Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

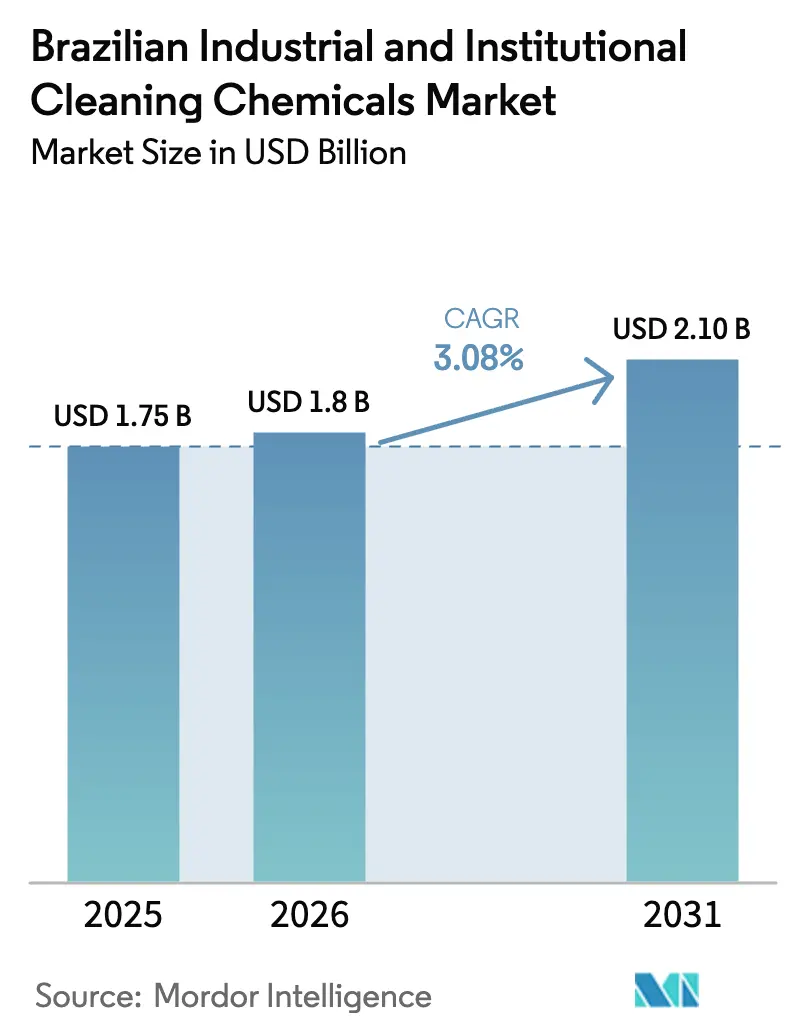

| Base Year Market Size (2025) | USD 1.75 Billion |

| Market Size (2026) | USD 1.8 Billion |

| Market Size (2031) | USD 2.10 Billion |

| Growth Rate (2026 - 2031) | 3.08% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Brazilian Industrial And Institutional Cleaning Chemicals Market Analysis by ���ϲ�����

The Brazilian Industrial and Institutional Cleaning Chemicals Market size is expected to increase from USD 1.75 billion in 2025 to USD 1.80 billion in 2026 and reach USD 2.10 billion by 2031, growing at a CAGR of 3.08% over 2026-2031. Steady economic reopening, the build-out of healthcare and food-service infrastructure, and rising scrutiny of quaternary ammonium compounds (QACs) sustain mid-single-digit demand momentum even as petrochemical feedstock prices remain volatile. Surfactants draw particular interest because the country’s ethanol and cashew value chains generate large glycerin and phenolic byproduct pools that underpin cost-competitive bio-based formulations. Infection-control protocols established during the pandemic continue to underpin elevated usage of disinfectants, while labor shortages in hospitality and retail accelerate adoption of concentrated, auto-dosed products that cut manual handling and reduce inventory losses. Multinational suppliers leverage enzyme and probiotic technologies to meet tightening environmental rules and to secure premium contracts, whereas many regional producers compete on price in Brazil’s fragmented commercial channel.

Key Report Takeaways

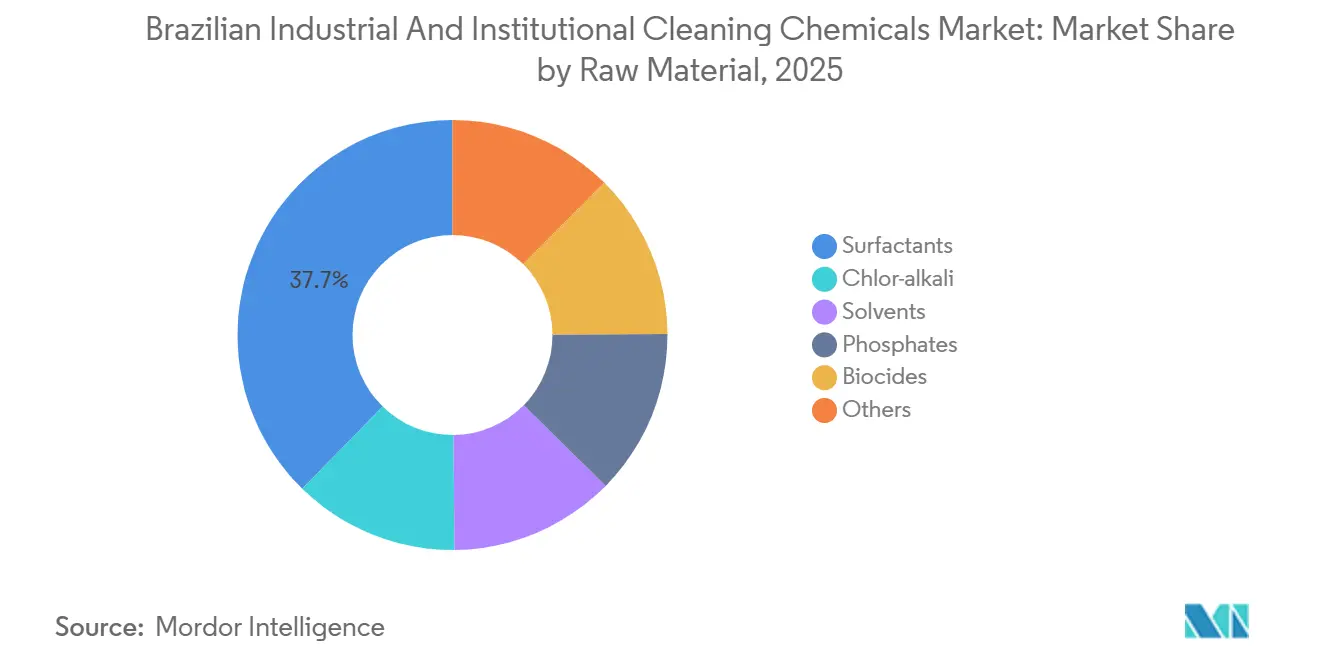

- By raw material, surfactants captured 37.69% of the Brazilian industrial and institutional cleaning chemicals market share in 2025 and are forecast to post the fastest 3.89% CAGR through 2031.

- By product type, general-purpose cleaners led with 42.31% revenue contribution in 2025, while disinfectants and sanitizers are forecast to post the fastest 4.96% CAGR through 2031.

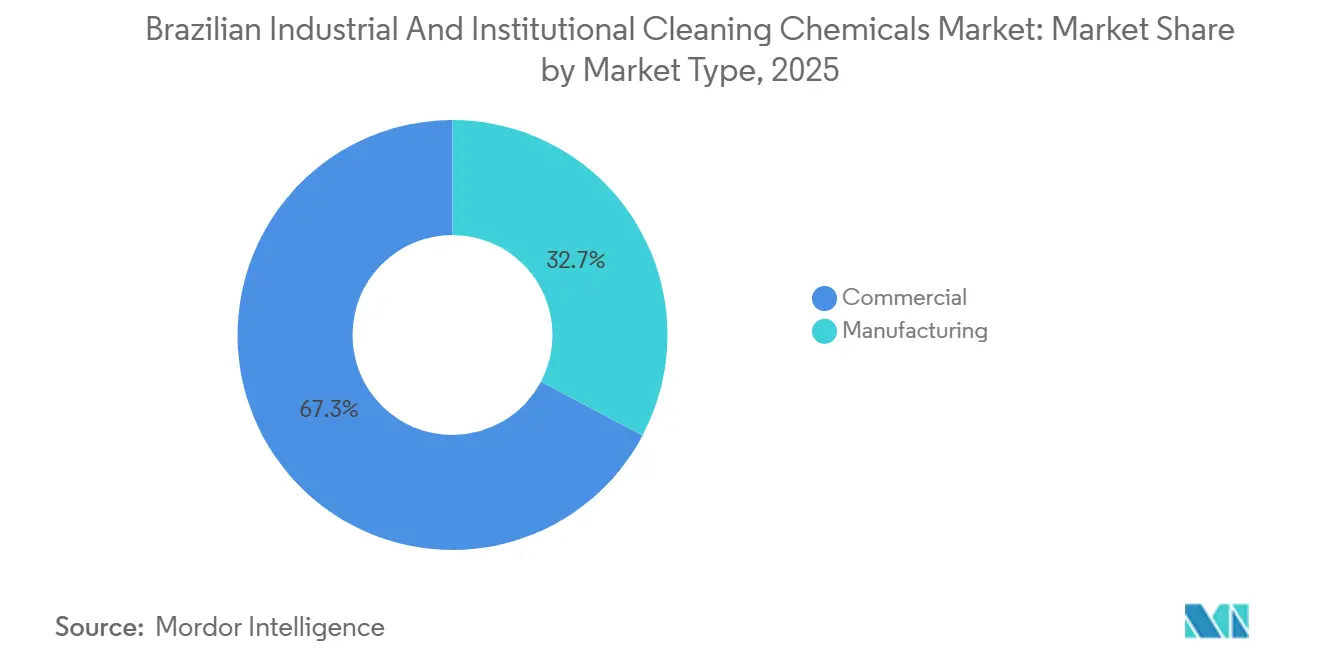

- By market type, the commercial segment held 67.26% of the Brazilian industrial and institutional cleaning chemicals market size in 2025 and is expected to grow at a 3.29% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Brazilian Industrial And Institutional Cleaning Chemicals Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-COVID infection-control mandates across healthcare and food-service | +0.8% | National, concentrated in Southeast (São Paulo, Rio de Janeiro) and South regions | Medium term (2-4 years) |

| Expansion of hospital and diagnostic infrastructure | +0.6% | National, with early gains in São Paulo, Minas Gerais, Rio Grande do Sul | Long term (≥ 4 years) |

| Export-oriented food and beverage processing sanitation needs | +0.7% | National, strongest in Center-West (meat processing), Southeast (orange juice), South (poultry) | Medium term (2-4 years) |

| Bio-based surfactant boom leveraging Brazilian agro-feedstocks | +0.5% | National, feedstock concentration in Center-West (soy), Northeast (cashew), Southeast (sugarcane) | Long term (≥ 4 years) |

| IoT-driven smart dosing and inventory systems | +0.4% | Urban centers and multinational-operated facilities in São Paulo, Rio de Janeiro, Paraná | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Post-COVID Infection-Control Mandates Across Healthcare and Food-Service

Surface pathogens, like Acinetobacter, can linger for up to five months, underscoring the heightened hygiene vigilance in hospitals and restaurants[1]Pan American Health Organization, “Regional IPC Guidance,” paho.org. Brazilian facilities, while adhering to the price-sensitive purchasing rules of the Sistema Único de Saúde, are striving to meet global benchmarks. This has led to a surge in demand for broad-spectrum disinfectants, especially those compatible with stainless steel and electronics. Research revealed that diners prioritize perceived cleanliness when selecting restaurants. As a result, restaurant operators are ramping up the use of alcohol-based wipes and QAC sprays. ANVISA’s RDC 989/2025 sets biodegradability standards for anionic surfactants, compelling a reformulation of traditional QAC products[2]Agência Nacional de Vigilância Sanitária, “RDC 989/2025,” anvisa.gov.br. This regulation is hastening the industry's pivot towards enzymatic or probiotic alternatives, which promise both effectiveness and a reduced environmental footprint. As a result, Brazil's market for industrial and institutional cleaning chemicals sees a sustained demand for surface disinfectants and hand hygiene solutions.

Expansion of Hospital and Diagnostic Infrastructure

Brazil has numerous hospitals and primary-care units, with ongoing investments targeting reduced wait times and enhanced diagnostic capabilities. Public procurement leans towards concentrated liquids to cut freight costs. In contrast, major private chains are integrating Internet-of-Things (IoT) dosing systems, which not only auto-adjust chemical levels but also log compliance data. Ecolab’s 3D TRASAR platform, now a fixture in several private hospitals across São Paulo, showcases performance boosts and record-keeping benefits, earning nods from Joint Commission auditors. With the expansion of private facilities, there's a notable uptick in premium service contracts, further enriching Brazil's industrial and institutional cleaning chemicals market.

Export-Oriented Food and Beverage Processing Sanitation Needs

Brazil's food-processing sector is on track for annual growth through 2028. To comply with U.S. FDA HACCP rules and European Union microbial standards, export plants are increasingly turning to alkaline degreasers, acidic descalers, and biocide rotations, which are essential in preventing resistant strains. Facilities in poultry, soy, and juice sectors are utilizing Clean-in-Place systems that demand low-foaming, quick-rinse chemistries to reduce downtime. Moreover, technical services like water-hardness testing, dosing calibration, and residue analysis have emerged as key differentiators, allowing multinationals to secure multi-year supply contracts and expand their presence in Brazil's industrial and institutional cleaning chemicals market.

Bio-Based Surfactant Boom Leveraging Brazilian Agro-Feedstocks

In 2024, the production of ethanol led to significant streams of glycerin, primed for conversion into fatty-acid-based surfactants. In the Northeast, cashew-nut-shell liquid is being harnessed to produce phenolic surfactants known for their strong emulsification properties. Meanwhile, enzyme startups in the region are setting ambitious targets, aiming for a reduction in the cost of imported enzymes by 2026. Lifecycle assessments reveal that these bio-surfactants boast carbon footprints up to 46 percent lower than traditional linear alkylbenzene sulfonate. This not only aligns with ANVISA regulations but also resonates with corporate sustainability objectives. Given these supportive feedstock dynamics and regulatory winds, bio-surfactants are poised to capture additional demand in Brazil's industrial and institutional cleaning chemicals market during the forecast period.

Restraints Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Occupational health hazards from QACs and chlorinated solvents | -0.4% | National, enforcement concentrated in Southeast industrial corridors | Medium term (2-4 years) |

| Volatile energy and feedstock costs | -0.6% | National, acute in petrochemical-dependent formulations | Short term (≤ 2 years) |

| Proliferation of informal/counterfeit cleaning products | -0.3% | National, most prevalent in micro-enterprise and informal retail channels | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Occupational Health Hazards from QACs and Chlorinated Solvents

California's DTSC has raised alarms about QACs, linking them to risks like dermal irritation, asthma, and reproductive toxicity. These concerns echo in Brazilian workplaces. While ANVISA has already prohibited specific QACs in cosmetics, it is now turning its attention to cleaning products, implementing a risk-based registration approach. Safety data sheets for heavy-duty cleaners containing chlorine emphasize the need for goggles and proper ventilation. However, many micro-enterprises struggle to meet these compliance standards. To shield their employees from potential hazards, hospitals and food exporters are increasingly opting for hydrogen peroxide or enzyme-based systems. This shift narrows the market for high-hazard actives in Brazil's industrial and institutional cleaning chemicals sector.

Volatile Energy and Feedstock Costs

In 2025, Braskem's decision to hibernate its Alagoas chlor-alkali plant tightened the domestic supply of caustic soda, coinciding with a drop in chlorine prices. This move underscored the unpredictable dynamics of petrochemical inputs. This volatility has been challenging for formulators bound by fixed customer contracts. Although the adoption of enzymes and biosurfactants offers some mitigation against these price swings, many producers remain vulnerable to petrochemical fluctuations. This exposure has been squeezing profitability in Brazil's industrial and institutional cleaning chemicals market, particularly as buyers push back against price hikes.

Segment Analysis

By Raw Material: Agro-Feedstock Integration Lifts Surfactant Economics

Surfactants held 37.69% of the Brazilian industrial and institutional cleaning chemicals market share in 2025 and are forecast to post a 3.89% CAGR through 2031. This ascent is anchored in the burgeoning supply of ethanol-derived glycerin and cashew phenolics. These not only reduce cost bases but also meet the biodegradability standards set by ANVISA. Should the current trends continue, the market size for surfactants in Brazil's industrial and institutional cleaning sector could approach substantial levels by 2031. While chlor-alkali intermediates remain pivotal for bleach and hypochlorite production, recent cutbacks in domestic capacity have heightened procurement risks. This has led to a partial shift towards sodium carbonate and enzyme systems. Additionally, while solvents, phosphates, and biocides round out the raw-material spectrum, they face mounting environmental scrutiny. In response, international suppliers are rolling out concentrated, safer-chemistry variants tailored to Brazil's unique water hardness.

Regulatory changes are driving a wave of innovation in raw materials. The biodegradability stipulation in RDC 989/2025 mandates expensive environmental fate studies. This has nudged smaller formulators to lean on turnkey enzyme solutions from global biocatalyst companies. Apexzymes projects that by 2026, local enzyme production will be priced at a fraction of current import rates. Such a shift could redirect a portion of the annual surfactant demand towards bio-hybrid formulations. Looking ahead, the integration of feedstocks, coupled with regional logistical benefits, is poised to bolster the competitive edge of Brazil's domestic surfactant producers in the industrial and institutional cleaning chemicals arena.

By Product Type: Disinfectants Narrow the Gap With General-Purpose Cleaners

General-purpose cleaners accounted for 42.31% of 2025 revenue, reflecting broad usage across offices, retail, and hospitality. Yet disinfectants and sanitizers are projected to rise at a 4.96% CAGR, outpacing every other product class. The market size for disinfectants in Brazil's industrial and institutional cleaning sector is set to grow, bolstered by persistent infection-control practices. Meanwhile, laundry-care products are undergoing a transformation, with solutions like protease, lipase, and phosphodiesterase facilitating cold-water washes and minimizing surfactant use, making them attractive to energy-conscious establishments like hotels and hospitals. Additionally, warewashing chemicals are reaping the benefits of Brazil's food-service sector, which is expanding annually, leading to a surge in the adoption of automated dish machines that require scale inhibitors and rinse aids.

Innovation in the sector is heavily focused on enhancing efficacy and promoting sustainability. For instance, enzyme-rich formulations that reduce surfactant usage resonate with corporate carbon reduction commitments. At the same time, probiotic sprays, known for their seven-day residual action, are carving out a niche in the healthcare sector. While vehicle-wash and specialty-metal cleaners are relatively smaller segments, they are consistently sought after by automotive and electronics manufacturers, particularly in regions like São Paulo and the southern parts of Brazil. As the Brazilian market for industrial and institutional cleaning chemicals pivots towards higher-value, compliance-centric subsegments, it's clear that technological differentiation will play a pivotal role in determining market leaders.

By Market Type: Commercial Sphere Dominates but Manufacturing Adds High Complexity

Commercial establishments generated 67.26% of the 2025 turnover in the Brazilian industrial and institutional cleaning chemicals market and should advance at a 3.29% CAGR until 2031. Food-service operators, predominantly independent, lean towards single-use sachets and mid-tier disinfectants. These choices ensure visible cleanliness while adhering to tight budgets. Hospitals and diagnostic labs, on the other hand, procure broad-spectrum disinfectants, floor finishes, and instrument sterilants. They emphasize traceability and eco-labels, often entering multisite contracts. Retailers focus on concentrated floor and glass cleaners to optimize shelf stock and cut logistics costs.

Manufacturing plants spanning food, beverage, automotive, and electronics sectors may consume lower volumes but demand specialized chemistries. These are rigorously validated through lab analysis, residue testing, and ISO audits. Food exporters face the challenge of aligning with EU microbial limits and U.S. FDA residue ceilings, elevating their compliance standards. Automotive assemblers depend on degreasers and phosphating baths to ensure paint adhesion. Moreover, precision cleaning for circuit boards demands residue-free solvents and closed-loop rinsing systems. As a result, while commercial accounts dominate in volume, industrial buyers contribute to higher margins and technical-service revenue, influencing strategic segmentation in Brazil's industrial and institutional cleaning chemicals market.

Geography Analysis

In 2025, São Paulo and the wider Southeast region dominated Brazil's retail cleaning-chemical revenues, thanks to the area's dense clusters of restaurants, hospitals, and factories. This region is home to BASF’s surfactant complex in Guaratinguetá and Ecolab’s research center in Campinas, providing suppliers with economies of scale and swift feedback for product development. Furthermore, heightened scrutiny from ANVISA in São Paulo and Rio de Janeiro has led to a stricter adherence to RDC 989/2025, subsequently boosting the demand for biodegradable and enzyme-enhanced formulations.

Brazil’s South, encompassing Paraná, Santa Catarina, and Rio Grande do Sul, not only anchors the nation's poultry and pork export complex but also hosts automotive and electronics parks. These industries increasingly depend on solutions like Clean-in-Place, metal pre-treatment, and precision cleaning. A testament to the rising IoT influence in hospitality is Ecolab’s 3D TRASAR installation at a resort in Santa Catarina. Consequently, the South's market for industrial and institutional cleaning chemicals leans heavily towards high-performance degreasers and water-efficient dosing systems.

In the Center-West, where soybean and beef production thrives, there's a heightened emphasis on sanitation in meat plants and grain elevators. Additionally, glycerin streams from local sugarcane ethanol mills are fueling bio-surfactant initiatives, seamlessly linking agricultural output with chemical demand. Moving to the Northeast, the cashew-nut-shell liquid is pivotal for producing phenolic surfactants. Meanwhile, processors of seafood and tropical fruits are on the lookout for disinfectants that meet stringent export standards. Although there's a tendency for cost-driven purchasing and a market for informal products due to relaxed enforcement outside the Southeast, impending federal decrees on chemical-substance inventories hint at a future of tighter nationwide regulation.

In summary, suppliers are fine-tuning their market strategies to align with regional nuances: offering compliance-focused, tech-driven solutions in the Southeast and South, while adopting a more price-sensitive and logistics-flexible approach in the Center-West and Northeast. This strategic geographic tailoring is bolstering the nationwide penetration of Brazil's industrial and institutional cleaning chemicals market.

Competitive Landscape

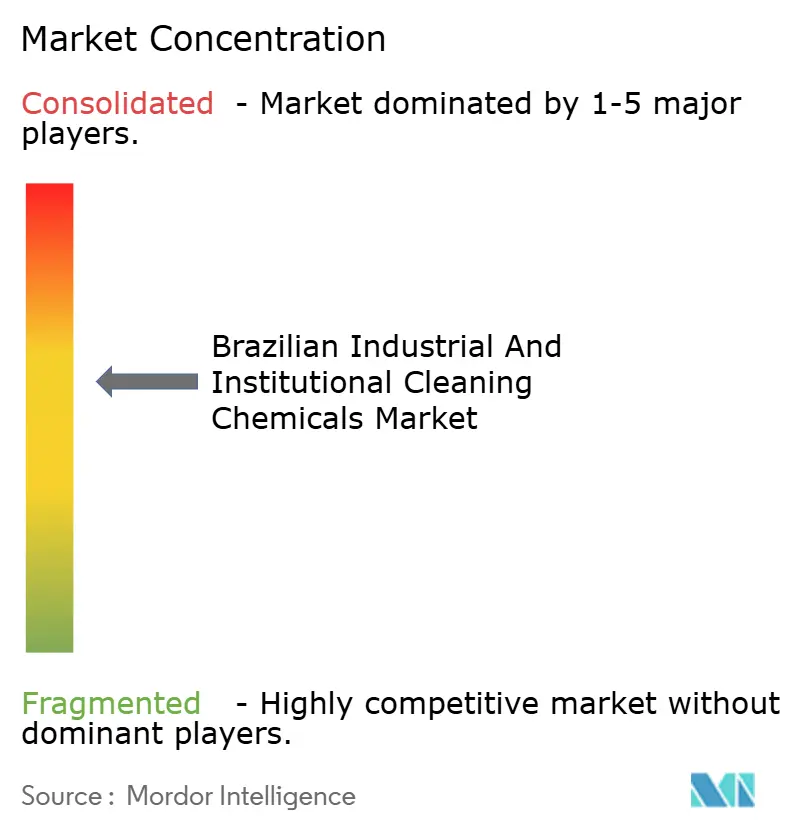

The Brazilian industrial and institutional cleaning chemicals market is moderately consolidated. Consolidation extends beyond chemicals. Suzano and Kimberly-Clark’s joint venture integrates industrial wiping and professional-cleaning brands, broadening distribution. Product pipelines emphasize safer chemistry. Domestic firms respond with refill pouches and diluted concentrates that fit lower-capex channels. Informal suppliers still serve micro-enterprises but face rising enforcement risk as ANVISA tightens oversight. Consequently, technical differentiation, regulatory compliance, and digital service capability separate premium players from price-takers within the Brazilian industrial and institutional cleaning chemicals market.

Brazilian Industrial And Institutional Cleaning Chemicals Industry Leaders

Unilever

Reckitt Benckiser Group PLC

Grupo MCassab

Bombril

Ecolab

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Nouryon broke ground on a customer experience and innovation center in Itupeva, aiming to accelerate specialty-surfactant development for home and institutional cleaners.

- March 2024: Univar Solutions entered a new Brazilian distribution agreement with Arxada to supply biocides, preservatives, and performance additives across industrial markets.

Brazilian Industrial And Institutional Cleaning Chemicals Market Report Scope

Industrial and Institutional (I&I) cleaning chemicals are defined as concentrated, high-performance substances specifically formulated for heavy-duty cleaning, sanitation, and maintenance of non-residential facilities, including factories, hospitals, schools, hotels, and commercial buildings. These chemicals are typically sold in bulk—such as drums or pails—and are designed to effectively remove grease, oils, microorganisms, and dirt.

The market is segmented by raw material, product type, and market type. By raw material, the market is segmented into chlor-alkali, surfactants, solvents, phosphates, biocides, and others. By product type, the market is segmented into general-purpose cleaners, disinfectants and sanitizers, warewashing and dishwashing, laundry care, vehicle wash products, and others (metal, electronic component cleaning products, etc.). By market type, the market is segmented into commercial and manufacturing.

By Raw Material

| Chlor-alkali |

| Surfactants |

| Solvents |

| Phosphates |

| Biocides |

| Others |

By Product Type

| General-Purpose Cleaners |

| Disinfectants and Sanitizers |

| Warewashing and Dishwashing |

| Laundry Care |

| Vehicle Wash Products |

| Others (Metal, Electronic Component Cleaning Products, etc.) |

By Market Type

| Commercial | Food Service |

| Retail | |

| Laundry and Dry-Cleaning | |

| Healthcare | |

| Car Wash | |

| Offices, Hotels and Lodging | |

| Manufacturing | Food and Beverage Processing |

| Fabricated Metal Products | |

| Electronic Components | |

| Other Manufacturing Processes |

| By Raw Material | Chlor-alkali | |

| Surfactants | ||

| Solvents | ||

| Phosphates | ||

| Biocides | ||

| Others | ||

| By Product Type | General-Purpose Cleaners | |

| Disinfectants and Sanitizers | ||

| Warewashing and Dishwashing | ||

| Laundry Care | ||

| Vehicle Wash Products | ||

| Others (Metal, Electronic Component Cleaning Products, etc.) | ||

| By Market Type | Commercial | Food Service |

| Retail | ||

| Laundry and Dry-Cleaning | ||

| Healthcare | ||

| Car Wash | ||

| Offices, Hotels and Lodging | ||

| Manufacturing | Food and Beverage Processing | |

| Fabricated Metal Products | ||

| Electronic Components | ||

| Other Manufacturing Processes | ||

Key Questions Answered in the Report

How large is the Brazilian industrial and institutional cleaning chemicals market in 2026?

The Brazilian industrial and institutional cleaning chemicals market size was USD 1.80 billion in 2026.

What is the expected growth rate for cleaning chemicals used in Brazilian institutions through 2031?

The overall market is projected to expand at a 3.08% CAGR from 2026 to 2031, reaching USD 2.10 billion.

Which raw material segment holds the largest share in Brazil’s professional cleaning sector?

Surfactants led with 37.69% of Brazilian industrial and institutional cleaning chemicals market share in 2025.

Why are disinfectants growing faster than general cleaners in Brazil?

Persistent infection-control protocols in healthcare and food-service facilities are driving a 4.96% CAGR for disinfectants through 2031.

What role do bio-based surfactants play in Brazil’s cleaning-chemicals outlook?

Rising ethanol and cashew processing yields abundant glycerin and phenolic feedstocks, enabling cost-competitive, lower-carbon bio-surfactants that align with stricter ANVISA biodegradability rules.

Page last updated on: