Artificial Intelligence As A Service Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

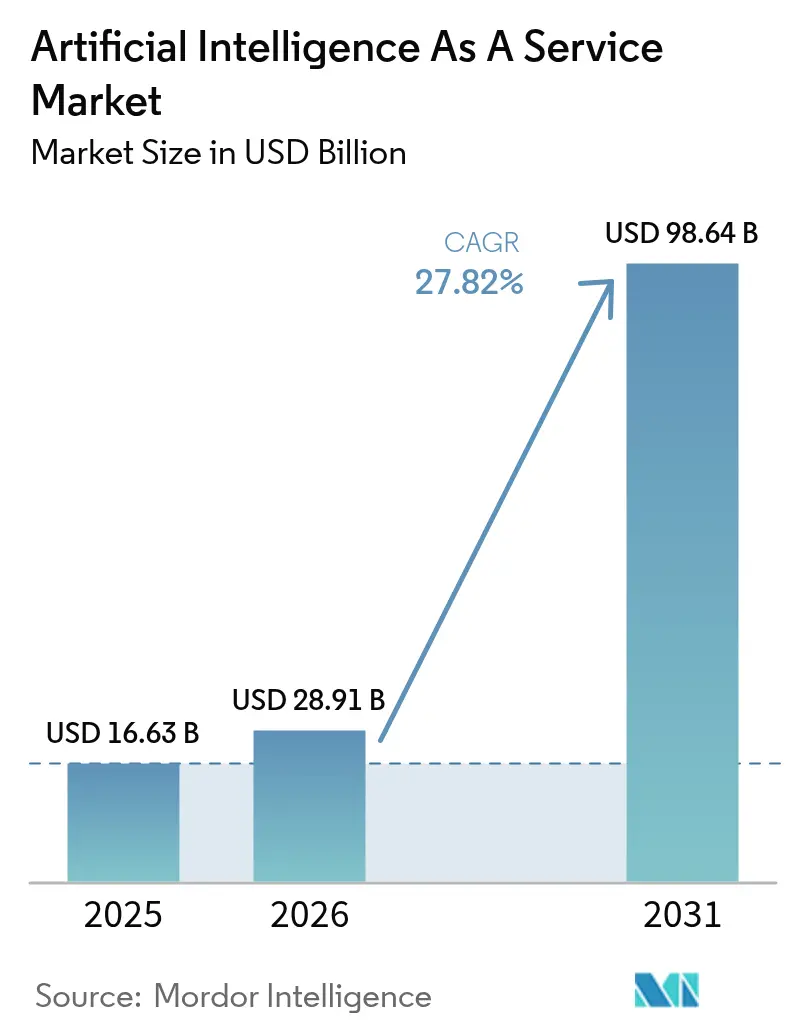

| Market Size (2026) | USD 28.91 Billion |

| Market Size (2031) | USD 98.64 Billion |

| Growth Rate (2026 - 2031) | 27.82% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Artificial Intelligence As A Service Market Analysis by ���ϲ�����

The Artificial Intelligence as a Service market size is projected to expand from USD 20.63 billion in 2025 and USD 28.91 billion in 2026 to USD 98.64 billion by 2031, registering a 27.82% CAGR between 2026 and 2031. Rapid enterprise migration from on-premise model training toward pay-per-use cloud inference is redefining procurement economics as upfront capital outlays fall and refresh cycles accelerate. Public cloud offerings remained the preferred entry point in 2025 because startups valued speed over governance, yet hybrid configurations are rising as regulated institutions balance data-sovereignty laws against the elasticity of hyperscale compute. Custom accelerators, notably AWS Trainium3, are pushing unit costs for large-language-model inference well below prior GPU benchmarks, opening production budgets for real-time transcription, vision analytics, and digital-twin simulations. Market momentum is further reinforced by low-code platforms embedding generative-AI APIs that slash application-development timelines, while government-backed sovereign-cloud programs in Asia and the Middle East expand regional capacity for workloads that Western providers cannot legally host.

Key Report Takeaways

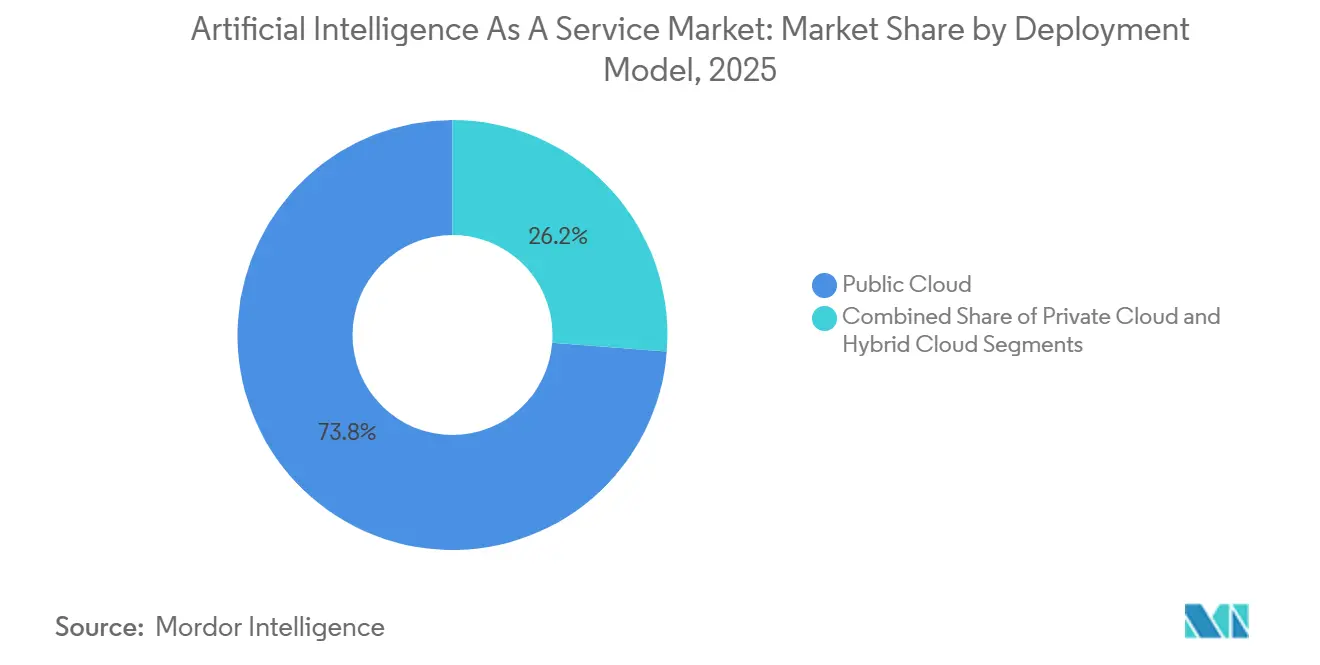

- By deployment model, public cloud led with 73.78% revenue share in 2025; hybrid cloud is forecast to expand at a 29.11% CAGR through 2031.

- By service type, machine-learning platform services held 40.37% of the Artificial Intelligence as a Service market share in 2025, while AI infrastructure services are projected to grow at 28.52% through 2031.

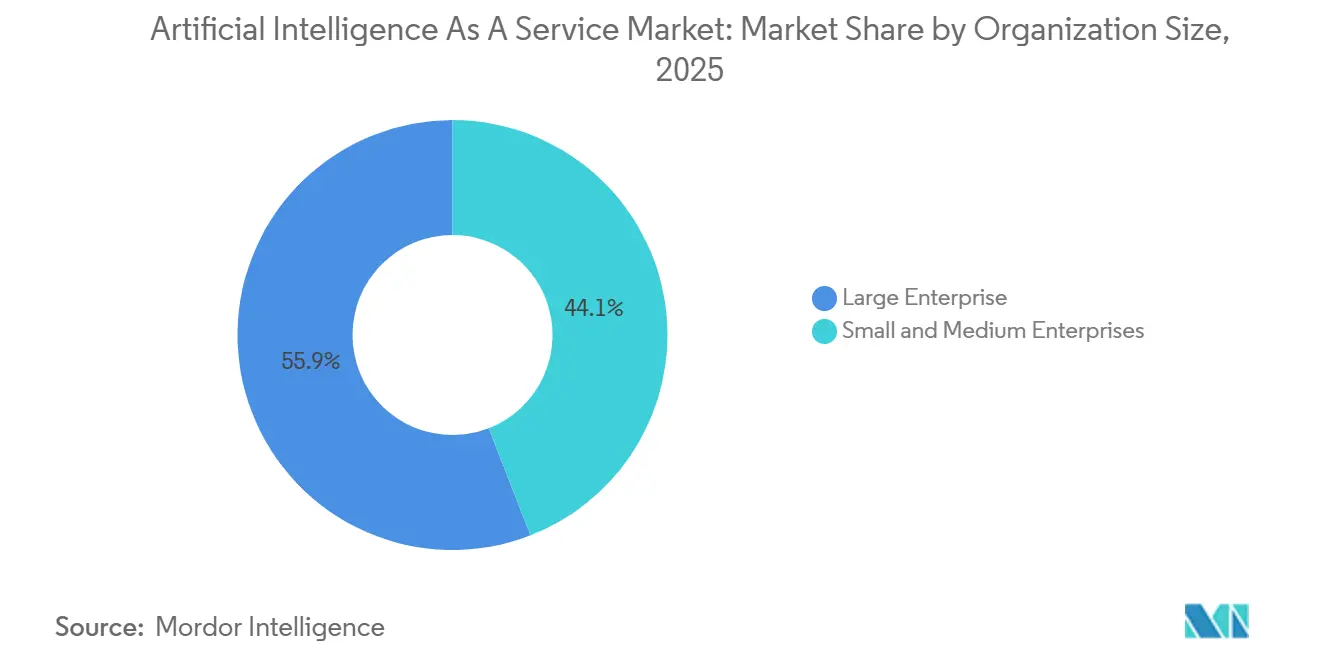

- By organization size, large enterprises accounted for 55.91% of 2025 revenue; small and medium enterprises are advancing at a 28.33% CAGR to 2031.

- By end-user industry, BFSI captured 23.46% of 2025 revenue, yet healthcare and life sciences are advancing at a 29.06% CAGR through 2031.

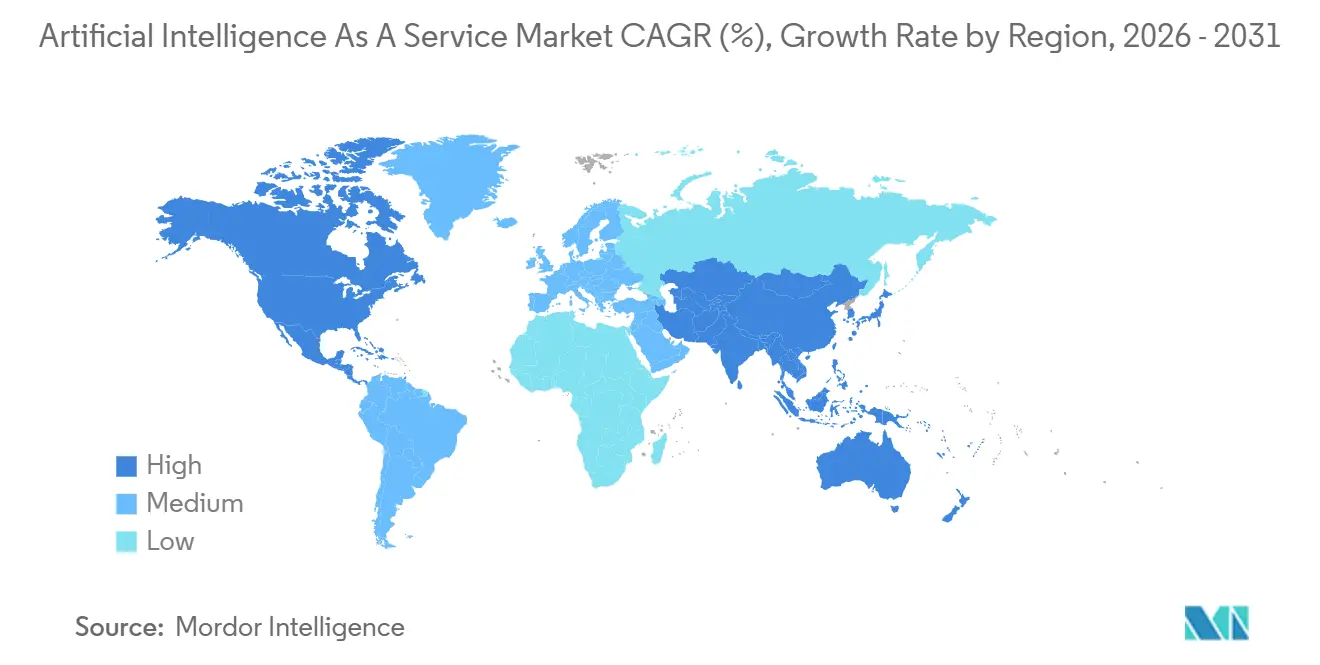

- By geography, North America captured a 39.71% share in 2025; Asia-Pacific is accelerating at a 29.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Artificial Intelligence As A Service Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Predictive and Prescriptive Analytics | +4.2% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Subscription-Based AI Tools Lowering Total Cost of Ownership for SMEs | +3.8% | Global, strongest in Asia-Pacific and South America | Short term (≤ 2 years) |

| Generative-AI APIs Embedded in Low-Code Platforms | +5.1% | North America and Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Rapid Adoption of Public-Cloud AIaaS in Emerging Markets | +4.6% | Asia-Pacific, Middle East, Africa, South America | Medium term (2-4 years) |

| Custom AI Accelerators Slashing Inference Cost | +3.9% | Global, led by North America and Asia-Pacific | Long term (≥ 4 years) |

| Verticalised AIaaS Bundles for Regulated Sectors | +3.4% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Growing Demand for Predictive and Prescriptive Analytics

Companies are replacing descriptive dashboards with forward-looking cloud models that propose concrete actions, fueling sustained consumption of Artificial Intelligence as a Service market capacity. Retailers optimise warehouse stocking by querying demand-forecast APIs, while manufacturers embed prescriptive maintenance algorithms into IoT sensor streams to curb costly downtime.[1]Deloitte Consulting, “2024 Global Supply Chain Survey,” deloitte.com Financial-services desks now stream sub-millisecond forecasts from co-located AI inference endpoints, reflecting an arms race in latency-sensitive trading. Utilities dispatch renewable generation based on weather-driven load predictions, a scenario once priced out of reach on legacy servers. The driver’s relevance cuts across every vertical that must respond to rapidly shifting market signals.

Subscription-Based AI Tools Lowering Total Cost of Ownership for SMEs

Pay-as-you-go pricing collapses entry barriers, letting firms with revenues below USD 10 million invoke high-accuracy sentiment analysis or fraud detection for fractions of a cent per call. The Artificial Intelligence as a Service market benefits because vendors shoulder infrastructure refresh and model retraining, guaranteeing SMEs always run the latest algorithms. Adoption is visible in Brazilian fintechs underwriting micro-loans and Southeast Asian retailers launching recommendation engines without full-time data scientists. Provider-hosted updates also mitigate cybersecurity exposure, making cloud inference safer than unmanaged on-premise code. As subscription economics align with limited SME cash flow, deployment accelerates across emerging markets.

Generative-AI APIs Embedded in Low-Code Platforms

Low-code suites that surface large language models through natural-language prompts let business users build AI features in hours, not quarters.[2]Appian Corporation, “Appian AI and Process Automation,” appian.com A European insurer cut claims-processing time from weeks to hours by combining workflow templates with GPT-4 content generation. Similar integrations span customer-relationship management, enterprise resource planning, and human-capital applications, meaning the Artificial Intelligence as a Service market now monetises not only compute but also democratised development. Surveys show a majority of enterprises plan to embed gen-AI in low-code tools within two years, underscoring how platform vendors without native AI risk attrition.

Rapid Adoption of Public-Cloud AIaaS in Emerging Markets

Sovereign-cloud mandates paired with state subsidies are driving a wave of capacity build-outs across Asia-Pacific and Africa.[3]Government of India, “National AI Cloud Initiative,” meity.gov.in Kenya’s GPU-as-a-service pricing undercuts Western hyperscalers, unlocking agritech and healthtech applications. Thailand and Indonesia have similar policies anchoring models inside national borders, which directs demand toward regional providers. As data-localisation laws proliferate, cloud inference workloads shift geographically, enlarging the Artificial Intelligence as a Service market base beyond North America and Europe.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Cloud Compute-Cost Inflation | -2.8% | Global, most acute in North America and Europe | Short term (≤ 2 years) |

| Heightened Regulatory Scrutiny on Model Provenance | -2.1% | Europe, expanding to North America and Asia-Pacific | Medium term (2-4 years) |

| Data-Privacy and Compliance Costs Rising | -1.9% | Global, led by Europe and North America | Medium term (2-4 years) |

| Persistent MLOps Talent Shortage | -1.6% | Global, most severe in Asia-Pacific and South America | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Heightened Regulatory Scrutiny on Model Provenance

The EU AI Act obliges providers to document training data, model architecture, and validation history, inflating compliance costs for any Artificial Intelligence as a Service market participant serving European clients. Financial-services and healthcare buyers demand third-party audits to attest fairness and robustness, with fees stretching into six figures per model. Smaller vendors delay launches or confine themselves to low-risk applications outside scope, consolidating share among capital-rich hyperscalers and large consultancies.

Escalating Cloud Compute-Cost Inflation

NVIDIA H100 shortages forced hyperscalers to raise on-demand inference rates 15-20% in early 2026, straining budgets for startups lacking reserved capacity. Some enterprises consider repatriating steady-state inference to on-premise clusters, yet capacity constraints and silicon refresh cycles hinder swift moves. Although vendor chips promise relief, workloads often need code refactoring, tempering near-term migration potential. Elevated pricing may persist until new supply from NVIDIA’s Blackwell architecture normalises the GPU market.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Hybrid Cloud Optimises Compliance and Elasticity

Hybrid configurations accounted for a smaller base in 2025 yet are expanding at 29.11% through 2031, outpacing the overall Artificial Intelligence as a Service market CAGR. Banks and hospitals keep sensitive records on-premise to satisfy regulators while training and batch inference run in public clouds when spot prices dip, trimming total cost of ownership without breaching data-sovereignty rules. The Artificial Intelligence as a Service market size for hybrid solutions is projected to overtake private clouds before 2030 as tooling from Databricks and Snowflake streamlines cross-environment orchestration.

Public cloud remains dominant because digital-native firms still prize speed over control, but escalating EU and GCC localisation statutes steer incremental demand toward hybrid blueprints. Azure confidential-computing virtual machines, which secure data in use, illustrate how hyperscalers tailor public offerings to mimic private-cloud assurances. Operational complexity persists around dataset synchronisation and model promotion pipelines, yet rising skills in DevSecOps and policy-driven automation mitigate friction. Consequently, hybrid architectures should secure roughly one-third of Artificial Intelligence as a Service market share by 2031.

By Service Type: Infrastructure Services Surge on Custom Silicon Economics

AI infrastructure services are tracking a 28.52% growth curve, eclipsing the broader Artificial Intelligence as a Service market trajectory as buyers graduate from managed AutoML layers to direct access over GPUs, TPUs, and purpose-built inference chips. In 2025, machine-learning platforms still commanded 40.37% revenue, yet their share is eroding as experienced data-science teams chase lower unit costs and finer control. The Artificial Intelligence as a Service market size for infrastructure offerings will expand further once Microsoft debuts its Maia silicon, intensifying price competition and reinforcing hyperscaler lock-in.

Platform services retain relevance for mid-market clients lacking MLOps expertise, and cognitive-API suites remain indispensable where latency or data volumes render bespoke training overkill. Nonetheless, generative-AI workloads tilt economics decisively toward raw accelerators because inference dominates billable consumption. Smaller regional clouds attempt to counter by negotiating bulk GPU discounts, though their gap may widen as hyperscalers amortise R-and-D across colossal fleets. Accordingly, infrastructure services could command close to 40% Artificial Intelligence as a Service market share by 2031.

By Organization Size: SMEs Accelerate on Pay-As-You-Go Utility

Large enterprises still generated 55.91% of 2025 spending, yet SMEs clock the faster 28.33% CAGR because usage-based billing eliminates capex and vendors absorb the complexity of retraining and scaling. The Artificial Intelligence as a Service market is therefore broadening beyond Fortune 500 adopters to encompass regional e-commerce stores, micro-finance lenders, and digitally savvy sole proprietors. As subscription thresholds fall below USD 100 per month, even family-owned retailers deploy chatbots and inventory forecasting engines that once required multidisciplinary teams.

Challenges remain in data ingestion and label quality, yet ecosystem players respond with turnkey pipelines and synthetic-data generators. SME adoption is most vibrant where mobile broadband is cheap and developer communities flourish, notably Southeast Asia and South America. As a result, the Artificial Intelligence as a Service market share historically held by conglomerates is slowly diluted, although absolute big-company spending continues to climb given expanding use-case breadth.

By End-User Industry: Healthcare Gains Momentum With Regulatory Tailwind

BFSI captured 23.46% of 2025 revenue after years of leadership in fraud detection, risk scoring, and algorithmic trading. However, healthcare and life sciences, driven by 14 FDA-cleared diagnostic algorithms in 2024, now record the strongest 29.06% CAGR and are poised to secure a quarter of Artificial Intelligence as a Service market share by 2031. The Artificial Intelligence as a Service market size for imaging-analysis platforms accelerates as Medicare begins reimbursing AI-assisted reads, and malpractice insurers discount premiums when hospitals deploy FDA-approved tools.

Pharmaceutical sponsors embrace cloud-based clinical-trial optimisation to automate cohort selection and adverse-event prediction, diminishing trial timelines by nearly one-third. BFSI remains vibrant, adding generative-AI document-processing bots and anti-fraud graph neural networks, yet its growth moderates relative to the explosive healthcare upswing. Retail, telecom, manufacturing, and energy continue absorbing AI capabilities, but none match the regulatory catalysts presently propelling clinical applications.

Geography Analysis

North America retained 39.71% of 2025 Artificial Intelligence as a Service market share because hyperscalers and venture-backed model labs concentrate compute, capital, and talent in the United States. Wide generative-AI adoption in workflow software sustains premium cloud billing, while Canada’s immigration-friendly policies draw researchers to emerging hubs in Toronto and Montreal. Growth is moderating as enterprise projects shift from pilots to optimised production, yet expansion persists in automotive, defense, and public-sector workloads.

Asia-Pacific is forecast to grow at 29.55% through 2031, the fastest regional climb in the Artificial Intelligence as a Service market, supported by sovereign-AI mandates in India, Thailand, and Indonesia demanding local hosting of models and data. Domestic providers enjoy policy preference, while Chinese giants invest billions in onshore GPU capacity to bypass U.S. export curbs. Japan and South Korea differentiate on language-specific natural-language processing that Western clouds struggle to localise. Australia and New Zealand contribute meaningfully via mining-sector predictive-maintenance deployments and banking chatbots.

Europe holds near 22% market share, constrained by GDPR and the AI Act, which together raise compliance expenses and slow rollout velocity for external vendors. However, regional champions such as T-Systems and OVHcloud capture workloads that require strict data residency. The Middle East is emerging quickly after Saudi Arabia’s NEOM and the United Arab Emirates made nine-figure investments in sovereign AI clouds. South America gains traction as Brazilian fintechs and Argentine agritech startups exploit low-cost credit-scoring and crop-monitoring APIs. Africa is nascent yet promising, with Kenya’s Konza Technopolis pioneering GPU-as-a-service and attracting pan-regional developers.

Competitive Landscape

The Artificial Intelligence as a Service market features moderate concentration; Amazon Web Services, Microsoft Azure, and Google Cloud jointly control about 60% of worldwide revenue, yet fragmentation intensifies as regional hyperscalers, vertical specialists, and open-source collectives gain share. Custom silicon competition is fierce: Trainium3 undercuts NVIDIA H100 inference pricing by roughly 40%, Google’s TPU v5 offers similar gains for TensorFlow, and Microsoft readies Maia to bolster Azure. These chips reduce variable costs enough to trigger mass workload migration but deepen vendor lock-in because compiler stacks diverge.

Pure-play vendors such as DataRobot, H2O.ai, and C3.ai anchor their value in AutoML, vertical templates, or governance modules that shrink deployment cycles from months to days. They court mid-market buyers underserved by hyperscaler professional-services teams. Regional providers seize data-sovereignty mandates; Alibaba’s USD 200 million build-out for Saudi Arabia’s NEOM exemplifies how geography and regulation intersect to create defensive moats against U.S. incumbents. Japanese, Korean, and Arabic language models further insulate domestic contenders from global competition.

Strategic moves during 2025-2026 include Microsoft’s USD 3 billion Southeast-Asia data-centre expansion, AWS’s general availability of Trainium3, and Google’s free PaLM 2 integration into Workspace, each designed to widen funnel reach and embed AI into daily workflows. Compliance innovation is another arena: IBM’s watsonx.governance and Databricks’ Unity Catalog promise faster EU AI Act conformance, differentiating platforms where regulation dictates buying criteria. Overall, success hinges on a blend of cost leadership from proprietary hardware, differentiated generative-AI services, and verticalised compliance wrappers.

Artificial Intelligence As A Service Industry Leaders

Microsoft Corporation

Google LLC

Amazon Web Services, Inc.

IBM Corporation

BigML Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Microsoft announced a USD 3 billion investment to expand Azure AI infrastructure across Jakarta, Manila, and Bangkok, adding localised compliance features for sovereign-cloud mandates.

- January 2026: Databricks launched Unity Catalog for AI Governance, cutting provenance-documentation time by an estimated 60% for European finance clients.

- December 2025: Amazon Web Services introduced Trainium3, delivering 40% lower inference cost per token than Trainium2 and entering general availability in January 2026.

- November 2025: Alibaba Cloud signed a USD 200 million partnership with Saudi Arabia’s NEOM to construct a sovereign AI cloud supporting smart-city workloads.

Global Artificial Intelligence As A Service Market Report Scope

Artificial Intelligence-as-a-Service (AIaaS) accounts for a third-party offering to outsource artificial intelligence. It allows companies or end-users to experiment with AI for various purposes by limiting initial investment and lowering risk.

The Artificial Intelligence As A Service Market Report is Segmented by Deployment Model (Public Cloud, Private Cloud, Hybrid Cloud), Service Type (Machine-Learning Platform Services, Cognitive Services, AI Infrastructure Services, Managed and Professional AI Services), Organisation Size (SMEs, Large Enterprises), End-User Industry (BFSI, Retail and E-Commerce, Healthcare and Life Sciences, IT and Telecom, Manufacturing, Energy and Utilities, Rest of End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Public Cloud |

| Private Cloud |

| Hybrid Cloud |

| Machine-Learning Platform Services |

| Cognitive Services (NLP, CV, Speech) |

| AI Infrastructure Services (GPU/TPU) |

| Managed and Professional AI Services |

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| BFSI |

| Retail and E-Commerce |

| Healthcare and Life Sciences |

| IT and Telecom |

| Manufacturing |

| Energy and Utilities |

| Rest of End-User Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| South-East Asia | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Deployment Model | Public Cloud | |

| Private Cloud | ||

| Hybrid Cloud | ||

| By Service Type | Machine-Learning Platform Services | |

| Cognitive Services (NLP, CV, Speech) | ||

| AI Infrastructure Services (GPU/TPU) | ||

| Managed and Professional AI Services | ||

| By Organisation Size | Small and Medium Enterprises (SMEs) | |

| Large Enterprises | ||

| By End-User Industry | BFSI | |

| Retail and E-Commerce | ||

| Healthcare and Life Sciences | ||

| IT and Telecom | ||

| Manufacturing | ||

| Energy and Utilities | ||

| Rest of End-User Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| South-East Asia | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How fast is spending on Artificial Intelligence as a Service growing toward 2031?

Market value is expected to climb from USD 28.91 billion in 2026 to USD 98.64 billion by 2031, reflecting a 27.82% CAGR locked in by demand for pay-per-use inference.

Which deployment pattern shows the strongest growth momentum?

Hybrid cloud leads in relative terms, advancing at a 29.11% CAGR as firms blend on-premise data control with public-cloud elasticity for training bursts.

Why are custom accelerators important for AI-in-the-cloud economics?

Chips such as AWS Trainium3 and Google TPU v5 cut per-token inference cost by up to 40%, enabling enterprises to scale generative-AI workloads without budget overruns.

What regulatory trend most affects European AIaaS providers?

The EU AI Act mandates provenance documentation for high-risk models, increasing compliance overhead by roughly 15-20% and favoring suppliers with robust governance toolkits.

Which vertical will likely outpace BFSI growth by 2031?

Healthcare and life sciences are set to secure roughly one-quarter market share thanks to FDA-cleared diagnostic algorithms and expanding reimbursement for AI-assisted reads.

How are SMEs benefiting from the Artificial Intelligence as a Service model?

Pay-as-you-go APIs remove capital expense barriers, letting small firms deploy sentiment analysis or fraud detection for fractions of a cent per call while providers manage updates.

Page last updated on: