Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

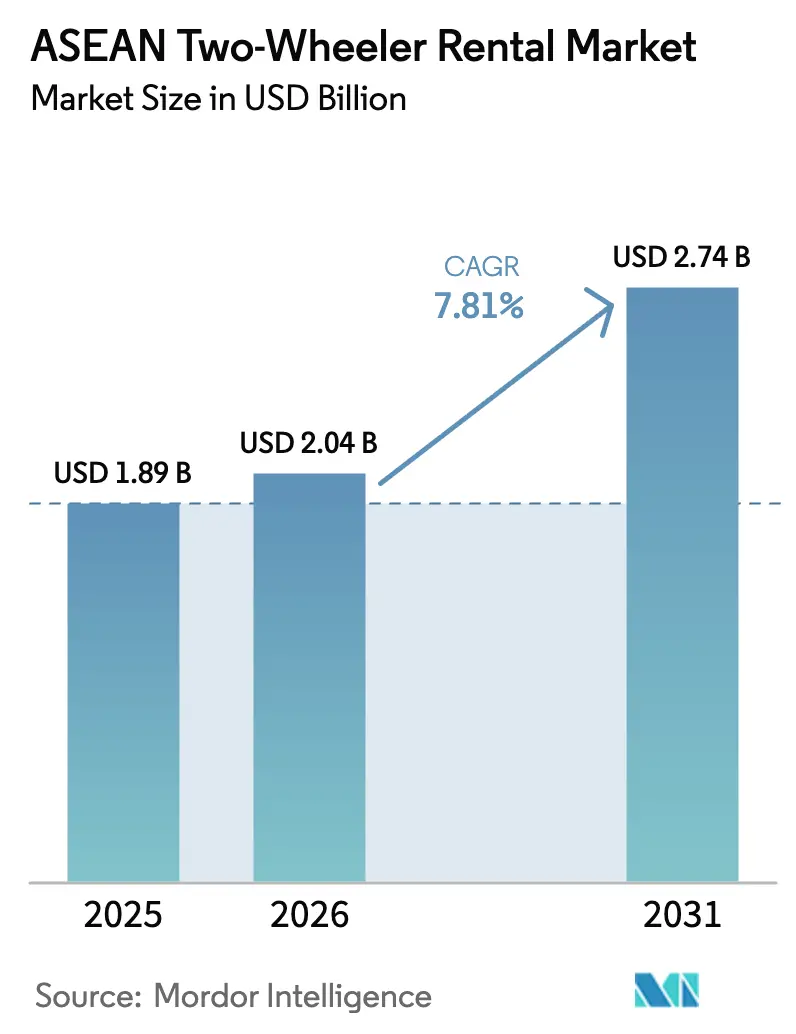

| Base Year Market Size (2025) | USD 1.89 Billion |

| Market Size (2026) | USD 2.04 Billion |

| Market Size (2031) | USD 2.74 Billion |

| Growth Rate (2026 - 2031) | 7.81% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. |

|

ASEAN Two-Wheeler Rental Market Analysis by ���ϲ�����

The ASEAN Two-Wheeler Rental Market size was valued at USD 1.89 billion in 2025 and is estimated to grow from USD 2.04 billion in 2026 to reach USD 2.74 billion by 2031, at a CAGR of 7.81% during the forecast period (2026-2031). A rapid shift from ownership to access-based mobility is underway as super-apps embed rental buttons beside ride-hailing, while city-level bans on internal-combustion motorcycles accelerate electrification. Tourism arrivals across Southeast Asia have already exceeded pre-pandemic levels, reviving short-term rental demand in Bali, Phuket, and Boracay. At the same time, chronic traffic congestion in Jakarta, Bangkok, and Metro Manila pushes commuters toward cost-efficient scooters that slip through gridlock faster than cars. Battery-swap networks now allow drivers to exchange depleted packs in under a minute, cutting downtime and lifting daily trip counts by 30-40%. Consolidation is accelerating: Grab, GoTo, and Xanh SM all use embedded microlending to lock in riders, while OEMs such as VinFast and Gogoro enter the rental arena and underprice smaller shops by leveraging manufacturing scale.

Key Report Takeaways

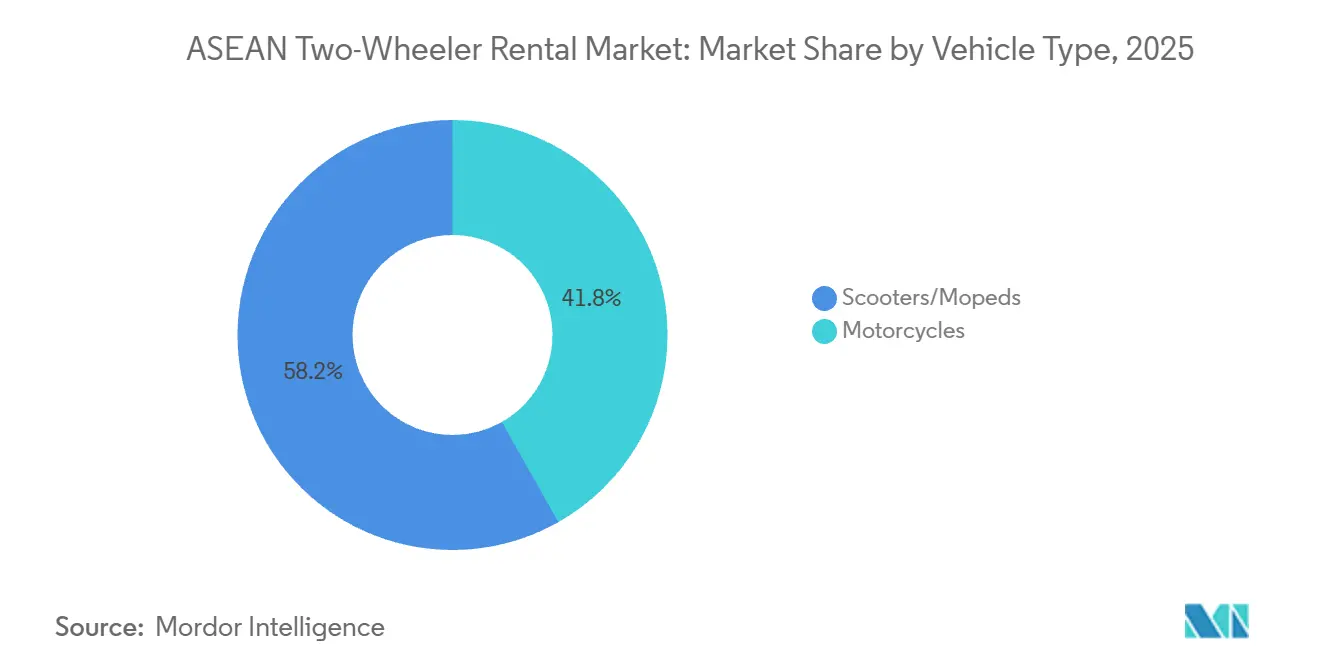

- By vehicle type, scooters and mopeds led with 58.16% of the ASEAN two-wheeler rental market share in 2025.

- By rental duration, short-term options accounted for 64.08% of the ASEAN two-wheeler rental market in 2025, whereas monthly subscriptions are advancing at a 11.03% CAGR through 2031.

- By application, tourism accounted for 61.37% of the ASEAN two-wheeler rental market in 2025; commuting is expanding at a 12.48% CAGR through 2031.

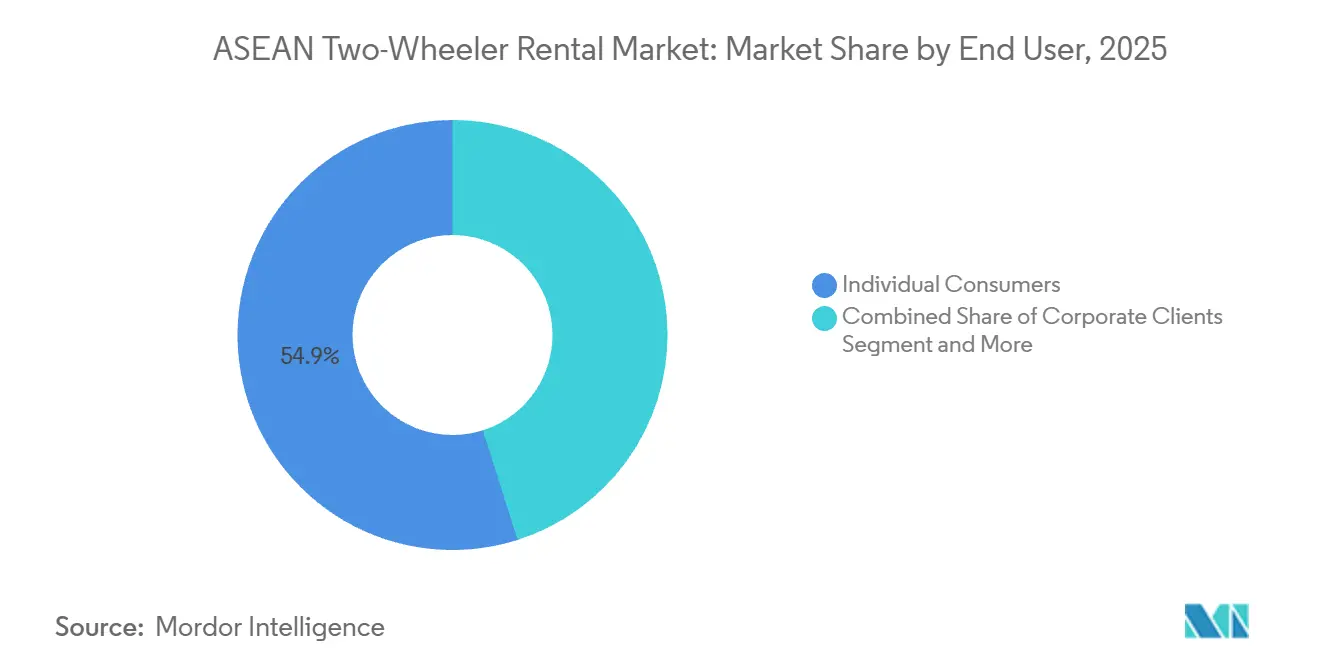

- By end user, individual consumers accounted for 54.87% of 2025 revenue, while fleet operators are growing at 11.55% each year.

- By geography, Indonesia dominated the ASEAN two-wheeler rental market with 34.11% market share in 2025, yet Vietnam is growing fastest at a 13.47% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

ASEAN Two-Wheeler Rental Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tourism-Led Demand Rebound Post-COVID | +2.1% | Bali, Phuket, Boracay, Da Nang | Short Term (≤ 2 Years) |

| Urban Congestion Drives Cost-Effective Commuting | +1.8% | Jakarta, Bangkok, Metro Manila, Ho Chi Minh City | Medium Term (2–4 Years) |

| Super-Apps Integrate Two-Wheeler Rentals | +1.6% | Indonesia, Vietnam, Thailand, Philippines, Malaysia | Medium Term (2–4 Years) |

| Battery-Swap Ecosystems Slash EV Downtime | +1.3% | Indonesia, Vietnam, Singapore | Long Term (≥ 4 Years) |

| City-Level ICE Bans Pivot Fleets to E-Scooters | +1.0% | Hanoi, Ho Chi Minh City, Jakarta, Bangkok | Long Term (≥ 4 Years) |

| Embedded Microlending Unlocks Tier-2 Driver Pool | +0.9% | Indonesia, Philippines, Vietnam, Thailand | Medium Term (2–4 Years) |

| Source: ���ϲ����� | |||

Tourism-Led Demand Rebound Post-COVID

International arrivals surpassed 2019 levels in 2025, reigniting scooter demand in beach and island destinations. Bali’s motorcycle rentals recovered to pre-pandemic volumes at daily rates of 50,000–150,000 IDR (USD 3.10–9.30), while Phuket operators charge 400–1,800 THB (USD 11–50) per day. Vietnam welcomed 17.5 million visitors in 2024[1]"Vietnam welcomed over 1.7 million international visitors in December 2024" The Vietnam National Tourism Administration, vietnam.vn., spurring fleet expansions of 25-30% in Da Nang and Nha Trang. Operators add electric scooters to appeal to eco-minded travelers, as seen in Grab Thailand’s 2024 EV rollout across five cities. Average rental length is stretching from three to six days, boosting revenue per unit and stabilizing offseason cash flow.

Urban Congestion Drives Cost-Effective Commuting

Bangkok commuters lose 61 hours annually in traffic, Manila’s gridlock costs USD 3.5 billion each year, and Jakarta’s average commute exceeds 90 minutes. Ride-hailing motorcycle trips in Indonesia jumped 13% to 9 billion in 2024, with many gig workers shifting to rental plans to avoid upfront purchases. Ho Chi Minh City’s 7 million-plus motorcycles underscore how dense fleets still beat cars in point-to-point speed. Corporate subsidies for delivery riders shrink monthly rental costs by 15-20%, making subscriptions attractive. Xanh SM’s revenue-share model lets drivers keep 80% of fares, pushing their monthly income target above USD 700. These economics cement the ASEAN two-wheeler rental market as a critical pillar of last-mile logistics.

Super-Apps Integrate Two-Wheeler Rentals

Grab and GoTo account for a significant share of Indonesia’s ride-hailing market value, enabling them to cross-sell rentals, insurance, and maintenance within a single wallet. GrabElectric already deploys 8,500[2]Putra Adhiguna, "Electrifying Indonesia’s Road Transport," Institute for Energy Economics and Financial Analysis, ieefa.org. electric bikes in Indonesia, targets 14,000 by 2026, and partners with Pertamina for battery swaps. GoTo’s GoRide Transit links rentals with bus and rail routes, easing suburban commutes. Vietnam’s Be Group reached EBITDA breakeven after three profitable quarters by bundling rentals with payments and delivery. Such embedded ecosystems squeeze margins for standalone rental shops that lack payment rails or data scale.

Battery-Swap Ecosystems Slash EV Downtime

Swap Energi runs 1,000+ swap kiosks and controls approximately 70%[3]"Top 10 Battery Swapping Companies in Indonesia 2025," TYCORUN, batteryswapcabinet.com. of Indonesia’s battery-swap footprint, cutting recharge waits to 60 seconds. Grab Vietnam and Charge+ installed 200 stations, enabling drivers to complete 12-15 rides daily, versus 8-10 with plug-in charging. Gogoro’s Singapore launch charges fleets SGD 70 per month for unlimited swaps, an uptime-as-a-service proposition. The Asian Development Bank projects 2 million Indonesian electric motorcycles by 2030—if swaps scale to 5,000 sites for USD 500 million. Early movers may reap network effects but risk stranded assets if battery standards diverge.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Accident and Insurance Premiums | −1.2% | Indonesia, Vietnam, Thailand, Philippines | Short Term (≤ 2 Years) |

| Regulatory Patchwork Across ASEAN | −0.9% | Philippines, Indonesia, Myanmar | Medium Term (2–4 Years) |

| Non-Standard Batteries Inflate Spare-Part Costs | −0.7% | Indonesia, Vietnam, Thailand | Long Term (≥ 4 Years) |

| Monsoon-Season Utilization Dips | −0.5% | Thailand, Vietnam, Philippines, Myanmar | Short Term (≤ 2 Years) |

| Source: ���ϲ����� | |||

High Accident and Insurance Premiums

Motorcycles cause 43% of ASEAN road deaths, with Indonesia logging 26,000 fatalities in 2024 and Vietnam 10,500, forcing insurers to raise premiums 15-20% on risky corridors. Thailand saw 15,000 motorcycle deaths in 2024, leading insurers to add 5-10 THB per-trip surcharges that cut rental margins by up to 12%. Helmet use below 50% in rural Philippines magnifies claims, says the Asian Development Bank. Operators deploy telematics from DRVR to monitor behavior, cutting theft by 20% and fuel by 26% but also letting underwriters price risk driver-by-driver. This granular pricing can exclude high-risk, low-income riders, undercutting the inclusivity promise of embedded finance.

Regulatory Patchwork Across ASEAN

The Philippines still runs a pilot program with 8,000 accredited riders and no permanent motorcycle-taxi law, chilling long-term investment. Indonesia’s draft rental decree remains unpublished, so provinces levy fees ranging from USD 50 to USD 500 per bike per year. Myanmar lacks any formal rules, pushing activity into informal peer-to-peer channels. Differing safety codes—SNI in Indonesia, QCVN in Vietnam, TIS in Thailand—force OEMs to run separate production lines, inflating unit costs 10-15%. Until harmonization advances, the ASEAN two-wheeler rental market will remain a patchwork of localized compliance burdens.

Segment Analysis

By Vehicle Type: Electric Scooters Surge Ahead

Scooters and mopeds accounted for 58.16% of revenue in 2025, yet electric models will post 14.92% annual growth, nearly double the ASEAN two-wheeler rental market CAGR. Internal-combustion bikes still cost less up front, but battery-swap savings and looming urban bans are pushing operators to electrify fleets quickly. Motorcycles above 150 cc remain popular for hillier tourist zones, though their 41.84% share is slipping. Grab added 8,500 electric units in Indonesia, targeting 14,000 by 2026, while VinFast plans Indonesian showrooms by mid-2026. OEM-backed platforms undercut stand-alone shops, tightening margins across the ASEAN two-wheeler rental industry.

Electric scooters commanded 62% of the ASEAN two-wheeler rental market size for scooters in 2025 and are forecast to reach 75% by 2031. Their maintenance costs are 25% below those of petrol peers, and battery-swap uptime boosts daily revenue per vehicle by roughly 35%. Operators without capital for fleet replacement risk losing share once city-level ICE bans bite, making financing partnerships critical.

By Rental Duration: Subscriptions Build Stickier Cash Flows

Short-term products, mostly daily rentals to tourists, contributed 64.08% of revenue in 2025. However, long-term subscriptions are expanding at 11.03%, as gig riders prefer predictable weekly or monthly fees that include maintenance, swaps, and insurance. Charged Asia leases e-scooters in Jakarta at 1.2 million IDR (USD 71) per month, with 90% of its 1,500-unit fleet on subscription.

The ASEAN two-wheeler rental market size for subscriptions is projected to climb from USD 0.69 billion in 2026 to USD 1.15 billion by 2031, reflecting a 10.8% CAGR. The lifetime value per bike is 30-40% higher than for ad-hoc hires because utilization gaps shrink and debt service aligns with cash receipts. Platforms with integrated wallets automatically collect dues, slashing default risk.

By Application: Commuting Narrows the Gap

Tourism still accounted for 61.37% of revenue in 2025, but commuting grew at 12.48% annually and could match tourism by 2029. Leisure renters accept higher per-day charges, yet monsoon swings and seasonality create idle months.

Commuting accounts for 38.63% of the ASEAN two-wheeler rental market share in 2025 and is projected to claim 45% by 2031. Gig riders complete 12-15 deliveries daily, allowing operators to amortize vehicles in 2 years, compared with 3+ years for tourism fleets. The swap infrastructure further benefits commuters who require minimal downtime.

By End User: Fleet Operators Scale Faster

Individual consumers represented 54.87% of revenue in 2025, but corporate and platform fleets are growing 11.55% each year by signing multi-year leases. Blueshark offers Malaysian SMEs packages at RM 487 (USD 108) per month, bundling telematics and maintenance.

Fleet deals accounted for 30% of the ASEAN two-wheeler rental market size in 2026 and should top 40% by 2031. Deep contracts give operators bankable cash flows, supporting cheaper debt and bulk vehicle discounts.

By Distribution Mode: Online Platforms Take Control

Online channels accounted for 72.62% of revenue in 2025 and will grow at a 16.38% CAGR as mobile-first users increasingly expect app-based booking, GPS tracking, and instant payments. Offline agencies remain relevant on islands where walk-ins dominate but face shrinking volumes.

The ASEAN two-wheeler rental market size for online platforms is likely to hit USD 2.1 billion by 2031. Super-apps leverage cross-selling, cashback, and loyalty points to lock riders in, whereas traditional shops must pivot to niche premium bikes or guided tours to survive.

Geography Analysis

Indonesia generated 34.11% of 2025 revenue, supported by 6.3 million new two-wheeler sales and over 1,000 swap stations that give Grab and GoTo scale advantages. Provincial fees vary widely, adding compliance complexity, yet demand remains robust as Jakarta’s commute exceeds 90 minutes. Swap Energi’s network effect positions it as a de facto standard in swaps, though competing Chinese battery formats threaten to fragment the market.

Vietnam is the fastest riser at 13.47% CAGR. Xanh SM overtook Grab with a 44.68% ride-hailing share in Q2 2025 by granting drivers 80% of fares. City plans to ban ICE bikes by 2030, plus VPBank loans for 100,000 e-motorcycles, to unlock a huge tier-2 driver pool. Be Group reached profitability with 500,000 drivers, showing that the ASEAN two-wheeler rental market can deliver sustainable margins when fleet electrification aligns with swap rollouts.

Thailand, the Philippines, Malaysia, and Singapore jointly account for around 37% of revenue. Bangkok congestion, subsidies worth 18,000 THB for EVs, and Grab’s EV fleets sustain Thai growth. Philippine operators await permanent legislation beyond the 8,000-rider pilot, but JoyRide’s 20,000-strong force and Angkas’ 26,000 lobbied hard in 2025. Malaysia hosts 16.7 million motorcycles, yet only 0.23% are electric, although iMotorbike’s USD 10 million round suggests appetite for subscription models. Singapore’s certificate-of-entitlement costs above SGD 10,000 (USD 7,400) deter ownership, so Gogoro’s SGD 70-per-month swap subscription targets fleets that need guaranteed uptime.

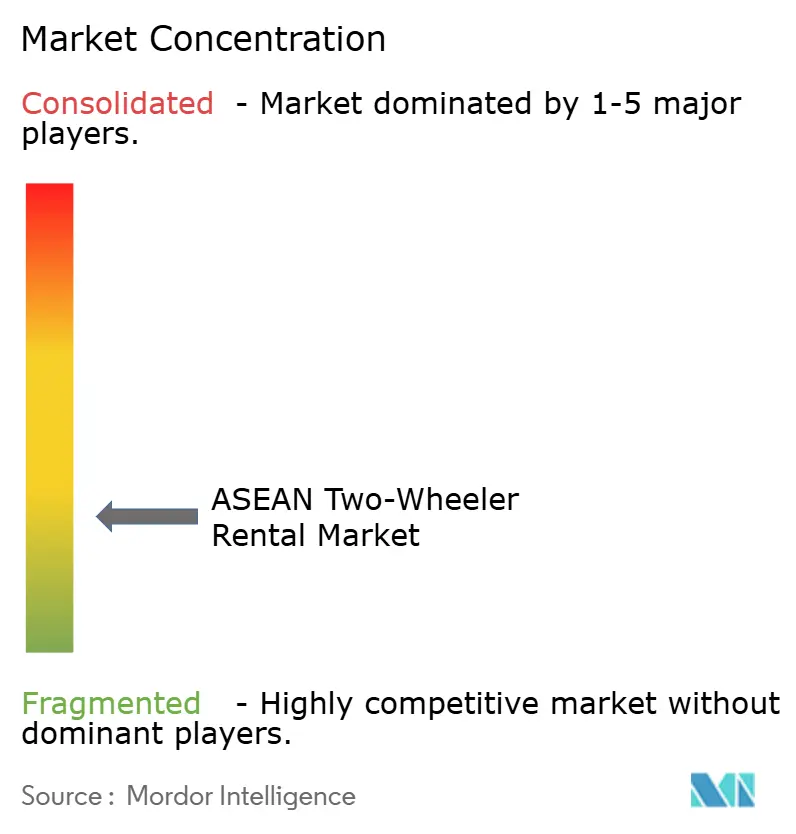

Competitive Landscape

Competitive intensity in the ASEAN two-wheeler rental market remains moderate but is steadily shifting toward consolidation as large platforms seek scale advantages. A potential USD 7 billion merger between Grab and GoTo would create a dominant regional mobility player with significant control over Indonesian transactions and a meaningful presence across Southeast Asia. In Vietnam, Xanh SM rapidly expanded using vertically integrated electric motorcycles, capturing substantial urban share and reshaping competitive dynamics. At the same time, Be Group has reached improved profitability milestones, demonstrating that operational scale and subscription-based revenues can offset the gradual tapering of ride subsidies.

Strategic differentiation increasingly hinges on ecosystem partnerships and infrastructure alliances. Collaborations such as Grab's partnership with Pertamina and Charge+'s partnership with Gogoro strengthen charging and battery-swapping reliability while raising barriers to entry through network lock-in. Fleet-optimization platforms such as DRVR deliver measurable efficiency gains, including fuel savings and reduced theft exposure, enhancing asset utilization economics. These technology integrations improve uptime and provide tangible cost advantages for large-scale operators.

OEM participation is intensifying competitive pressure within the rental landscape. VinFast and KYMCO-backed Sleek EV are entering rental and fleet segments directly, leveraging manufacturing scale and financing arms to undercut independent operators when necessary. Such vertically integrated strategies allow vehicle cross-subsidization and faster fleet refresh cycles. While opportunities remain in corporate leasing, subscription mobility, and cross-border fleet redeployment, these segments require significant capital commitment and regulatory sophistication. As capacity expands, pricing discipline and ecosystem control will likely define the next phase of competition.

ASEAN Two-Wheeler Rental Industry Leaders

-

Grab Holdings Ltd.

-

GoTo Group (Gojek)

-

Angkas Holdings Inc.

-

JoyRide Logistics & Transport Inc.

-

Be Group JSC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: VinFast officially announced its entry into Indonesia’s electric scooter market, signing strategic MoUs with multiple local dealers to deploy its e-scooter portfolio, including models with battery-swapping capability. The rollout in the Jabodetabek metropolitan area is expected to expand across the country throughout 2026, supported by integrated retail, financing, and charging infrastructure partners.

- January 2026: Vietnam’s e-scooter segment recorded dramatic growth in 2025, with domestic sales rising nearly sixfold as gasoline bike demand eroded under tightening emissions rules and electrification incentives.

ASEAN Two-Wheeler Rental Market Report Scope

The ASEAN two-wheeler Rental Market report covers the current and upcoming trends with recent technological development. The report will provide a detailed analysis of various areas of the market by vehicle, rental duration and application. The market share of significant two-Wheeler Rental companies across ASEAN nations will be provided.

By Vehicle Type

| Motorcycles |

| Scooters/Mopeds |

By Rental Duration

| Short-Term |

| Long-Term |

By Application

| Tourism |

| Daily Commuting |

By End User

| Individual Consumers |

| Corporate Clients |

| Fleet Operators |

By Distribution Mode

| Online Platforms |

| Offline Rental Agencies |

By Geography

| Indonesia |

| Malaysia |

| Singapore |

| Philippines |

| Thailand |

| Vietnam |

| Myanmar |

| Rest of ASEAN |

| By Vehicle Type | Motorcycles |

| Scooters/Mopeds | |

| By Rental Duration | Short-Term |

| Long-Term | |

| By Application | Tourism |

| Daily Commuting | |

| By End User | Individual Consumers |

| Corporate Clients | |

| Fleet Operators | |

| By Distribution Mode | Online Platforms |

| Offline Rental Agencies | |

| By Geography | Indonesia |

| Malaysia | |

| Singapore | |

| Philippines | |

| Thailand | |

| Vietnam | |

| Myanmar | |

| Rest of ASEAN |

Key Questions Answered in the Report

How big will the ASEAN two-wheeler rental market be by 2031?

It is forecast to reach USD 2.74 billion by 2031, expanding at 7.81% CAGR from 2026.

Which country is growing fastest in rental demand?

Vietnam leads with a projected 13.47% CAGR to 2031, driven by electrification mandates and super-app competition.

What vehicle type dominates fleet composition?

Scooters and mopeds held 58.16% revenue in 2025, and electric variants are accelerating at 14.92% yearly.

Why are battery-swap stations important?

Swap kiosks cut recharge waits to about one minute, allowing drivers 30-40% more trips per day and boosting operator returns.

Are monthly subscriptions overtaking daily rentals?

Subscriptions grow at 11.03% per year, outpacing daily hires as gig workers favor predictable costs and bundled maintenance.

Page last updated on: