Blood Culture Tests Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 7.47 Billion |

| Market Size (2031) | USD 12.19 Billion |

| Growth Rate (2026 - 2031) | 10.29% CAGR |

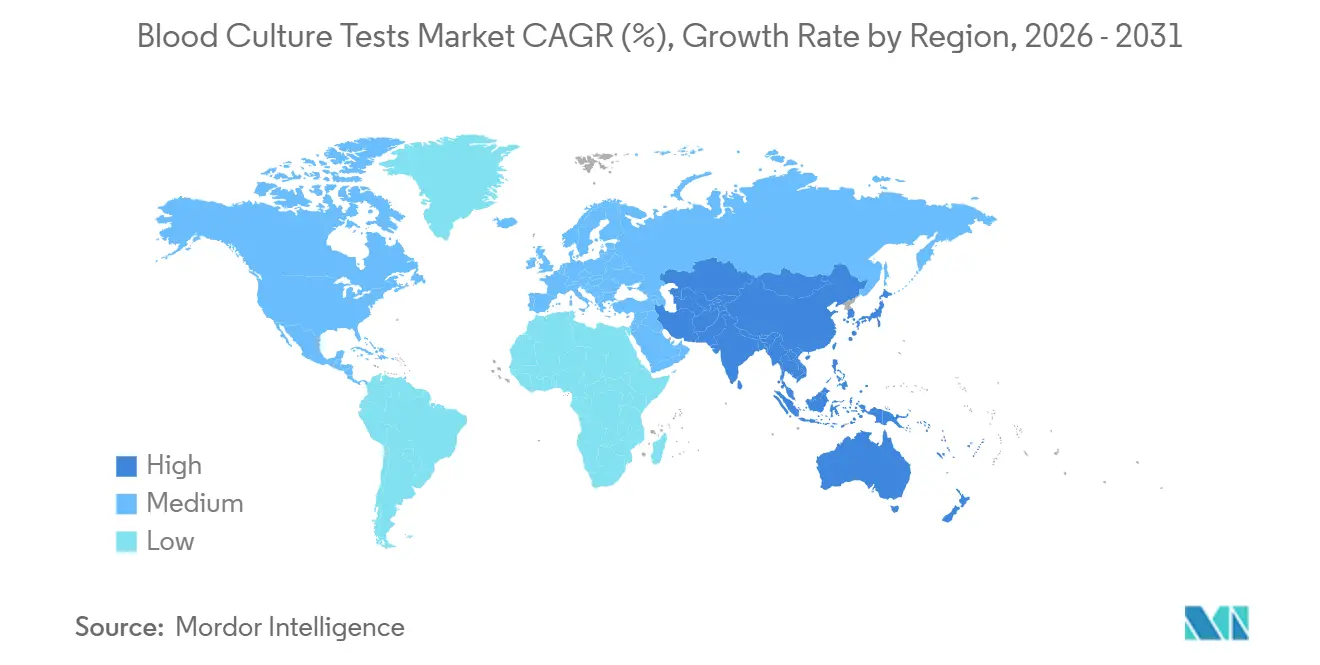

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

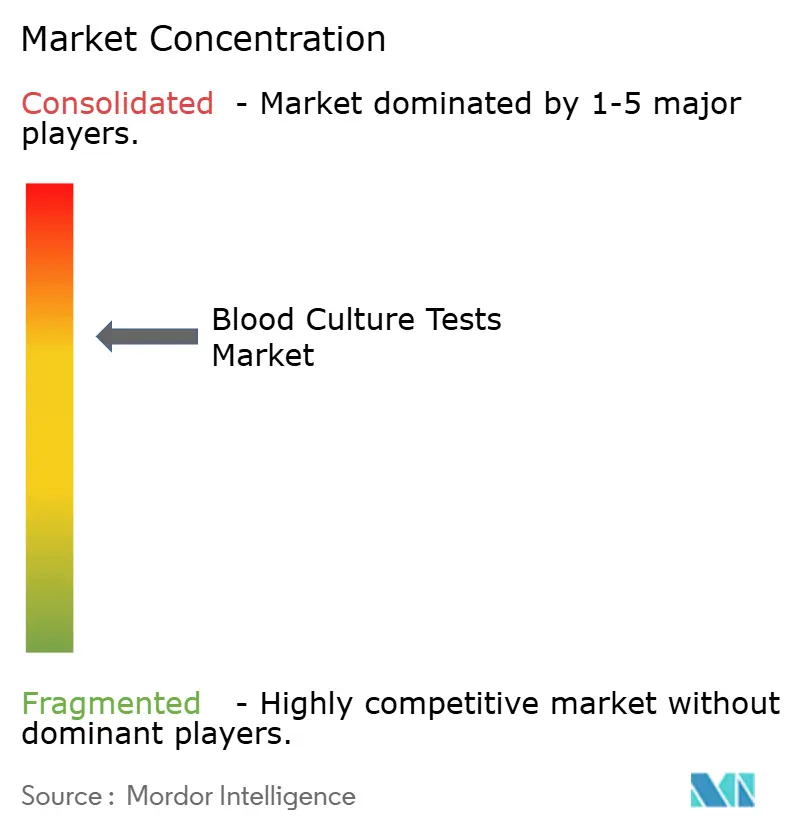

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Blood Culture Tests Market Analysis by ���ϲ�����

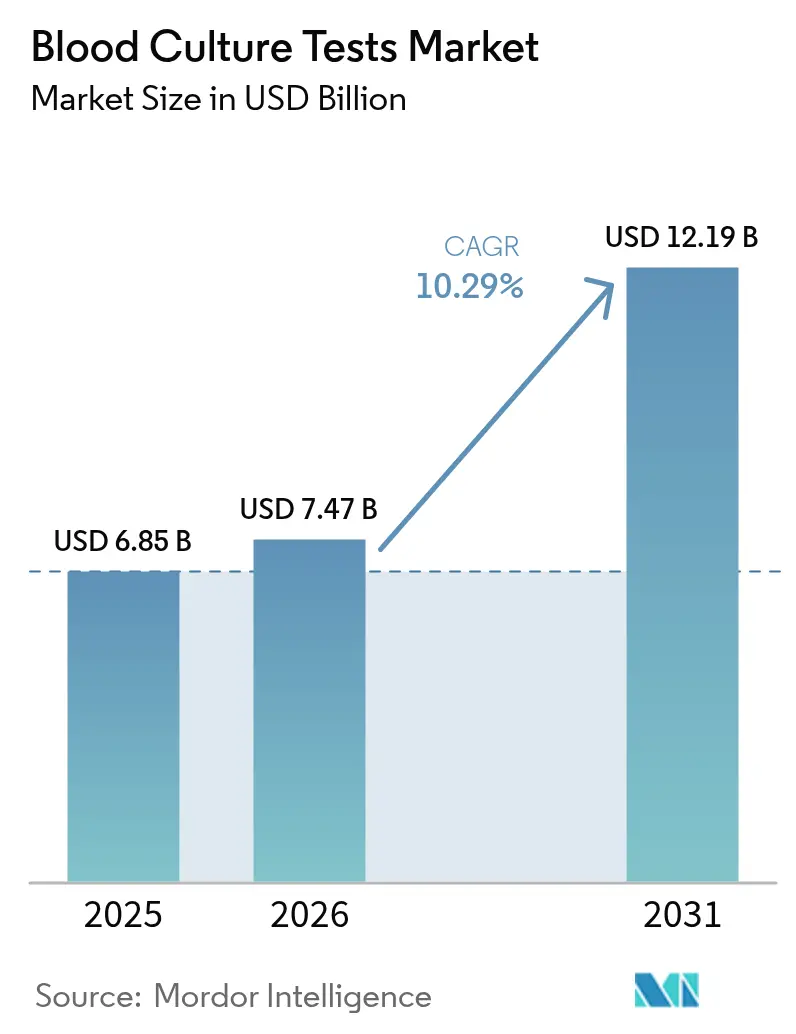

The Blood Culture Tests Market size is expected to increase from USD 6.85 billion in 2025 to USD 7.47 billion in 2026 and reach USD 12.19 billion by 2031, growing at a CAGR of 10.29% over 2026-2031.

Supply-chain fragility shown by the July 2024 BD BACTEC media outage, the continued clinical and financial burden of sepsis, and rising confidence in culture-independent platforms have reordered procurement priorities across hospital microbiology. Because a conventional blood culture takes as long as five days to deliver definitive results, optimal empiric therapy reaches only half of septic patients, keeping mortality at roughly 350,000 U.S. lives per year and costs at USD 62 billion. Automated incubators paired with real-time connectivity now process more than four-fifths of specimens, while software modules that stream live positivity alerts into stewardship dashboards are scaling even faster as hospitals chase value-based reimbursement targets.

Key Report Takeaways

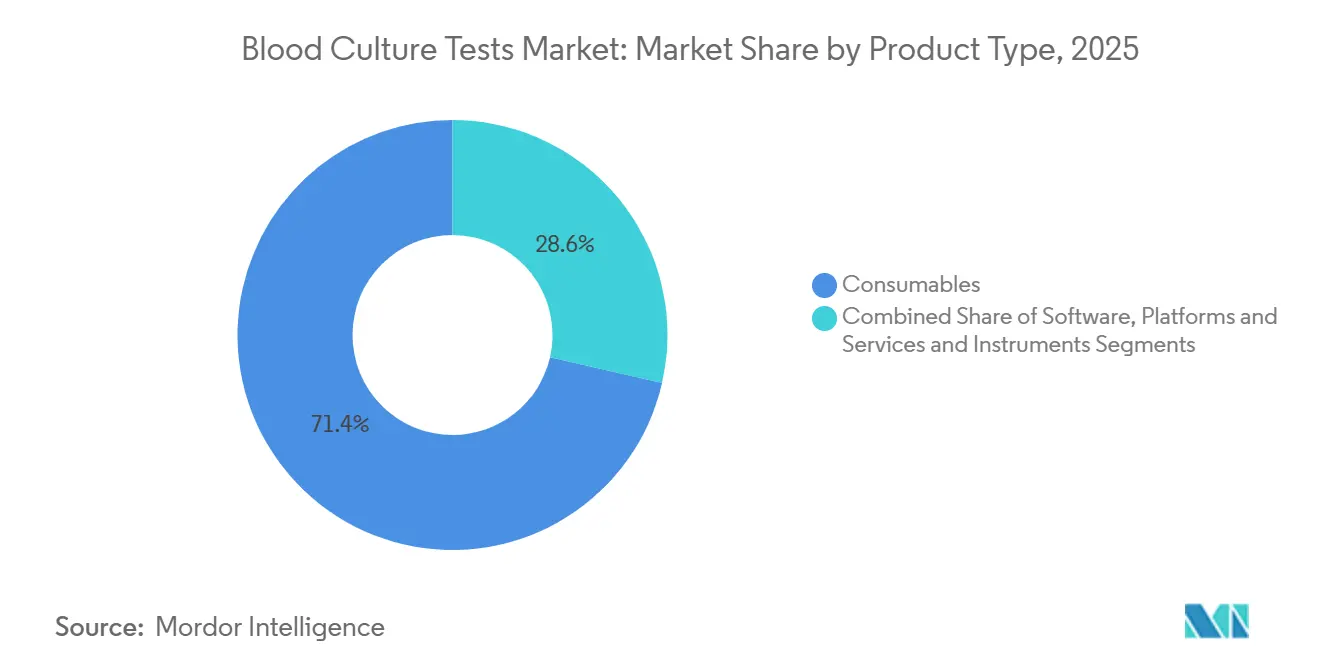

- By product type, consumables commanded 71.42% of 2025 revenue; software, platforms, and services are on track for the fastest growth at a 14.63% CAGR through 2031.

- By method, automated workflows held 81.57% of the blood culture tests market share in 2025, and the segment is projected to expand at a 13.83% CAGR over 2026-2031.

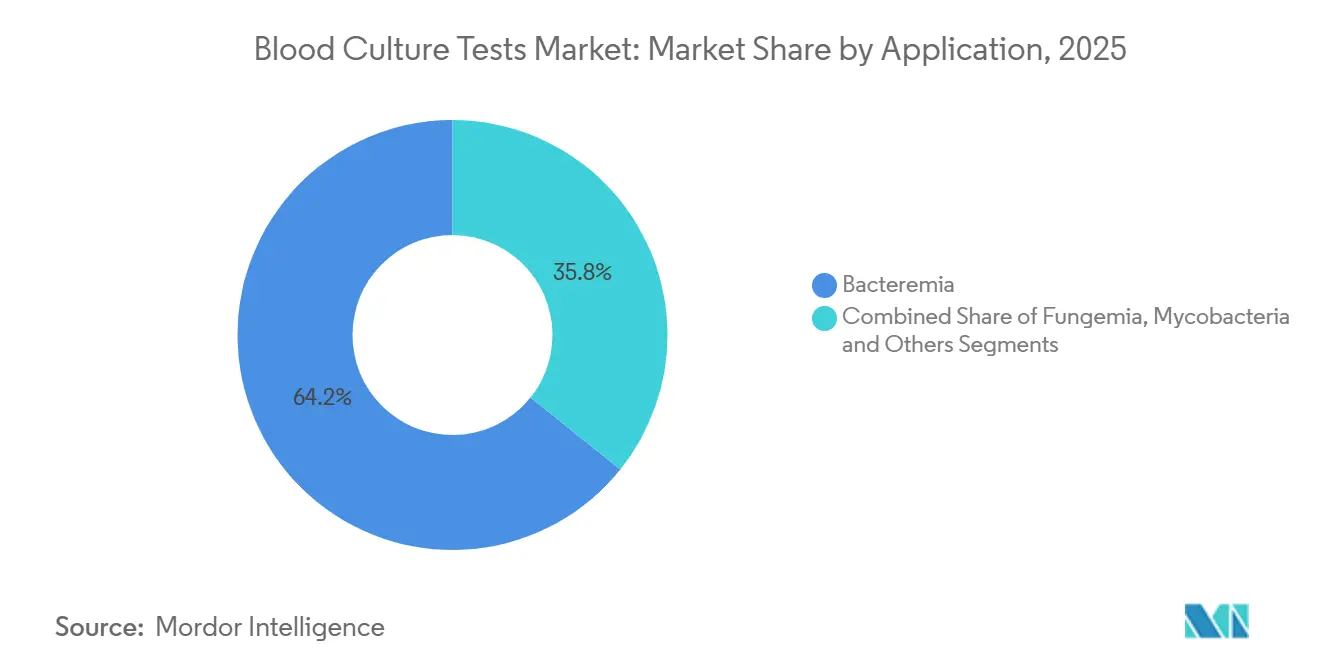

- By application, bacteremia represented 64.24% of the blood culture tests market size in 2025, whereas mycobacteria testing is advancing at a 12.63% CAGR to 2031.

- By end user, hospital laboratories accounted for 66.11% of 2025 revenue, while reference laboratories are forecast to post a 13.31% CAGR during the same period.

- Geographically, North America led with 41.82% of global revenue in 2025; Asia-Pacific is projected as the fastest-growing region at a 12.72% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Blood Culture Tests Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Incidence of Bloodstream Infections and Sepsis | +2.1% | Global, with acute pressure in North America and Europe | Short term (≤ 2 years) |

| Growing Demand for Rapid Diagnostic Techniques in Hospitals | +1.9% | North America, Europe, APAC urban centers | Medium term (2-4 years) |

| Technological Advancements in Automated Blood-Culture Systems | +1.6% | Global, led by North America and Europe | Medium term (2-4 years) |

| Favourable Reimbursement Policies for Sepsis Testing | +1.4% | North America, select European markets | Short term (≤ 2 years) |

| Antibiotic-Stewardship Programmes Boosting Test Volumes | +1.3% | Global, with regulatory mandates in North America and Europe | Long term (≥ 4 years) |

| Expansion of Testing Capacity in Outpatient Infusion Centres | +0.8% | North America, emerging in APAC | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Rising Incidence of Bloodstream Infections and Sepsis

Sepsis accounts for 49 million global cases and 11 million deaths every year, numbers that anchor 2026 health-security debates.[1] Danielle Stanek, “Sepsis Fact Sheet,” World Health Organization, who.int In the United States it remains the top inpatient killer, adding USD 62 billion in hospitalization expenditures while successful early therapy hinges on faster pathogen identification. Fungal threats amplify risk; U.S. surveillance recorded 36% of the 8,033 Candida auris isolates captured in 2022-2023 stemmed from blood cultures.[2]Michael Craig, “Candida auris Surveillance and Laboratory Capacity — United States, 2022–2023,” Centers for Disease Control and Prevention, cdc.gov Each hour of antimicrobial delay raises mortality up to 8%, a reality driving hospitals to invest in next-generation diagnostics that slash time-to-result and sustain double-digit expansion for the blood culture tests market.

Growing Demand for Rapid Diagnostic Techniques in Hospitals

Hospital payment models now tie reimbursement to documented time-to-appropriate therapy. Traditional culture workflows delay actionable results for up to five days, but T2Bacteria delivers species calls in under five hours directly from whole blood, and Accelerate Arc provides phenotypic susceptibility within seven hours from a positive bottle.[3]Kristina Iacovino, “510(k) Premarket Notification Database,” U.S. Food and Drug Administration, fda.gov Evidence shows these platforms move targeted therapy 42 hours sooner and cut intensive-care stays by five days, outcomes that translate into immediate cost avoidance.

Technological Advancements in Automated Blood-Culture Systems

Continuous monitoring, automated Gram staining, and MALDI-TOF identification are converging on single consoles. Bruker’s MALDI Biotyper earned FDA clearance in 2025 for direct Candida auris calls from positive bottles, furnishing species-level data within 30 minutes of growth detection. BD’s USD 17.5 billion pursuit of Waters aims to add mass-spectrometry precision to its BACTEC line, potentially offering metabolite-based identification that bypasses subculture steps. These advances drive up-front capital requirements yet lower touchpoints, reduce contamination, and reinforce automated dominance in the blood culture tests market.

Favorable Reimbursement Policies for Sepsis Testing

CMS applied a 2.4% Consumer Price Index update to the 2025 Clinical Laboratory Fee Schedule and introduced 21 new PLA codes covering advanced infectious-disease diagnostics. Payment reductions for non-ADLT tests are now capped at 15% a year through 2028, giving laboratories budget predictability. Commercial payers are layering value-based clauses that pay bonuses for shorter hospital stays, reinforcing hospital demand for rapid culture or culture-independent methods.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Automated Instruments & Consumables | -1.2% | Global, acute in low- and middle-income countries | Medium term (2-4 years) |

| Risk Of Contamination and False Positives | -0.9% | Global, with regulatory scrutiny in North America and Europe | Short term (≤ 2 years) |

| Shift Toward Syndromic Molecular Panels Bypassing Culture | -1.1% | North America, Europe, APAC urban centers | Medium term (2-4 years) |

| Limited Cold-Chain Logistics in Low-Income Regions | -0.6% | Sub-Saharan Africa, South Asia, Latin America rural areas | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

High Cost of Automated Instruments & Consumables

An analyzer costs between USD 80,000 and USD 150,000, and annual service contracts add another 10-15% of purchase price. A 2024 Lancet Microbe survey showed 28.8% of low-income nations pay more than USD 15 per blood culture, a figure that deters automation. The July 2024 BD BACTEC bottle shortage magnified cost anxiety by proving how single-vendor dependence can halt testing in under-resourced hospitals.

Risk of Contamination and False Positives

Contamination rates hover at 2-3%, adding USD 4,000-8,000 per event in unnecessary care, and the College of American Pathologists pegs ≤3% as the quality benchmark. New CDC guidelines urge skin antisepsis, closed-loop collection devices, and specialized phlebotomy teams, but adoption remains uneven, particularly outside tertiary centers.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Consumables Drive Recurring Demand

Consumables generated 71.42% of 2025 revenue in the blood culture tests market and spiked during the second half of 2024 as laboratories stockpiled BD alternatives after the media shortage. Instruments capture smaller share yet remain indispensable. Software, platforms, and services are sprinting at a 14.63% CAGR. BD Synapsys, BD EpiCenter, and �����Dz�é������ܳ� MYLA now deliver live positivity alerts into electronic health records, reducing phone calls and trimming labor costs. In a value-based care environment, such dashboards are no longer optional but rather accreditation expectations. Accessories—from disinfectant-capped bottles to sterile transfer devices—move in lockstep with media sales and benefit from heightened contamination-control protocols.

By Method: Automation Dominates, Manual Workflows Persist

Automation accounted for 81.57% of 2025 revenue and will expand at a 13.83% CAGR through 2031 as multi-hospital systems centralize microbiology. A typical BD BACTEC FX unit can flag growth within 9-14 hours and, when coupled with Bruker MALDI-TOF, deliver species calls inside 30 minutes, shrinking total turnaround by nearly two days compared with manual methods. Nonetheless, 18.43% of testing remains manual, centered in under-funded facilities where electricity is unreliable and volumes are thin. India’s PM-ABHIM plan to outfit 730 district labs with semi-automated incubators should nudge some of these users toward entry-level automation. Meanwhile, culture-independent systems like T2Dx are on track to secure 5-7% of automated revenue by 2031 after Cardinal Health placed the platform in over 6,000 U.S. hospitals.

By Application: Bacteremia Leads, Mycobacteria Surges

Bacteremia accounted for 64.24% of 2025 segment revenue, sustained by required reporting of central-line infections to CMS and The Joint Commission. Rapid ESKAPE pathogen identification by panels such as T2Bacteria drives additional growth in high-acuity wards. The blood culture tests market size for mycobacteria applications is projected to leap 12.63% annually as WHO tuberculosis goals force resource-focused nations to adopt BD MGIT liquid culture in tandem with molecular detection. Fungemia testing, though smaller, is benefiting from widespread Candida auris screening mandates; Bruker’s freshly cleared workflow flags the organism within hours, tightening infection-control loops. The “Others” bucket—including anaerobes and fastidious organisms—retains niche relevance, especially in tertiary centers that perform transplant workups.

By End User: Hospital Labs Still Command, Reference Networks Accelerate

Hospital laboratories captured 66.11% of 2025 revenue because sepsis bundles mandate blood cultures within one hour of fever onset and most U.S. hospitals choose on-site processing to meet the deadline. Yet reference laboratories ride a 13.31% CAGR; Quest’s eight 2024 acquisitions add USD 1 billion in annual revenue and deepen logistics reach. Labcorp’s 110,000 ft² Raritan expansion can now handle 110,000 daily specimens, signaling commitment to high-volume outreach. Academic and government research centers, while a smaller slice, continue to anchor surveillance and validation studies crucial to guideline updates.

Geography Analysis

North America held 41.82% of 2025 revenue after CMS lifted the 2025 laboratory fee schedule by 2.4% and added 21 PLA codes for advanced infectious-disease tests. The BD media shortage accelerated U.S. discussion on culture-independent backstops, helping T2 Biosystems secure exclusive distribution via Cardinal Health. Canada, through LifeLabs, accounts for roughly 2% of regional revenue, while Mexico’s IMSS modernization program drives incremental analyzer placements.

Asia-Pacific is forecast to grow 12.72% annually, the highest for any region. India’s PM-ABHIM blueprint funds 730 Integrated Public Health Laboratories; Japanese policymakers launched the Japan Institute for Health Security in April 2025 with antimicrobial-resistance surveillance as a pillar. China’s EUR 300.99 million ADB loan will finish new provincial labs by 2027, embedding quality microbiology in Guangxi, Guizhou, and Shaanxi. Australia and South Korea maintain high automation penetration, while Indonesia and the Philippines partner with private labs to bolster capacity.

Europe remains robust as ESCMID guidelines codify culture-guided therapy; hospitals in Germany and France are replacing decade-old incubators with BD, �����Dz�é������ܳ�, and Bruker systems that bundle connectivity. The Middle East and Africa show uneven progress: Gulf states finance state-of-the-art infection-control labs, yet Sub-Saharan Africa wrestles with electricity and cold-chain gaps, sustaining manual dominance. South America, led by Brazil’s SUS upgrades, is installing semi-automated platforms in tertiary centers while rural outposts depend on couriered samples to regional hubs.

Competitive Landscape

The top tier of the blood culture tests market is moderately consolidated. BD, �����Dz�é������ܳ�, and Bruker dominate automated placements via capital-equipment agreements that lock customers into proprietary media and service contracts. BD’s USD 17.5 billion Waters acquisition points toward a future where metabolite fingerprints could displace some culture steps.

Culture-independent innovation sits in a white-space niche. T2 Biosystems now taps Cardinal Health’s 6,000-hospital footprint; its T2Bacteria and T2Candida panels give three-to-five-hour pathogen calls from whole blood, bypassing the incubator entirely. Accelerate Diagnostics won FDA clearance for Accelerate Arc in September 2024 and filed WAVE in March 2025, both offering under-eight-hour phenotypic susceptibility. Software ecosystems secure stickiness; BD Synapsys, �����Dz�é������ܳ� MYLA, and independent LIS players compete to own the stewardship dashboard that pharmacists and infection-control leaders view daily.

Blood Culture Tests Industry Leaders

Becton, Dickinson and Company

�����Dz�é������ܳ�

F. Hoffmann-La Roche AG

Danaher Corp.

Thermo Fisher Scientific Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: SSG Hospital in India installed an automated culture system processing 80 samples per run under a GETCO CSR grant.

- March 2025: Accelerate Diagnostics, Inc., submitted its Accelerate WAVE system and a positive blood culture gram-negative test kit to the U.S. Food and Drug Administration (FDA) seeking 510(k) clearance.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the blood culture tests market as the value generated from commercial sales of consumables, instruments, and associated laboratory services used to isolate and identify microorganisms directly from patient blood samples in accredited clinical laboratories worldwide.

Procedures performed at the bedside or on non-blood specimens (urine, CSF, sputum) fall outside this scope.

Scope Exclusion: Rapid point-of-care sepsis panels run outside a laboratory setting are not counted.

Segmentation Overview

- By Product Type

- Instruments

- Automated Blood Culture Instruments

- Manual/Conventional Instruments

- Consumables

- Media

- Assay Kits & Reagents

- Accessories & Disposables

- Software, Platforms, and Services

- Instruments

- By Method

- Conventional/Manual

- Automated

- Automated Microbial Detection Systems

- Automated Gram-Staining Systems

- Others

- By Application

- Bacteremia

- Fungemia

- Mycobacteria

- Others

- By End User

- Hospital Laboratories

- Reference Laboratories

- Academic & Research Institutes

- Others (POC / Clinics)

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Telephone interviews and short surveys with microbiologists, infection-control nurses, procurement heads, and regional distributors across North America, Europe, and Asia Pacific helped us validate market share moves, average selling prices, and the pace of automation roll-outs, filling data gaps flagged during desk work.

Desk Research

We began with exhaustive desk work, drawing on open datasets from the CDC's National Healthcare Safety Network, ECDC's Antimicrobial Resistance Surveillance, WHO Global Health Observatory, and trade statistics from UN Comtrade for culture-media ingredient flows. Clinical adoption trends were cross-checked through PubMed meta-analyses and guidelines from bodies such as CLSI. Company 10-Ks, FDA 510(k) listings, and import-export filings were then screened to collect baseline shipment and price clues. Premium sources, including D&B Hoovers for manufacturer financial splits and Dow Jones Factiva for deal flow, supplemented public material. This list is illustrative; many additional references informed our evidence base.

Market-Sizing & Forecasting

A unified model applies a top-down hospital procedure pool built from sepsis incidence, blood-culture per-case penetration, and average tests per admission, and is balanced with selective bottom-up vendor revenue roll-ups for cross-check. Key variables include intensive-care bed density, antimicrobial resistance alerts, reimbursement fee schedules, automation penetration rate, and median consumable ASP. Five-year forecasts rely on multivariate regression with scenario stress tests, guided by expert consensus on infection trends and technology uptake. Where bottom-up totals under-represent fast-growing regions, gap factors are transparently applied and documented.

Data Validation & Update Cycle

Outputs pass two analyst reviews and variance screens against external infection and trade benchmarks. Models refresh annually; interim recalculations are triggered by material events such as major product launches or guideline changes, ensuring clients always receive the latest view.

Why Mordor's Blood Culture Tests Baseline Numbers Inspire Confidence

Published figures often differ because each publisher selects unique product baskets, base years, and price assumptions, then updates them on different clocks.

Key drivers of gaps include the inclusion of non-laboratory rapid tests, higher assumed test prices, or aggressive growth multipliers linked to post-COVID sepsis awareness, elements that Mordor's disciplined scope and moderated scenarios purposely exclude.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.39 B (2025) | ���ϲ����� | - |

| USD 6.60 B (2024) | Global Consultancy A | Counts bloodstream infection panels and emergency-department POC kits, inflating base size |

| USD 6.74 B (2024) | Regional Consultancy B | Applies uniform 12% ASP uplift and higher automation penetration assumptions |

| USD 5.20 B (2023) | Industry Journal C | Older base year combined with linear CAGR extension; refresh cadence every five years |

Taken together, these comparisons show that Mordor analysts favor a narrowly defined, annually refreshed baseline grounded in observable hospital usage and validated ASPs, delivering a balanced and reproducible foundation for strategic decisions.

Key Questions Answered in the Report

How large is the blood culture tests market in 2026?

It is valued at USD 7.47 billion, with a projected 10.29% CAGR to reach USD 12.19 billion by 2031.

Which segment of the blood culture tests market is growing fastest?

Software, platforms, and services are forecast to rise at 14.63% CAGR as hospitals prioritize data connectivity.

Why is Asia-Pacific considered the most attractive growth region?

Government programs in India, Japan, and China are funding hundreds of new public-health laboratories, pushing regional CAGR to 12.72%.

How are rapid molecular panels affecting demand for traditional cultures?

Syndromic panels can trim culture volumes 10-15% in high-acuity units, but susceptibility testing requirements keep culture relevant.

What is the main cost barrier for low-income hospitals?

Analyzer capital costs of USD 80,000-150,000 plus annual service fees and expensive media push per-test costs above USD 15.

Page last updated on: