Bladder Scanners Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

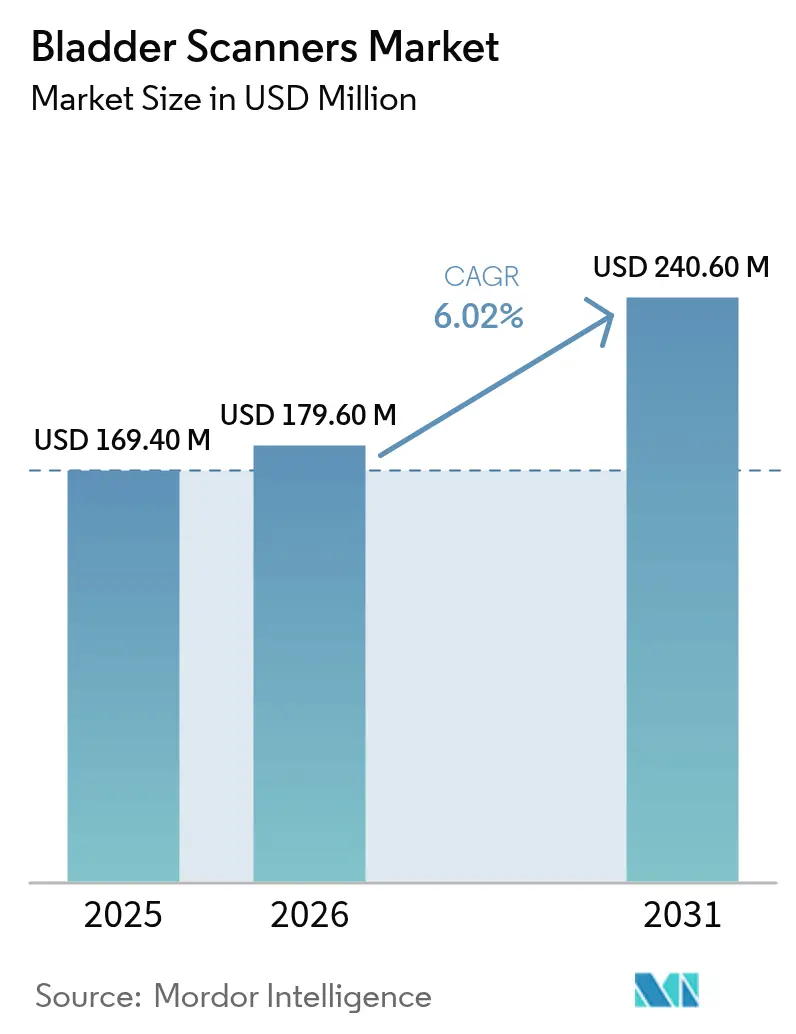

| Market Size (2026) | USD 179.60 Million |

| Market Size (2031) | USD 240.60 Million |

| Growth Rate (2026 - 2031) | 6.02% CAGR |

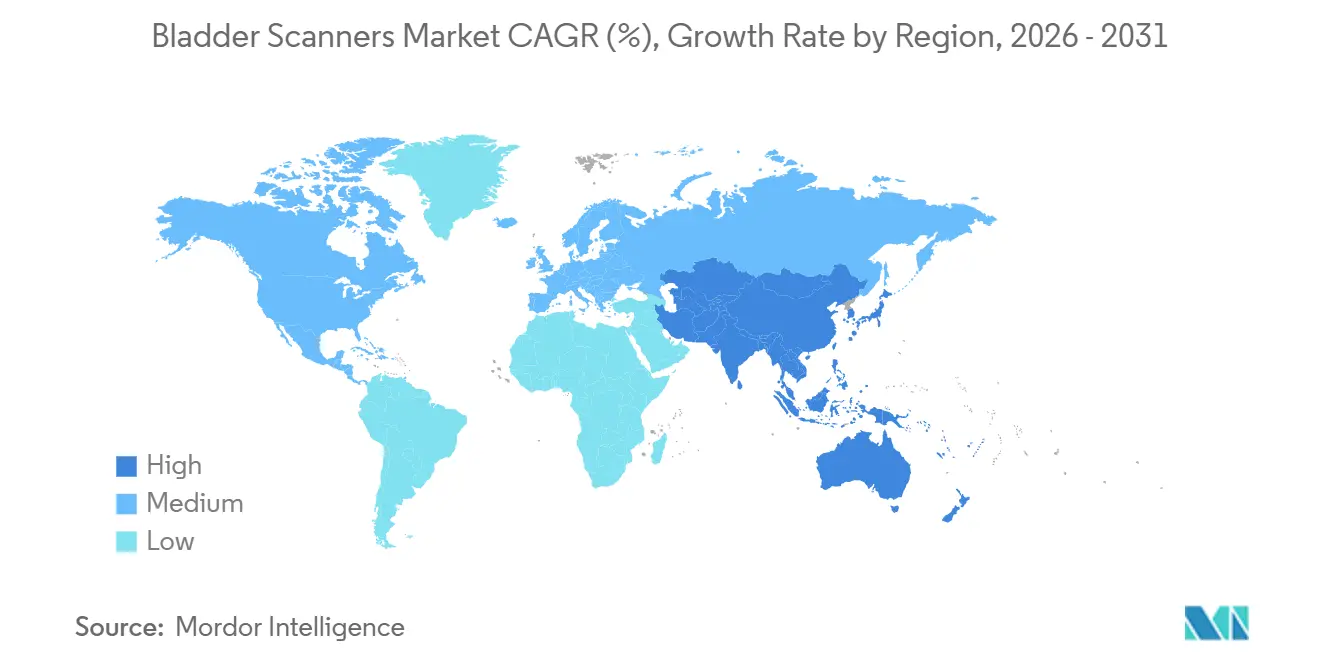

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Bladder Scanners Market Analysis by ���ϲ�����

The Bladder Scanners Market size is projected to expand from USD 169.40 million in 2025 and USD 179.60 million in 2026 to USD 240.60 million by 2031, registering a CAGR of 6.02% between 2026 to 2031.

Accelerating adoption in acute and post-acute care, increasing regulatory clearances for artificial intelligence (AI)-enabled devices, and cost pressures associated with catheter-associated urinary tract infections (CAUTIs) are the primary factors driving robust market growth. Device vendors are utilizing AI-based 3-D volumetric imaging to enhance clinical accuracy beyond a 0.97 correlation with gold-standard computed tomography, thereby expanding the use of point-of-care ultrasound among non-radiologist clinicians. Government reimbursement reforms, particularly the United States Current Procedural Terminology (CPT) 51798 payment for bladder volume scanning and Japan’s Diagnosis-Related Group (DRG) incentives, are reducing return-on-investment cycles for hospitals and ambulatory surgical centers (ASCs). Additionally, demographic aging is increasing long-term demand for non-invasive urinary monitoring in rehabilitation and home-care settings. Portable and handheld platforms priced below USD 15,000 are improving access in resource-constrained facilities and gradually shifting volume away from benchtop systems.

Key Report Takeaways

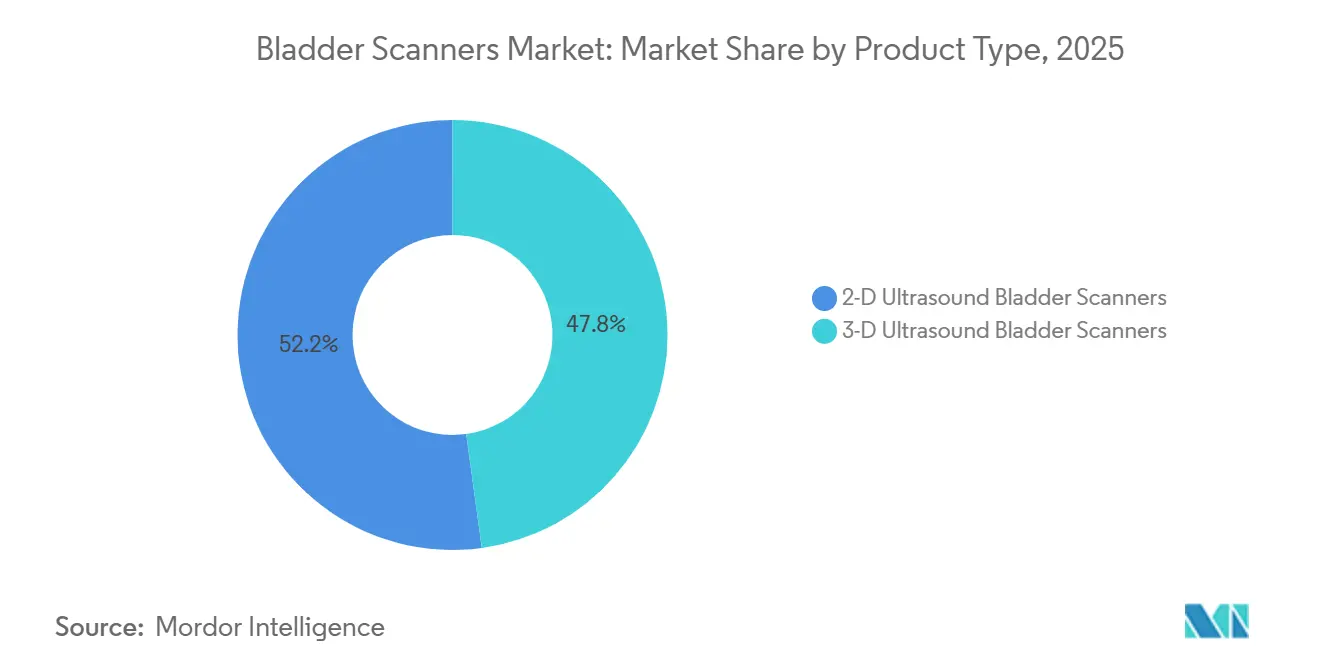

- By product type, 2-D ultrasound units led with 52.18% of the bladder scanner market share in 2025, while 3-D models are advancing at a 7.50% CAGR to 2031.

- By portability, cart-based systems held 64.70% revenue share of the Bladder scanner market size in 2025; handheld devices are forecast to post a 6.38% CAGR through 2031.

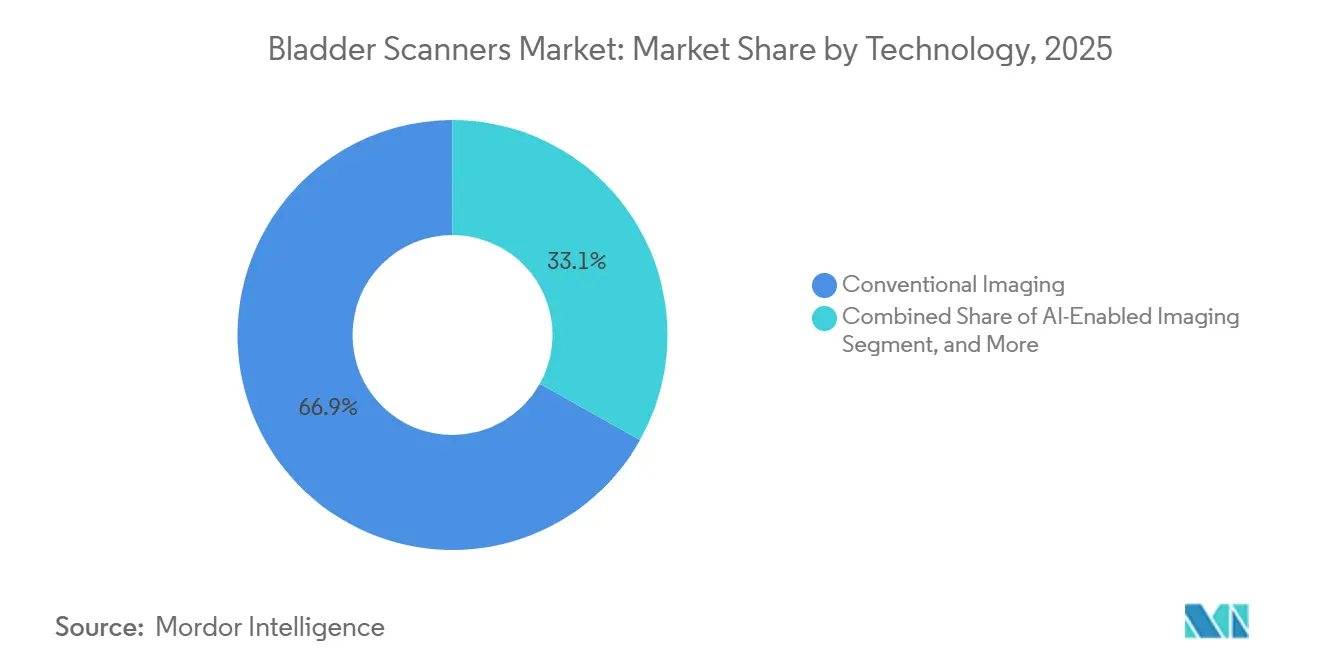

- By technology, conventional imaging retained 66.88% share in 2025, while AI-enabled scanners are projected to grow at 6.89% between 2026-203.

- By end user, hospitals and clinics generated 72.22% of 2025 revenue, yet ASCs will register the fastest 6.47% CAGR through 2031.

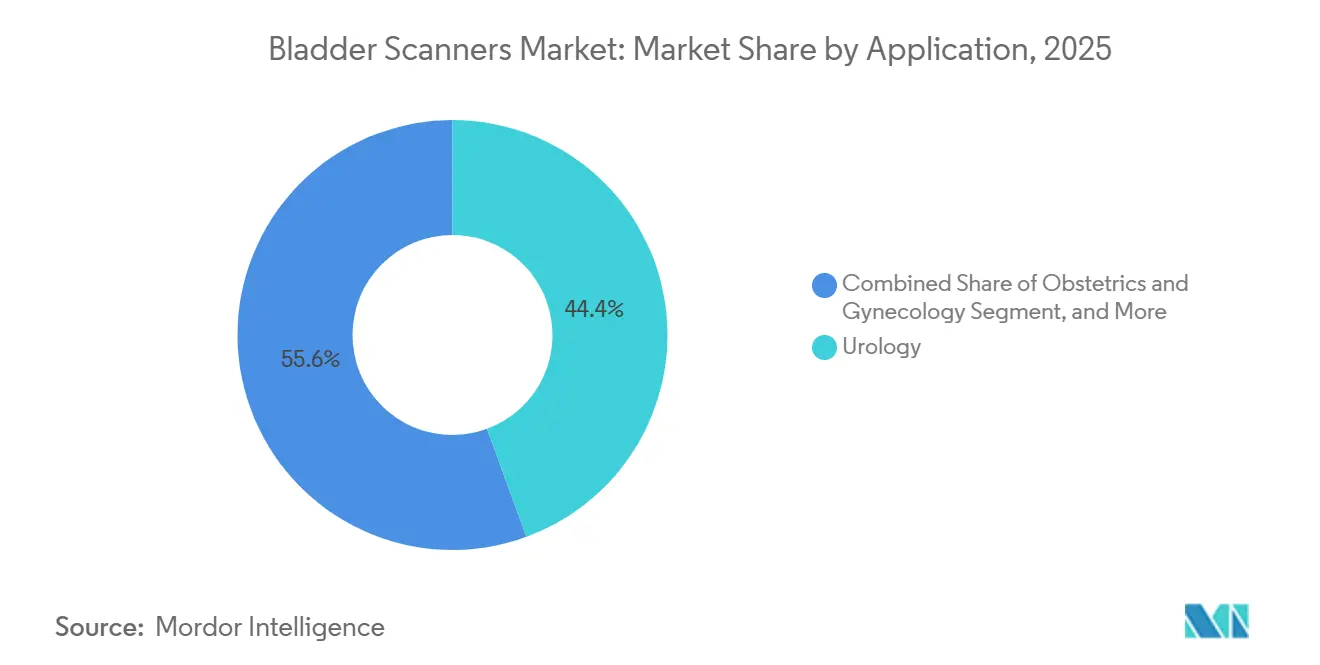

- By application, urology generated 44.40% of 2025 revenue, and obstetrics & gynecology will register the fastest 7.44% CAGR through 2031.

- By region, North America captured 38.74% of global sales in 2025; Asia-Pacific is projected to expand at 6.85% a year over 2026-2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Bladder Scanners Market Trends and Insights

Driver Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Aging population & increasing prevalence of urological conditions | +1.5% | Global, high in Japan, Europe, U.S. | Long term (≥ 4 years) |

| Surge in point-of-care ultrasound adoption in ED & peri-operative care | +1.3% | North America, Europe, APAC tier-1 cities | Medium term (2-4 years) |

| AI-enabled 3-D volumetric imaging enhancing diagnostic accuracy & billing compliance | +1.0% | North America, Western Europe, Japan | Medium term (2-4 years) |

| Eras protocols replacing routine catheterization with scanning | +1.2% | Global, early in North America, Northern Europe | Short term (≤ 2 years) |

| Growth of ambulatory & home-care settings needing non-invasive monitoring | +0.8% | North America, APAC urban centers | Medium term (2-4 years) |

| Healthcare cost containment initiatives | +0.7% | Global, U.S. value-based care | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Aging Population & Increasing Prevalence of Urological Conditions

By 2030, one in six people globally will be aged 60 or older, increasing the number of individuals susceptible to conditions such as benign prostatic hyperplasia and neurogenic bladder, both of which require regular post-void residual checks.[1]World Health Organization, “Ageing and Health,” who.int In Japan, the demographic challenge is evident: the percentage of individuals aged 65 and older is set to rise from 29.3% in 2024 to an estimated 34.8% by 2040, straining hospital capacities and promoting home-based bladder monitoring.[2]Statistics Bureau of Japan, “Population Estimates Monthly Report,” stat.go.jp Research indicates that postoperative urinary retention impacts up to 70% of specific surgical groups, while the risk of daily catheter-associated urinary tract infections (CAUTIs) from extended catheter use stands at 3-7%. As a result, non-invasive scanners play a pivotal role in infection prevention and align with value-based contracts that impose financial penalties for readmissions due to device-related urinary tract infections.

Surge in Point-of-Care Ultrasound Adoption in ED & Peri-Operative Care

Emergency departments have integrated ultrasound triage, reducing the time for diagnosing urinary retention from 45 minutes (previously reliant on radiology referrals) to under 5 minutes at the bedside. The Enhanced Recovery After Surgery pathways stipulate catheter removal on the first postoperative day, necessitating prompt assessments of residuals to prevent bladder overdistension. In 2024, the American College of Emergency Physicians officially designated bladder ultrasound as a core competency; as a result, residency programs now require 25 supervised scans for board eligibility.[3]Agency for Healthcare Research and Quality, “Toolkit for Reducing Catheter-Associated Urinary Tract Infections,” ahrq.gov Consequently, hospitals are gravitating towards portable ultrasound units, priced between USD 8,000-15,000, which achieve break-even points more swiftly than traditional carts exceeding USD 30,000.

AI-Enabled 3-D Volumetric Imaging Enhancing Diagnostic Accuracy & Billing Compliance

While traditional 2-D ellipsoid calculations can err by ±20% with irregular bladder geometries, AI-driven 3-D reconstructions reduce this error to under 10% and minimize operator variability. In 2025, FUJIFILM Sonosite unveiled a 46 megahertz probe that offers sub-millimeter resolution, enhancing scans for pediatric and obese patients. Automated reporting systems now seamlessly integrate with electronic medical records, auto-filling Current Procedural Terminology 51798 fields. This innovation has led to a 15-20% increase in billable scan volumes during the first year at select U.S. pilot sites.

ERAS Protocols Opt for Scanning Over Routine Catheterization

As per the 2024 updates to colorectal and orthopedic Enhanced Recovery After Surgery guidelines, indwelling catheter use is now capped at under 24 hours. Nursing staff is directed to depend on bladder scanning post this period. A 2025 meta-analysis highlighted a reduction in catheter reinsertion rates among hip-arthroplasty patients, dropping from 18% to 7% with the implementation of nurse-led scanning protocols.[4]Diagnostics, “Three-Dimensional Ultrasound Bladder Volume Measurement Accuracy,” mdpi.com In 2023, U.S. Ambulatory Surgery Centers, which conducted 38,600 knee arthroplasties, began using handheld scanners to meet same-day discharge requirements.[5]Centers for Disease Control and Prevention, “Catheter-associated Urinary Tract Infections,” cdc.gov

Restraint Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High capital cost for small practices | –0.9% | Global, acute in rural U.S., LMICs | Short term (≤ 2 years) |

| Shortage of trained sonographers in rural LMICs | –0.7% | Sub-Saharan Africa, South Asia, rural Latin America | Long term (≥ 4 years) |

| Inconsistent reimbursement codes outside the United States & Japan | –0.5% | Europe, Middle East, Latin America | Medium term (2-4 years) |

| Stringent regulatory and approval challenges | –0.4% | Global, focus on EU MDR, China NMPA | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

High capital cost and limited budgets in small practices

Entry-level portable scanners are priced at USD 8,000, while comprehensive three-dimensional (3-D) artificial intelligence (AI) platforms soar to USD 35,000, significantly exceeding the annual equipment budgets of rural clinics. The United States Medicare reimburses approximately USD 25 for each Current Procedural Terminology (CPT) 51798 scan. This reimbursement structure necessitates that low-volume offices perform between 320 to 1,400 procedures just to break even on their initial investment. While leasing options and the refurbished market provide some financial relief, a 7.5% tariff on finished scanners in India results in end-user prices being 15-20% steeper than those in North America.

Shortage of Trained Sonographers in Rural LMICs

By 2030, the World Health Organization predicts a shortfall of 11 million health workers, particularly imaging specialists, who are predominantly found in urban hospitals. AI-driven handheld devices, such as the Butterfly iQ+ Bladder, can annotate directly on smartphone screens, simplifying their usage. However, they still require certified oversight in regulated environments. Adoption is also hindered by Nigeria's electricity challenges, with 68% of clinics lacking a consistent 8-hour power supply.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: 3-D Scanners Gain Traction Despite 2-D Dominance

In 2025, two-dimensional devices commanded a dominant 52.18% share of the bladder scanner market, due to their integration into established nursing workflows and appealing price points. Meanwhile, three-dimensional scanners are projected to grow at a robust 7.50% compound annual growth rate (CAGR), driven by urologists' demand for volumetric precision in cases like prolapse and neurogenic bladder. In 2025, FUJIFILM unveiled a 46 MHz transducer, enhancing pediatric applications, and Canon rolled out dual-mode platforms, allowing seamless toggling between 2-D and 3-D imaging without probe changes. As we look ahead, price reductions from semiconductor-based arrays are expected to bridge the gap between basic 2-D and entry-level 3-D units, hastening the shift in technology adoption in Ambulatory Surgical Centers (ASCs) and educational hospitals.

Additionally, artificial intelligence (AI)-driven reimbursement incentives bolster this momentum. Medicare's automated data extraction from 3-D systems simplifies auditing, encouraging financial managers to modernize their equipment. While the European Union's post-market surveillance under the Medical Device Regulation (MDR) leans towards the decade-long safety track record of 2-D systems, hospitals are increasingly recognizing the clinical advantages of 3-D precision in intricate urological procedures. Consequently, while 2-D systems will continue to lead in volume, all new growth is set to favor 3-D systems through 2031.

By Portability: Cart-Based Systems Anchor Hospital Workflows

In 2025, cart-based platforms dominated the bladder scanner market, accounting for 64.70% of the market share. Their success is attributed to seamless integration with electronic medical records and robust battery life, allowing emergency departments to scan up to 100 patients daily. These carts, equipped with 12-inch displays and mobile wheeled stands, facilitate easy movement across departments, a feature highly valued by infection-control committees. Looking ahead, this sub-segment is projected to grow at a 6.38% CAGR until 2031, driven by hospitals in Latin America and Southeast Asia modernizing their radiology fleets.

Handheld scanners priced below USD 8,000 are experiencing rapid adoption in home care settings, rural clinics, and even veterinary practices, especially following Butterfly Network's collaboration with Clipper in 2025. While these handheld devices forgo standalone displays by connecting to smartphones, they must adhere to Food and Drug Administration (FDA) mobile health guidelines, necessitating accuracy validation across diverse handset models. On the other hand, bench-top units, though still present in dialysis centers and long-term care wards due to their alignment with consistent patient flow, are experiencing stagnant sales.

By Technology: AI Imaging Disrupts Conventional Workflows

In 2025, conventional imaging commanded a dominant 66.88% market share, underscoring the significant presence of hospitals hesitant about artificial intelligence (AI) validation. Meanwhile, AI-driven imaging is projected to grow at a robust 6.89% CAGR. This surge is attributed to deep-learning models that can now deliver results in under 30 seconds and automatically populate Current Procedural Terminology (CPT) reporting fields. Notably, Butterfly’s Ultrasound-on-Chip integrates inference models directly on the probe, effectively sidestepping cloud latency and ensuring compliance with General Data Protection Regulation (GDPR) regulations in Europe.

Industry giants GE Healthcare and Siemens Healthineers are modernizing older imaging carts, either through software enhancements or by acquiring licenses for third-party algorithms. Furthermore, the Food and Drug Administration's (FDA) 2024 guidelines on machine learning emphasize the need for ongoing performance evaluations, a move that favors vendors with substantial clinical trial funding.

By End User: Ambulatory Surgical Centers Outpace Hospitals

Hospitals and clinics lead the charge, conducting up to 200 bladder scans daily across emergency, urology, and perioperative units. Meanwhile, Ambulatory Surgery Centers (ASCs), buoyed by a 15.4% Medicare payment surge in 2023, are not only registering the swiftest growth at a 6.47% CAGR but are also expanding the bladder scanner market. They're doing this by investing in portable scanners, ensuring same-day discharges. Knee arthroplasty volumes surged by 257% from 2020 to 2023, with each procedure necessitating residual checks before patient release.

Home-health agencies are gaining traction, due to Medicare's 2024 remote monitoring expansion, which now reimburses bladder volume tracking for heart-failure and spinal-injury patients. While diagnostic imaging chains and rehabilitation centers maintain a steady demand, long-term care facilities are turning to affordable handhelds to reduce Catheter-Associated Urinary Tract Infection (CAUTI) incidences among their elderly residents.

By Application: Urology and Emergency Medicine Lead Adoption

In 2025, urology accounted for 44.40% of the revenue, while obstetrics and gynecology are projected to grow at the fastest rate, with a CAGR of 7.44% through 2031. Urology continues to dominate, utilizing 3-D precision for residual measurements in cases like benign prostatic hyperplasia and spinal cord injuries. Emergency medicine sees the most significant growth, as bedside bladder scanning not only reduces evaluation time for acute retention but also ensures timely adherence to quality metrics. Obstetrics focuses on postpartum retention issues, whereas gynecology uses scanners to minimize catheter use after pelvic surgery.

Perioperative surgery integrates scanners into Enhanced Recovery After Surgery (ERAS) protocols, leading to lower reinsertion rates and shorter hospital stays, bolstering the bladder scanner market. Rehabilitation centers synchronize scanner applications with intermittent catheterization, highlighting a consistent, albeit specialized, demand.

Geography Analysis

North America generated 38.74% of global revenue in 2025, anchored by CMS payment models that reward CAUTI reduction and by widespread AI-enabled ultrasound familiarity among clinicians. Ongoing FDA quality-system updates slated for 2026 are expected to harmonize manufacturing benchmarks, reducing procurement risk for providers.

Asia-Pacific is forecast to post a 6.85% CAGR through 2031, underpinned by expanding healthcare investments and accelerating POCUS training programs. China and India spearhead volume demand as tertiary centers adopt 3D scanners for surgical wards, while Japan and South Korea emphasize AI algorithms that align with national digital-health strategies. Australia and Southeast-Asian markets favor portable units compatible with constrained clinical footprints.

Europe shows balanced growth amid CE-mark standardization and infection-prevention campaigns integrating bladder scanners into national quality frameworks. Germany, France, Italy, Spain, and the United Kingdom drive adoption based on public-insurance reimbursement, whereas Central and Eastern European countries adopt through donor-funded procurement. South America and Middle East & Africa remain nascent yet promising as infrastructure upgrades prioritize affordable, easy-to-train modalities in high-burden urological settings.

Competitive Landscape

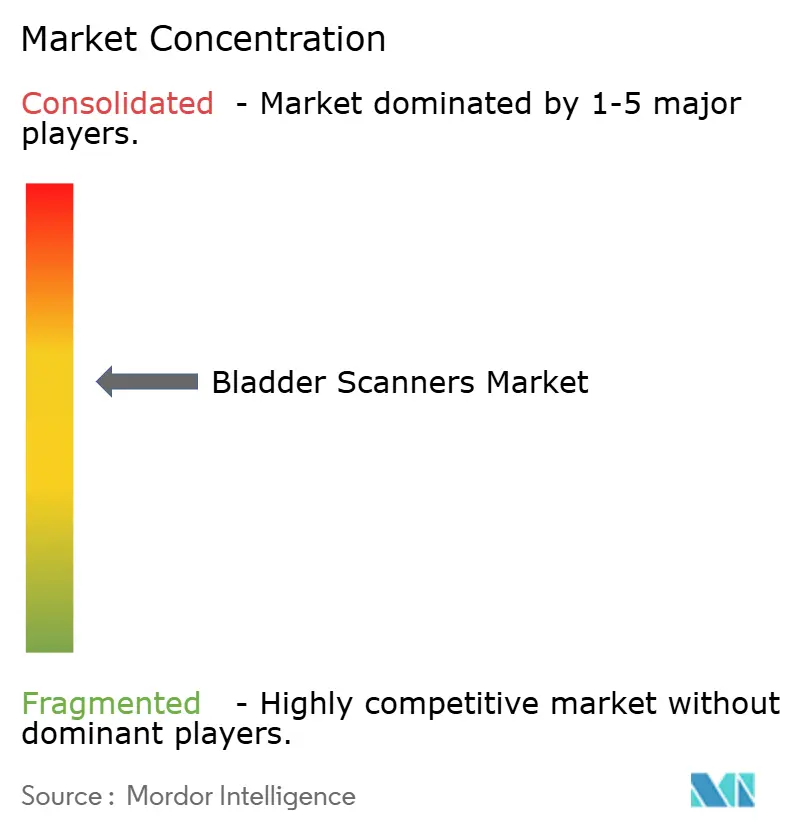

The Bladder Scanner Market displays moderate concentration. Verathon dominates with its BladderScan portfolio and proprietary ImageSense AI, which validates ±7.5% accuracy at clinically relevant volumes. Laborie Medical Technologies, Mindray Bio-Medical Electronics, and GE HealthCare pursue ecosystem strategies that embed bladder modules within broader ultrasound or patient-monitoring platforms.

New entrants leverage FDA 510(k) approvals to commercialize AI-native handheld devices, as seen with Clarius Mobile Health’s Bladder AI clearance in January 2024. Continuous-monitoring prototypes from Northwestern University hint at disruptive potential, while wearable-sensor startups collaborate with textile firms to test pressure-based alternatives in post-acute care.

Strategic moves center on acquisitions and product-line expansions. Boston Scientific’s USD 3.7 billion Axonics purchase expands its urology franchise into implantable solutions. Medtronic’s Hugo robotic surgery submission highlights convergence between surgical robotics and diagnostic imaging, potentially integrating bladder-volume checks into procedure workflows. As AI capabilities standardize, competition is likely to pivot toward connectivity, cybersecurity, and lifetime service offerings rather than solely imaging accuracy.

Bladder Scanners Industry Leaders

GE Healthcare Inc

Roper Technologies Inc. (Verathon Inc.)

Mcube Technology Co. Ltd

Vitacon

dBMEDx

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: FUJIFILM Sonosite introduced the UHF46-20 transducer, the first 46 MHz ultra-high-frequency POCUS probe for enhanced bladder imaging.

- May 2025: dBMEDx Inc has raised USD 250,000 in funding to advance its mission of transforming patient care. This funding will support enhancements to its flagship product, the BBS Revolution, a cutting-edge bladder scanner designed for efficient use by healthcare teams.

Global Bladder Scanners Market Report Scope

As per the scope of the report, a bladder scanner is a non-invasive ultrasound device or a tool that provides a virtual two or three-dimensional (3D) or (2D) image of the bladder and the volume of urine retained within the bladder for diagnosing, managing and treating urinary outflow dysfunction. The bladder scanner market is segmented by product, end-user, and geography. By product, the market is segmented into bench-top bladder scanners, portable bladder scanners, and handheld bladder scanners. By end user, the market is segmented into hospitals, diagnostic centers, and other end users. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major global regions. The report offers the value (in USD) for the above segments.

| 2-D Ultrasound Bladder Scanners |

| 3-D Ultrasound Bladder Scanners |

| Portable / Cart-Based Scanners |

| Handheld Scanners |

| Bench-top Scanners |

| Conventional Imaging |

| AI-Enabled Imaging |

| Hospitals & Clinics |

| Ambulatory Surgical Centers |

| Diagnostic Centers |

| Long-Term-Care Facilities / Nursing Homes |

| Home Healthcare |

| Urology |

| Emergency Medicine |

| Obstetrics & Gynecology |

| Surgery (Peri-operative) |

| Rehabilitation & Physiotherapy |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | 2-D Ultrasound Bladder Scanners | |

| 3-D Ultrasound Bladder Scanners | ||

| By Portability | Portable / Cart-Based Scanners | |

| Handheld Scanners | ||

| Bench-top Scanners | ||

| By Technology | Conventional Imaging | |

| AI-Enabled Imaging | ||

| By End User | Hospitals & Clinics | |

| Ambulatory Surgical Centers | ||

| Diagnostic Centers | ||

| Long-Term-Care Facilities / Nursing Homes | ||

| Home Healthcare | ||

| By Application | Urology | |

| Emergency Medicine | ||

| Obstetrics & Gynecology | ||

| Surgery (Peri-operative) | ||

| Rehabilitation & Physiotherapy | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2026 valuation of the Bladder Scanner Market?

The Bladder Scanner Market is valued at USD 179.6 million in 2026.

What is the 2026 valuation of the Bladder Scanner Market?

It is forecast to expand at a 6.02% CAGR, reaching USD 240.6 million by 2031.

Which product category leads in revenue share?

3D ultrasound scanners held 52.18% of global revenue in 2025.

Which region is growing the quickest?

Asia-Pacific is projected to grow at a 6.85% CAGR between 2026-2031.

Why are ASCs important to future demand?

Ambulatory Surgical Centers adopt scanners to comply with ERAS protocols, enabling non-invasive monitoring and supporting a 6.47% CAGR in this setting.

How does AI benefit bladder scanning?

AI automates bladder-boundary detection, delivering ±7.5% accuracy and reducing operator training time, which in turn improves reimbursement eligibility.

Page last updated on: