Cannabis Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 45 Billion |

| Market Size (2031) | USD 86.60 Billion |

| Growth Rate (2026 - 2031) | 14.00% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Cannabis Market Analysis by ���ϲ�����

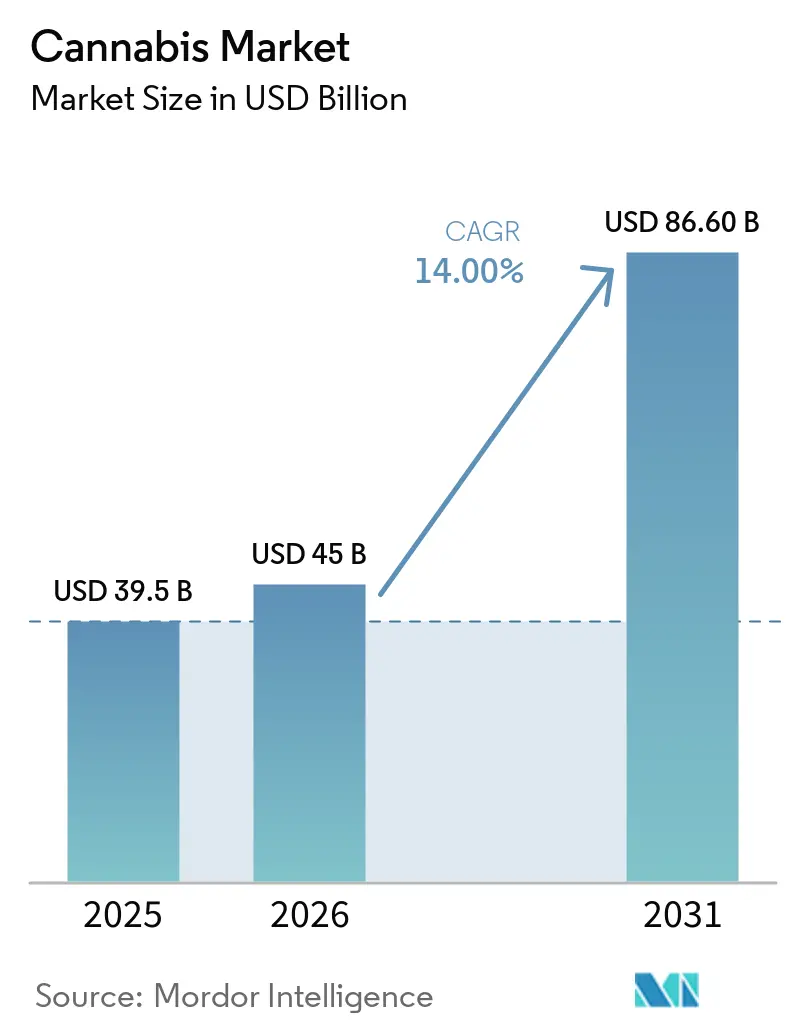

The cannabis market size is valued at USD 39.5 billion in 2025 and is anticipated to grow from USD 45.0 billion in 2026 to USD 86.6 billion by 2031, at a CAGR of 14.0% from 2026 to 2031. The cannabis market is increasingly driven by regulatory developments, which are reshaping cash flow, capital access, and market entry conditions more rapidly than shifts in consumer demographics. The United States Drug Enforcement Administration's (DEA) reclassification of state-licensed medical marijuana from Schedule I to Schedule III on April 22, 2026, removed the Section 280E tax burden, unlocking USD 1.6 billion to USD 2.2 billion in annual capital. Similarly, Europe is advancing regulatory frameworks, with Germany’s Cannabis Act effective from April 2024 and France notifying the European Commission in March 2025 of its plans to commercialize medical cannabis. These reforms are accelerating regulatory alignment, compelling operators to focus on licensed market timing, pharmaceutical-grade compliance, and distribution access rather than cultivation output. However, execution risks remain, as operators must secure banking access, establish cross-border clarity, and ensure compliant patient-acquisition channels to convert these regulatory advancements into sustainable profitability. The evolving regulatory landscape underscores the need for strategic adaptation to achieve long-term success in the cannabis market.

Key Report Takeaways

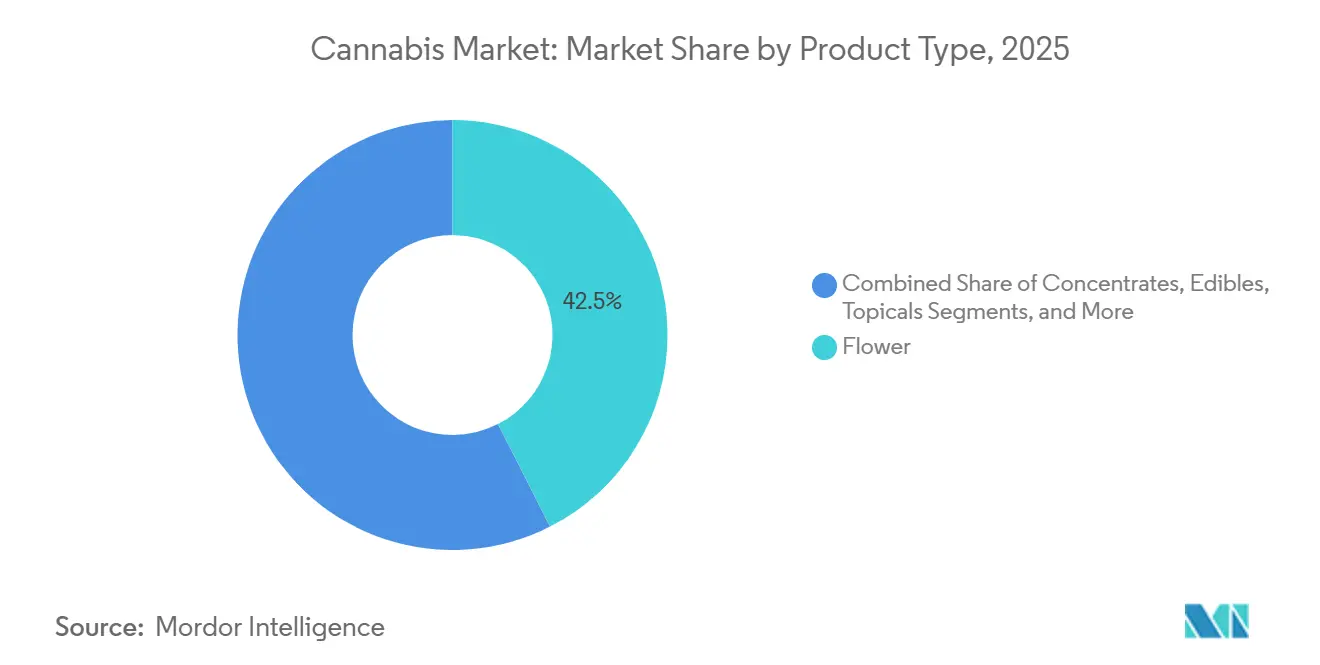

- By product type, flower was the largest segment, accounting for 42.5% of the cannabis market share in 2025, while beverages were the fastest-growing segment, with a 14.6% CAGR over 2026-2031.

- By usage, medical cannabis was the largest segment with 56.8% of cannabis market share in 2025, while adult-use was the fastest segment at 14.4% CAGR over 2026-2031.

- By compound, THC-dominant products were the largest segment with 63.0% of the cannabis market size in 2025, while CBD-dominant products were the fastest segment at 14.5% CAGR over 2026-2031.

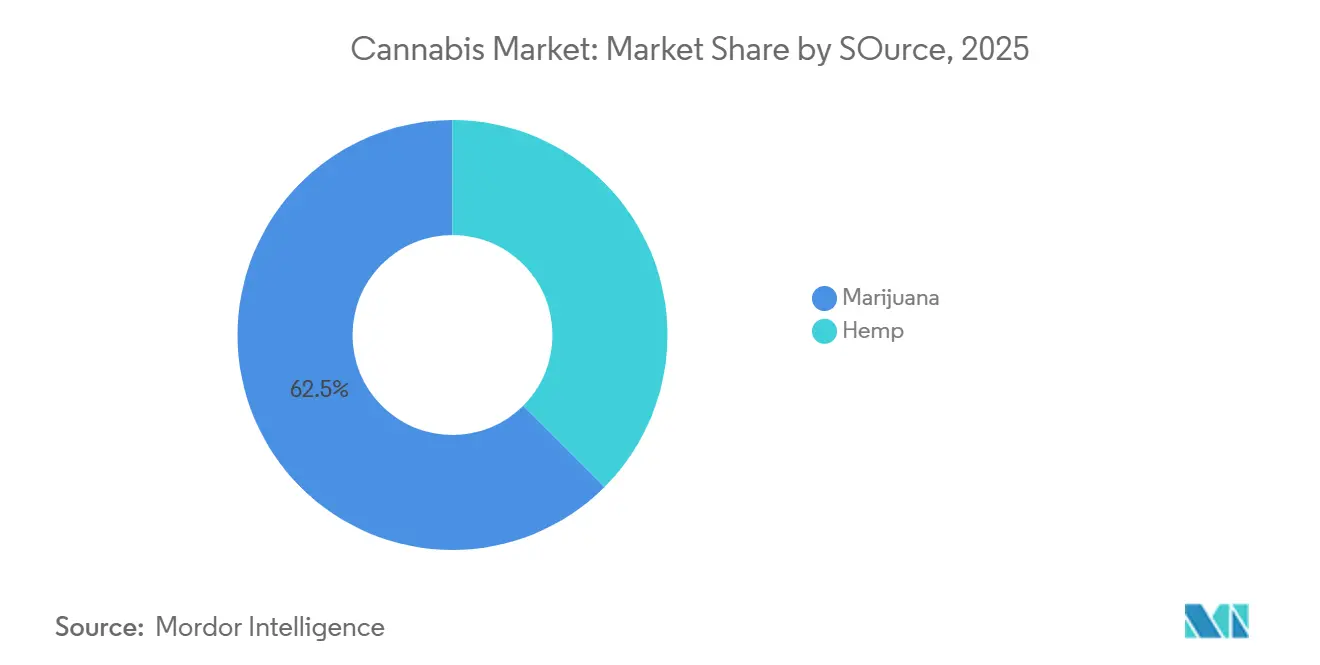

- By source, Marijuana held the largest share, accounting for 62.5% of the cannabis market size in 2025, whereas Hemp posted the fastest 14.90% CAGR through 2026-2031.

- By distribution channel, dispensaries were the largest segment, accounting for 58.1% of cannabis market share in 2025, while online direct-to-consumer was the fastest-growing segment, with a 14.2% CAGR over 2026-2031.

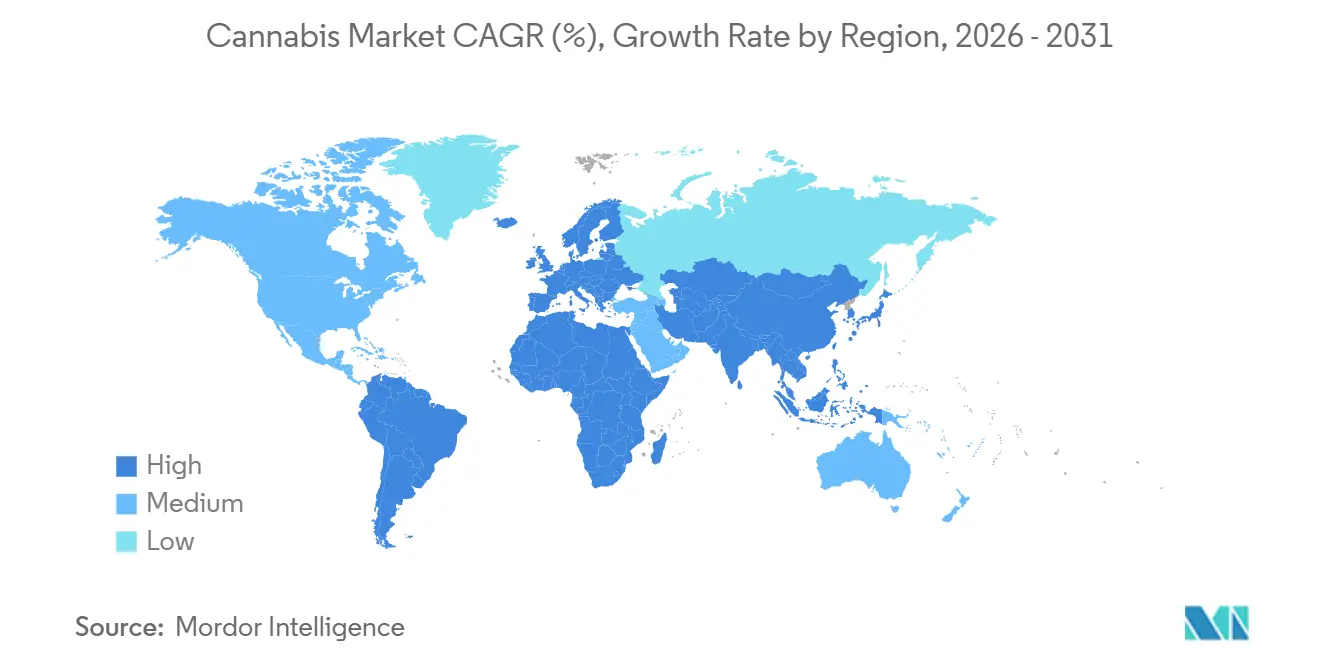

- By geography, North America was the largest region with 73.0% share in the cannabis market size in 2025, while Asia-Pacific was the fastest region with 14.8% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cannabis Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding adult-use and medical legalization | +3.8% | Global, with the strongest relevance in the United States, Germany, Brazil, and Colombia, where legal reform is directly widening regulated demand and investment activity | Short term (≤ 2 years) |

| Rising prescription use for chronic pain and neurological symptoms | +2.9% | North America, Europe, and Asia-Pacific, where clinical adoption is moving through physician channels and specialist prescribing pathways | Medium term (2-4 years) |

| Product innovation in edibles, beverages, and precision-dose formats | +2.4% | North America and Europe, with spillover into Australia and Israel, as regulated formats broaden beyond flower | Short-term (≤ 2 years) and medium-term (2-4 years) |

| Premiumization toward high-potency flower and concentrates | +1.7% | North America, with early regulated uptake in Germany, as potency and quality influence pharmacy and adult-use product mix | Short-term (≤ 2 years) and medium-term (2-4 years) |

| Digital prescribing and telehealth workflows are reducing access friction | +1.3% | Germany, Australia, the United Kingdom, Poland, and Israel, where remote access has widened the patient funnel in regulated medical channels | Medium term (2-4 years) |

| European Union Good Manufacturing Practice (EU-GMP) manufacturing expansion and improving pharmacy-channel supply | +1.1% | Europe, especially Germany, Portugal, and Malta, with additional relevance for Australia and the United Kingdom through import-linked pharmacy supply chains | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Expanding Adult-Use and Medical Legalization

The Drug Enforcement Administration's (DEA) rescheduling of medical marijuana from Schedule I to Schedule III, effective April 22, 2026, is projected to result in estimated annual tax relief of USD 1.6 billion to USD 2.2 billion for licensed medical operators, which is anticipated to drive growth and further expansion of adult-use markets. Legal reforms are reshaping the cannabis market by influencing tax policies, licensing incentives, and investor behavior beyond demographic demand. The April 2026 DEA rescheduling decision reduced taxes for state-licensed medical operators while enhancing the federal legitimacy of the United States medical cannabis market, encouraging institutional capital re-engagement. In Europe, Germany’s Cannabis Act (effective April 1, 2024) and France’s March 2025 notification to the European Commission demonstrate progress in regulatory convergence. This convergence underscores the importance of aligning with legal timelines and favoring operators with compliant production and import capabilities and established medical distribution networks. As more countries adopt Germany’s model and related frameworks, companies meeting pharmaceutical standards are poised to gain a competitive edge, driving the market toward greater regional harmonization.

Rising Prescription Use for Chronic Pain and Neurological Symptoms

The cannabis market is gaining momentum as a growing body of medical evidence reduces physician hesitation. A 2025 randomized study in PAIN found that medical cannabis users were 2.6 times more likely to achieve meaningful pain relief than those using prescription medications, alongside a 39.3% reduction in morphine milligram equivalent dosage. Similarly, research in JAMA Internal Medicine linked New York’s medical cannabis program to a 22% reduction in opioid prescribing over 18 months, highlighting economic benefits for payers and health systems. Long-term evidence from a five-year study in Biomedicines showed a decline in Brief Pain Inventory scores for patients with diabetic neuropathy from 9.0 to 2.0, addressing concerns of conservative prescribers. Together, these findings are driving the cannabis market toward formal prescribing pathways, repeat usage, and reimbursement frameworks, reducing its reliance on consumer advocacy.

Product Innovation in Edibles, Beverages, and Precision-Dose Formats

The cannabis market is evolving as newer formats address challenges of uncertain onset and dosing. Nano-emulsification has reduced THC beverage onset times, making them more suitable for social and session-based use. This shift is reflected in the planned rollout of lower-dose beverage lines in 2025 and 2026, signaling their emergence as a core product category. Concurrently, innovations such as Curaleaf’s QMID metered-dose inhaler, authorized in the United Kingdom and Germany, are establishing pharmaceutical-grade delivery systems that enhance access to regulated medical markets. These advancements collectively drive innovation-led revenue growth, though the increasing focus on beverages and devices may pressure margins for operators without proprietary technologies, underscoring the importance of innovation in sustaining market competitiveness.

Premiumization Toward High-Potency Flower and Concentrates

The cannabis market has increasingly shifted toward potency-focused consumption, particularly in mature North American markets where value is assessed by psychoactive effect per dollar. A 2025 National Geographic report highlighted that live sauce products can contain around 70% THC, crystalline isolate diamonds can exceed 85% THC, and premium flower typically ranges between 20% and 25% THC. This shift is reflected in the declining share of medical flowers in the United States, which fell from about 70% in 2014 to 40% by 2025, confirming a structural change in consumer preferences. Consequently, operators that prioritized cultivation over extraction now face weaker pricing and reduced profitability for standard flower and commodity products. However, Germany demonstrates that regulatory frameworks can influence market dynamics, as early pharmacy demand continues to sustain premium pricing for compliant indoor flower. This highlights how potency and regulatory settings together shape value capture in the cannabis market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Banking, tax, and interstate commerce barriers | -3.0% | North America, especially the United States, where federal inconsistency keeps financial access and operating efficiency below consumer-sector norms | Short-term (≤ 2 years) and medium-term (2-4 years) |

| Advertising, packaging, and claims restrictions | -1.2% | Global, with acute relevance in Canada, Australia, Germany, and the United Kingdom, where compliant brand communication is tightly constrained | Medium term (2-4 years) |

| Pharmaceutical-grade compliance bottlenecks and batch-release delays | -0.8% | Europe, especially Germany, Malta, and Portugal, along with Israel, where regulated medical supply depends on validated manufacturing and release systems | Medium term (2-4 years) and Long term (≥ 4 years) |

| Cross-border tariff and import-policy volatility | -0.5% | Israel, Canada, Germany, and Australia, where imports remain important to supply balance, and policy change can alter landed cost quickly | Short-term (≤ 2 years) and medium-term (2-4 years) |

| Source: ���ϲ����� | |||

Banking, Tax, and Interstate Commerce Barriers

The cannabis market in the United States remains inefficient due to incomplete federal reform, even after the April 2026 rescheduling to Schedule III. While medical cannabis operators gained tax relief, the recreational market continues to face inconsistent regulations and restricted access to banking, credit, and insurance services, driving up operational costs. Interstate commerce barriers further intensify these inefficiencies, requiring multi-state operators to replicate production facilities across states rather than centralize operations. These combined challenges hinder the market's ability to achieve scale benefits, underscoring the need for unified federal reforms to unlock its full growth potential.

Advertising, Packaging, and Claims Restrictions

The cannabis market faces slower growth when brands are restricted in communicating product use and benefits. Countries such as Canada, Australia, and Germany enforce distinct regulations on branding, promotion, and health-related messaging, requiring operators to manage multiple compliance frameworks. These restrictions limit smaller brands, as key customer-acquisition channels, particularly digital platforms, are either heavily restricted or inaccessible. Larger retail chains and established dispensary networks, however, leverage shelf presence, in-store traffic, and staff interactions to maintain their market position. This dynamic slows brand development, weakens consumer exposure to innovation, and reduces pricing competition, ultimately reinforcing the dominance of incumbent players.

Segment Analysis

By Product Type: Beverage Growth Undercuts Flower's Long-Run Dominance

In 2025, flower accounted for 42.5% of the cannabis market share, maintaining its position as the largest segment and the primary entry format in both medical and adult-use channels due to its familiarity, ease of use, and availability. However, the cannabis market in mature North American states is structurally shifting away from flower, with pre-rolls emerging as a practical alternative that retains much of flower’s appeal while eliminating preparation efforts, particularly for first-time adult-use consumers.

Non-combustible formats such as edibles and capsules remain essential for clinical users prioritizing measured consumption, while topicals and transdermals are gaining traction in medical applications due to fewer regulatory barriers and suitability for specific treatments. Beverages, however, are driving the fastest growth, with a projected CAGR of 14.6% from 2026 to 2031, fueled by advancements in faster-onset technology and their positioning as alcohol alternatives. This shift highlights a growing divide between companies innovating with proprietary formats and those reliant on undifferentiated flower pricing, signaling a long-term transformation in consumer preferences and market dynamics.

By Usage: Adult-Use Momentum Pressures Medical-Channel Unit Economics

Medical cannabis, accounting for 56.8% of the cannabis market share in 2025 by usage, remains the largest segment due to established state programs, physician pathways, and pharmacy-based access models. Its significance lies in stronger repeat behavior, structured referral patterns, and lower customer-acquisition costs than in adult-use retail. Features such as physician oversight, potential reimbursement, and robust patient data collection further solidify its role. Meanwhile, the wellness and nutraceutical segment, driven by CBD-based products, shows potential but faces growth limitations due to regulatory constraints. This underscores the medical segment's critical role in providing stability as adult-use channels expand.

Adult-use cannabis, with a projected CAGR of 14.4% over 2026-2031, is the fastest-growing segment, driven by the transition of illicit purchases into licensed channels. However, much of this growth reflects the formalization of existing consumption rather than new demand. As the initial conversion stabilizes, operators may face challenges in sustaining growth, requiring improved product offerings, retail execution, and disciplined capital allocation. Despite the rapid growth of adult-use, the cannabis market's reliance on the medical segment persists, as its structured and stable economics provide a foundation that open retail competition alone cannot match. Together, these dynamics highlight the interdependence of medical stability and adult-use growth in shaping the market's future.

By Compound: Minor Cannabinoids Are the Next Formulary Frontier

THC-dominant products, which held 63.0% of the cannabis market share in 2025, remain the largest category, driven by their established psychoactive efficacy and a stronger evidence base compared to newer cannabinoids. A 2025 systematic review supported by the Agency for Healthcare Research and Quality highlighted that an oral THC-to-CBD spray moderately improved chronic pain severity compared to a placebo, reinforcing the case for regulated medical use and formulary inclusion[1]Source: National Center for Biotechnology Information, “Living Systematic Review Supported by the Agency for Healthcare Research and Quality,” National Library of Medicine, ncbi.nlm.nih.gov . This reliance on THC-led formats underscores their scalability and clinical credibility, particularly in structured medical systems requiring robust evidence. Balanced THC and CBD formulations further complement this demand, addressing anxiety, sleep, and pain where single-compound products may not suffice.

CBD-dominant products are the fastest-growing segment, with a projected CAGR of 14.5% from 2026 to 2031, supported by expanding pharmacy retail, wellness products, and low-THC regulatory frameworks. These developments are particularly relevant in markets with strict THC thresholds, enabling broader sales outside controlled-substance channels. Simultaneously, interest in minor cannabinoids such as CBG, CBN, and THCV signals a shift toward targeted functionality, differentiated formulations, and clearer clinical applications. This evolving focus suggests a transition from broad cannabinoid branding to a segmented strategy aligned with specific patient needs and precise dosing expectations, positioning minor cannabinoids as a pivotal component in the future of the cannabis market.

By Source: Hemp's Regulatory Ambiguity Creates a Structural Compliance Asymmetry

Marijuana, accounting for 62.5% of the cannabis market size in 2025, highlights the sustained demand for high-THC products driven by established cultivation systems in North America and evolving pharmaceutical frameworks in Europe and Israel. Key markets such as the United States, Canada, and Germany anchor this dominance, particularly in medical and adult-use systems where controlled potency and formal licensing are critical. The market share of marijuana-derived products remains closely tied to legal structures governing prescription access, dispensary operations, and compliant supply chains.

Hemp, projected to grow at a 14.9% CAGR from 2026 to 2031, is rapidly expanding due to its role in lower-THC formats and as a feedstock for CBD and other cannabinoids. Its growth benefits from lighter regulatory requirements and agricultural scalability, especially in regions with stricter marijuana cultivation laws. However, regulatory inconsistencies create a competitive gap, as hemp-derived products often face lower compliance costs. Over time, clearer regulations are projected to reduce this disparity. Together, marijuana's established dominance and hemp's rapid growth reflect a cannabis market evolving under diverse regulatory and compliance frameworks, with both sources shaping the industry's future trajectory.

By Distribution Channel: Digital Channels Erode Dispensary Gatekeeping Power

Dispensaries accounted for 58.1% of the cannabis market by distribution channel in 2025, reflecting their central role in age-verification, product testing, tax collection, and staff-assisted purchasing under legalization frameworks. Their dominance is further supported by a wide product selection and local accessibility, particularly in high-density areas where customers value reliable assortments and in-person guidance. However, pharmacies are emerging as key players in countries such as Germany, Australia, the United Kingdom, and Israel, where medical cannabis is integrated into established pharmaceutical systems. Meanwhile, mass retail remains limited to CBD and hemp-derived products due to the exclusion of full-spectrum THC products from mainstream networks.

Online direct-to-consumer channels, with a projected CAGR of 14.2% from 2026 to 2031, are reshaping the market by leveraging telehealth prescribing and home delivery to challenge the traditional dominance of dispensaries. Delivery services, particularly in urban markets, offer lower costs and greater convenience, drawing demand away from physical storefronts. This shift highlights a growing advantage for asset-light entrants, as digital growth reduces the reliance on extensive dispensary networks. Consequently, brand strength, compliance systems, and logistics execution are becoming more critical than store count. As regulations increasingly support delivery and remote access, the bargaining power of large dispensary chains is anticipated to weaken, signaling a significant transformation in the cannabis market's distribution dynamics.

Geography Analysis

In 2025, North America dominated the cannabis market with a 73.0% share, driven by the United States' extensive multi-state operator base and Canada's mature retail system. However, growth in the region is anticipated to slow as legalization-led opportunities have largely been realized. Future expansion will depend on federal reforms, interstate commerce regulations, and consolidation strategies. In contrast, Europe is emerging as a key growth region, with Germany advancing medical access and France signaling broader policy changes, indicating a shift towards a more integrated market.

The Asia-Pacific region, with a projected CAGR of 14.8% from 2026 to 2031, is the fastest-growing segment, though growth is concentrated in regulated medical systems. Australia plays a pivotal role, supported by updates to the Authorized Prescriber framework in December 2025 that bolster the prescription channel[2]Source: Therapeutic Goods Administration, “Authorised Prescriber Scheme Update,” Therapeutic Goods Administration, tga.gov.au . Significant demand is evident, with Australians spending AUD 400 million (USD 260 million) on medicinal cannabis in the first half of 2024, despite the market's reliance on imports. Similarly, South America, with a projected CAGR of 13.6% over 2026-2031, is building its regulated supply framework, led by Colombia and Brazil. Colombia's recognition of cannabis flower as a medicinal product and Brazil's regulatory advancements in 2026 are anticipated to strengthen compliance and production capabilities, driving regional growth[3]Source: Secretaria de Comunicação Social, “Medicinal Cannabis Production Resolutions RDC 1012-1015/2026,” gov.br, gov.br .

In the Middle East, Israel remains the primary driver due to its regulated medical framework, though reliance on imports makes the market sensitive to trade policies. Africa's growth is led by South Africa, Morocco, and Lesotho, leveraging cultivation potential and export-oriented medical cannabis. Morocco and Lesotho are particularly significant for integrating into regulated export supply chains, aligning with global trends of expanding medical access and stricter quality standards. Together, these regional developments highlight a global cannabis market transitioning from initial legalization phases to a more structured and regulated growth trajectory.

Competitive Landscape

The cannabis market remains highly fragmented, with the top five operators by revenue holding only a limited share, preventing any single company from influencing pricing across regions. Companies such as Curaleaf Holdings, Trulieve Cannabis Corp., and Green Thumb report significant sales but lack dominant market presence, highlighting a competitive landscape driven by regional density, compliant supply chains, and channel control. This fragmentation has led to recurring strategic themes, including state-level consolidation in the United States, expansion into European pharmacy channels, and diversification into beverages and precision-dose formats to counter deflation in flower prices.

Recent strategic moves underscore the varied approaches shaping the market. In May 2026, Curaleaf acquired Four 20 Pharma in Germany, strengthening its pharmacy-led medical channel and European distribution. Aurora Cannabis, in April 2026, acquired Safari Flower Company for USD 26.5 million, adding a certified cultivation facility in Ontario to boost European exports. Meanwhile, Green Thumb Industries expanded its U.S. retail network to 113 stores in 2025, focusing on disciplined growth. These actions reflect a market where operators tailor strategies, whether through retail expansion, pharmaceutical exports, or portfolio diversification, based on regional legal and market conditions.

Unsettled areas in the market present opportunities for long-term advantage. Pharmaceutical-grade precision dosing offers potential through clinical validation and delivery control, while digital patient infrastructure can reduce costs via compliant intake, prescribing support, and telehealth-led fulfillment. Additionally, the shift toward robust operational systems, emphasizing seed-to-sale traceability and data-driven cultivation, is becoming critical. Companies that align regulatory compliance with targeted strategies are better positioned to succeed, as the market evolves beyond reliance on cultivation volume or broad retail exposure.

Cannabis Industry Leaders

Curaleaf Holdings, Inc.

Trulieve Cannabis Corp.

Green Thumb Industries Inc.

Verano Holdings Corp.

Cresco Labs Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Curaleaf Holdings completed the full acquisition of Four 20 Pharma GmbH in Germany, consolidating an EU-GMP-certified production and clinic network and establishing direct access to Germany's pharmacy channel for medical cannabis products.

- April 2026: Aurora Cannabis acquired Safari Flower Company for USD 26.5 million, including USD 15 million in cash, gaining a 59,000-square-foot EU-GMP-certified cultivation facility in Ontario that strengthens Aurora's pharmaceutical-grade export capacity for European pharmacy markets.

- February 2026: Brazil's Agência Nacional de Vigilância Sanitária (ANVISA) published four regulatory resolutions, RDC 1012-1015/2026, establishing the first comprehensive domestic production framework for medicinal cannabis in South America's largest pharmaceutical market.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global cannabis market as the value of legally cultivated, processed, and traded flower, concentrates, infused edibles and beverages, topicals, and prescription-grade formulations that contain cannabinoids sourced from Cannabis sativa or indica. Values are recorded at wholesale-equivalent prices and cover medical, adult-use, and wellness channels worldwide.

Scope Exclusions: hemp fiber, industrial hempseed, illicit trade, vaping hardware, and cultivation equipment are not included.

Segmentation Overview

- By Product Type

- Flower

- Pre-Rolls

- Concentrates

- Edibles

- Beverages

- Topicals and Transdermals

- Tinctures and Sublinguals

- Capsules and Softgels

- By Usage

- Medical

- Adult-Use / Recreational

- Wellness and Nutraceutical

- By Compound

- THC-Dominant

- CBD-Dominant

- Balanced THC/CBD

- Minor Cannabinoids

- By Source

- Marijuana

- Hemp

- By Distribution Channel

- Dispensaries

- Pharmacies

- Online Direct-to-Consumer

- Delivery Services

- Mass-Market Retail

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- South America

- Brazil

- Colombia

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Netherlands

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- Australia

- Thailand

- Japan

- South Korea

- New Zealand

- Rest of Asia-Pacific

- Middle East

- Israel

- Turkey

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Lesotho

- Morocco

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Analysts speak with regulators, licensed growers, dispensary managers, clinicians, and supply-chain auditors across North America, Europe, Latin America, and Asia-Pacific. Their insights on wholesale pricing, patient onboarding, and upcoming rule changes help us stress-test secondary findings and calibrate forecast drivers.

Desk Research

We review open datasets from agencies such as the US FDA, Health Canada, Germany's BfArM, UN Comtrade, and Eurostat to map production, trade, and patient uptake. Industry bodies like the Canadian Cannabis Council and the European Industrial Hemp Association supply licensing and retail statistics, while peer-reviewed journals track prescription trends. Company 10-Ks, state excise-tax ledgers, and news feeds from Dow Jones Factiva and D&B Hoovers refine price and capacity signals. The sources named are illustrative; many more were consulted for validation and context.

Market-Sizing and Forecasting

We begin with a top-down build that multiplies adult-use participation rates and registered patient counts by average spend per buyer, then benchmark results against sampled ASP times legal volume data from public filers. Key variables tracked include cultivation licenses issued, retail price per gram, chronic-pain prevalence, average THC potency, and excise-tax shifts. A multivariate regression links these indicators to historic market value, while selective bottom-up supplier roll-ups act as guardrails, and gap-filling relies on region-specific price-elasticity factors vetted in expert calls.

Data Validation and Update Cycle

Outputs pass an anomaly screen, peer review, and senior sign-off. We refresh models every year and trigger interim updates after landmark legalization votes or supply shocks, so clients always receive the latest vetted baseline.

Why Mordor's Cannabis Baseline Commands Reliability

Published estimates often diverge because firms vary in scope, price normalization, and refresh cadence.

Key gap drivers include some publishers folding in packaging or grow-light revenues, others adding hemp-derived CBD, and several using retail receipts without netting taxes, which inflates totals that Mordor analysts purposely keep aligned with wholesale equivalence.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 44.6 B | ���ϲ����� | |

| USD 72.8 B | Global Consultancy A | Includes accessories and retail markups |

| USD 59.6 B | Industry Association B | Combines cannabis with hemp-CBD and assumes uniform legalization |

These contrasts show that Mordor's disciplined scope setting, price normalization, and annual refresh create a transparent, repeatable baseline that decision-makers can trust.

Key Questions Answered in the Report

What is the 2026 size of the cannabis sector?

The cannabis market stands at USD 45.0 billion in 2026 and is projected to reach USD 86.6 billion by 2031, growing at a 14.0% CAGR over 2026-2031.

Which region leads global revenue for cannabis in 2025?

North America was the largest regional segment, accounting for 73.0% of global revenue in 2025, supported by the United States' multi-state operator base and Canada's mature retail network.

Which region is expanding the fastest over 2026-2031?

Asia-Pacific is the fastest-growing regional segment, with a 14.8% CAGR over 2026-2031, led mainly by Australia's prescription channel and selective medical advances across the region.

Which product category leads sales, and which one grows the fastest?

Flower was the largest product type with a 42.5% share in 2025, while beverages are the fastest-growing product type at a 14.6% CAGR over 2026-2031, as faster-onset and lower-dose formats gain ground.

Why is regulation so important for a cannabis company's strategy?

Regulation directly affects tax treatment, banking access, medical prescribing, and cross-border trade, which means legal timing often shapes profitability and market entry more than cultivation capacity alone.

How concentrated is competition among the top cannabis companies?

Competition is highly fragmented because the top 5 operators accounted for only 12.97% of global revenue in 2025, so no company had broad pricing authority across geographies.

Page last updated on: