreign direct investment, and construction-input inflation feed a multivariate regression that projects value through 2030. Where bottom-up data show gaps, we prorate volumes using occupancy trends from verified property managers before blending into the master series.

Data Validation & Update Cycle

Outputs pass a three-layer review: automated outlier scans, senior analyst cross-checks with external yardsticks, and a final reconciliation against new deals logged in Dow Jones Factiva. Reports refresh annually; material events such as tax reform or large IPOs trigger interim recalculations, ensuring clients receive an up-to-date view.

Why Mordor's Mexico Commercial Real Estate Baseline Commands Confidence

Published estimates often diverge because firms choose different asset baskets, price bases, or refresh cadences. Our disciplined scope, variable selection, and annual re-benchmarking mean stakeholders can rely on one coherent yardstick.

Key gap drivers include some publishers counting only brokered rentals, others folding residential and raw land into totals, several applying macro GDP elasticities without property evidence, and many freezing exchange rates for multi-year spans.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 64.18 B (2025) | ���ϲ����� | - |

| USD 5.13 B (2024) | Regional Consultancy A | Narrow rental fee scope, limited property types, unvalidated multipliers |

| USD 269.62 B (2023) | Global Consultancy B | Blends residential and land, GDP-based scaling, no asset-level checks |

| USD 48.25 B (2023) | Industry Journal C | Transaction-only lens, excludes owner-occupied industrial stock, fixed FX rate |

In sum, ���ϲ����� delivers a balanced, transparent baseline grounded in verifiable property data and refreshed assumptions, giving decision-makers numbers they can trace, test, and trust.

Key Questions Answered in the Report

What is the Mexico commercial real estate market growth outlook through 2031?

The market is projected to grow from USD 64.18 Billion in 2026 to USD 92.44 billion by 2031 at a 6.9% CAGR, led by logistics and data centre adjacency dynamics.

Which property type leads the Mexico commercial real estate market and why?

Logistics leads with a 33.22% share in 2025 and the fastest 8.1% CAGR through 2031 due to e-commerce density, last-mile demand, and automation-ready specifications in urban edge warehouses.

How are financing conditions shaping development decisions in Mexico's commercial real estate?

Despite policy rate cuts, lending spreads remain elevated, and construction credit is tight, which pushes developers toward stabilized rentals and build to lease structures rather than speculative sales.

Where are the fastest growing geographies within Mexico commercial real estate?

Querétaro records the steepest CAGR at 7.33% as hyperscale data centre campuses expand, while Mexico City remains the largest node by value with tight Class A office dynamics.

What makes rentals outperform sales in the Mexico commercial real estate market?

Rentals benefit from affordability pressures, tighter mortgage underwriting, and landlord offerings like inflation linked leases, energy bundles, and higher TI packages that reduce occupier capex.

How does data centre expansion affect the broader Mexico commercial real estate market?

Hyperscale campuses concentrate in power and fiber-rich corridors, creating digital adjacency premiums for nearby industrial land and tightening pre-leasing in Monterrey and Querétaro as grid upgrades progress.

Page last updated on: