Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

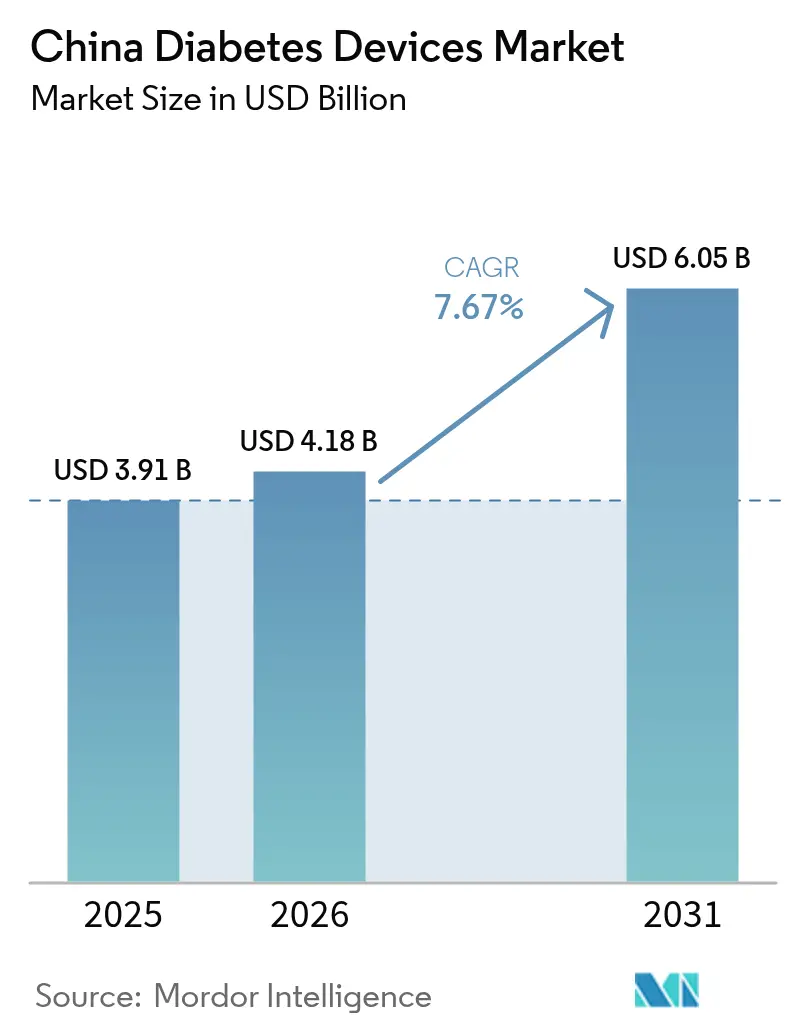

| Base Year Market Size (2025) | USD 3.91 Billion |

| Market Size (2026) | USD 4.18 Billion |

| Market Size (2031) | USD 6.05 Billion |

| Growth Rate (2026 - 2031) | 7.67% CAGR |

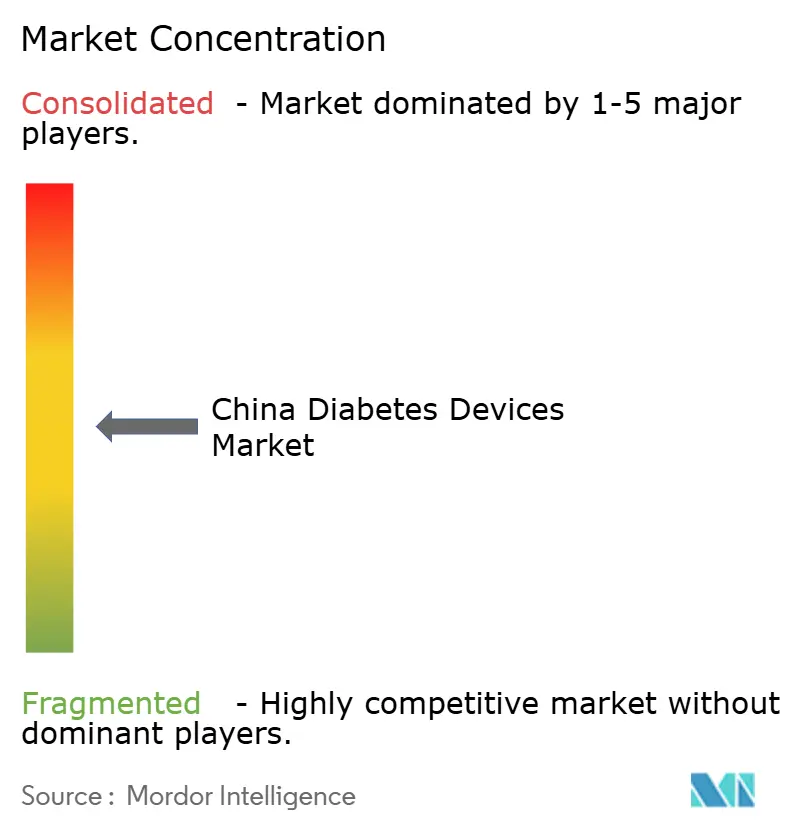

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

China Diabetes Devices Market Analysis by ���ϲ�����

The China Diabetes Devices Market size was valued at USD 3.91 billion in 2025 and is estimated to grow from USD 4.18 billion in 2026 to reach USD 6.05 billion by 2031, at a CAGR of 7.67% during the forecast period (2026-2031).

Demand is rising as Beijing’s Healthy China 2030 program hardwires routine diabetes screening into primary care, provincial reimbursement steadily adds continuous glucose monitoring and smart pens, and e-commerce brings devices to lower-tier cities that lack the breadth of hospital pharmacies. Domestic manufacturers hold a structural cost edge because rare-earth inputs, tax incentives, and proximity to contract assemblers compress average selling prices by 35–50% relative to multinational brands. Cloud-linked glucometers and Bluetooth enabled pens now integrate with hospital information systems, allowing physicians to document time-in-range gains that unlock higher disease related group tariffs. Regulatory frictions persist, yet order 797 channels top-tier devices through a single national review that supports quicker rollouts for firms with China-domiciled units.

Key Report Takeaways

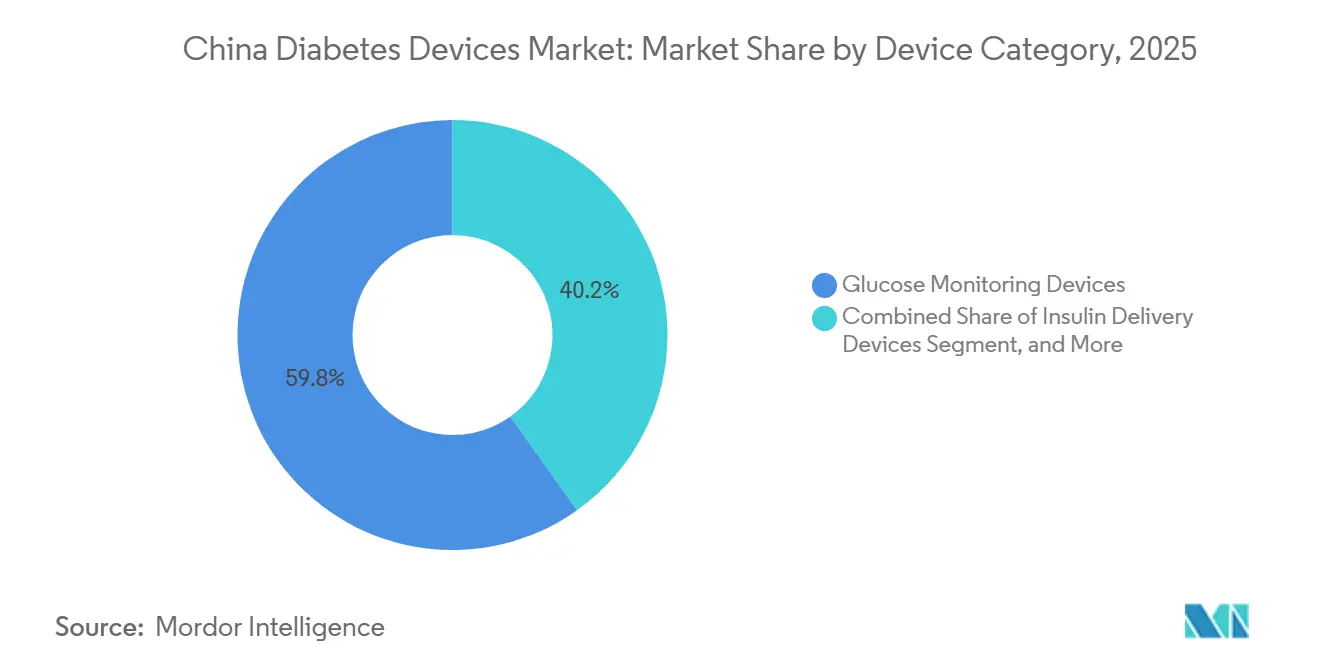

- By device category, glucose monitoring commanded 59.83% of 2025 revenue, while insulin delivery is forecast to expand at an 8.78% CAGR through 2031.

- By diabetes type, Type 2 accounted for 85.93% of utilization in 2025; Type 1 is projected to grow at a 11.97% CAGR through 2031.

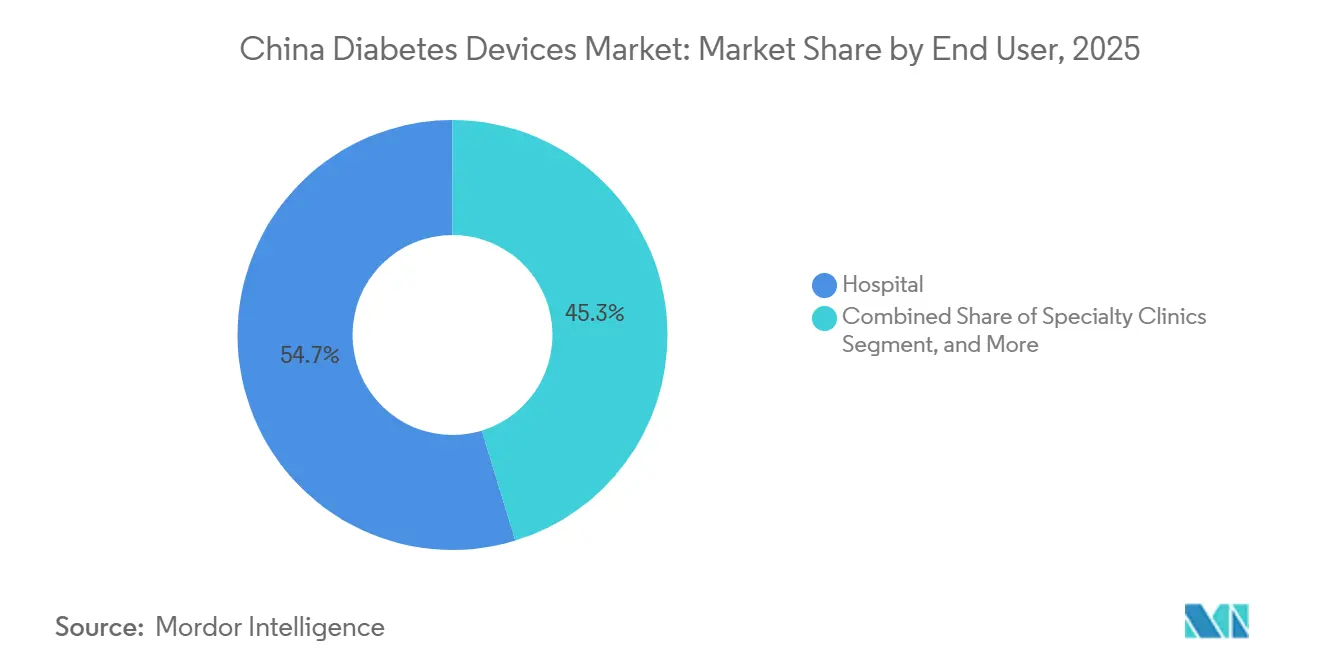

- By end user, hospital led with 54.72% of sales in 2025; online channels recorded the fastest 8.34% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Diabetes Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Diabetes Prevalence and Aging Population in China | +2.9% | National, with higher impact in urban areas | Long term (≥ 4 years) |

| Government Healthcare Reforms and Insurance Coverage Expansion | +2.0% | National, with early gains in tier-1 cities | Medium term (2-4 years) |

| Technological Advancements in Glucose Monitoring and Insulin Delivery | +1.6% | Urban areas, particularly eastern coastal regions | Medium term (2-4 years) |

| Growing Affordability of Domestic Devices | +1.2% | National, with higher impact in tier-2 and tier-3 cities | Short term (≤ 2 years) |

| Increasing Adoption of Digital Health and Telemedicine | +1.0% | Urban areas, with gradual expansion to rural regions | Medium term (2-4 years) |

| Expanding Private and Public Hospital Infrastructure | +0.8% | National, with concentration in eastern provinces | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Rising Diabetes Prevalence and Earlier Disease Onset

China reported 141 million diagnosed cases in 2025, plus 73.5 million undiagnosed adults, for a total of 49.7% latent prevalence.[1]National Health Commission, “Healthy China 2030 Initiative,” nhc.gov.cn Age-standardized rates exceed 20% in Beijing, Tianjin, and Shanghai, where diets and sedentary work contribute to earlier onset. Healthy China 2030 now requires fasting glucose checks for every adult above 35, adding 8–10 million newly identified patients each year. Longer disease duration increases the risk of complications, prompting clinicians to monitor continuously to delay microvascular injury. Guangdong and Zhejiang set aside RMB 2.3 billion (USD 316 million) in 2025 for community diabetes programs that bundle subsidized glucometers with education.[2]Guangdong Provincial Health Commission, “Community Diabetes Management Funding,” gdwst.gov.cn

Government Reimbursement Expansion for CGM and Insulin Pens

Beijing, Shanghai, Tianjin, Guangdong, Henan, and Yunnan moved CGM sensors and smart pens onto basic medical insurance lists between 2024 and 2025, lowering patient out-of-pocket spending by 40–60%.[3]National Healthcare Security Administration, “Reimbursement Expansion,” nhsa.gov.cn Eighteen provinces now publish reimbursement device catalogs, signaling nationwide diffusion. The cross-provincial settlement network links 550,400 hospitals and provides real-time claim approval, an advance that eases adoption for migrant workers who often return to hometown clinics for follow-up. Commercial health policies sold in 300 cities add another payor layer that covers sensors at 70–80% co-insurance. Asymmetry remains: Beijing shoulders 80% of CGM costs for Type 1 but only 30% for Type 2, preserving premium price pools for pediatric and pump-dependent users.

Domestic Manufacturing Cost Advantage Lowering Prices

Vertically integrated plants in Changsha and Hangzhou shorten supply chains and cut import duties, letting Sinocare price glucometers at RMB 150–200 (USD 21–28) versus RMB 350–450 (USD 48–62) for offshore rivals. MicroTech Medical’s Equil patch pump retails for RMB 18,000 (USD 2,480), forty percent below Medtronic’s MiniMed 780G. CGM sensors dropped from RMB 400–600 to RMB 100–300 within one year once Sibionics and Yuwell scaled automated lines. The cost gap rests on cheaper rare-earth magnets, tariff relief, and buy-China procurement rules that favor domestic brands delivering quality parity.

E-Commerce Reach into Lower-Tier Cities

JD Health shipped 8 million meter kits to Tier 2 and 3 municipalities in 2024 and supports same-day delivery across 30 cities. Online channels grow at a 14.01% CAGR because bundling sensors with video consults and auto-replenishment trim acquisition costs by roughly one-third. TMall’s medical device hub posted USD 3.2 billion in annual revenue from 3,300 merchants, with 22% stemming from diabetes products. Digital reimbursement pilots allow claims submission by mobile app and 48-hour approval, eliminating trips to county hospitals. Price sensitivity runs 35% higher outside Tier 1, making typical 20% e-commerce discounts decisive for first-time buyers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost of Advanced Devices | -1.4% | National, with acute impact in Tier 3 cities | Medium term (2–4 years) |

| Fragmented & Evolving NMPA Regulatory Pathways | -0.8% | National, affecting foreign manufacturers lacking China-domiciled legal entities | Short term (≤ 2 years) |

| Data-Privacy & Cybersecurity Concerns for Cloud-Linked Devices | -1.1% | National, with heightened sensitivity in urban centers (Tier 1 & Tier 2 cities) | Medium term (2–4 years) |

| Sensor-Grade Rare-Earth Supply Risks Inflating BOM Costs | -0.9% | Global, with concentrated upstream risk in Inner Mongolia | Long term (3–6 years) |

| Source: ���ϲ����� | |||

High Upfront Cost of Advanced Devices

Fourteen-day CGM packs coupled with transmitters generate annual spending of RMB 24,000–36,000 (USD 3,300–4,950), equal to 86–129% of average disposable income in Tier 3 counties. Pumps priced between RMB 18,000 and RMB 45,000 remain beyond the reach of most Type 2 patients. Reimbursement seldom covers consumables, leaving households to absorb RMB 8,000–15,000 (USD 1,100–2,065) each year. Awareness is low; a 2024 Chinese Diabetes Society survey found that 62% of Type 2 respondents were unaware of CGM availability and 74% believed pumps were hospital-only devices. Volume-based procurement will cut strip prices by up to 80% and could slow CGM conversion. Subscription pilots, such as Yuwell’s RMB 99-per-month model, show early promise but remain concentrated in urban Zhejiang.

Fragmented and Evolving NMPA Regulatory Pathways

Order 797, effective January 2025, requires foreign brands to establish local legal entities and to shoulder additional surveillance costs of RMB 2–5 million (USD 275,000–688,000) per year. Class III devices, including CGM and pumps, now need 120 local trial subjects, which stretches approval to 18 months. Class II meters clear in roughly eight months but require multiple provincial filings. The unique device identifier rule compels barcodes on all Class III products by 2026 and demands packaging line retrofits. Abbott’s November 2025 Libre 3 recall highlighted stricter enforcement, as the NMPA froze imports within 30 days rather than 90 days in the United States.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Category: Monitoring Devices Lead, Delivery Systems Accelerate

Glucose monitoring accounted for 59.83% of the China diabetes devices market in 2025, supported by widespread use of SMBG meters among Type 2 patients who test 2–4 times daily. The Chinese diabetes devices market share for monitoring skews toward Sinocare, which produces strips at costs 35–50% under multinational equivalents and holds 30–40% of volumes. Continuous monitoring is climbing quickly after six provinces reimbursed sensors that cut patient costs nearly in half. Sibionics and Yuwell secured 12% combined share within one year by pricing sensors 30–40% below Abbott, whose November 2025 recall opened shelf space for domestic models.

Insulin delivery will grow at an 8.78% CAGR, and its segment will drive the China diabetes devices market as the adoption of Bluetooth pens and patch pumps widens. Pens generated 68% of delivery revenue in 2025 after Jiangsu Delfu demonstrated 21% insulin savings across 150,000 connected units. MicroTech’s Equil and Medtrum’s A7+ pumps expand the options for patients seeking automated basal adjustment at a lower entry price. Closed-loop systems that use CGM data to fine-tune basal rates are poised to dominate high-acuity Type 1 care once Abbott-Medtronic interoperability is implemented in clinics in 2026.

By Diabetes Type: Type 2 Dominates Volume, Type 1 Drives Innovation

Type 2 covers 85.93% of device users and keeps basic meters in mass circulation. Lower test frequency and tighter budgets cap per-patient revenue, yet the absolute headcount secures a high consumables throughput. Price sensitivity is most acute in Tier 3 cities, where e-commerce discounts foster brand switching. Novo Nordisk’s Wegovy, approved mid-2024, could curtail long-term insulin dependence and, by extension, blunt device volumes if weight reduction scales.

Type 1 posted an 11.97% forecast CAGR as pediatric incidence climbs, and Beijing reimburses sensors for every newly diagnosed child. Each patient represents three to four times the device revenue of a typical Type 2 case, as therapy depends on lifelong monitoring and insulin delivery. Implantable sensors lasting 180 days appeal to adolescents who dislike frequent insertions, and a 365-day model awaits NMPA filing in 2026. Hybrid closed-loop platforms are now routine in Tier 1 clinics and are expected to spread to affluent Tier 2 cities before the forecast horizon ends.

By End User: Home-Care Settings Gain Momentum

Hospitals accounted for 54.72% of the China diabetes devices market size in 2025, reflecting the concentration of endocrinologists and reimbursement pathways in higher-level institutions. Nearly 88% of tertiary facilities now follow formal CGM operating procedures, supporting consistent demand. Patient preference for specialist oversight keeps footfall high, notwithstanding policy efforts to redirect visits to primary care.

Home-Care Settings, expanding at an 8.34% CAGR, represent the fastest-growing end-user group. Smartphone-linked glucometers and AI-enabled coaching apps empower self-management, while telemedicine follow-ups cut travel burdens. Randomized studies in Tianjin show that digitally integrated care reduced fasting glucose by 1.68% and HbA1c by 0.45% compared with usual care. These gains reinforce policy emphasis on out-of-hospital management and elevate the China diabetes devices market share of home-based users.

Geography Analysis

East China generated significant 2025 revenue for the China diabetes devices market, buoyed by Shanghai, Jiangsu, and Zhejiang, where disposable income reaches RMB 68,000 (USD 9,360) and hospital networks can support advanced pumps. Shanghai alone allocated RMB 1.2 billion in subsidies that cover sensors for Type 1 children. Manufacturing density further anchors the region, as Sinocare, MicroTech, and Yuwell plants are within one day's trucking distance of most contract magnet suppliers.

South China is driven by Guangdong’s updated reimbursement list, which cuts patient costs for 12 sensor models and 8 pump brands by roughly half. The Greater Bay Area fast track lets foreign brands sell before national clearance, reducing launch lag by a year and a half. West and Northwest provinces remain under 10% because incomes trail and hospitals stock fewer SKUs, yet JD Health now covers eight Tier 3 cities with same-day shipment, chipping away at access barriers.

Provincial reimbursement disparity spurs medical travel. Type 2 patients in Beijing often head to Henan, where a flat 50% reimbursement beats the 30% co-pay at home. Disease-related group tariffs differ by province as well; Zhejiang offers a 12% bonus for hospitals that document glycemic improvement through CGM uploads, but Henan offers no similar uplift, thus device rollouts proceed unevenly.

Competitive Landscape

Domestic players Sinocare, MicroTech Medical, Yuwell, and Sibionics field low-cost sensors and vertically integrated strips, together holding a significant 2025 share, which anchors a moderately concentrated China diabetes devices market. Abbott, Medtronic, Roche, and Dexcom defensively own 35% by focusing on accuracy metrics under 9% mean absolute relative difference and interoperability with pumps. Sinocare’s 2024 distribution deal with Menarini carries its CGM to 15 European markets, validating quality and strengthening export credentials. Abbott and Medtronic formed a data integration pact in 2024 that couples Libre sensors with MiniMed 780G closed-loop pumps to heighten switching costs once launched. Medtrum, Ottai, and PHC Group pursue white space in implantable sensors and Type 2 hybrid loops.

Volume-based procurement looms large; the tenth national round, announced in January 2025, will embrace strips, then wider devices, pushing bidders to sacrifice margins for guaranteed shares. Rare-earth export controls that raise offshore magnet costs by 15–25% could compel multinationals to localize final assembly to preserve price competitiveness. Compliance with the Personal Information Protection Law forces every firm to host patient data on mainland servers, adding roughly 20–30% to cloud costs, an overhead easier for domestic leaders to absorb through subsidy programs with Alibaba or Tencent cloud arms.

China Diabetes Devices Industry Leaders

Medtronics

Becton, Dickinson & Company

Abbott Diabetes Care

Roche Diabetes Care

Dexcom Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Novo Nordisk secured NMPA approval for Ozempic (semaglutide) for type 2 diabetes.

- January 2024: AstraZeneca won NMPA clearance for Xigduo XR, a once-daily dapagliflozin/metformin combination.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the China diabetes devices market as every factory-sealed instrument sold in mainland China that either monitors blood glucose, glucometers, test strips, lancets, continuous-glucose sensors and receivers, or delivers insulin, including reusable and disposable pens, pumps, cartridges, syringes, and jet injectors. The valuation covers hardware and integral consumables sold through hospital, retail, and online channels, expressed in USD retail revenue.

Scope exclusion: pharmaceutical insulin, oral antidiabetics, mobile apps sold without paired hardware, and aftermarket accessories are outside this estimate.

Segmentation Overview

- By Device Category

- Glucose Monitoring Devices

- Self-Monitoring Blood Glucose (SMBG) Devices

- Glucometers

- Test Strips

- Lancets

- Continuous Glucose Monitoring (CGM) Devices

- Sensors

- Durables (Receivers & Transmitters)

- Self-Monitoring Blood Glucose (SMBG) Devices

- Insulin Delivery Devices

- Insulin Pens

- Insulin Pumps

- Insulin Syringes

- Jet Injectors

- Other Diabetes-Care Devices

- Glucose Monitoring Devices

- By Diabetes Type

- Type 1 Diabetes

- Type 2 Diabetes

- Gestational & Others

- By End User

- Hospital

- Specialty Clinics

- Home Care Settings

- Other End Users

Detailed Research Methodology and Data Validation

Primary Research

Interviews with endocrinologists, diabetes-center heads, procurement officers at tier-2 hospitals, CGM distributors along the eastern seaboard, and product managers at domestic device makers helped us stress-test adoption rates, average selling prices, and inventory cycles across urban and rural cohorts, ensuring regional realities temper desk assumptions.

Desk Research

We began by mapping the adult diabetes population, device unit imports, and reimbursement policies from sources such as the National Bureau of Statistics of China, the International Diabetes Federation Atlas, the National Health Commission bulletins, and peer-reviewed journals like The Lancet Diabetes & Endocrinology. Company filings, IPO prospectuses, and provincial tender documents enriched price and channel insights. Our analysts supplemented these open datasets with selective extractions from D&B Hoovers for manufacturer revenue splits, Volza for shipment records, and Dow Jones Factiva for recall and regulation news. This list is illustrative; numerous other public and subscription datasets were referenced during validation.

Market-Sizing & Forecasting

Top-down modeling started with diabetic prevalence and average testing frequency to reconstruct monitoring demand, while insulin-treated patient pools and device penetration built the delivery segment. Results were cross-checked with bottom-up snapshots drawn from sampled supplier revenues and channel checks. Key variables like adult diabetes prevalence, CGM penetration, strips-per-patient per month, insulin pen installed base, average retail price shifts, and reimbursement coverage ratios anchor every calculation. A multivariate regression linking GDP per capita, aging index, and reimbursement depth to device uptake drives the 2025-2030 forecast, and scenario analysis adjusts for policy or pricing shocks. Gaps in bottom-up datapoints, such as unreported online volumes, were bridged through sensitivity ranges agreed with interviewees.

Data Validation & Update Cycle

Model outputs pass anomaly screens against historical import volumes, IDF prevalence trends, and select hospital procurement data. Senior analysts review variances, rerun assumptions where needed, and sign off before publication. The report refreshes annually, with interim updates triggered by major regulatory or pricing events; a last-minute pass guarantees clients receive the latest calibrated view.

Why Mordor's China Diabetes Devices Baseline Earns Decision-Makers' Trust

Published estimates often diverge because firms select different product mixes, price levels, and refresh cadences. Our disciplined scoping, variable selection, and yearly overhaul reduce those gaps.

Key gap drivers stem from: (1) some publishers omitting CGM durables or e-commerce channels, (2) others folding testing consumables and pharmaceutical insulin into one value, and (3) varied currency conversions and mid-year inflation adjustments.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.88 B (2025) | ���ϲ����� | - |

| USD 3.20 B (2025) | Regional Consultancy A | Excludes CGM receivers; relies on import data only |

| USD 6.22 B (2023) | Global Consultancy B | Combines devices with insulin and testing consumables |

| USD 1.89 B (2024) | Trade Journal C | Counts hospital channels, ignores e-commerce and clinic retail |

The comparison shows how scope breadth and data vintage swing totals by billions. Because our analysts isolate device-only revenue, align units with the latest IDF population base, and refresh assumptions every twelve months, ���ϲ����� provides a balanced, transparent baseline that executives can trace and replicate with confidence.

Key Questions Answered in the Report

How fast is the China diabetes devices market expected to grow through 2031?

It is forecast to advance at a 7.67% CAGR from 2026 to 2031, reaching USD 6.05 billion by the end of the period.

Which device category holds the largest revenue share today?

Glucose monitoring devices, mainly self-monitoring blood glucose meters and strips, contributed 59.83% of 2025 revenue.

What drives the rapid rise of online sales channels for diabetes devices in China?

E-commerce platforms such as JD Health and TMall combine same-day delivery, bundled telehealth services, and expanding digital reimbursement, delivering a 14.01% CAGR through 2031.

How do domestic manufacturers maintain a price edge over multinational rivals?

Local firms benefit from rare-earth supply proximity, tariff exemptions, and policy incentives that cut average selling prices by 35–50%.

What regulatory changes affect foreign diabetes device makers in China?

Order 797 mandates a China-domiciled legal entity and lengthens Class III approval to 18 months, while UDI barcoding and data localization add compliance costs.

Page last updated on: