Charcoal Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

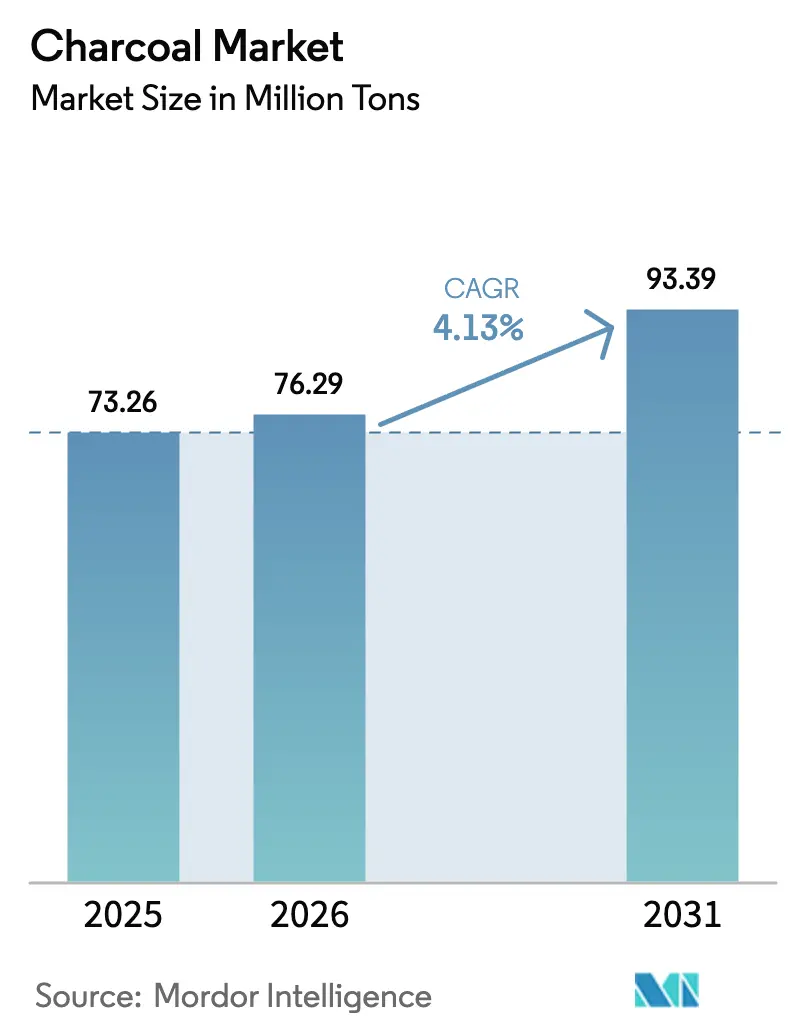

| Market Volume (2026) | 76.29 Million tons |

| Market Volume (2031) | 93.39 Million tons |

| Growth Rate (2026 - 2031) | 4.13% CAGR |

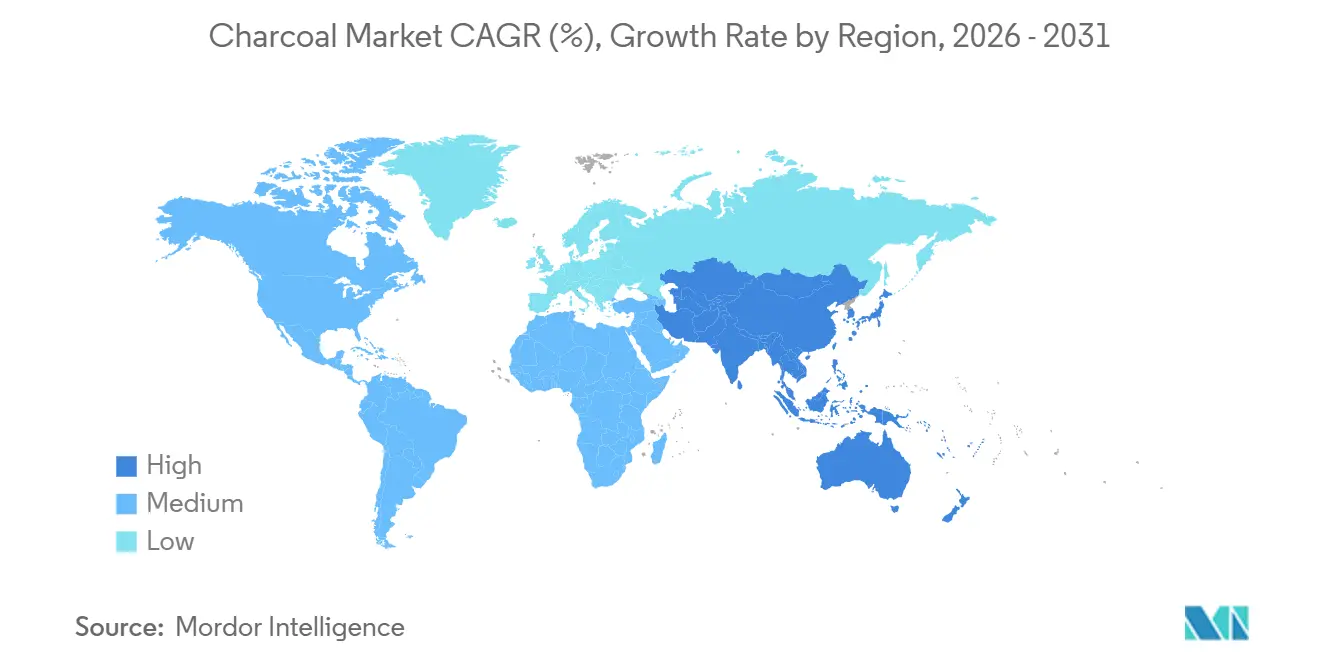

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Charcoal Market Analysis by ���ϲ�����

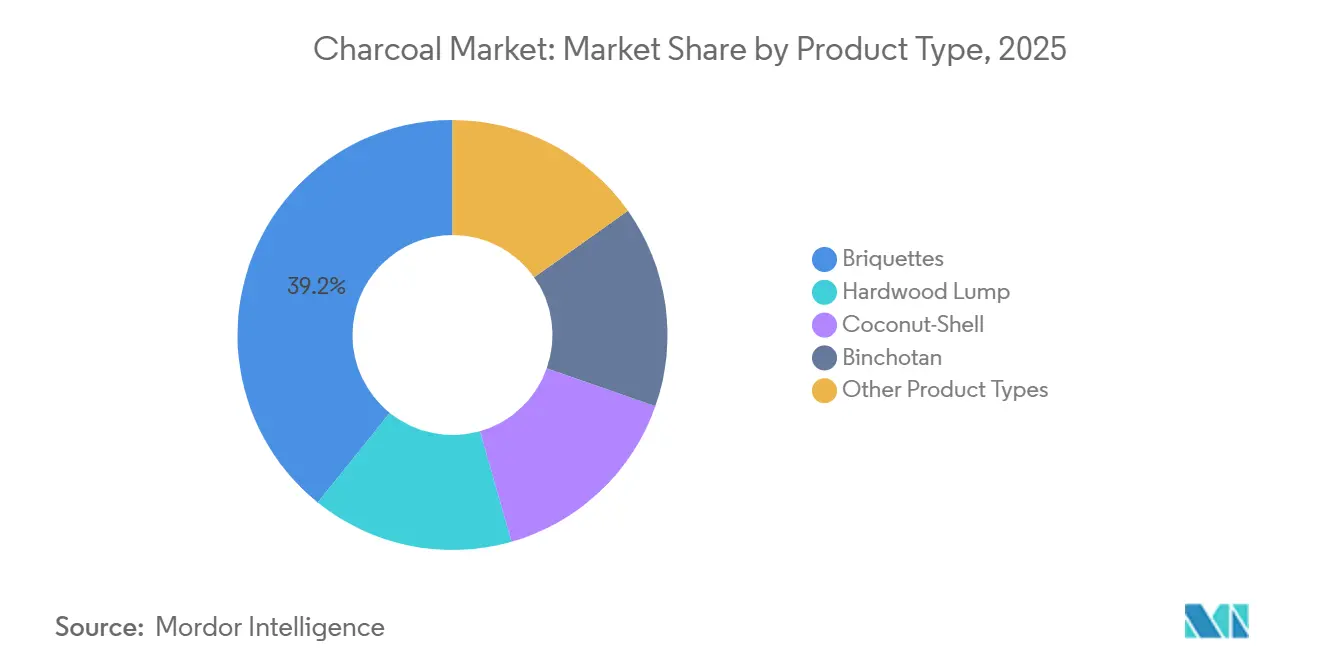

The Charcoal Market size is projected to expand from 73.26 Million tons in 2025 and 76.29 Million tons in 2026 to 93.39 Million tons by 2031, registering a CAGR of 4.13% between 2026 to 2031. Charcoal demand is evolving in two distinct ways. In emerging economies, charcoal remains a primary household fuel. In contrast, high-income regions have embraced it as a premium grilling choice and as an input for industrial purification. These differing applications have led to a split in regional supply chains. Tropical producers send large quantities of charcoal to barbecue hubs in OECD regions. However, these producers are losing ground domestically, as cities in the Africa-Pacific region increasingly turn to subsidized liquefied petroleum gas (LPG). The divergence in usage is also evident in product and feedstock selections. Briquettes accounted for a 39.22% market share in the base year 2025, but coconut-shell charcoal is expanding at the fastest rate due to its high adsorption capacity, making it a preferred choice for municipal water utilities and pharmaceutical companies. Furthermore, producers obtaining Forest Stewardship Council (FSC) certification and biochar carbon credits are gaining an edge. They are securing tenders in Europe and Japan, where there is a premium on traceability and low-emission origins.

Key Report Takeaways

- By product type, briquettes led with 39.22% of charcoal market share in 2025, while coconut-shell charcoal is forecast to grow at a 5.31% CAGR to 2031.

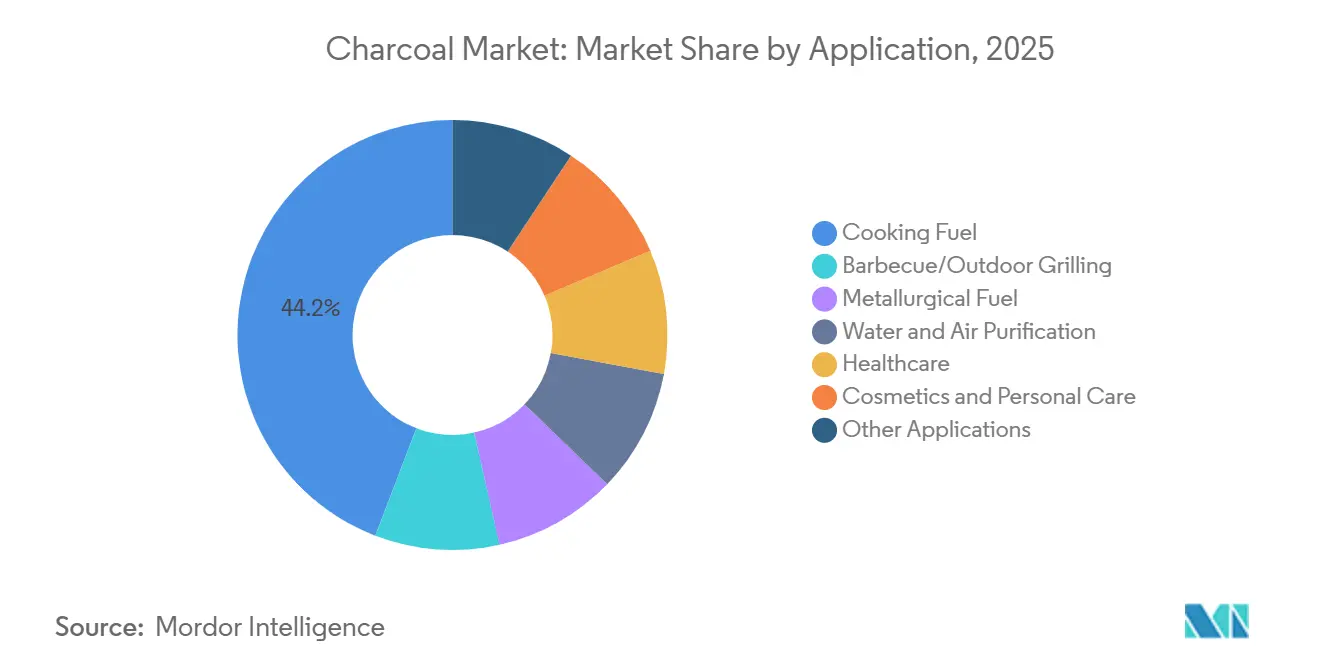

- By application, cooking fuel accounted for 44.15% of the charcoal market size in 2025 and barbecue plus outdoor grilling is advancing at a 5.12% CAGR through 2031.

- By region, Asia-Pacific captured 55.23% of charcoal market share in 2025 and is projected to expand at a 5.34% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Charcoal Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Outdoor grilling and BBQ culture surge | +0.80% | North America, Europe, Japan | Medium term (2-4 years) |

| Activated-charcoal demand in purification | +1.10% | Global urban hubs | Long term (≥ 4 years) |

| Industrial coke substitution in steel/cement | +1.30% | China, India, Southeast Asia | Medium term (2-4 years) |

| Certified-sustainable charcoal for ESG trade | +0.60% | Europe, Japan, North America (imports) | Long term (≥ 4 years) |

| Biochar carbon-credit revenue | +0.40% | Australia, North America, Brazil, Indonesia, Philippines | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Outdoor Grilling and BBQ Culture Surge in Developed Markets

Artisanal lump charcoal and Japanese Binchotan command significantly higher prices than standard commodity briquettes. To demonstrate their long-term commitment to the charcoal market, Weber and Blackstone launched co-branded charcoal accessories in multiple countries following their merger. Meanwhile, Kingsford introduced a “Beercoal” line infused with Miller Lite, highlighting how flavor innovation appeals to seasoned consumers in North America. Concurrently, European retailers are shifting their offerings toward coconut-shell briquettes to comply with Germany's stringent PM2.5 regulations. This trend toward premiumization not only increases average unit values but also offsets the decline in volume within saturated markets, ensuring consistent growth for the charcoal market.

Expansion of Activated-Charcoal Demand in Purification and Healthcare

Following the U.S. Environmental Protection Agency's PFAS limits, municipal water filtration has increasingly relied on coconut-shell activated carbon[1].U.S. Environmental Protection Agency, “PFAS National Primary Drinking Water Regulations,” epa.gov In response to a tight supply of raw materials, Jacobi Carbons has implemented a price increase. The World Health Organization's continued designation of activated charcoal as an essential medicine has driven its rising demand in pharmaceuticals. These high-purity sectors, which are willing to pay a premium, have shielded suppliers from the shift toward cooking-fuel substitution. This trend has supported the overall growth of the charcoal market.

Industrial Use as Coke Substitute in Iron, Steel and Cement

China is encouraging blast-furnace operators to blend biochar with metallurgical coke, targeting a reduction in carbon intensity by 2028[2]China MIIT, “Guidelines on Carbon Reduction in the Steel Industry,” miit.gov.cn . In India, cement producer Sagar Cements signed a biochar co-firing agreement, reaping the benefits of both carbon-credit revenues and fuel savings. Industrial buyers, valuing a steady bulk supply, are open to lower-grade feedstocks and are entering into multi-year contracts. This approach not only provides producers with a stable offtake, balancing the unpredictable cooking segment, but also further diversifies the charcoal market.

Certified-Sustainable Charcoal Unlocking ESG Export Channels

The EU Deforestation Regulation mandates the proof of origin for every shipment entering its market. In Japan, importers are implementing similar standards for Binchotan charcoal. Brazilian and Indonesian plantation operators, now vertically integrated, are financing GPS tracking and third-party audits. As a result, they are commanding price premiums over their uncertified competitors. These premiums are being reinvested into replanting initiatives and upgrading kilns, which not only tightens the supply from informal sources but also elevates the professionalism of the global charcoal market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid LPG/electric-cooking roll-out | -1.00% | Kenya, Nigeria, Ghana, India, Bangladesh, Vietnam, Indonesia | Short term (≤ 2 years) |

| Scrutiny of charcoal particulate emissions | -0.50% | California, Germany, United Kingdom | Medium term (2-4 years) |

| Volatile ocean-freight rates | -0.40% | West Africa-to-Europe, Southeast Asia-to-OECD, South America-to-Asia | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Rapid LPG/Electric-Cooking Roll-Out in Africa and Asia Urban Hubs

Kenya's initiative to subsidize cylinder refills has increased LPG penetration in Nairobi. Meanwhile, India's Ujjwala Yojana has not only provided a substantial number of LPG connections but also aims to achieve broader national coverage by 2027. In Ho Chi Minh City, EVN, Vietnam's state utility, is incentivizing induction stove purchases, which is reducing peak gas demand and accelerating the transition away from charcoal. These measures collectively reduce urban cooking-fuel demand and moderate the charcoal market in its traditionally dominant segment.

Rising Scrutiny of Charcoal Particulate Emissions in OECD Barbecue Hotspots

In 2024, the South Coast Air Quality Management District in California proposed stricter particulate limits for commercial charcoal grills. Meanwhile, Germany's environment agency encouraged consumers to transition to low-smoke briquettes, leading retailers to reallocate shelf space accordingly. In response, Duraflame introduced a "Clean Burn" briquette infused with mineral additives to reduce visible smoke. However, rising compliance costs have increased prices, which may suppress consumption in the premium segment of the charcoal market.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Coconut-Shell Charcoal Accelerates on Purification Demand

As water utilities and pharmaceutical manufacturers secure long-term supply contracts, coconut-shell charcoal is projected to grow at a 5.31% CAGR during the forecast period of 2026-2031, outpacing slower-moving segments. In 2025, briquettes held a 39.22% share of the charcoal market, bolstered by North American grocery dominance. However, growth is plateauing as enthusiasts shift toward hardwood lump. Lump varieties, known for their higher burn temperatures and reduced ash production, face limited market share due to a constrained hardwood supply and elevated unit costs. In Tokyo, restaurants showcase the niche binchotan, illustrating how quality differentials can boost margins, even with modest sales volumes.

Continuous-feed kilns in Indonesia and the Philippines are yielding cleaner emissions and higher outputs. This advancement positions coconut-shell charcoal to seize a more significant portion of the charcoal market, spanning both fuel and non-fuel uses. A recent price increase from a leading producer underscores the tightening supply of coconut shells and its escalating strategic significance. Considering this, producers of hardwood lumps and briquettes are diversifying their feedstock, now blending in materials such as sugarcane bagasse and sawdust. However, regulatory scrutiny on mangrove harvesting poses challenges, limiting these substitution options.

By Application: Industrial and Purification Segments Outpace Traditional Cooking

Cooking fuel accounted for 44.15% of the 2025 volume, yet urban LPG adoption is beginning to plateau. Barbecue and outdoor grilling emerged as the fastest-growing segment, boasting a 5.12% CAGR during the forecast period of 2026-2031, driven by premium product launches and lifestyle marketing in North America and Europe. In 2025, industrial users shifted additional tons, replacing petroleum coke in blast furnaces and cement kilns. This transition highlighted their preference for alternatives and reduced their dependence on LPG and electric options. As utilities upgraded plants to meet PFAS regulations, the U.S. saw a notable surge in demand for activated-charcoal purification, leading to an incremental annual volume boost.

Beyond utilities, industries such as pharmaceuticals, cosmetics, and horticulture capitalized on this heightened demand. The healthcare sector, benefiting from activated charcoal's endorsement on the World Health Organization's essential list, experienced consistent and significant demand. Simultaneously, while biochar soil amendments remained a niche, they experienced swift growth, spurred by credit premiums in carbon schemes across Australia and North America. This broadening of applications not only reduced risks but also strengthened the overall charcoal market.

Geography Analysis

Asia-Pacific controlled 55.23% of global volume in 2025 and is expected to expand at a 5.34% CAGR during the forecast period of 2026-2031. China's forestry agency reported significant output in 2025, with a large portion directed towards steel and cement plants. These plants blend charcoal into their processes as a strategy to reduce carbon intensity. Meanwhile, India presents a contrasting scenario: while urban demand for charcoal has been declining due to an aggressive rollout of LPG, rural areas continue to depend on solid fuels. This reliance keeps the country's baseline consumption steady. In the ASEAN region, exporters are capitalizing on the abundance of coconut-shell feedstock. They are shipping premium-quality activated carbon to Japan and South Korea, both of which offer higher prices for traceable supplies.

In 2025, North America accounted for a significant share of the global charcoal market. The United States imported a substantial amount of charcoal, predominantly from Paraguay, Argentina, and Mexico, to bolster its domestic production. Canada, while on a smaller scale, shares a similar grilling culture with the United States. In contrast, Mexico plays a dual role, both consuming and exporting charcoal, thanks to its integrated carbonization clusters located in Michoacán and Jalisco. Europe, holding a notable share of the global market, is witnessing a shift. To comply with the EU Deforestation Regulation, European importers are now channeling their orders towards certified suppliers in Brazil and Indonesia. This pivot is not only reshaping established trade routes but also driving up landed costs.

South America stands out as both a producer and exporter in the charcoal landscape. In 2025, Brazil's eucalyptus plantations produced a notable amount, with a significant portion of this output finding its way to buyers in the OECD. Meanwhile, Argentina and Paraguay are honing in on dense quebracho lump charcoal, which fetches premium prices in United States specialty retail outlets. The dynamics in the Middle-East and Africa are varied: South Africa is a key exporter to Europe, while urban centers in Kenya and Nigeria are pivoting towards LPG. Saudi Arabia, with its limited forestry resources, turns to imports to cater to its modest grilling market. These regional disparities underscore the multifaceted growth trajectory of the global charcoal market.

Competitive Landscape

The charcoal market is moderately fragmented. Kingsford and Royal Oak, two major North American players, utilize in-house bagging and nationwide retail contracts but face growing artisanal competition. In activated carbon, Jacobi Carbons and Haycarb are advancing with innovative activation furnaces, tailoring pore structures for specific contaminants, and securing long-term supply deals with water authorities. Indonesian startups using continuous-feed kilns are reducing emissions and increasing charcoal yields, challenging traditional batch-kiln operators. Sustainability has become a key market differentiator. Recently, Royal Oak expanded its FSC-certified lump-charcoal program to more European countries, while Fogo Charcoal, with FSC-certified Argentine quebracho, has entered Japanese and EU markets, achieving premium pricing. Technology integration is rising, with Weber-Blackstone linking grill sales to proprietary charcoal subscriptions, converting one-time buyers into repeat customers. Producers combining feedstock control, traceability, and branded distribution are strengthening their market position. Regulatory compliance is reshaping competition, as companies providing GPS harvest data and third-party audits secure EU contracts, while non-compliant micro-kilns in West Africa lose opportunities. Expertise in biochar credits is gaining importance; for example, Oxford Charcoal’s soil amendment product generates revenue and incorporates Verra-certified carbon removals, appealing to corporations seeking offset solutions. The focus has shifted from scaling production to commercializing low-smoke formulations, automating kilns, and leveraging carbon benefits.

Charcoal Industry Leaders

Kingsford Products Company

Royal Oak Enterprises, LLC

Duraflame, Inc.

Haycarb PLC

BRICAPAR S.A. Charcoal Briquettes

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Haycarb announced a BOI-certified activated-carbon plant in the Philippines. With coconut shells being the primary raw material for activated carbon production, this location ensures sustainability and supply chain efficiency, aligning perfectly with Haycarb’s commitment to responsible sourcing and eco-friendly carbon solutions.

- July 2025: Jacobi Carbons Group has announced a 15% to 20% price increase on all grades of coconut shell-based activated carbons. This decision is attributed to the continuous rise in raw material costs, which requires adjustments to the pricing structure.

Global Charcoal Market Report Scope

Charcoal is an inorganic carbon-based compound that is obtained by the incomplete combustion of animal and plant products within a low-oxygen environment. Generally, it is produced by burning wood and other organic matter such as cellulose, bagasse, bones, and others. The charcoal is manufactured using both traditional and technologically advanced methods. Under the traditional method, pit kilns are used to produce low-quality charcoal, whereas, under the modern method, industrial equipment is used to manufacture high-quality charcoal with a carbon content of over 82%.

The charcoal market is segmented by product type, application, and geography. By product type, the market is segmented into briquettes, hardwood lumps, coconut shells, binchotan, and other product types (sugar charcoal, mangrove, shisha, sawdust, and root). By application, the market is segmented into cooking fuel, metallurgical fuel, water and air purification, healthcare, cosmetics and personal care, and other applications (barbeque and horticulture). The report also covers the market size and forecasts for the charcoal market in 16 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of volume (tons).

| Briquettes |

| Hardwood Lump |

| Coconut-Shell |

| Binchotan |

| Other Product Types (Sugar Charcoal, Mangrove, Shisha, Sawdust, and Root) |

| Cooking Fuel |

| Barbecue/Outdoor Grilling (Retail and HoReCa) |

| Metallurgical Fuel |

| Water and Air Purification |

| Healthcare |

| Cosmetics and Personal Care |

| Other Applications (Barbeque and Horticulture) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product Type | Briquettes | |

| Hardwood Lump | ||

| Coconut-Shell | ||

| Binchotan | ||

| Other Product Types (Sugar Charcoal, Mangrove, Shisha, Sawdust, and Root) | ||

| By Application | Cooking Fuel | |

| Barbecue/Outdoor Grilling (Retail and HoReCa) | ||

| Metallurgical Fuel | ||

| Water and Air Purification | ||

| Healthcare | ||

| Cosmetics and Personal Care | ||

| Other Applications (Barbeque and Horticulture) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected global charcoal market volume by 2031?

The charcoal market size stands at 76.29 million tons in 2026, and it is projected to reach 93.39 million tons by 2031 at a 4.13% CAGR.

Which product type is growing fastest in the charcoal market?

Coconut-shell charcoal leads with a projected 5.31% CAGR through 2031 because water treatment and pharmaceutical buyers prefer its high adsorption capacity.

Why are sustainability certifications important for charcoal exporters?

FSC and similar schemes are now required to access EU and Japanese markets under deforestation regulations, and certified shipments fetch 40-50% price premiums over uncertified volumes.

What factors could restrain urban charcoal demand?

Rapid roll-out of subsidized LPG cylinders and electric induction stoves in African and Asian cities is cutting charcoal use by double-digit rates each year.

Page last updated on: