Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

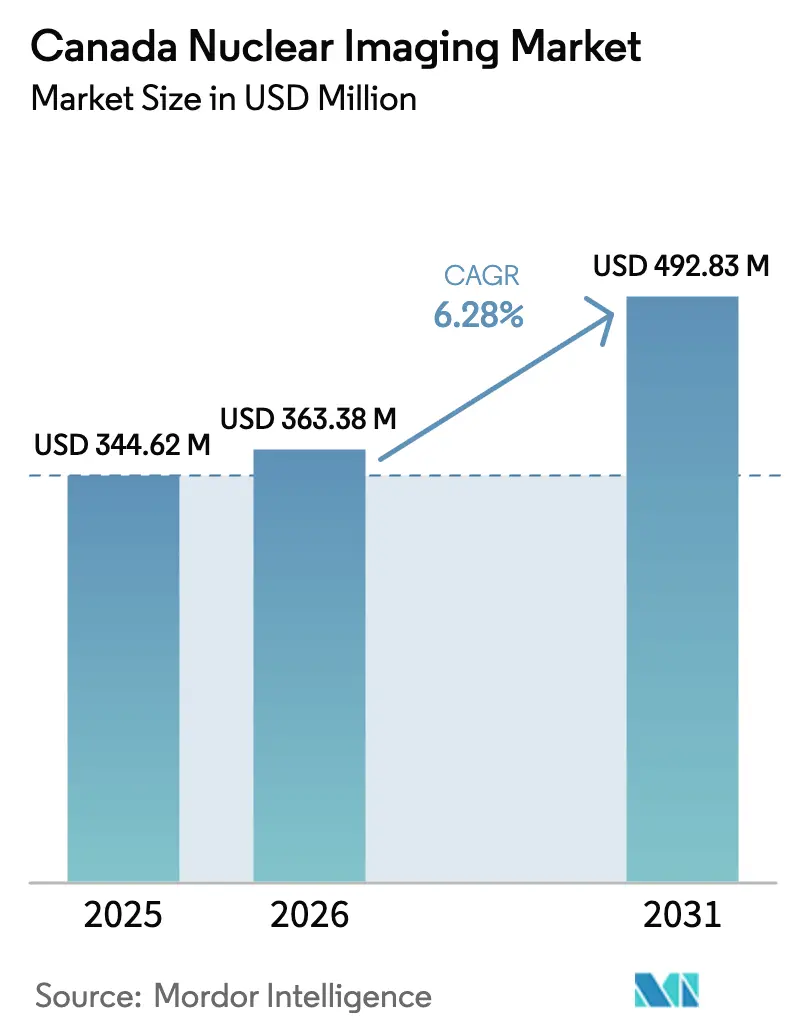

| Base Year Market Size (2025) | USD 344.62 Million |

| Market Size (2026) | USD 363.38 Million |

| Market Size (2031) | USD 492.83 Million |

| Growth Rate (2026 - 2031) | 6.28% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Canada Nuclear Imaging Market Analysis by ���ϲ�����

The Canada Nuclear Imaging Market size is projected to expand from USD 344.62 million in 2025 and USD 363.38 million in 2026 to USD 492.83 million by 2031, registering a CAGR of 6.28% between 2026 to 2031.

Escalating cancer and cardiovascular disease prevalence, widening access to hybrid scanners, and sizeable provincial investments in cyclotron capacity continue to lift procedure volumes. Hybrid PET/CT retains the largest revenue share, yet hybrid PET/MR is advancing most rapidly as academic centers pursue simultaneous metabolic, functional, and structural imaging. Software platforms underpinned by artificial-intelligence reconstruction are expanding faster than hardware because hospitals are looking for productivity gains that offset technologist shortages. At the same time, distributed isotope production initiatives in Ontario, British Columbia, and Alberta are tempering the single-point-of-failure risk that followed the 2018 closure of the National Research Universal reactor.

Key Report Takeaways

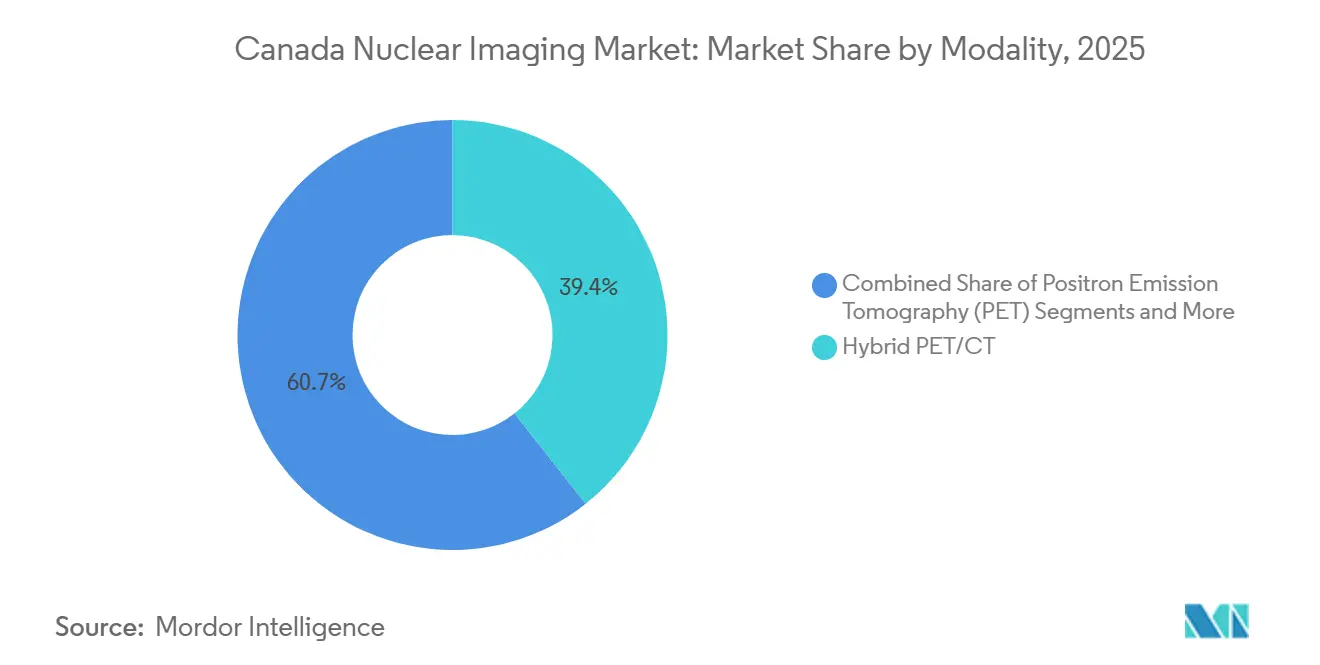

- By modality, hybrid PET/CT held 39.35% revenue share in 2025, while hybrid PET/MR is projected to record the fastest 10.24% CAGR through 2031.

- By component, equipment captured 63.63% of revenue in 2025, whereas software platforms are forecast to expand at a 9.57% CAGR to 2031.

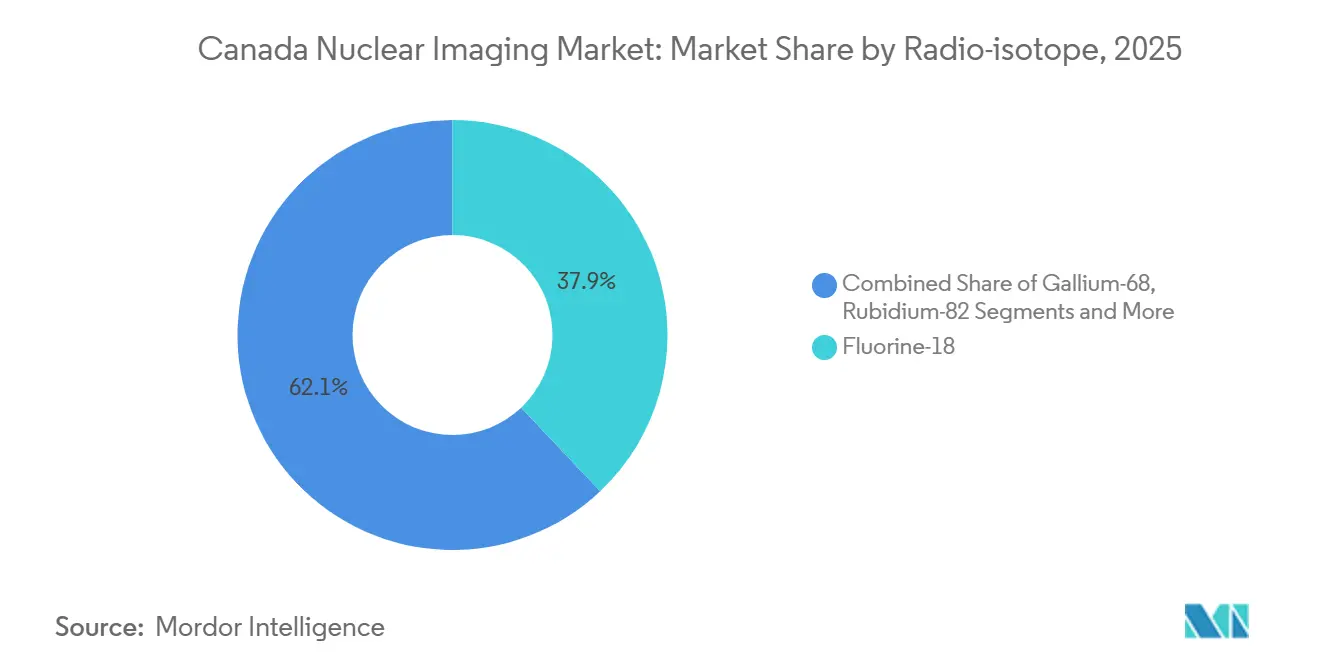

- By radio-isotope, fluorine-18 commanded 37.94% revenue share in 2025 and gallium-68 is on track for a 10.33% CAGR through 2031.

- By application, oncology led with 52.68% revenue share in 2025, while neurology is set to grow at an 8.29% CAGR through 2031.

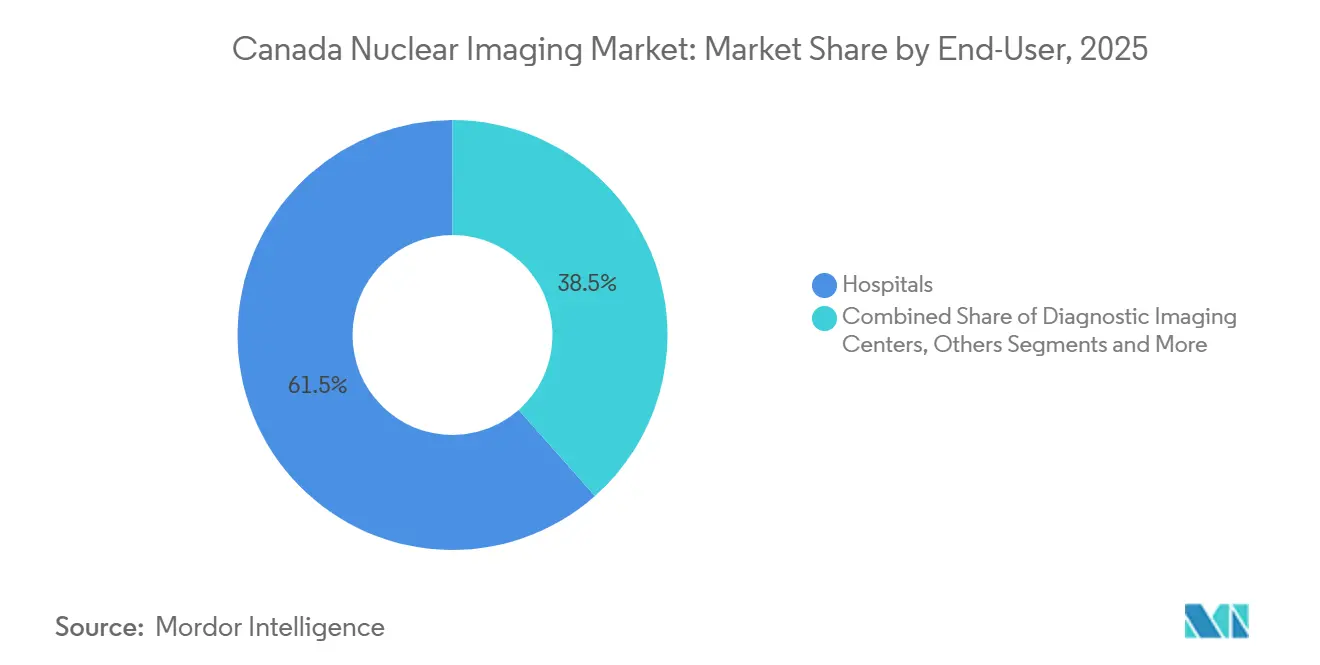

- By end user, hospitals generated 61.53% of revenue in 2025 and academic and research institutes are expected to post the highest 8.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Canada Nuclear Imaging Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing prevalence of cancer and CVD | +1.8% | Ontario, Quebec, British Columbia | Long term (≥ 4 years) |

| Rising adoption of hybrid PET/CT & SPECT/CT | +1.5% | Academic hubs in Toronto, Montreal, Vancouver, Calgary | Medium term (2-4 years) |

| Government investments in radiopharma supply | +1.2% | British Columbia, Alberta, Ontario | Medium term (2-4 years) |

| Digital detector innovations lowering dose | +0.9% | Early adopters in Nova Scotia, British Columbia | Short term (≤ 2 years) |

| Expansion of non-F-18 cyclotron isotopes | +0.7% | Vancouver, Toronto, Montreal academic centers | Long term (≥ 4 years) |

| U.S.–Canada border medical-tourism demand | +0.3% | British Columbia, Ontario border regions | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Growing Prevalence of Cancer & CVD

Canada registered 247,100 new cancer cases and 88,100 cancer deaths in 2024, while 2.4 million adults live with cardiovascular disease, a burden that is reshaping diagnostic pathways.[1]Canadian Cancer Society, “Canadian Cancer Statistics 2024,” Canadian Cancer Society, cancer.ca FDG PET/CT stays central for non-small-cell lung cancer staging, whereas gallium-68 PSMA PET is now displacing conventional imaging for intermediate- and high-risk prostate cancer after Health Canada cleared Pluvicto in 2022.[2] Health Canada, “Notice of Compliance: Pluvicto,” Government of Canada, canada.ca Rubidium-82 cardiac PET attracts cardiology departments because it delivers 75% less radiation than technetium-99m SPECT. Cancer Care Ontario plans six additional PET scanners by 2028, reinforcing capacity in underserved regions.The Canada nuclear imaging market therefore enjoys a 1.8-percentage-point CAGR lift tied directly to disease-burden growth.

Rising Adoption of Hybrid PET/CT & SPECT/CT

The 2022–2023 Canadian Medical Imaging Inventory listed 60 PET/CT and 331 SPECT/CT units compared with 210 standalone SPECT cameras that now average 13.2 years of service.[3]Canadian Agency for Drugs and Technologies in Health, “Canadian Medical Imaging Inventory 2021-2022,” CADTH, cadth.ca Integrated scanners shorten time-to-diagnosis and reduce interpretive uncertainty because anatomical and functional data are co-registered in one session. New digital platforms such as GE HealthCare’s Omni Legend and Siemens Healthineers’ Biograph Vision Quadra increase photon sensitivity two- to three-fold, which translates into 50% lower dose or 40% faster acquisitions. Provincial health authorities in Nova Scotia and British Columbia funded digital SPECT/CT installations in 2024, signaling growing willingness to back premium technology. Rising hybrid adoption contributes an additional 1.5-percentage-point lift to the Canada nuclear imaging market CAGR.

Government Investments in Radiopharmaceutical Capacity

After the National Research Universal reactor closed in 2018, Canada pivoted towards cyclotron-based isotope production. TRIUMF obtained CAD 35 million (USD 26 million) in 2023 to develop a national isotope ecosystem that includes gallium-68 and actinium-225. British Columbia’s CAD 32 million cyclotron and Alberta’s Calgary Radiopharmaceutical Centre, under construction through 2027, decentralize supply and shorten delivery times for short-lived tracers. BWXT Medical’s Target Delivery System at Darlington gained a license in 2023 and now produces molybdenum-99, yttrium-90, and indium-111. These projects raise domestic self-sufficiency and add 1.2 percentage points to the market’s forecast CAGR.

Digital Detector Innovations Lowering Dose

Cadmium zinc telluride detectors in SPECT and silicon photomultiplier arrays in PET convert photons to electrical signals with higher efficiency, doubling photon sensitivity and sharpening energy resolution. The Queen Elizabeth II Health Sciences Centre documented a 40% technetium-99m dose reduction for myocardial perfusion studies after installing a GE StarGuide SPECT/CT in 2024. Nanaimo Regional General Hospital achieved similar results, halving bone-scan acquisition time while expanding daily capacity. Dose optimization aligns with Health Canada radiation-safety guidelines and partially offsets workforce shortages, delivering a 0.9-percentage-point CAGR boost.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Radio-isotope supply risks post-NRU closure | -1.1% | Remote and northern regions nationwide | Medium term (2-4 years) |

| High capex and opex of hybrid scanners | -0.8% | Smaller hospitals and rural facilities | Long term (≥ 4 years) |

| Health Canada regulatory approval timelines | -0.5% | National | Medium term (2-4 years) |

| Shortage of certified nuclear-medicine staff | -0.9% | Particularly acute in Atlantic provinces and North | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Radio-Isotope Supply Risks Post-NRU Closure

With domestic molybdenum-99 production absent until BWXT Medical’s ramp-up hits full stride, many hospitals still depend on South African and European reactors for technetium-99m generators. Transport disruptions can delay deliveries of isotopes whose half-life is just six hours, forcing postponement of non-urgent scans. TRIUMF’s direct cyclotron production, though approved, satisfies only a fraction of national demand. British Columbia and Alberta projects will narrow the gap by 2027, but Atlantic provinces and northern territories will remain vulnerable to weather-related shipping delays. The result is a -1.1 percentage-point drag on the Canada nuclear imaging market CAGR.

High Capex & Opex of Hybrid Scanners

PET/CT units cost USD 1.8 million–3.5 million, SPECT/CT units require USD 1.5 million–2.5 million, and annual service contracts can top USD 0.5 million. Utilization below about 1,200 scans per year risks negative returns, a barrier for smaller hospitals. Forty-one percent of PET/CT systems already exceed ten years of age, signaling deferred replacement cycles. Leasing mitigates upfront cost yet raises lifetime expense by 20%–30%. Consequently, capital constraints subtract 0.8 percentage points from the Canada nuclear imaging market’s trend growth.

Segment Analysis

By Modality: Hybrid Platforms Sustain Leadership While PET/MR Accelerates

Hybrid PET/CT generated 39.35% of modality revenue in 2025, underlining its entrenched role in oncology staging and therapy response. Stand-alone SPECT cameras are declining as hospitals pivot to hybrid SPECT/CT systems that offer both functional and anatomical data without requiring patient relocation. The Canada nuclear imaging market size for hybrid PET/CT modalities is projected to climb at the overall 6.28% CAGR, whereas hybrid PET/MR leads with a 10.24% CAGR due to superior soft-tissue contrast essential for neuro-oncology and inflammatory bowel disease. Equipment makers have responded: GE HealthCare’s 32 cm-axial Omni Legend shortens total-body scan time to 12 minutes, and Siemens Healthineers’ 106 cm-axial Biograph Vision Quadra enables simultaneous multi-organ pharmacokinetics for theranostic dosimetry. Digital cadmium zinc telluride detectors in next-generation SPECT/CT deliver twice the photon sensitivity of legacy photomultiplier tubes, permitting 50% dose cuts that help labs meet dose-optimization mandates. Hospitals in Halifax and Nanaimo adopted such systems in 2024, evidencing readiness to pay premium prices when dose savings and higher throughput combine. As old SPECT fleets age out—the average system is 13.2 years—the Canada nuclear imaging market share held by hybrid scanners will keep widening.

By Component: Equipment Still Dominates Yet Software Gains Momentum

Equipment captured 63.63% of component revenue in 2025 because several provinces budgeted for hybrid-scanner replacements, but software subscriptions are rising at 9.57% annually as AI-driven image-reconstruction and lesion-quantification tools become standard. The Canada nuclear imaging market size tied to software is therefore growing faster than hardware even though suppliers often bundle first-year licenses with scanner deals. AI-assisted quantification from Siemens’ AI-Rad Companion or GE HealthCare’s Edison platform cuts radiologist reading time 30%–40%, a critical benefit when staffing is tight. Vendors now price upgrades on a per-study or annual-license basis, creating resilient recurring revenue. Consumables such as radiopharmaceutical doses and quality-control phantoms ride on procedure volumes, which expand at the overall 6.28% CAGR. BWXT Medical’s domestic yttrium-90 and indium-111 production will further anchor recurring consumable revenue as isotope self-sufficiency improves.

By Radio-Isotope: Fluorine-18 Retains Primacy, Gallium-68 Surges

Fluorine-18 contributed 37.94% of isotope revenue in 2025 because FDG PET/CT occupies the oncology mainstream and the 110-minute half-life supports regional distribution. Technetium-99m remains indispensable for bone, cardiac, and renal scanning, yet supply risks continue until domestic molybdenum-99 output stabilizes. Gallium-68 is the fastest-growing isotope at a 10.33% CAGR and underpins PSMA and DOTATATE imaging. Health Canada’s approval of lutetium-177 PSMA-617 in 2022 cemented the theranostic pairing that drives diagnostic gallium-68 use. Provincial cyclotron projects will allow on-site gallium-68 generator production, improving access beyond Ontario. Rubidium-82 cardiac PET gains favor because it delivers 75% lower radiation than technetium-99m SPECT while avoiding cyclotron dependence. Investigational isotopes such as copper-64 and zirconium-89 are now in Phase II academic trials, setting the stage for diversified isotope portfolios after 2030.

By Application: Oncology Commands, Neurology Accelerates

Oncology absorbed 52.68% of application revenue in 2025 thanks to FDG PET/CT and accelerating PSMA PET utilization. Neurology is forecast to grow at 8.29% CAGR as amyloid and tau PET tracers gain reimbursement, enabling earlier Alzheimer’s differentiation. Cardiology sits second in share; the shift from SPECT to PET proceeds as rubidium-82 generators lower dose and improve accuracy. Endocrinology remains a smaller yet steady niche, rooted in iodine-based thyroid imaging and therapy. Infection and inflammation studies continue contracting as CT and MRI alternatives mature. Large provincial cancer-centers in British Columbia and Ontario have already embedded PSMA theranostics into routine pathways, underscoring oncology’s catalytic role for the Canada nuclear imaging market.

By End User: Hospitals Hold Lead, Academic Institutes Outpace Growth

Hospitals generated 61.53% of end-user revenue in 2025, reflecting single-payer referral patterns. Diagnostic imaging centers offer shorter waits but still face volume ceilings under provincial reimbursement caps. Academic and research institutes grow fastest at 8.12% CAGR because they secure federal grants and industry partnerships for total-body PET, theranostics, and novel radiopharmaceutical trials. The Canada nuclear imaging market share tilted toward hospitals will gradually narrow as academic centers commercialize innovations that downstream hospitals later adopt. Academic hubs also house new cyclotron facilities that distribute isotopes to regional hospitals, reinforcing their pivotal supply-chain role.

Geography Analysis

Ontario, Quebec, and British Columbia account for nearly 70% of Canada nuclear imaging market capacity because they host large population centers and academic medical networks. Ontario leads on absolute procedure volume, with Princess Margaret Cancer Centre and the Ottawa Hospital anchoring theranostic adoption. Quebec’s CHUM and McGill University Health Centre leverage in-house cyclotrons to support high tracer diversity. British Columbia’s USD 23.7 million University of British Columbia cyclotron, operational since 2026, positions the province as the western isotope hub, cutting delivery times for isotopes whose half-life is less than two hours. Alberta’s Calgary Radiopharmaceutical Centre, slated for completion in 2027, will serve Prairie provinces and trim dependency on Ontario. Atlantic provinces lean on Halifax’s Queen Elizabeth II Health Sciences Centre, where a 2024 digital SPECT/CT upgrade improved throughput and reduced technetium-99m dose, yet patients in rural communities still drive hundreds of kilometers for scans. Northern territories remain dependent on medical evacuations to southern centers because population density cannot justify on-site facilities.

Reimbursement policies shape regional growth. Ontario’s six-scanner expansion aimed for 2028 prioritizes northern and eastern communities, whereas British Columbia funnels nuclear-medicine funding through BC Cancer’s centralized network. Alberta maintains a mixed public-private model, allowing independent imaging centers to contract services, but logistics complexity increases for isotope supply. Technologist shortages further widen regional disparities: vacancy rates climb above 10% in Atlantic Canada, leading to longer appointment backlogs despite hardware upgrades. Decentralized cyclotron investment will alleviate some supply pressure by 2031, yet Ontario’s mature academic ecosystem retains first-mover advantage, maintaining the province’s status as the innovation hub of the Canada nuclear imaging market.

Competitive Landscape

The Canadian nuclear imaging market has a moderate concentration profile. Competition revolves around detector efficiency, axial field of view, and bundled AI analytics. GE’s 32 cm Omni Legend emphasizes shorter scan times, Siemens’ 106 cm-long Vision Quadra targets total-body kinetics, Philips favors low-dose workflow integration, and Canon leverages Aquilion-based CT back-ends for PET/CT. On the isotope side, BWXT Medical, Nordion, Jubilant Radiopharma, Lantheus, and Curium carve overlapping niches. BWXT’s Target Delivery System in Darlington produces molybdenum-99, yttrium-90, and indium-111 for generator assembly. Lantheus recorded USD 136.5 million in PYLARIFY revenue in Q3 2024, a 59% year-over-year spike that confirms commercial appetite for PSMA tracers.

Future white-space centers on theranostics and ultra-short-lived isotopes. Bruce Power’s October 2025 expansion of lutetium-177 production positions Canada as a potential net exporter of therapeutic isotopes. Kinectrics’ September 2025 completion of a ytterbium-176 enrichment line provides domestic supply for lutetium-177 precursors, guarding against foreign-source risk. Smaller challengers like Advanced Cyclotron Systems Inc. target regional isotope production to shrink last-mile delivery delays. Regulatory barriers remain significant: Health Canada’s 12- to 18-month approval pathway favors well-resourced incumbents, yet investigator-initiated academic trials on copper-64 and zirconium-89 could pave the way for new entrants by the end of the decade. With provincial health authorities embracing dose-reducing digital detectors, vendors that bundle AI applications and flexible financing are well placed to defend share.

Canada Nuclear Imaging Industry Leaders

GE Healthcare

Koninklijke Philips N.V.

Siemens Healthineers

Jubilant Radiopharma

BWXT Medical

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: BWXT Medical announced first commercial shipments of domestically produced technetium-99m generators from its Darlington facility, marking a milestone in Canadian isotope self-sufficiency.

- October 2025: Bruce Power confirmed a major expansion of lutetium-177 production capacity to support global demand for prostate-cancer theranostics.

- September 2025: Kinectrics, a BWXT division, completed a facility expansion to become North America’s sole source of enriched ytterbium-176 feedstock for lutetium-177 manufacturing.

Canada Nuclear Imaging Market Report Scope

Nuclear imaging is a non-invasive diagnostic method that uses radiotracers to evaluate organ function and structure at the cellular level, focusing on metabolic activity, blood flow, and tissue functionality.

The Canada Nuclear Imaging Market Report is segmented by Modality, Component, Radio‑isotope, Application, and End User. By Modality, the market is segmented into Positron Emission Tomography, Single Photon Emission CT, Hybrid PET/CT, Hybrid SPECT/CT, and Others. By Component, the market is segmented into Equipment, Software, and Accessories & Consumables. By Radio‑isotope, the market is segmented into Fluorine‑18, Technetium‑99m, Iodine‑123/131, Gallium‑68, Rubidium‑82, and Others. By Application, the market is segmented into Oncology, Cardiology, Neurology, Endocrinology, and Others. By End User, the market is segmented into Hospitals, Diagnostic Imaging Centers, Academic & Research Institutes, and Others. Market Forecasts are Provided in Terms of Value (USD).

By Modality

| Positron Emission Tomography (PET) |

| Single Photon Emission CT (SPECT) |

| Hybrid PET/CT |

| Hybrid SPECT/CT |

| Others (e.g., PET/MR) |

By Component

| Equipment |

| Software |

| Accessories & Consumables |

By Radio-isotope

| Fluorine-18 |

| Technetium-99m |

| Iodine-123/131 |

| Gallium-68 |

| Rubidium-82 |

| Others |

By Application

| Oncology |

| Cardiology |

| Neurology |

| Endocrinology |

| Others |

By End User

| Hospitals |

| Diagnostic Imaging Centers |

| Academic & Research Institutes |

| Others |

| By Modality | Positron Emission Tomography (PET) |

| Single Photon Emission CT (SPECT) | |

| Hybrid PET/CT | |

| Hybrid SPECT/CT | |

| Others (e.g., PET/MR) | |

| By Component | Equipment |

| Software | |

| Accessories & Consumables | |

| By Radio-isotope | Fluorine-18 |

| Technetium-99m | |

| Iodine-123/131 | |

| Gallium-68 | |

| Rubidium-82 | |

| Others | |

| By Application | Oncology |

| Cardiology | |

| Neurology | |

| Endocrinology | |

| Others | |

| By End User | Hospitals |

| Diagnostic Imaging Centers | |

| Academic & Research Institutes | |

| Others |

Key Questions Answered in the Report

How large is the Canada nuclear imaging market in 2026 and where is it headed?

The market stood at USD 363.38 million in 2026 and is forecast to reach USD 492.83 million by 2031 at a 6.28% CAGR.

Which modality is growing fastest in Canadian nuclear imaging?

Hybrid PET/MR adds the most momentum, advancing at a 10.24% CAGR thanks to superior neuro-oncology and inflammatory-disease applications.

What is driving the strong uptake of gallium-68 tracers?

Health Canada approvals for PSMA theranostics, provincial cyclotron investments, and reimbursement for DOTATATE imaging are propelling gallium-68 demand.

Why are software platforms outpacing hardware revenue growth?

AI-driven reconstruction and workflow tools sold on subscription cut reading time and boost scanner throughput, creating recurring revenue that grows at 9.57% annually.

How are isotope supply risks being mitigated post-NRU reactor closure?

New cyclotron facilities in British Columbia and Alberta, TRIUMF’s isotope-ecosystem funding, and BWXT’s Darlington molybdenum-99 production collectively reduce reliance on overseas reactors.

Which provinces are investing most heavily in nuclear-medicine capacity?

Ontario, British Columbia, and Alberta lead with scanner additions and cyclotron builds, while Quebec maintains strong in-house cyclotron infrastructure.

Page last updated on: