Cast Acrylic Sheet Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

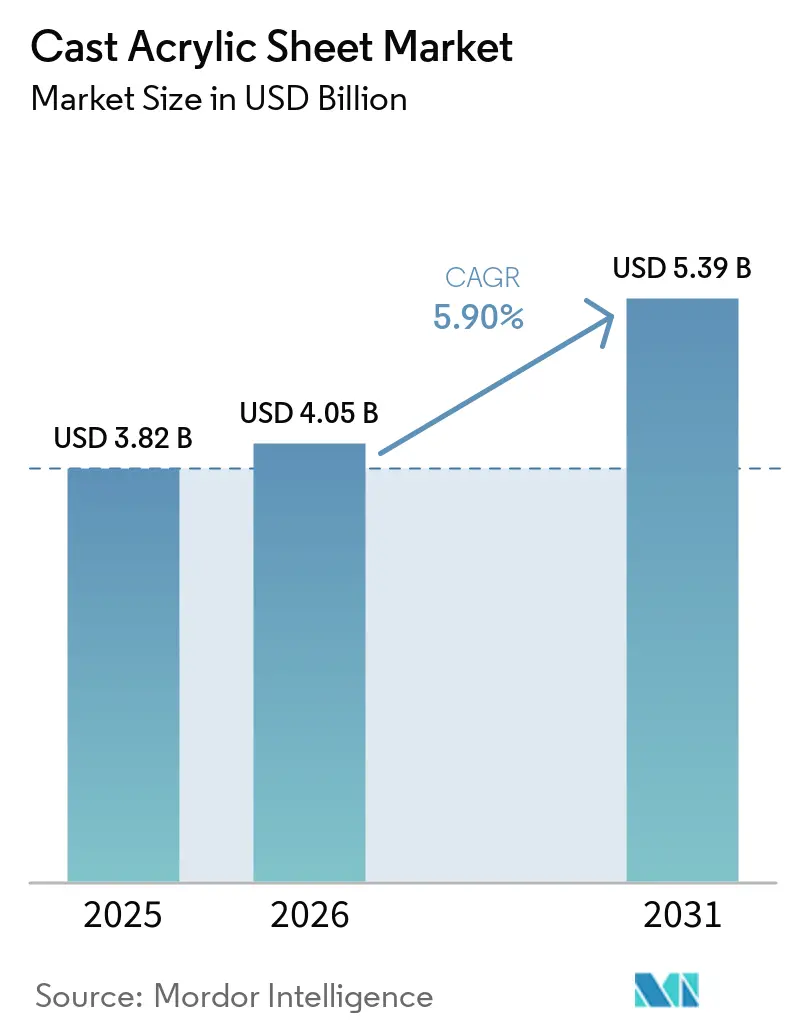

| Market Size (2026) | USD 4.05 Billion |

| Market Size (2031) | USD 5.39 Billion |

| Growth Rate (2026 - 2031) | 5.90% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Cast Acrylic Sheet Market Analysis by ���ϲ�����

The Cast Acrylic Sheet Market size is projected to expand from USD 3.82 billion in 2025 and USD 4.05 billion in 2026 to USD 5.39 billion by 2031, registering a CAGR of 5.90% between 2026 to 2031. Expanding point-of-sale hygiene infrastructure, rapid secondary-glazing uptake for building-integrated photovoltaics, and premium aquaculture investment continue to drive demand in the cast acrylic sheet market. Producers are increasingly adopting bio-based MMA production methods and chemical-recycling feedstock to reduce embodied carbon footprints and manage feedstock price volatility. Specialty grades, including impact-modified, UV-blocking, and light-diffusing variants, command higher prices, helping to alleviate margin pressures. Regional capacity expansions in Asia-Pacific are strengthening supply chain resilience and reducing delivery lead times. Competitive dynamics remain moderate as backward-integrated leaders maintain control over feedstock and operate multi-regional production facilities. However, agile regional specialists are gaining market share through shorter order-to-ship cycles and customized surface treatments.

Key Report Takeaways

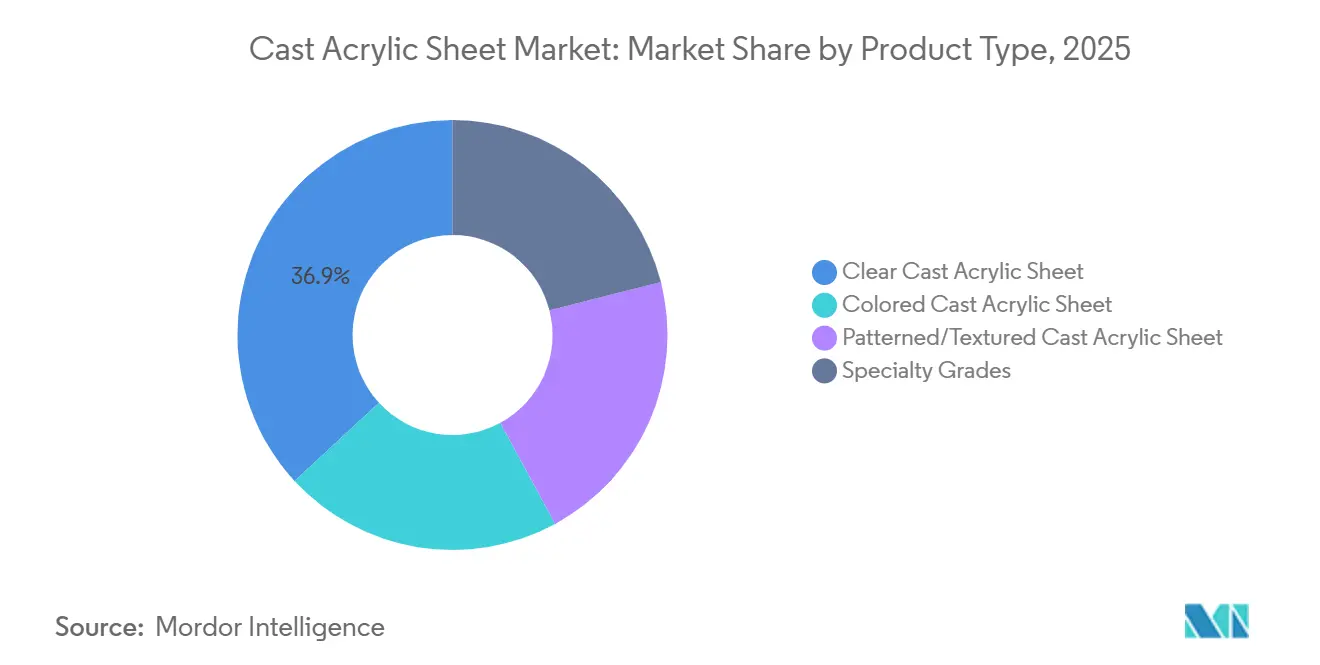

- By product type, clear cast acrylic sheet held 36.87% of the cast acrylic sheet market share in 2025, while specialty grades are advancing at a 6.68% CAGR through 2031.

- By thickness, 5.1–10 mm dominated with 39.88% of the cast acrylic sheet market share in 2025; greater than 20 mm (block) are set to grow at a 6.72% CAGR through 2031.

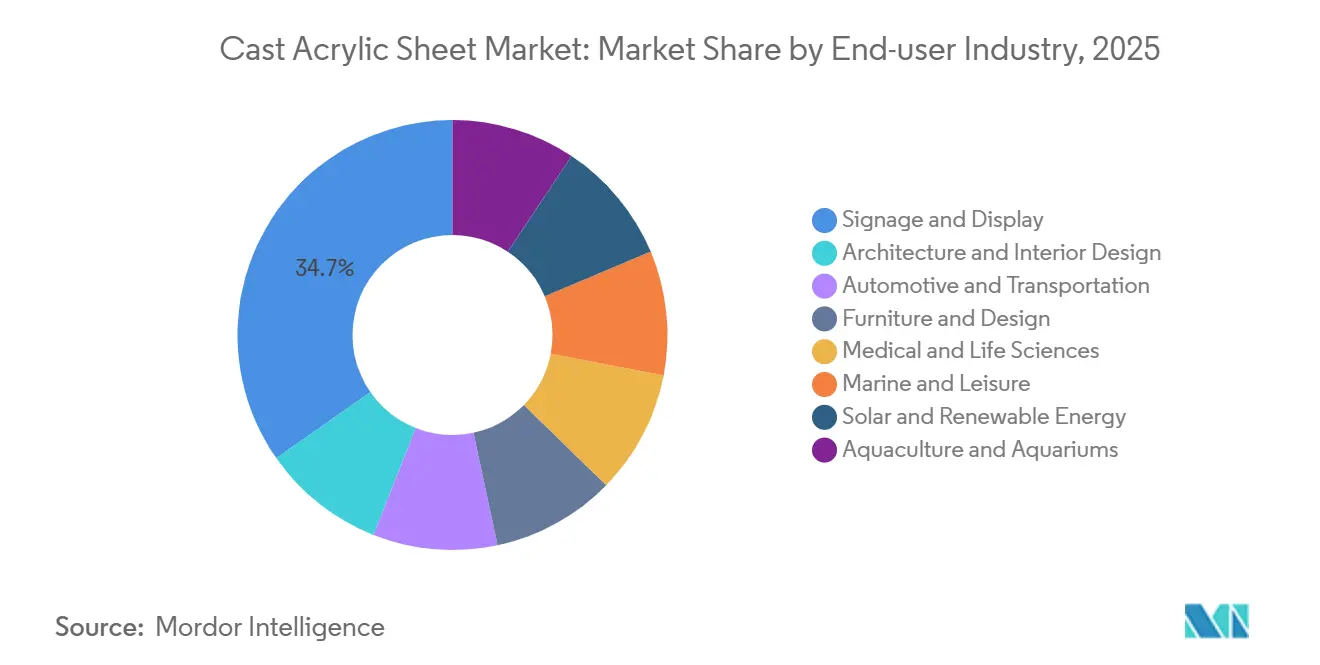

- By end-user industry, signage and display captured 34.69% of the cast acrylic sheet market share in 2025, whereas architecture and interior design are forecast to expand at a 6.89% CAGR through 2031.

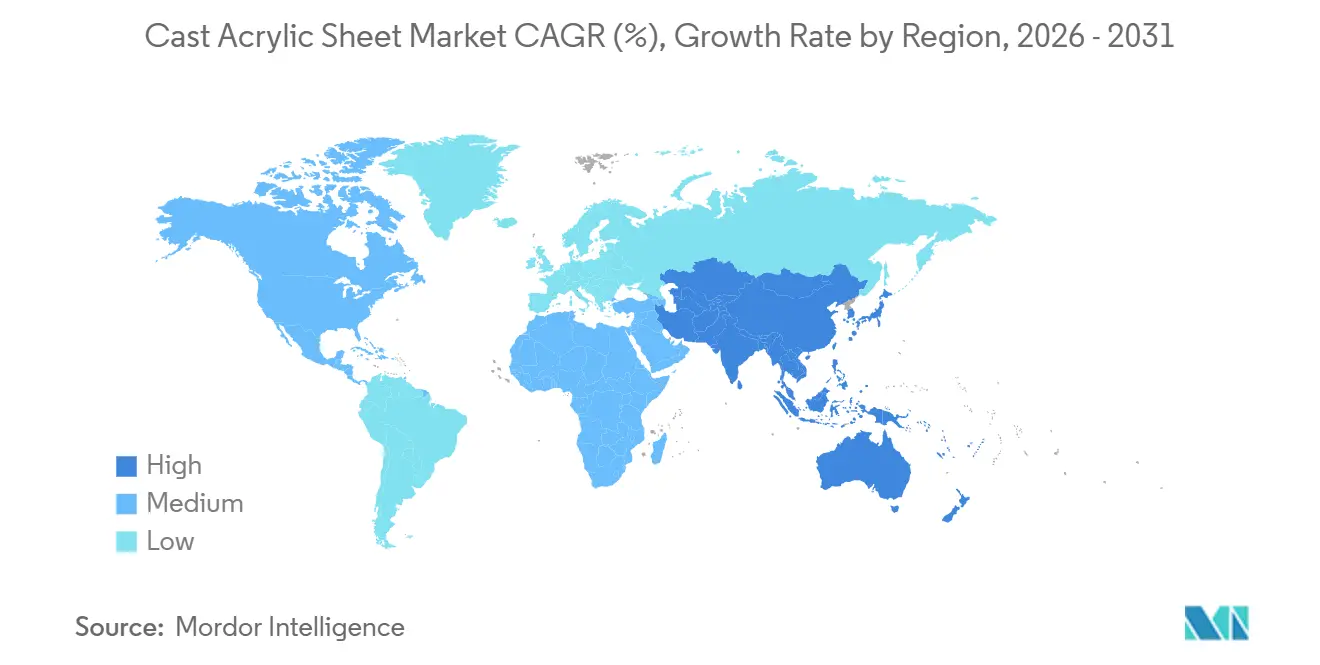

- By geography, Asia-Pacific commanded 48.02% of the cast acrylic sheet market share in 2025 and is poised for a 7.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cast Acrylic Sheet Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand in signage and display applications | +1.2% | Global, with concentration in Asia-Pacific urban centers and North America retail corridors | Medium term (2-4 years) |

| Increased glass substitution in construction and automotive | +0.9% | North America, Europe, China (green-building codes and lightweighting mandates) | Long term (≥ 4 years) |

| Rise of PoS protective screens post-COVID | +0.6% | Global, particularly high-traffic retail and hospitality in APAC and Europe | Short term (≤ 2 years) |

| Secondary glazing for BIPV and utility-scale solar farms | +0.7% | Europe (BIPV integration), India, and Middle-East (utility solar) | Long term (≥ 4 years) |

| Premium aquaculture viewing tanks adoption | +0.4% | Asia-Pacific (China, Japan, South Korea), North America coastal facilities | Medium term (2-4 years) |

| Sustainability repositioning through bio-based MMA supply | +0.5% | Europe (sustainability mandates), North America (corporate commitments) | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Growing Demand in Signage and Display Applications

Signage and display applications accounted for 34.69 of the 2025 revenue, as cast acrylic offers 92–93% light transmission and precise thickness tolerance, simplifying edge bonding. Large retail chains in Asia are transitioning from traditional PVC boards to UV-stabilized acrylic formats to comply with durability standards. Light-diffusing grades eliminate LED hot-spotting, supporting the growth of digital signage cabinets. Demand has stabilized and is now shifting from initial installations to scheduled refurbishments that incorporate anti-reflective and antimicrobial coatings. While polycarbonate remains the preferred material for high-impact applications like bus shelters, acrylic dominates in areas where optical clarity is prioritized over vandal resistance.

Increased Glass Substitution in Construction and Automotive

At half the density of glass, cast acrylic reduces dead loads in applications such as façade accents, skylight diffusers, and electric vehicle sunroofs. Impact-modified variants like DURAPLEX provide tenfold greater resistance compared to general-purpose sheets, renewing OEM interest in side-glazing concepts. Building-integrated photovoltaics increasingly specify acrylic secondary glazing to protect modules without adding structural steel weight. European embodied-carbon disclosures have slowed momentum, as cast PMMA has a carbon footprint of 4.77 kg CO₂-eq/kg, which is 27% higher than extruded sheets. Nevertheless, long-term weight savings and design flexibility continue to support its adoption.

Rise of PoS Protective Screens Post-COVID

Transparent barriers, initially introduced as temporary hygiene measures, have become permanent fixtures in retail environments. Facilities are now replacing early-generation panels with thicker, edge-polished versions that include cut-outs and pass-throughs. Anti-static and UV-blocking grades extend product lifecycles and maintain clarity under harsh lighting conditions. While most high-traffic sites completed rollouts by 2023, corporate hygiene standards ensure replacement demand follows a predictable five-to-seven-year cycle. Polycarbonate competes in vandal-prone areas but concedes clarity-critical applications to cast acrylic.

Sustainability Repositioning Through Bio-Based MMA Supply

In 2024, Evonik commercialized an ethylene-to-MMA production pathway, achieving life-cycle emissions reductions of approximately 30–50% compared to acetone cyanohydrin routes[1]Evonik Industries, “LiMA Bio-Based MMA Launch,” evonik.com. Sumitomo Chemical and Lummus Technology introduced closed-loop depolymerization processes that produce virgin-grade MMA while cutting carbon footprints by half. Early adopters of these technologies gain brand differentiation, mitigate crude oil price volatility, and align with EU product environmental footprint mandates.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in MMA and other raw-material prices | -0.8% | Global, with acute exposure in import-dependent regions (India, Southeast Asia) | Short term (≤ 2 years) |

| High-impact substitutes (polycarbonate, PETG) | -0.6% | North America and Europe (safety-glazing applications), and globally in automotive | Medium term (2-4 years) |

| Embodied-carbon scrutiny versus glass and PET | -0.4% | Europe (product-environmental-footprint mandates), North America (corporate sustainability targets) | Long term (≥ 4 years) |

| Tightening solvent-VOC emission standards in Asia | -0.3% | China, India, Southeast Asia (industrial coating and adhesive regulations) | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Volatility in MMA and Other Raw-Material Prices

Spot MMA prices ranged between USD 1.52 and USD 1.79 per kg in February 2026, impacting the already narrow EBITDA margins of 8–12% typical for mid-scale sheet producers. The cancellation of Mitsubishi Chemical’s 350-ktpa Louisiana complex in 2025 removed a potential supply buffer for North American markets. Chemical-recycling feedstock provides a partial hedge by creating alternative MMA streams that are less dependent on crude oil benchmarks.

High-Impact Substitutes (Polycarbonate, PETG)

Polycarbonate offers 250 times the impact resistance of glass, significantly outperforming acrylic's 10–20-fold advantage in safety-critical glazing applications. PETG combines near-glass clarity with lower material costs, making it a competitive option for point-of-sale trays. While impact-modified acrylics narrow the performance gap, polycarbonate suppliers are introducing abrasion-resistant coatings to address their historical weaknesses. However, acrylic remains the preferred material for medical implants and diagnostic housings, as ASTM standards restrict the use of BPA-based materials in direct-contact devices[2]ASTM International, “F3087-15 Standard for Acrylic Resins,” astm.org.

Segment Analysis

By Product Type: Specialty Grades Capture Innovation Premium

Specialty grades are anticipated to grow at a CAGR of 6.68% through 2031, adding significant value to the cast acrylic sheet market. Clear cast acrylic sheets held a 36.87% market share in 2025, driven by their established use in signage applications. Colored, patterned, and textured variants cater to decorative niches. Impact-modified DURAPLEX sheets create opportunities in mobility and machine-guard applications, while light-diffusing formulations improve LED luminaire efficiency. The availability of bio-based resins supports premium pricing strategies. Growth is also driven by co-extruded film laminates that incorporate scratch-resistant caps around impact cores, addressing demand in premium automotive interiors.

Demand for performance features has intensified competition among suppliers to patent additive packages that maintain 92–93% light transmission and Delta b ≤ 2 after 5,000 hours of Q-UV exposure. In-house color-matching centers, digital twin formulation tools, and rapid-heat-cycle mold technologies are reducing development cycles and strengthening OEM relationships. These trends reinforce the cast acrylic sheet market’s transition from a commodity-based approach to a solution-oriented focus.

By Thickness: Block Formats Serve High-Value Niches

The 5.1–10 mm thickness segment accounted for 39.88% of revenue in 2025, balancing rigidity with thermoformability. Thinner sheets (less than 5 mm) are used in disposable displays and protective covers, but face challenges due to handling fragility. For architectural partitions and mid-sized aquariums, 10.1–20 mm sheets dominate, offering stiffness without the complexity of block-grade processing. Greater than 20 mm sheets (block) are expected to grow at a CAGR of 6.72% through 2031.

Ultra-thick monoliths require 8–10-day polymerization cycles and multi-stage annealing to relieve internal stresses. Limited global production capacity results in lead times of 8–12 weeks, influencing demand planning for mega-aquariums and specialty yacht windows. Despite high unit costs, savings in structural steel and benefits in optical clarity contribute to overall system cost efficiency, ensuring the block segment’s continued relevance in the cast acrylic sheet market.

By End-user Industry: Architecture Outpaces Legacy Signage Demand

Signage and display applications accounted for 34.69% of market revenue in 2025, supported by omnichannel retail upgrades and sustained outdoor advertising investments. Automotive interiors, motorcycle windshields, and mobility glazing maintain baseline demand in the transportation sector, though safety-critical panes are predominantly made from polycarbonate. Furniture and décor applications leverage acrylic’s color fidelity and thermoformability, expanding its use in premium hospitality settings. Medical applications, such as diagnostic equipment housings and incubator panels, comply with ASTM F3087 standards, ensuring steady demand.

The architecture and interior design segment is anticipated to grow at a CAGR of 6.89% through 2031, driven by demand for façade cladding, skylight diffusers, and curved partitions. Integrated color eliminates the need for post-painting, while the material’s lower density reduces sub-frame requirements. Although embodied-carbon transparency poses challenges in European markets, recycling credits from depolymerized MMA help mitigate these issues, maintaining the market’s position in sustainable construction portfolios.

Geography Analysis

Asia-Pacific generated 48.02% of 2025 revenue and is poised for a 7.18% CAGR through 2031, supported by recycled-PMMA standards effective July 2026 that legalize post-industrial regrind feedstock. Chinese producers combine vertical MMA integration and high-capacity block casting to service aquarium megaprojects, while Japan and South Korea favor specialty light-diffusing grades for electronics backlights. India’s limited 5 ktpa domestic MMA base compels import dependence, yet rising infrastructure spend lifts signage and architectural orders and fortifies the cast acrylic sheet market in South Asia.

In North America, Plaskolite’s acquisition of the Matamoros facility and Röhm’s Wallingford expansion shorten supply chains and provide specialty-grade agility. The loss of Mitsubishi Chemical’s Louisiana MMA project, however, sustains feedstock tightness. Corporate sustainability pledges accelerate interest in depolymerized MMA, supporting future cast acrylic sheet market expansion despite raw-material headwinds.

In Europe, Germany leads regional supply after Röhm reinstated sulfuric-acid self-sufficiency and Evonik started the world’s widest PMMA co-extrusion line. Green-Deal life-cycle mandates challenge high-embodied-carbon materials, yet pilot chemical-recycling lines and bio-based MMA agreements help safeguard regional cast acrylic sheet market growth. Mediterranean yacht and aquarium builds maintain steady thick-sheet demand, balancing weaker industrial output in Eastern Europe.

Competitive Landscape

Five integrators, including Röhm, Plaskolite, Mitsubishi Chemical, 3A Composites GmbH, and PT Astari Niagara Internasional, are anchoring a moderately concentrated cast acrylic sheet market. Vertical feedstock ownership insulates EBITDA amid raw-material gyrations, while multi-regional production hedges logistics risk and supports just-in-time delivery. Röhm executed parallel expansions in Germany, the United States, and China to supply automotive interiors and medical compounding grades, reinforcing customer-proximity advantages. Evonik’s bio-MMA route delivers life-cycle value that aligns with OEM decarbonization targets, strengthening specification pull.

Trinseo’s divestment of its Mexican sheet plant to Plaskolite and the shutdown of Italian MMA output highlighted financial fragility among subscale incumbents. Plaskolite capitalized by integrating glass-clear DURAPLEX into its acquired footprint, boosting its cast acrylic sheet market presence in the Americas. Regional players in Southeast Asia court custom orders with rapid tool-change lines but remain exposed to MMA import premiums.

Strategic thrusts now focus on chemical recycling alliances, bio-based feedstock offtake, and high-impact formulations that defend acrylic against polycarbonate encroachment. Inline optical-clarity sensors and digital color-matching platforms underpin quality leadership, while advanced molding compounds create downstream synergies in specialty medical and electronics applications.

Cast Acrylic Sheet Industry Leaders

Mitsubishi Chemical Infratec Co.,Ltd.

Plaskolite

Röhm GmbH

3A Composites GmbH

PT Astari Niagara Internasional

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Arkema invested EUR 130 million to build a new acrylic acid purification unit at its Carling-Saint-Avold site in France, which is expected to become operational by 2026. This investment aimed to strengthen the supply chain for raw materials used in the cast acrylic sheet market.

- October 2025: Trinseo permanently ceased methyl methacrylate (MMA) and acetone cyanohydrin (ACH) production at its facilities in Rho and Porto Marghera, Italy. This affected the cast acrylic sheet market by reducing the availability of MMA, a critical raw material in its manufacturing process.

Global Cast Acrylic Sheet Market Report Scope

Cast acrylic sheets are high-quality, rigid thermoplastic sheets produced by pouring liquid raw material (MMA) between glass molds. They provide excellent light transparency and versatile performance. With a high molecular weight, these sheets are durable, UV-resistant, and suitable for laser cutting, fabrication, signage, and display applications.

The Cast Acrylic Sheet Market is segmented into product type, thickness, end-user industry, and geography. By product type, the market is segmented into clear cast acrylic sheet, colored cast acrylic sheet, patterned/textured cast acrylic sheet, and specialty grades. The specialty grades are further segmented into UV-resistant, anti-static, impact-modified, and light-diffusing. By thickness, the market is segmented into less than or equal to 5 mm, 5.1 – 10 mm, 10.1 – 20 mm, and greater than 20 mm (block). By end-user industry, the market is segmented into signage and display, architecture and interior design, automotive and transportation, furniture and design, medical and life sciences, marine and leisure, solar and renewable energy, and aquaculture and aquariums. The report also covers the market size and forecasts for cast acrylic sheet in 17 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Clear Cast Acrylic Sheet | |

| Colored Cast Acrylic Sheet | |

| Patterned/Textured Cast Acrylic Sheet | |

| Specialty Grades | UV-resistant |

| Anti-static | |

| Impact-modified | |

| Light-diffusing |

| Less than or equal to 5 mm |

| 5.1 – 10 mm |

| 10.1 – 20 mm |

| Greater than 20 mm (Block) |

| Signage and Display |

| Architecture and Interior Design |

| Automotive and Transportation |

| Furniture and Design |

| Medical and Life Sciences |

| Marine and Leisure |

| Solar and Renewable Energy |

| Aquaculture and Aquariums |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product Type | Clear Cast Acrylic Sheet | |

| Colored Cast Acrylic Sheet | ||

| Patterned/Textured Cast Acrylic Sheet | ||

| Specialty Grades | UV-resistant | |

| Anti-static | ||

| Impact-modified | ||

| Light-diffusing | ||

| By Thickness | Less than or equal to 5 mm | |

| 5.1 – 10 mm | ||

| 10.1 – 20 mm | ||

| Greater than 20 mm (Block) | ||

| By End-user Industry | Signage and Display | |

| Architecture and Interior Design | ||

| Automotive and Transportation | ||

| Furniture and Design | ||

| Medical and Life Sciences | ||

| Marine and Leisure | ||

| Solar and Renewable Energy | ||

| Aquaculture and Aquariums | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the Cast Acrylic Sheet Market?

The Cast Acrylic Sheet Market stands at USD 4.05 billion in 2026 and is expected to reach USD 5.39 billion by 2031.

Which region leads revenue in 2025?

Asia-Pacific contributes 48.02% of global revenue in 2025.

Which thickness segment is growing fastest through 2031?

Greater than 20 mm (block) are forecast to post a 6.72% CAGR through 2031 owing to aquarium and marine uptake.

How are producers lowering carbon footprints?

They are adopting bio-based MMA routes, chemical-recycling feedstock, and energy-efficient casting lines.

Page last updated on: