Barrier Material Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

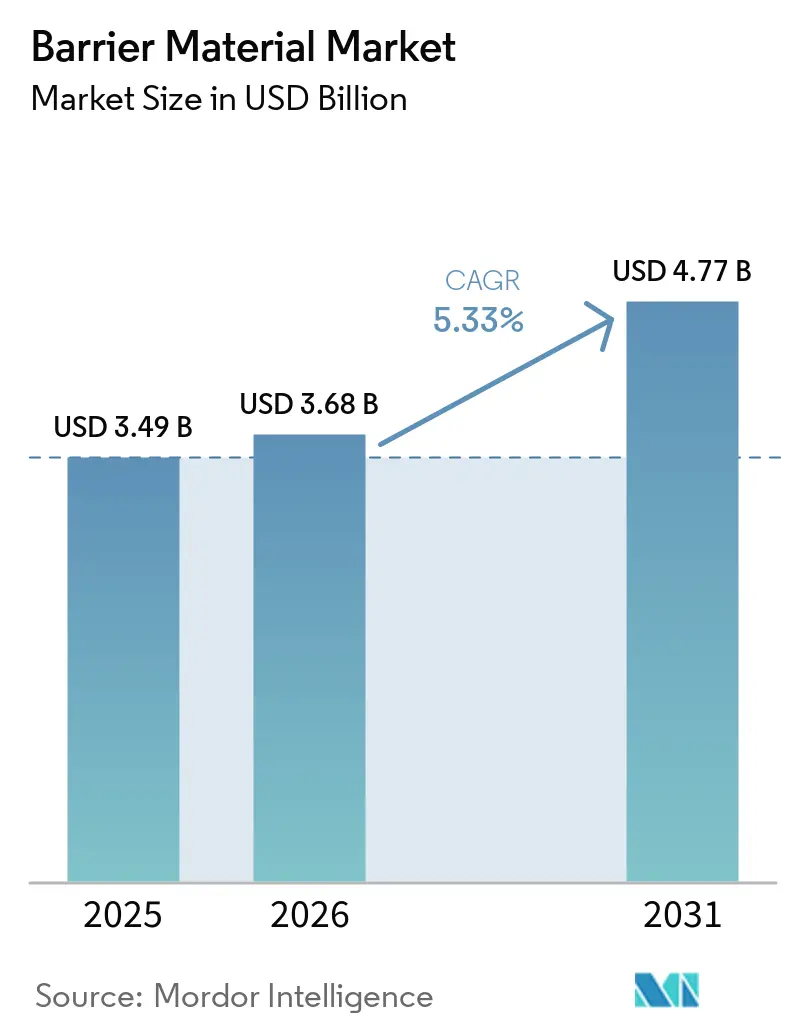

| Market Size (2026) | USD 3.68 Billion |

| Market Size (2031) | USD 4.77 Billion |

| Growth Rate (2026 - 2031) | 5.33% CAGR |

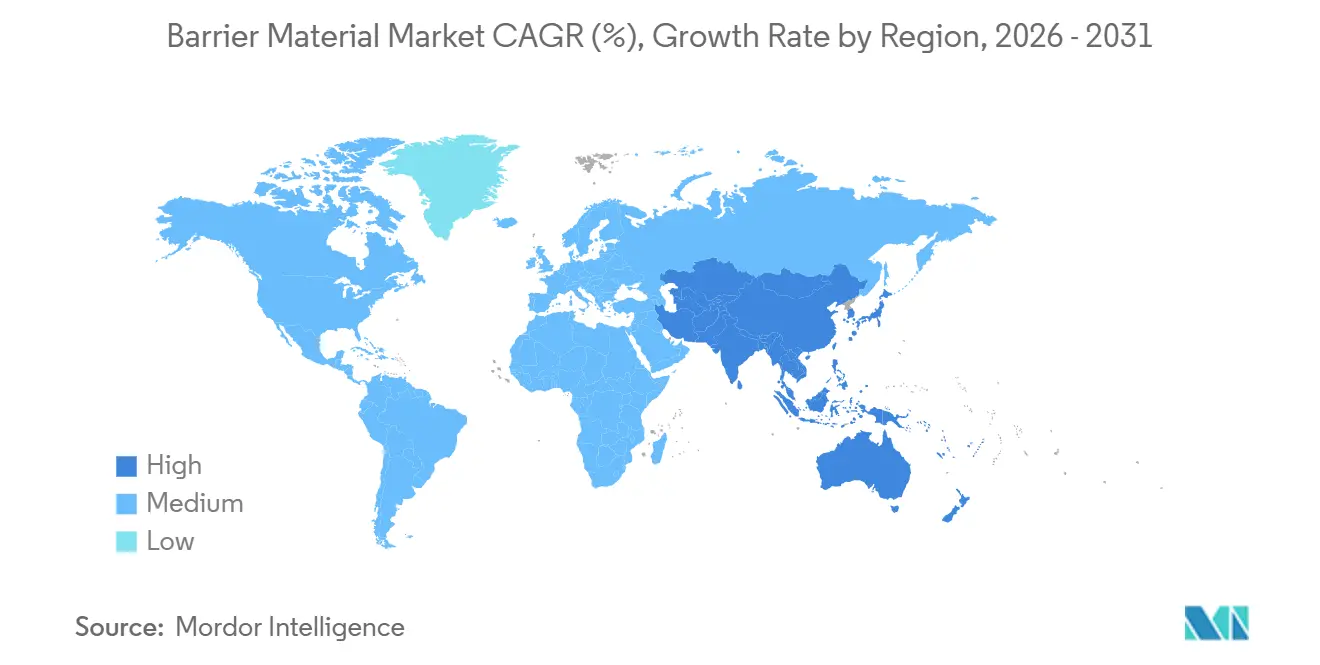

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Barrier Material Market Analysis by ���ϲ�����

The Barrier Material Market size was valued at USD 3.49 billion in 2025 and is estimated to grow from USD 3.68 billion in 2026 to reach USD 4.77 billion by 2031, at a CAGR of 5.33% during the forecast period (2026-2031). Pharmaceutical cold-chain expansion in Asia-Pacific, e-commerce growth that demands durable flexible formats, and regulatory moves away from per- and polyfluoroalkyl substances (PFAS) are accelerating the transition from aluminum and polyvinylidene chloride (PVDC) toward recyclable polyolefin coatings and ethylene vinyl alcohol (EVOH) structures. Polyvinylidene chloride retained 44.68% of 2025 revenue despite environmental scrutiny, but EVOH is gaining relevance as modified-atmosphere packaging widens shelf life without synthetic preservatives. R&D investment is intensifying around plasma-deposited silicon-oxide and aluminum-oxide coatings that promise metallized-film performance on mono-material polyethylene and polypropylene, while nanocellulose films edge toward semi-commercial scale in Scandinavia. Competitive activity is shifting upstream as resin suppliers such as Mitsubishi Chemical and Asahi Kasei integrate into film extrusion, and downstream as global converters offer machine-direction orientation and proprietary adhesive chemistries to trim weight without sacrificing stiffness.

Key Report Takeaways

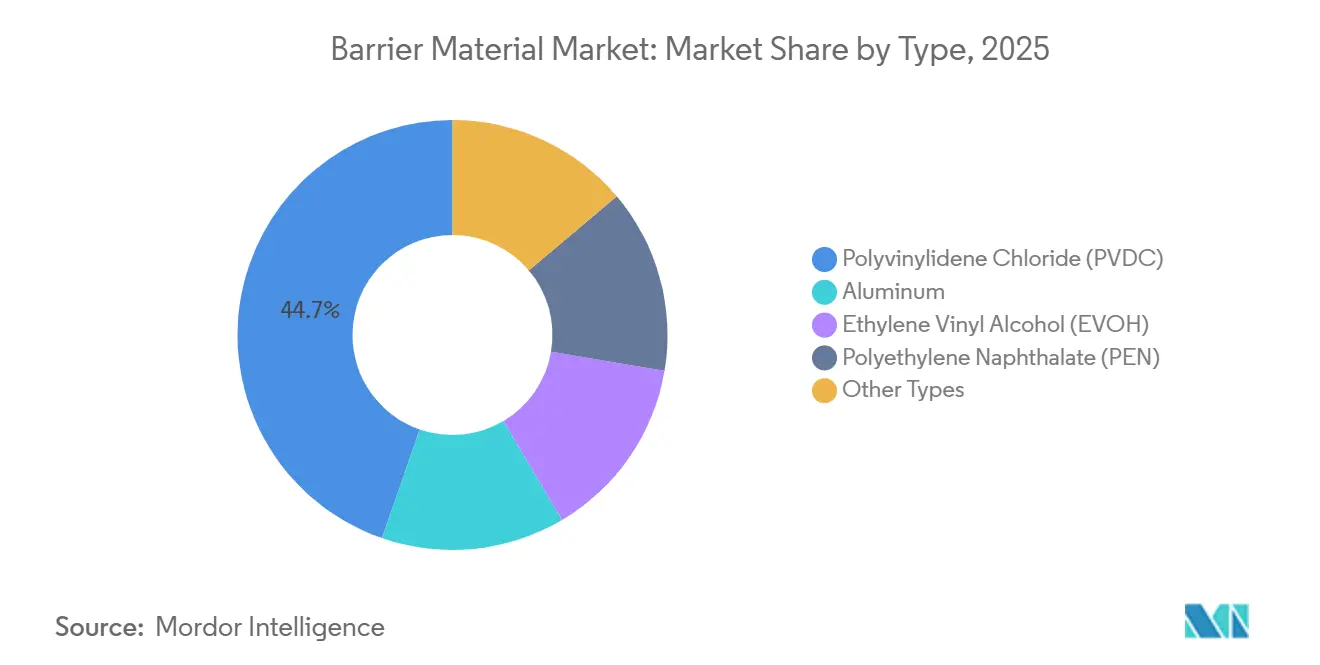

- By type, polyvinylidene chloride (PVDC) led with a 44.68% of the barrier material market share in 2025, while Ethylene Vinyl Alcohol (EVOH) is the fastest-growing type at a 5.73% CAGR through 2031.

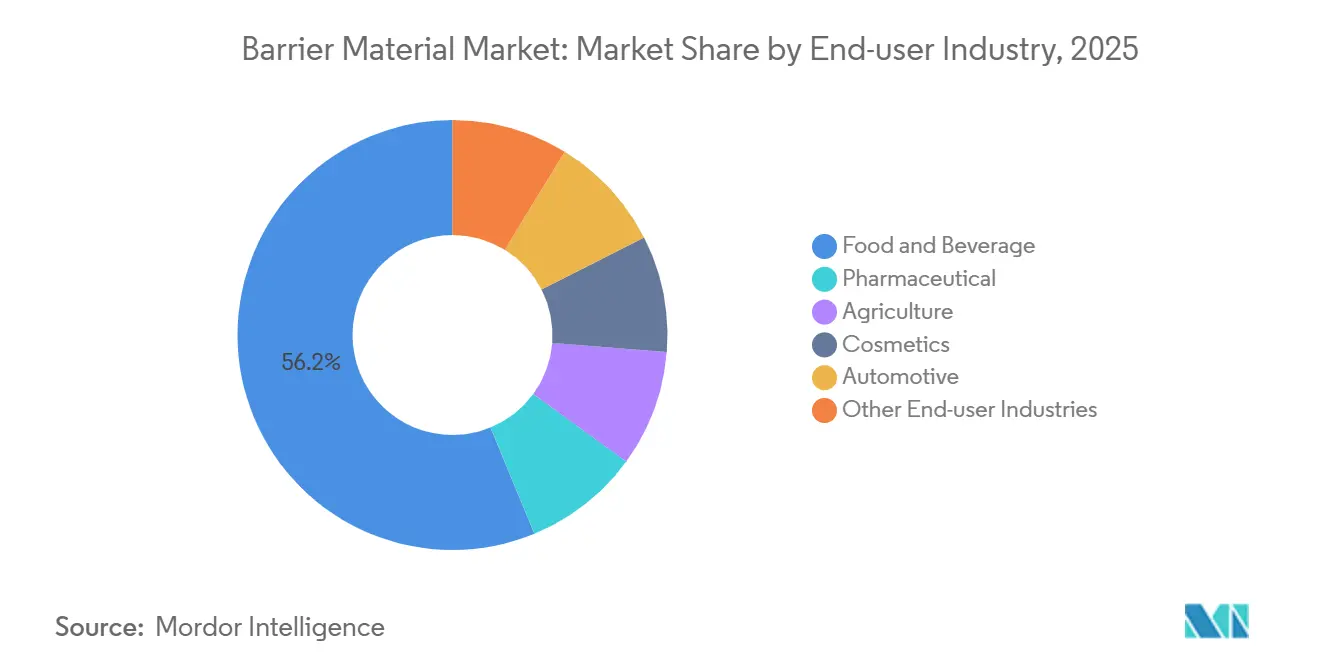

- By end-user industry, food and beverage captured 56.22% of the barrier material market share in 2025, while pharmaceutical is projected to expand at a 5.93% CAGR through 2031.

- By geography, Asia-Pacific captured 42.21% of of the barrier material market share in 2025 and it is advancing at a 5.75% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Barrier Material Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pharmaceutical blister demand in Asia-Pacific | +1.2% | Asia-Pacific core, spillover to Middle-East and Africa | Medium term (2-4 years) |

| E-commerce-driven multilayer flexible packaging | +0.9% | Global, with highest intensity in Asia-Pacific and North America | Short term (≤ 2 years) |

| Recyclable polyolefin barrier coatings | +0.7% | North America and Europe, early adoption in Australia | Medium term (2-4 years) |

| PFAS-free grease-barrier regulations | +0.6% | North America and Europe | Short term (≤ 2 years) |

| Nanocellulose barrier-film scale-up | +0.3% | Europe (Scandinavia), pilot projects in North America | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Pharmaceutical Blister Demand in Asia-Pacific

India and China are converting strip packs to aluminum-PVC and aluminum-aluminum blisters to protect moisture-sensitive active ingredients under stricter Good Manufacturing Practice rules, driving double-digit capital-expenditure growth on high-speed thermoforming lines. Cold-chain logistics for vaccines and insulin specify aluminum foil laminated with polyamide or polyester, a barrier threshold polymer films cannot meet without added metallization[1]Pharmaceuticals Export Promotion Council of India, “Annual Export Report 2025,” pharmexcil.com . China’s 2024 child-resistant mandate for opioid analgesics further boosts demand for push-through lidding, tightening PVDC resin supply and raising spot prices across Southeast Asia.

E-commerce-Driven Multilayer Flexible Packaging

Online grocery penetration above 12% of total food retail in Asia-Pacific has lifted demand for multilayer pouches that survive automated fulfillment, temperature swings, and last-mile handling. Oxygen-sensitive cheese and cured-meat snacks require transmission rates below 1 cc/m²/day, achievable only with EVOH cores flanked by a polyethylene sealant layer. U.S. audits attribute 9% of food-category e-commerce returns to burst pouches, steering converters toward thicker sealants and hot-tack adhesives that bond before the web cools, reducing damage claims despite adding 3–5 g per pack. Quick-commerce platforms in India and Indonesia now specify laser-scored stand-up pouches, but score lines disrupt material homogeneity and complicate recycling streams.

Recyclable Polyolefin Barrier Coatings

Mono-material polyethylene and polypropylene webs coated with silicon-oxide or aluminum-oxide via plasma deposition are replacing EVOH-polyethylene laminates in dry-snack packaging. Amcor’s AmPrima range aligns polymer chains through machine-direction orientation to lower oxygen permeability to 5 cc/m²/day without a separate barrier resin, granting access to polyethylene recycling streams that collect 35%–40% of flexible films in Germany and the Netherlands. Shelf-life, however, falls from 12 months in EVOH laminates to 9 months in coated polyolefin, limiting export potential.

PFAS-Free Grease-Barrier Regulations

The U.S. FDA’s 2024 voluntary phase-out of short-chain PFAS and California’s 2025 ban on PFAS food packaging are accelerating reformulation toward stearic-acid and chitosan coatings that deliver inconsistent grease resistance once condensation forms. Converters report coat-weight increases of 25%–40% and lower line speeds. European Union Packaging and Packaging Waste Regulation draft texts add to compliance urgency, yet Asian markets continue legacy PFAS coatings for domestic supply, creating a bifurcated global specification landscape.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Environmental limits on aluminum | -0.8% | Global, with highest impact in Europe and North America | Medium term (2-4 years) |

| Recycling challenges for multilayers | -0.6% | Global, acute in Asia-Pacific and South America | Short term (≤ 2 years) |

| Fluorochemical supply-chain disruptions | -0.4% | North America and Europe | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Environmental Limits on Aluminum

Primary aluminum smelting emits 16 tons CO₂ per ton of metal, prompting European pharma firms to pilot transparent high-barrier polyester and EVOH laminates that cut package carbon footprints by up to 50%. Recycled content in foil stock rose to 28% in 2025, yet post-consumer collection of thin-gauge foil remains below 15% due to contamination. Vacuum-deposited aluminum-oxide coatings on polyester achieve water-vapor transmission below 0.5 g/m²/day but require ≥5,000 tons/year to match foil economics, limiting early adoption.

Fluorochemical Supply-Chain Disruptions

The U.S. EPA’s 2024 listing of several PFAS as hazardous substances caused feedstock shortages for PVDF and PVF specialty barriers, delaying production at battery-film and cold-chain packaging lines[2]U.S. Environmental Protection Agency, “Designation of PFAS as Hazardous Substances 2024,” epa.gov . European producers scrambled for fluorine-free alternatives, but humidity-resistant grease barriers remain elusive, slowing fast-food packaging rollouts.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: EVOH Gains as Oxygen Sensitivity Rises

Ethylene Vinyl Alcohol (EVOH)is forecast to expand at a 5.73% CAGR from 2026 to 2031, the fastest among barrier resins, as processors seek modified-atmosphere solutions that extend shelf life for deli meats, pasta, and produce without preservatives. The barrier material market share of Polyvinylidene Chloride (PVDC) stood at 44.68% in 2025, but retail delisting in Europe is eroding that lead. Aluminum anchored in pharmaceutical blisters and aseptic cartons, where moisture ingress cannot be tolerated. Polyethylene naphthalate serves premium craft beer and oxygen-scavenging bottles but remains niche because resin prices exceed USD 4,000/tons.

Converters typically co-extrude EVOH between polyethylene or polypropylene tie layers that shield the hydrophilic core from moisture, preserving oxygen-barrier performance even at 80% relative humidity. Kuraray’s Eval portfolio spans ethylene contents from 27% to 48% mole percent, letting processors tune crystallinity for throughput or barrier needs. Pharmaceutical formulations are specifying EVOH base webs to replace PVC over plasticizer-migration concerns, but regulatory approval cycles still run 18–24 months.

By End-user Industry: Pharmaceutical Outpaces Food Growth

Food and beverage captured 56.22% of barrier material demand in 2025 and while pharmaceutical is projected to grow at a 5.93% CAGR through 2031. Blister packs demand moisture-vapor transmission below 0.05 g/m²/day, a threshold met by aluminum-based laminates but challenging for all-plastic formats without cost-prohibitive layers. In the Food and beverage industry, dairy, fresh meat, and snacks are collectively driving modified-atmosphere packaging that doubles shelf life versus polyethylene-only films. Silage films used in agriculture are designed to maintain anaerobic conditions. Oxygen transfer rates exceeding 500 cc/m²/day can result in mold formation and dry-matter losses. Automotive uptake for battery-pouch laminates is rising with electric-vehicle production, but current tonnage trails packaging demand by an order of magnitude.

Geography Analysis

Asia-Pacific accounted for 42.21% of barrier material market revenue in 2025 and is advancing at a 5.75% CAGR to 2031. China’s pharmaceutical packaging output grew 13% year-on-year in 2025 as blister lines absorbed new PVDC and aluminum capacity to serve Africa and Latin America. India’s flexible-packaging majors added EVOH co-extrusion lines to support multinational food brands; UFlex alone operates 12 barrier-film lines across three sites. Japan and South Korea pilot nanocellulose and bio-based barriers, but commercial volumes are minimal.

In North America, PFAS reformulation expenses, paired with inflation-sensitive consumers, slowed converter price pass-through. FDA guidance on PFAS phase-out forced coating-line retrofits, but grease-barrier performance still varies with humidity. Canada’s single-use plastics rules exempt essential food-safety formats, yet provincial extended-producer-responsibility fees are rising 8%–12% per year. Mexico’s near-shoring boom attracted USD 50 million-plus capacity announcements from Amcor and Sealed Air in 2024.

Europe’s share is shaped by recycled-content mandates pushing mono-material polyolefins. Germany’s dual system recycled 38% of flexible films in 2024, the continent’s top rate, although food contamination impedes closed-loop use. France’s AGEC law drives refillable pouches that require durable barriers across multiple cycles. South America and Middle-East and Africa combine for a lower share, with Brazil adopting blister formats for traceability compliance and Saudi Arabia investing USD 200 million in domestic flexible capacity under Vision 2030.

Competitive Landscape

The barrier material market is moderately fragmented. The top five manufacturers, Amcor, Kuraray, Mondi, Huhtamäki, and Syensqo, controlled roughly 35%–40% of global capacity in 2025. Amcor’s USD 8.4 billion acquisition of Berry Global’s consumer-packaging assets deepened EVOH and PVDC capabilities across 47 plants, with expected USD 650 million in synergies by 2027. Sealed Air differentiates with Cryovac shrink-bag systems that cut labor costs for meat processors while extending shelf life. Resin suppliers Kuraray, Mitsubishi Chemical, and Asahi Kasei are integrating downstream, leveraging captive EVOH and PVDC capacities to capture film-conversion margins and secure offtake for proprietary grades.

Patent filings for plasma-enhanced chemical-vapor deposition and atomic-layer deposition surged 18% in 2025, signaling a race to apply nanometer-thick silicon-oxide or aluminum-oxide coatings on polyethylene and polypropylene without compromising recyclability. Smaller converters compete through short-run digital printing and rapid prototyping for emerging brands that lack the volume for dedicated dies. Technology adoption is uneven: North American and European plants are investing in real-time barrier-property monitoring, whereas many Asian and Latin American lines still rely on offline testing, creating variability that premium-food and pharmaceutical clients increasingly reject.

White-space innovation in bio-based and compostable barriers is gaining policy support even though performance gaps remain. Partnerships such as Mondi-Stora Enso on paper-based pouches or Toppan-Toray on castor-oil-derived bio-polyamides illustrate incumbents’ hedging strategies against potential future bans on certain fossil-based materials.

Barrier Material Industry Leaders

Amcor plc

KURARAY CO., LTD.

Syensqo

Mondi

Huhtamäki Oyj

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Tetra Pak, in partnership with the Italian dairy company Sterilgarda Alimenti, introduced the first 1-litre package with a paper-based barrier. This development represented a notable step in the carton packaging industry's shift towards low-carbon, renewable materials by increasing the renewable content to 90% when combined with plant-based polymers.

- April 2026: UPM Specialty Materials and specialty paper producer Felix Schoeller introduced a recyclable barrier material designed for flexible food packaging applications, such as wrappers for chocolate and snack bars. The product is intended to assist packaging manufacturers in complying with recyclability requirements outlined in the EU Packaging and Packaging Waste Regulation (PPWR).

Global Barrier Material Market Report Scope

Barrier materials are substances engineered to limit or prevent the transfer of specific elements, such as moisture, gases (e.g., oxygen, carbon dioxide), light, or chemicals, between two environments. These materials play a critical role in industries such as food and pharmaceutical packaging, construction, and electronics, ensuring product integrity and safety.

The barrier material market is segmented by type, end-user industry, and geography. By type, the market is segmented into polyvinylidene chloride (PVDC), aluminum, ethylene vinyl alcohol (EVOH), polyethylene naphthalate (PEN), and other types. By end-user industry, the market is segmented into food and beverage, pharmaceutical, agriculture, cosmetics, automotive, and other end-user industries. The report also covers the market size and forecasts for barrier material in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Polyvinylidene Chloride (PVDC) |

| Aluminum |

| Ethylene Vinyl Alcohol (EVOH) |

| Polyethylene Naphthalate (PEN) |

| Other Types |

| Food and Beverage |

| Pharmaceutical |

| Agriculture |

| Cosmetics |

| Automotive |

| Other End-user Industries |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Polyvinylidene Chloride (PVDC) | |

| Aluminum | ||

| Ethylene Vinyl Alcohol (EVOH) | ||

| Polyethylene Naphthalate (PEN) | ||

| Other Types | ||

| By End-user Industry | Food and Beverage | |

| Pharmaceutical | ||

| Agriculture | ||

| Cosmetics | ||

| Automotive | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the barrier material market?

The barrier material market stands at USD 3.68 billion in 2026 and is projected to reach USD 4.77 billion by 2031.

Which region adds the most demand in 2025?

Asia-Pacific contributes the largest demand of 42.21% in 2025, supported by pharmaceutical outsourcing, e-commerce grocery growth, and new barrier-film capacity.

Why are converters investing in mono-material polyolefins?

Plasma-deposited silicon-oxide coatings on polyethylene and polypropylene create recyclable high-barrier films that meet emerging design-for-recycling mandates.

How are PFAS regulations influencing material choices?

North American and European bans are pushing suppliers toward fluorine-free grease-barrier chemistries, though coat weights rise and humidity performance varies.

Page last updated on: