Chondroitin Sulfate Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.39 Billion |

| Market Size (2031) | USD 1.63 Billion |

| Growth Rate (2026 - 2031) | 3.26% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

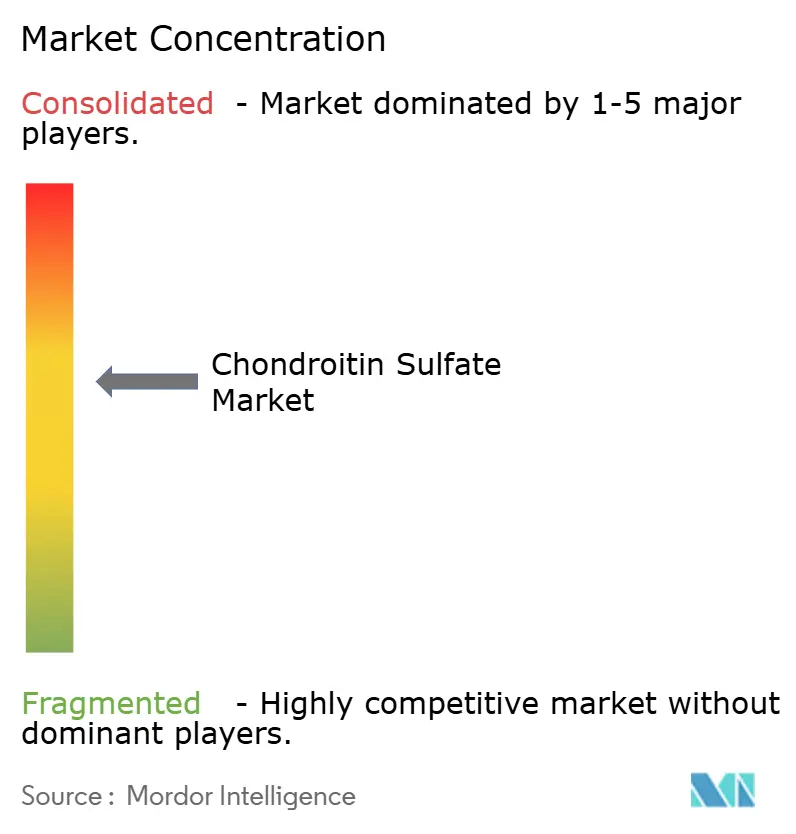

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Chondroitin Sulfate Market Analysis by ���ϲ�����

The Chondroitin Sulfate Market size is projected to be USD 1.35 billion in 2025, USD 1.39 billion in 2026, and reach USD 1.63 billion by 2031, growing at a CAGR of 3.26% from 2026 to 2031.

Consistent consumer demand for joint-health products supports headline growth, yet the value pool is clearly tilting toward pharmaceutical-grade active pharmaceutical ingredients (APIs) and biosynthetic variants that deliver margins two to three times higher than commodity animal extracts. Prevalence of osteoarthritis among adults aged 45 and older continues to anchor baseline volumes. Still, the fastest revenue gains come from injectable viscosupplements and low-molecular-weight formats aimed at regenerative medicine. Regulatory upgrades in the United States, the European Union, and Japan are tightening quality thresholds, effectively splitting the arena into a high-compliance pharmaceutical tier and a price-sensitive nutraceutical tier. Makers able to scale GMP-certified fermentation, maintain multi-jurisdictional Drug Master Files, and secure cartilage traceability are widening their competitive lead.

Key Report Takeaways

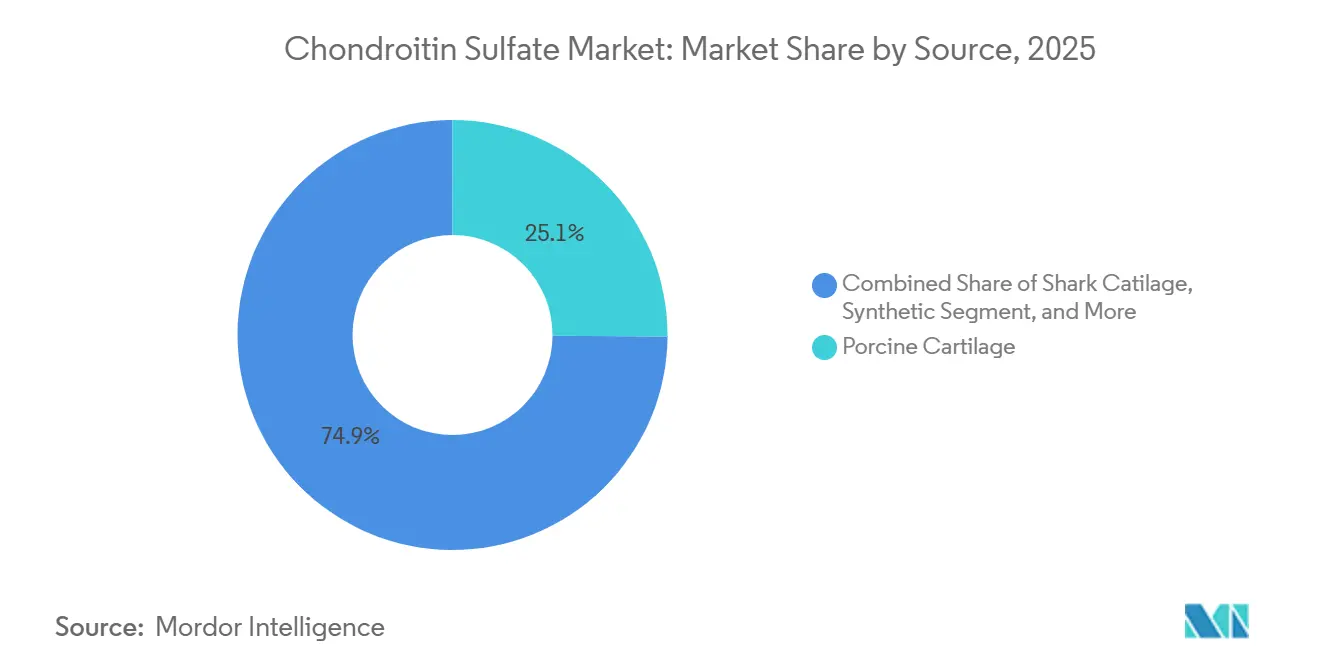

- By source, porcine cartilage led with 25.12% of the chondroitin sulfate market share in 2025; synthetic variants are projected to advance at a 5.81% CAGR through 2031.

- By grade, pharmaceutical-grade held 49.62% of the chondroitin sulfate market size in 2025, while food-grade registers the fastest 5.18% CAGR to 2031.

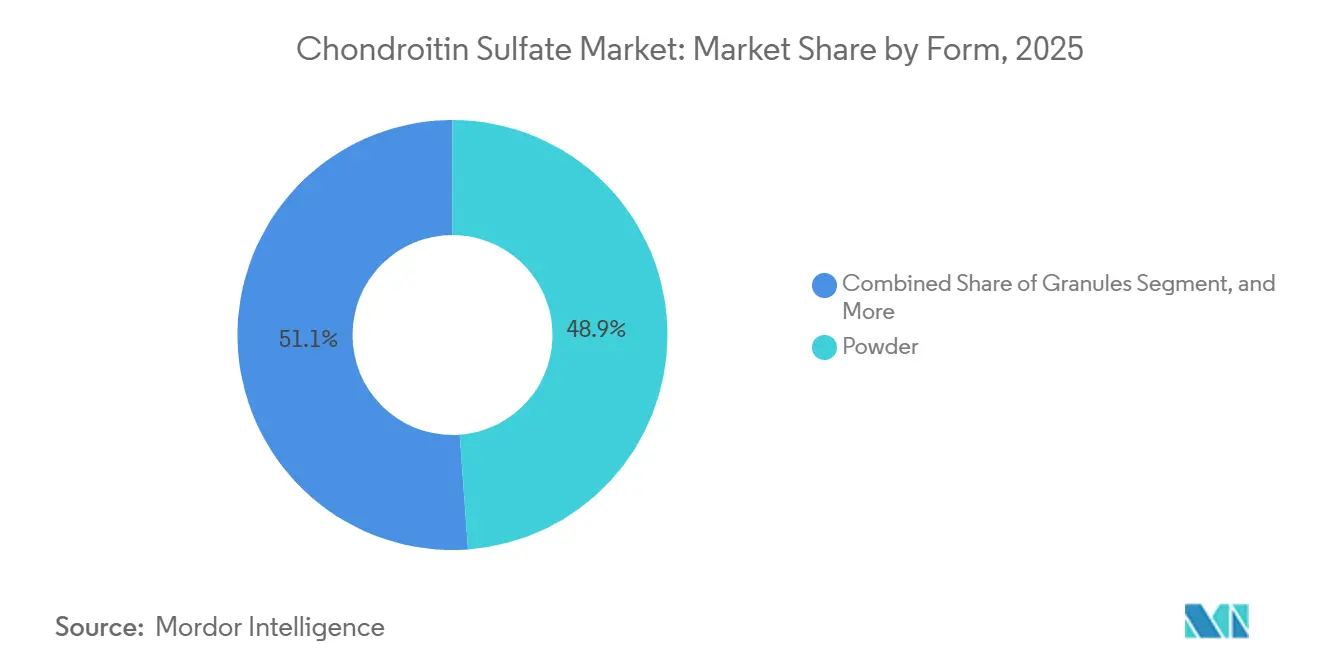

- By form, powder accounted for 48.86% share of the chondroitin sulfate market size in 2025 and granules are set to expand at 5.66% CAGR through 2031.

- By application, cosmetics captured 48.22% revenue share in 2025; pharmaceuticals are forecast to grow at a 5.29% CAGR to 2031.

- By geography, North America commanded 38.62% of 2025 revenue, whereas Asia-Pacific is poised for the highest 6.54% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Chondroitin Sulfate Market Trends and Insights

Driver Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Intensifying osteoarthritis prevalence among 45+ adults | +1.2% | Global, especially North America, Europe, Japan, South Korea, China | Long term (≥ 4 years) |

| Rising nutraceutical adoption in joint-health supplements | +0.9% | North America, Europe, urban China, India, Southeast Asia | Medium term (2–4 years) |

| Regulatory upgrades endorsing pharmaceutical-grade CS | +0.5% | United States, European Union, United Kingdom, Switzerland | Short term (≤ 2 years) |

| Expansion of bovine cartilage processing in China & India | +0.4% | China (Shandong, Jiangsu), India (Maharashtra, Gujarat) | Medium term (2–4 years) |

| Growth of injectable viscosupplement R&D | +0.3% | United States, Japan, South Korea, Germany, France | Long term (≥ 4 years) |

| Emerging demand for low-molecular-weight CS | +0.2% | United States, European Union, Japan | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Intensifying Osteoarthritis Prevalence Among 45+ Population

In 2024, the Global Burden of Disease Study reported 595 million cases of osteoarthritis worldwide, a 132% increase since 1990, with projections suggesting the number could exceed 1 billion by 2050.[1]GBD 2021 Osteoarthritis Collaborators, “Global, Regional, and National Burden of Osteoarthritis, 1990–2020, and Projections to 2050,” The Lancet Rheumatology, thelancet.com In China, 15.6% of adults over 40 grapple with bilateral knee osteoarthritis, leading to a validated daily chondroitin sulfate dosage of 1,200-1,500 mg, as per the CONCEPT trial.[2]National Institutes of Health, “Chondroitin Sulfate Versus Celecoxib Versus Placebo for Knee Osteoarthritis (CONCEPT),” ClinicalTrials.gov, clinicaltrials.gov In the U.S., Medicare Advantage's coverage of viscosupplement injections has shifted occasional users to regulars, with patients now averaging 3-5 g per quarterly procedure. While Asia-Pacific boasts a significant aging demographic, 220 million Chinese citizens aged 65+ in 2024, the region faces challenges. Reimbursement gaps have kept oral supplements ahead, resulting in lower revenue per patient than in the U.S.[3]CITES Secretariat, “Traceability of Shark Products in International Trade,” cites.org However, suppliers that ensure consistent GMP-grade output stand to gain the most from long-term volume growth.

Rising Nutraceutical Adoption in Joint-Health Supplements

Preventive self-care trends convert pharmaceutical insights into over-the-counter formats, propelling joint-health supplements past USD 100 billion globally. In Asia-Pacific, middle-class consumers integrate chondroitin sulfate powders, granules and chewables into daily routines, attracted by combination formats that cut pain in as few as five days when paired with collagen and Boswellia serrata. Standardization gaps still differentiate pharmaceutical-grade from food-grade, but premium nutraceuticals bridge this divide as brands tout USP-level purity to justify higher price points.

Regulatory Upgrades Endorsing Pharmaceutical-Grade CS

Health authorities sharpen distinctions between grades. FDA GRAS Notice 666 anchors safety for food applications up to 1,200 mg/day. EMA approvals across 13 nations elevate pharmaceutical-grade material to ethical-drug status. These actions reward firms that invest in validated processes and discourage opportunistic suppliers reliant on minimal testing. The compliance premium fuels vertical integration, tighter supplier audits and advanced analytics to guarantee molecular-weight consistency and impurity thresholds.

Expansion of Bovine Cartilage Processing Capacity in China & India

Cost-advantaged facilities in China and India expand capacity, underpinned by hot-pressure co-production that extracts both peptides and chondroitin sulfate from chicken or bovine sources. Indian plants turn buffalo by-products into 60–62 mg/g yields, diversifying raw-material pools. These localized feedstocks hedge against Western livestock cycles and enable flexible pricing for export buyers.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in animal-derived raw-material supply | -0.7% | Global, acute in regions dependent on imports | Short term (≤ 2 years) |

| Quality & adulteration concerns in food-grade CS | -0.5% | Global, regulatory scrutiny in developed markets | Medium term (2-4 years) |

| Stricter CITES controls on shark cartilage sourcing | -0.3% | Global, concentrated impact on shark-dependent suppliers | Medium term (2-4 years) |

| Plant-based glycosaminoglycan analogues gaining traction | -0.2% | North America & EU, early adoption in premium segments | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Volatility in Animal-Derived Raw-Material Supply

Livestock disease cycles, slaughterhouse shutdowns and CITES constraints on shark cartilage periodically curtail raw-material flows and elevate costs. Manufacturers hedge through multi-species sourcing and higher inventories, which lift working-capital requirements and price tags for end users. Synthetic pathways and fermentation reduce this exposure, encouraging strategic capex toward controlled bioprocessing.

Quality & Adulteration Concerns in Food-Grade CS

Analyses of United States supplements found some products delivering less than label claims and inconsistent molecular weights that blunt efficacy. Such lapses invite regulatory warnings, removal from e-commerce shelves, and dampened consumer trust. The reputational drag narrows growth in mainstream retail, steering discerning buyers toward pharmaceutical-grade or third-party-verified lines. In 2024, a study revealed that food-grade supplements exhibited 40-60% lower bioactivity and increased cytotoxicity compared to their pharmaceutical counterparts. The United States FDA issued several import alerts targeting undeclared synthetic polymers, which were found to manipulate assay values.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Biosynthetic Growth Offsets Porcine Volatility

The chondroitin sulfate market size for biosynthetic material is projected to grow at a 5.81% CAGR, the fastest among all source types. Vegan positioning, avoidance of CITES regulations and controlled heavy-metal profiles underpin willingness to pay premiums of 15-20% over conventional extracts. Porcine cartilage still accounted for 25.12% of 2025 revenue, supported by China’s Shandong and Jiangsu networks, yet pricing spikes tied to disease outbreaks are nudging formulators toward bovine and avian options. Bovine cartilage, historically holding the largest chondroitin sulfate market share, benefits from EFSA’s 2024 finding of “very low” BSE risk, narrowing the regulatory premium versus porcine sourcing. Shark cartilage’s share continues to shrink as clearance delays and traceability costs climb under stricter CITES oversight.

Capacity expansions in India’s Maharashtra and Gujarat add geographic diversification, but smaller throughput means Chinese suppliers remain cost leaders. Over the forecast period, biosynthetic supply will capture most incremental value, leaving animal-derived products to serve the price-sensitive nutraceutical tier.

By Grade: Pharmaceutical Tier Maintains Margin Advantage

The chondroitin sulfate market share of pharmaceutical-grade product will erode slightly as Asia-Pacific nutraceutical players expand, yet projected unit expansion keeps absolute volume rising. Food-grade output is set to post a 5.18% CAGR to 2031, fueled by direct-to-consumer e-commerce platforms willing to trade purity for affordability. Cosmetics-grade sits between the two in specification severity and benefits from premium absolutes in dermal fillers.

Because only a dozen suppliers maintain both European Pharmacopoeia certificates and FDA Drug Master Files, an effective moat protects injectable and ophthalmic revenue streams. Food-grade manufacturers would need multi-year capital spending to close the compliance gap, preserving price differentials throughout the outlook period.

By Form: Granules Win on Processing Speed

Powder held 48.86% of 2025 revenue due to its adaptability in capsules, tablets and drink mixes. Manufacturers favor powders for their low moisture content, long shelf life and compatibility with automated dosing lines. Granules, though only 15.23% share, rise at 5.66% CAGR on the back of improved flow properties, reduced dust and better dissolution in sachet sticks popular among Asian consumers.

Injectables occupy a specialized tier comprising high-viscosity solutions intended for intra-articular use. While volumes remain modest, average selling prices are substantially higher, and R&D in dual-polymer gels with hyaluronic acid hints at future revenue jumps. Tablets and capsules continue to satisfy convenience-seeking supplement buyers, with brand owners experimenting in layered bilayer constructs that release glucosamine and chondroitin sulfate at staggered rates to prolong bioavailability. Advances in spray-drying and fluid-bed coating underline formulation complexity as a competitive lever rather than pure commodity.

By Application: Cosmetics Lead, Pharmaceuticals Accelerate

Cosmetics surprisingly represented 48.22% sales in 2025, driven by anti-aging serums capitalizing on chondroitin sulfate’s hydrophilic matrix retention. The pharmaceutical cluster, however, posts the fastest 5.29% CAGR, bolstered by osteoarthritis prescriptions and investigative indications such as bladder pain syndrome where Controcyst® showed 26.3% IPSS score reductions. Dietary supplements hold a resilient mid-40% share, catering to proactive health consumers. Veterinary lines address aging pets, with chewable tablets gaining traction among companion-animal owners seeking non-NSAID relief.

Across these verticals, product developers converge on combination architectures—pairing chondroitin sulfate with biosimilar-grade collagen peptides, curcumin or omega-3 fatty acids to create differentiated SKUs. Synergy claims, validated in randomized trials, enable premiums and strengthen brand loyalty. Thus, application diversity hedges the overall chondroitin sulfate market against regulatory swings in any single therapeutic area.

Geography Analysis

North America retains 38.62% of 2025 revenue, anchored by insurance coverage for prescription chondroitin sulfate, a large osteoarthritis patient pool and well-established nutraceutical retail channels. GRAS acceptance for food use and FDA guidance on purity thresholds reinforce consumer trust, though litigation risk keeps manufacturers invested in high-end analytics. The region’s stable yet modest 2.78% CAGR reflects maturity.

Asia-Pacific rises fastest at 6.54% CAGR, propelled by capacity buildouts in China and India that feed both domestic and export demand. Aging demographics intersect with traditional medicine openness, accelerating uptake of sachet sticks and effervescent drinks that dissolve granulated chondroitin sulfate. Japanese clinical acceptance of condoliase for lumbar disc herniation further diversifies therapeutic landscapes.

Europe benefits from ethical-drug approvals across 13 countries, with physicians prescribing pharmaceutical-grade chondroitin sulfate in place of NSAIDs to mitigate cardiovascular risk. Southern European nutraceutical consumers favor combination formulas featuring Mediterranean botanicals. South America and Middle East & Africa trail but post mid-single-digit CAGR as local distributors negotiate licensing deals with European API suppliers, extending reach into private clinics and upscale pharmacies. Regional heterogeneity in labeling rules and halal certification continues to affect product-launch timelines.

Competitive Landscape

Market concentration is moderate: Bioiberica, IBSA Institut Biochimique, and Seikagaku Corporation integrate backward into the procurement of raw cartilage, ensuring traceability. Bioiberica’s clinical dossier and pan-European approvals anchor a defensible moat, while Seikagaku leverages proprietary enzymatic depolymerization for low-molecular-weight grades.

Gnosis by Lesaffre disrupts with MyCondro and Mythocondro, fermentation-based, vegan-certified, and 99% pure, positioning the firm as a synthetic-focused challenger. Emerging biotech spin-outs patent E. coli strains that complete sulfation pathways, foreshadowing license deals with pharmaceutical incumbents seeking ESG-aligned supply chains. Strategic collaborations center on co-marketing finished dosage forms such as drinkable collagen-chondroitin blends for Asian beauty-from-within segments.

M&A appetite remains selective: acquirers target firms with validated fermentation assets or strong regional distribution. Intellectual-property fences around low-molecular-weight derivatives and injectable gels shape negotiation leverage. Competitive advantage increasingly depends on regulatory dossier breadth, GMP certifications across regions, and data packages supporting combination efficacy, favoring capital-rich incumbents while leaving commodity resellers vulnerable to synthetic substitution.

Chondroitin Sulfate Industry Leaders

Rochem International Inc.

Merck KGaA (Sigma-Aldrich, Inc)

Synutra, Inc.

SARIA Bio-Industries International GmbH. (Bioiberica S.A.U.)

Gnosis by Lesaffre

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: IBSA launched a European multicenter study evaluating Sinogel (hyaluronic acid and sodium chondroitin) combined with platelet-rich plasma in patients with early knee osteoarthritis.

- December 2025: Zeria Group’s ScanDroitin won Individually Recognized Functional Ingredient status from South Korea’s Ministry of Food and Drug Safety.

- September 2025: Symrise reported positive clinical outcomes for Chondractiv Move, a collagen-plus-chondroitin blend targeting menopausal joint health.

- June 2025: BioCell Technology granted exclusive licensing rights for Liquid BioCell Collagen to a global nutraceutical distributor, enlarging joint-and-skin portfolios.

- April 2025: Gnosis by Lesaffre rebranded its fermentation-based Mythocondro to MyCondro, aiming for stronger consumer recall.

Global Chondroitin Sulfate Market Report Scope

As per the scope of the report, chondroitin sulfate is a glycosaminoglycan and is a significant component of the extracellular matrix (ECM) of many connective tissues, including cartilage, bone, skin, ligaments, and tendons. In supplements, chondroitin sulfate usually comes from animal cartilage.

The chondroitin sulfate market is segmented by source, grade, form, application, and geography. By source, the market is segmented into swine, shark, bovine, synthetic, and others. By grade, the market is segmented into pharmaceutical grade, food grade, and cosmetics grade. By form, the market is segmented into powder, granules, tablets & capsules, and injectable/solution. By application, the market is segmented into pharmaceuticals, cosmetics, and veterinary. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers market size and forecasts in value (USD) for the above segments.

| Bovine Cartilage |

| Porcine Cartilage |

| Shark Cartilage |

| Avian Cartilage |

| Synthetic |

| Other Sources |

| Pharmaceutical Grade |

| Food Grade |

| Cosmetics Grade |

| Powder |

| Granules |

| Tablets & Capsules |

| Injectable / Solution |

| Pharmaceuticals & OTC Drugs |

| Dietary Supplements |

| Cosmetics & Personal Care |

| Veterinary Medicine |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Source | Bovine Cartilage | |

| Porcine Cartilage | ||

| Shark Cartilage | ||

| Avian Cartilage | ||

| Synthetic | ||

| Other Sources | ||

| By Grade | Pharmaceutical Grade | |

| Food Grade | ||

| Cosmetics Grade | ||

| By Form | Powder | |

| Granules | ||

| Tablets & Capsules | ||

| Injectable / Solution | ||

| By Application | Pharmaceuticals & OTC Drugs | |

| Dietary Supplements | ||

| Cosmetics & Personal Care | ||

| Veterinary Medicine | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What CAGR is forecast for the chondroitin sulfate market through 2031?

The market is expected to expand at a 3.26% CAGR between 2026 and 2031, rising from USD 1.39 billion to USD 1.63 billion.

Which source segment will grow fastest by 2031?

Synthetic chondroitin sulfate, produced via fermentation or full biosynthesis, is projected to record a 5.81% CAGR.

Why do pharmaceutical-grade products carry a premium?

They comply with USP and EP pharmacopoeia standards, are supported by randomized clinical trials, and secure regulatory approvals, delivering validated therapeutic outcomes.

Which region offers the highest growth potential?

Asia-Pacific shows the fastest 6.54% CAGR, supported by expanded manufacturing capacity and rising demand from aging populations.

How are sustainability concerns being addressed?

Fermentation-based, non-animal chondroitin sulfate such as Mythocondro reduces reliance on animal cartilage and aligns with vegan, kosher, and halal requirements.

Page last updated on: