Canada Management Consulting Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

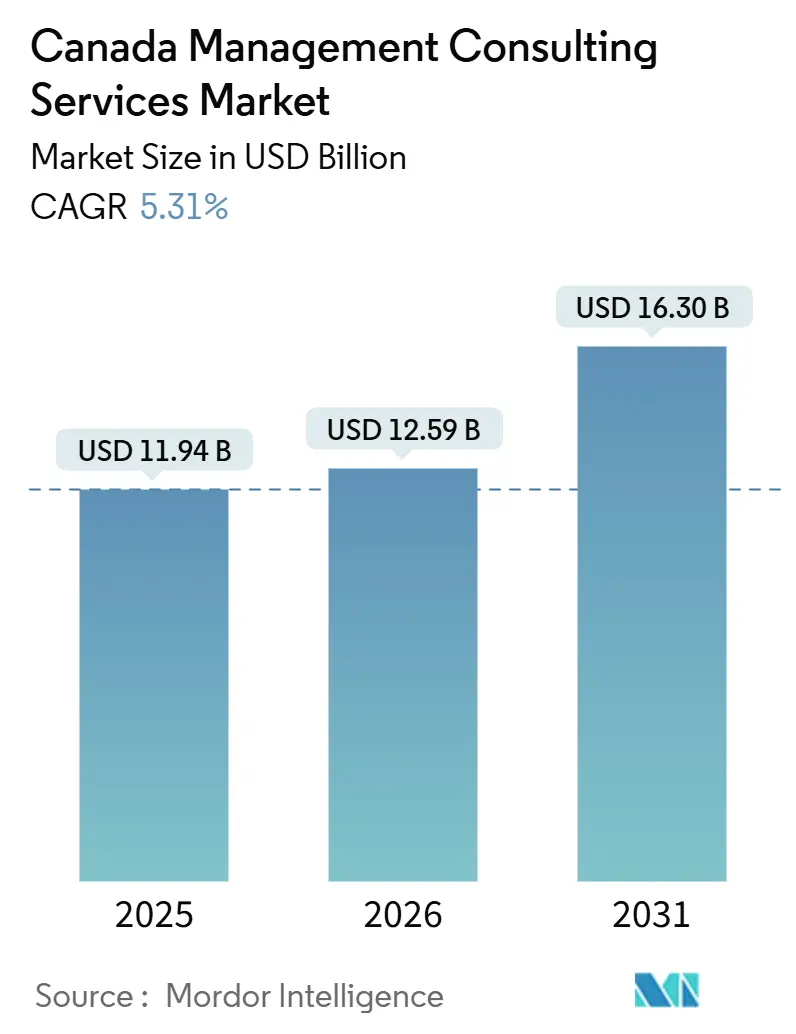

| Base Year Market Size (2025) | USD 11.94 Billion |

| Market Size (2026) | USD 12.59 Billion |

| Market Size (2030) | USD 16.30 Billion |

| Growth Rate (2026 - 2031) | 5.31% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Canada Management Consulting Services Market Analysis by ���ϲ�����

The Canada management consulting services market size is projected to be USD 11.94 billion in 2025, USD 12.59 billion in 2026, and reach USD 16.30 billion by 2031, growing at a CAGR of 5.31% from 2026 to 2031. Digital-first mandates, clean-tech incentives worth more than CAD 100 billion (USD 71.5 billion), and ESG-linked lending covenants continue to reshape advisory demand patterns. Large enterprises still account for most spending, yet small and medium-sized enterprises are accelerating adoption on the back of remote delivery, outcome-based pricing, and federal technology-grant programs. Technology consulting outpaces all other service lines as cloud migration, generative-AI pilots, and cybersecurity threats intensify. Provincial procurement reforms, meanwhile, pressure margins on government contracts, pushing firms toward higher-value niches such as climate transition, Indigenous reconciliation, and AI governance.

Key Report Takeaways

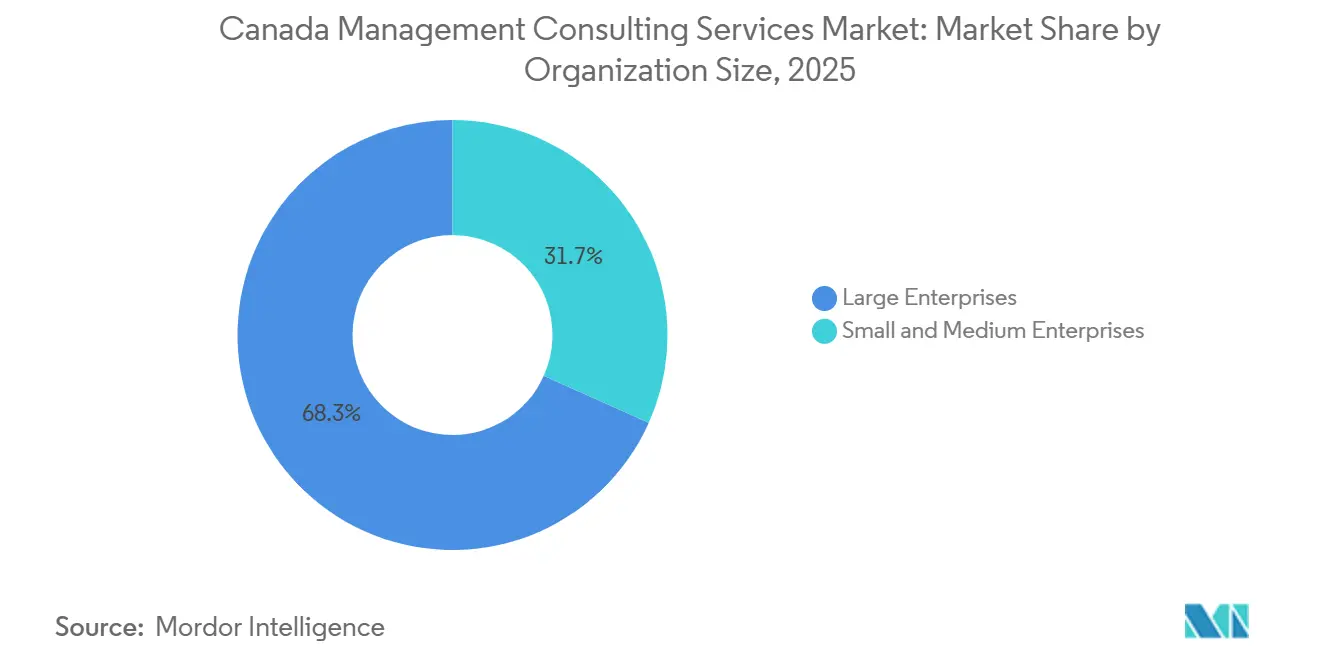

- By organization size, large enterprises held 68.30% revenue share in 2025, while the SME segment is expanding at a 5.88% CAGR to 2031 on the strength of modular, subscription-based engagements.

- By service type, strategy consulting commanded 29.45% share in 2025, but technology consulting is forecast to advance at a 9.10% CAGR as clients prioritize cloud, AI, and cybersecurity.

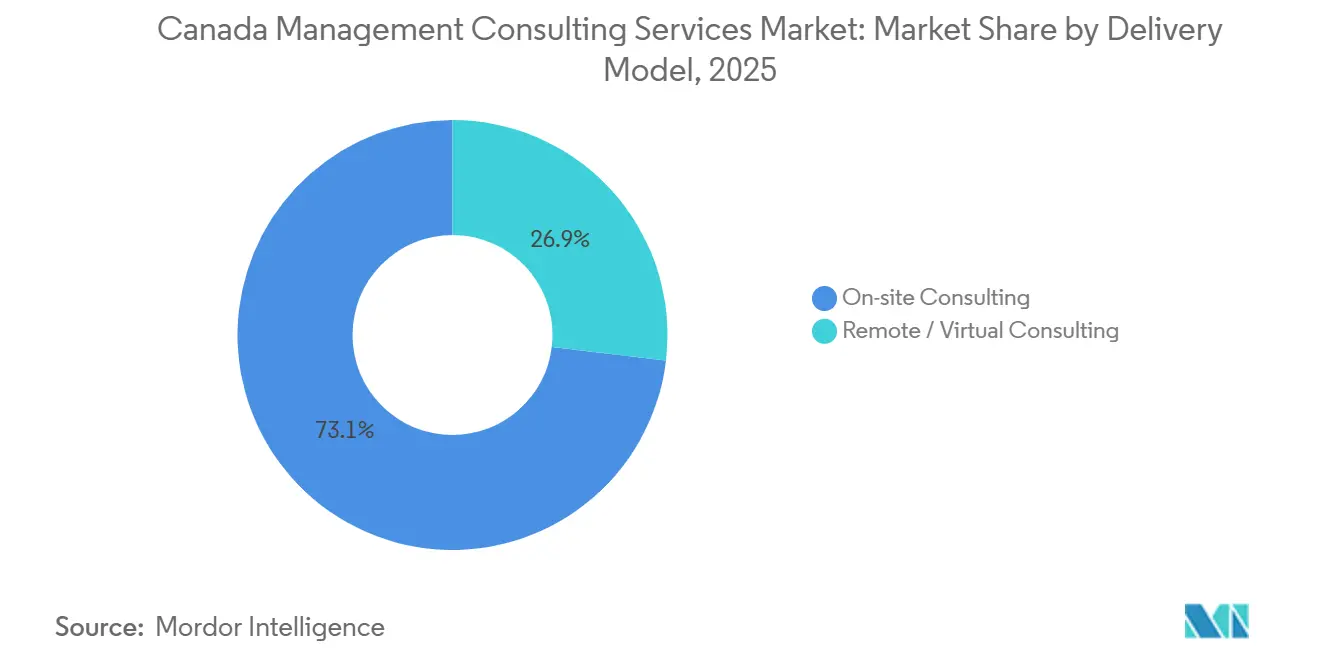

- By delivery model, on-site work retained 73.10% share in 2025; remote and virtual formats, however, are posting a 5.40% CAGR through 2031 in line with hybrid workforce norms.

- By end-user industry, financial services led with 43.40% of 2025 demand, while healthcare and life sciences is the fastest-growing vertical at a 7.32% CAGR on the back of digital-health mandates.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Canada Management Consulting Services Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital-First Transformation Programmes Post-COVID-19 | +1.8% | National, concentrated in Ontario and British Columbia | Medium term (2-4 years) |

| Government-Backed Clean-Tech Investment Incentives | +1.2% | National, led by Alberta, Quebec, and Atlantic provinces | Long term (≥ 4 years) |

| Rising Mid-Market M&A Activity Among Canadian Firms | +0.9% | National, strongest in Toronto, Montreal, and Calgary | Short term (≤ 2 years) |

| ESG-Linked Lending Mandates from Major Banks | +0.7% | National, early adoption in financial hubs | Medium term (2-4 years) |

| Shift to Outcome-Based Billing Models | +0.4% | Federal and provincial public sectors | Medium term (2-4 years) |

| Hyper-Specialized Indigenous-Owned Consulting Demand | +0.3% | National, early gains in resource-rich provinces | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Digital-First Transformation Programmes Post-COVID-19

Government’s Digital Ambition 2026 requires that 95% of federal services move online by December 2026, pushing 43 departments to modernize legacy systems. Royal Bank of Canada lifted annual technology spend to CAD 5.1 billion (USD 3.64 billion) in 2025, channeling funds toward AI-driven analytics.[1]Royal Bank of Canada, “2025 Annual Report,” rbc.com Resource players follow suit; Suncor earmarked CAD 1.2 billion (USD 857 million) to digitize oil-sands operations.[2]Suncor Energy, “Digital Transformation Program,” suncor.com Consulting firms now embed data engineers and cloud architects inside classic strategy squads, commanding premium blended rates. Regulatory drivers include Treasury Board service-design rules aligned with WCAG 2.1 accessibility standards, which make transformation advisory non-discretionary.

Government-Backed Clean-Tech Investment Incentives

Ottawa’s refundable Clean Technology Investment Tax Credit, offering up to 30% of eligible capital outlays, triggered more than 200 project filings by mid-2025. Alberta’s TIER program devoted CAD 750 million (USD 536 million) to carbon-capture and hydrogen schemes.[3]Government of Alberta, “TIER Framework,” alberta.ca Quebec’s Plan for a Green Economy mobilized CAD 6.7 billion (USD 4.79 billion) for electrification. Projects confront multijurisdictional approvals that can stretch 18-36 months, so sponsors seek consultants proficient in Impact Assessment Act compliance. Engagement scopes span feasibility models, Indigenous engagement, and supply-chain localization, sustaining double-digit advisory pipelines in energy and infrastructure.

Rising Mid-Market M&A Activity Among Canadian Firms

Deal counts in the CAD 50 million–CAD 500 million band climbed 18% year-over-year in 2025 as dry-powder topped CAD 80 billion (USD 57.2 billion). Tech deals formed 31% of volume, with cybersecurity and SaaS targets leading. Healthcare M&A expanded 24% amid consolidation of labs and home-care providers. Advisory teams now deploy rapid-response pods that close diligence, synergy sizing, and integration blueprints within 8-12 weeks. Toronto, Montreal, and Calgary offices house most transaction-services talent, allowing firms to monetize cross-border capital flows and private-equity demand for sector roll-ups.

ESG-Linked Lending Mandates from Major Banks

The Big Six banks pledge to mobilize more than CAD 2 trillion (USD 1.43 trillion) in sustainable finance by 2030. TD disclosed that 42% of its corporate loan book now carries sustainability-linked covenants. Scotiabank’s Climate Commitment compels high-emitting borrowers to table transition plans by 2027. Consultants partner with legal and engineering firms to craft materiality matrices, Scope 3 baselines, and lender-ready disclosures. OSFI Guideline B-15 cements the push by requiring climate risk integration within governance and capital frameworks.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying Talent Wars and Wage Inflation | -0.9% | National, acute in Toronto, Vancouver, and Montreal | Short term (≤ 2 years) |

| Procurement-Led Fee Compression in Public Sector | -0.6% | Federal and provincial government contracts | Medium term (2-4 years) |

| AI Self-Service Strategy Tools Reducing Entry-Level Work | -0.4% | National, concentrated in technology and financial services | Medium term (2-4 years) |

| Immigration Policy Uncertainty for Skilled Consultants | -0.3% | National, affecting major urban centers | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Intensifying Talent Wars and Wage Inflation

Median senior-consultant pay climbed 12% in 2025 to CAD 145,000–CAD 175,000 (USD 103,600–USD 125,000), while mid-tier attrition hovered near 22%. Skills shortages in cloud architecture, data science, and Indigenous relations spur bidding wars with tech firms and public agencies. Deloitte reported a 1.8-point rise in employee-cost ratio, sparking expansion of offshore delivery hubs. PwC spent CAD 45 million (USD 32.1 million) on AI upskilling, yet productivity lag slows monetization. Compliance costs also rise as new pay-transparency statutes and equity targets widen total reward packages.

Procurement-Led Fee Compression in Public Sector

Public Services and Procurement Canada’s rate caps have shaved 8-12% from average margins since 2023. Mandatory competitive tenders for anything above CAD 100,000 (USD 71,500) limit sole-source awards, while performance-based milestones tie payouts to user-adoption and cost-savings metrics. Ontario and British Columbia rolled out similar shared-services buying groups, amplifying price discipline. Firms pivot to premium niches, climate transition, digital identity, Indigenous reconciliation, yet these shorter, higher-value engagements increase revenue volatility and pipeline unpredictability.

Segment Analysis

By Organization Size: SMEs Accelerate Through Modular Advisory

SMEs narrowed the adoption gap in 2025, yet large enterprises still accounted for 68.30% of Canada management consulting services market revenue. The SME slice of the Canada management consulting services market size is projected to grow at a 5.88% CAGR to 2031, reflecting remote work norms, outcome-linked pricing, and grants such as the Canada Digital Adoption Program. SMEs typically commission engagements worth CAD 50,000–CAD 250,000 (USD 35,750–USD 178,750) for e-commerce upgrades, supply-chain digitization, or ESG reporting. Large multinationals continue to dominate enterprise-wide ERP rollouts, regulatory readiness, and post-merger integration programs that require multi-year commitments and proprietary toolkits.

Growth dynamics differ by region: Ontario hosts the majority of SME tech startups seeking fractional CFO and market-entry advice, while resource-rich provinces favor Indigenous economic-development roadmaps. Consulting firms tailor delivery models accordingly, offering subscription portals and asynchronous workshops to keep project costs predictable. As remote collaboration becomes the norm, boutique advisors located outside major metros now access national client pools without expanding physical footprints.

By Service Type: Technology Consulting Outpaces All Lines

Strategy consulting retained a 29.45% share of the Canada management consulting services market in 2025, yet technology workstreams are advancing at a 9.10% CAGR through 2031. Cyber attacks rose 32% in 2025, driving urgent reviews of security architecture and incident-response playbooks. Clients also scale generative-AI pilots into production, widening scope for data-governance, MLOps, and change-management engagements. Operations and HR consulting track close to overall growth, focusing on supply-chain resilience and hybrid-workforce design.

Other advisory lines, risk, compliance, and sustainability, benefit from new climate-disclosure rules. Firms frequently bundle these capabilities into end-to-end transformation programs, blurring service boundaries. The Canada management consulting services market size for technology engagements is forecast to reach USD 7 billion by 2031, underpinned by hyperscaler partnerships and pre-configured cloud accelerators. Despite faster growth, strategy work remains lucrative because board-level mandates demand senior-partner time and bespoke analysis, sustaining premium day rates.

By Delivery Model: Hybrid Norms Sustain On-Site Dominance

On-site delivery still captured 73.10% of 2025 spend, but remote models continue to expand at a 5.40% CAGR. Financial services and technology clients allocate roughly 65% of total project hours to virtual collaboration, reserving face-to-face meetings for steering committee approvals and go-live events. The Canada management consulting services market share for remote engagements rose from 24% in 2020 to 27% in 2025 and is on track to hit 30% by 2031.

Smaller firms leverage remote work to win national mandates without incurring real estate overhead. Treasury Board encourages federal departments to favor virtual workshops to cut travel emissions, provided secure data-room protocols are in place. Clients cite cost savings of 12–18% when using hybrid staffing, while consultancies widen access to specialized talent irrespective of geography.

By End-User Industry: Financial Services Leads, Healthcare Gains Momentum

Financial institutions generated 43.40% of 2025 revenue, fueled by open-banking readiness, AML modernization, and climate-risk stress tests. Healthcare and life sciences posted the fastest 7.32% CAGR on the back of provincial EHR rollouts, virtual-care expansion, and pharmaceutical-supply security. The Canada management consulting services market size for healthcare assignments is poised to surpass USD 2 billion by 2031, with projects ranging from cloud-hosted patient portals to AI-aided drug discovery.

Energy, government, retail, and media together form a diversified tail, each with sector-specific catalysts. Energy players seek carbon-capture feasibility studies; government entities pursue digital ID and carbon budgeting; retailers overhaul omnichannel logistics; media firms optimize streaming monetization models. Consultants add value by cross-pollinating insights across industries, especially around data privacy, user experience, and regulatory change.

Geography Analysis

Ontario anchored 45% of 2025 spending, supported by Toronto’s dense banking, insurance, and tech ecosystems. The province’s share is forecast to hold steady as open-banking regulations and fintech scale-ups sustain a continuous advisory backlog. Quebec contributed 23% of demand, propelled by Montreal’s aerospace, biopharma, and AI research clusters and the province’s aggressive clean-tech subsidies. British Columbia captured 15%, riding Vancouver’s thriving software scene, Asia-Pacific trade corridors, and renewable-energy projects.

The Prairies, Alberta, Saskatchewan, and Manitoba, account for roughly 12% of revenue. Engagements here focus on carbon-capture, hydrogen hubs, and Indigenous economic partnerships, reflecting economic diversification away from legacy hydrocarbons. Atlantic Canada held about 5% in 2025; offshore wind plans totaling 5 GW by 2030 and aquaculture modernizations underpin a 5.4% provincial CAGR.

Regulatory heterogeneity shapes regional project scopes. Ontario’s Environmental Assessment Act, Quebec’s wetlands legislation, and British Columbia’s impact rules impose distinct filings, timelines, and Indigenous consultation protocols. Federal overlays, the Impact Assessment Act, Fisheries Act, and Species at Risk Act, add complexity to interprovincial infrastructure, encouraging clients to hire consultancies able to synchronize multi-level permitting and stakeholder engagement.

Competitive Landscape

The market is moderately concentrated. The Big Four, Deloitte, PwC, EY, and KPMG collectively earned 35% of 2025 revenue through multidisciplinary practices and embedded audit relationships. MBB firms held 12%, retaining the boardroom for portfolio strategy, private-equity due diligence, and transformation blueprints. Technology-centric players, Accenture, IBM Consulting, and Capgemini captured 15%, differentiating on cloud accelerators, AI factories, and offshore scale.

Canadian-headquartered providers, MNP, CGI, WSP, Stantec, secured 18% share by combining regional offices, bilingual delivery, and deep regulatory familiarity. The remaining 20% is fragmented among boutiques, HR specialists, and Indigenous-owned practices that serve niche verticals such as Indigenous reconciliation and climate transition.

Strategic themes include ecosystem partnerships with hyperscalers, venture studios, and academic labs to co-develop IP and shorten project timelines. Generative AI tooling cuts proposal drafting and data synthesis hours by 15-20%, enabling senior consultants to handle more concurrent engagements. White-space opportunities emerge in Scope 3 carbon accounting, AI governance, and Indigenous economic development where regulatory ambiguity favors agile, specialist entrants.

Canada Management Consulting Services Industry Leaders

Deloitte Touche Tohmatsu Limited

McKinsey and Company Inc.

Accenture Plc

PricewaterhouseCoopers (PwC)

Ernst and Young (EY)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Deloitte Canada committed CAD 200 million (USD 143 million) over three years to build an AI and quantum-computing consulting practice anchored by a Quantum Innovation Lab in Waterloo.

- December 2025: PwC Canada acquired a Toronto-based Indigenous consultancy, adding 35 professionals skilled in stakeholder engagement and regulatory navigation.

- November 2025: Accenture inaugurated a 1,200-person Advanced Technology Center in Montreal, investing CAD 150 million (USD 107 million) to deepen generative-AI and cybersecurity services.

- October 2025: McKinsey launched a Climate Transition Hub in Calgary, deploying 50 senior consultants to advise on carbon-capture, hydrogen, and workforce transition.

Canada Management Consulting Services Market Report Scope

The Canada Management Consulting Services Market Report is Segmented by Organization Size (Large Enterprises, and SMEs), Service Type (Strategy, Operations, HR, Technology, and More), Delivery Model (On-site, and Remote/Virtual), and End-user Industry (IT, Healthcare, Financial Services, Manufacturing, Energy, Government, Real Estate, Retail, Media, Hospitality, and More). Market Forecasts are in Value (USD).

| Large Enterprises |

| Small and Medium-sized Enterprises |

| Strategy Consulting |

| Operations Consulting |

| HR Consulting |

| Technology Consulting |

| Other Service Types |

| On-site Consulting |

| Remote / Virtual Consulting |

| IT and Telecommunications |

| Healthcare and Life Sciences |

| Financial Services (BFSI) |

| Manufacturing and Industrial |

| Energy and Utilities |

| Government and Public Sector |

| Real Estate and Construction |

| Retail and Consumer Goods |

| Media, Entertainment and Sports |

| Hospitality and Travel |

| Other Industries |

| By Organization Size | Large Enterprises |

| Small and Medium-sized Enterprises | |

| By Service Type | Strategy Consulting |

| Operations Consulting | |

| HR Consulting | |

| Technology Consulting | |

| Other Service Types | |

| By Delivery Model | On-site Consulting |

| Remote / Virtual Consulting | |

| By End-user Industry | IT and Telecommunications |

| Healthcare and Life Sciences | |

| Financial Services (BFSI) | |

| Manufacturing and Industrial | |

| Energy and Utilities | |

| Government and Public Sector | |

| Real Estate and Construction | |

| Retail and Consumer Goods | |

| Media, Entertainment and Sports | |

| Hospitality and Travel | |

| Other Industries |

Key Questions Answered in the Report

What is the projected value of the Canada management consulting services market in 2031?

The market is forecast to reach USD 16.30 billion by 2031.

Which service line is growing fastest?

Technology consulting shows the highest momentum, advancing at a 9.10% CAGR through 2031 due to cloud, AI, and cybersecurity demand.

How quickly are SMEs increasing their consulting spend?

The SME segment is expected to grow at a 5.88% CAGR between 2026 and 2031 as modular, remote engagements lower entry barriers.

Which province generates the largest share of consulting demand?

Ontario leads with 45% of total 2025 spending, anchored by Toronto’s financial-services and tech ecosystems.