Allergy Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 24.49 Billion |

| Market Size (2031) | USD 35.28 Billion |

| Growth Rate (2026 - 2031) | 7.58% CAGR |

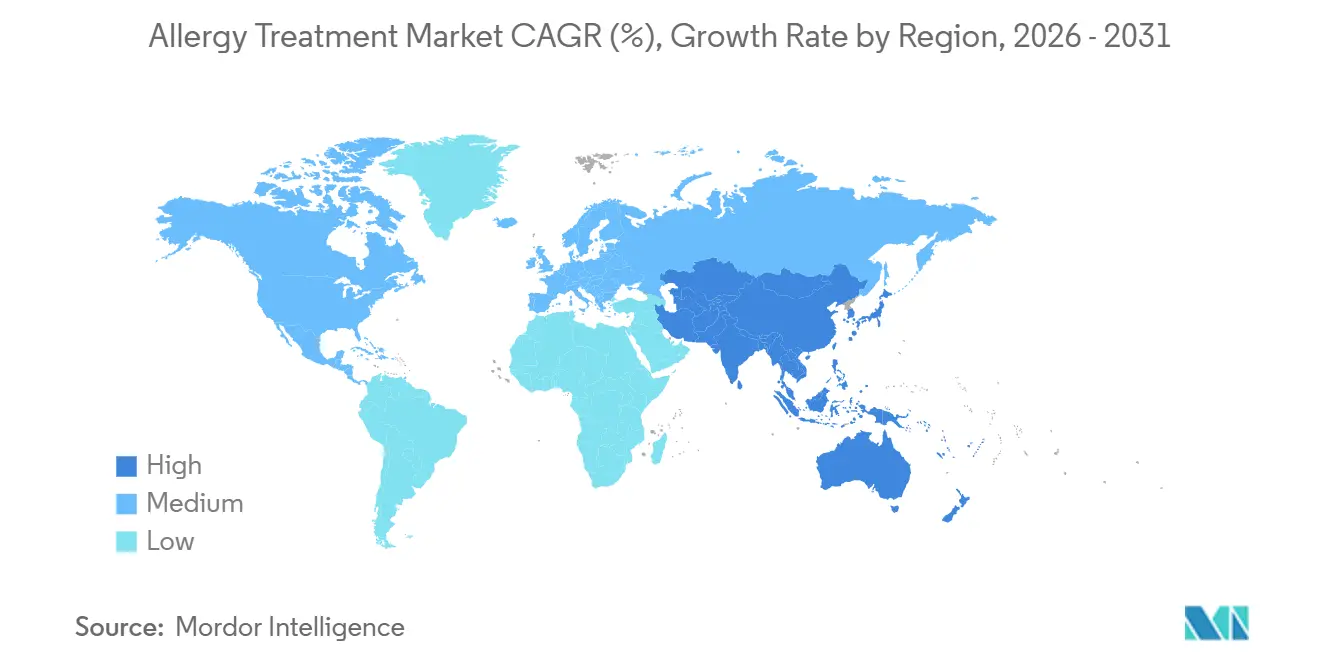

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Allergy Treatment Market Analysis by ���ϲ�����

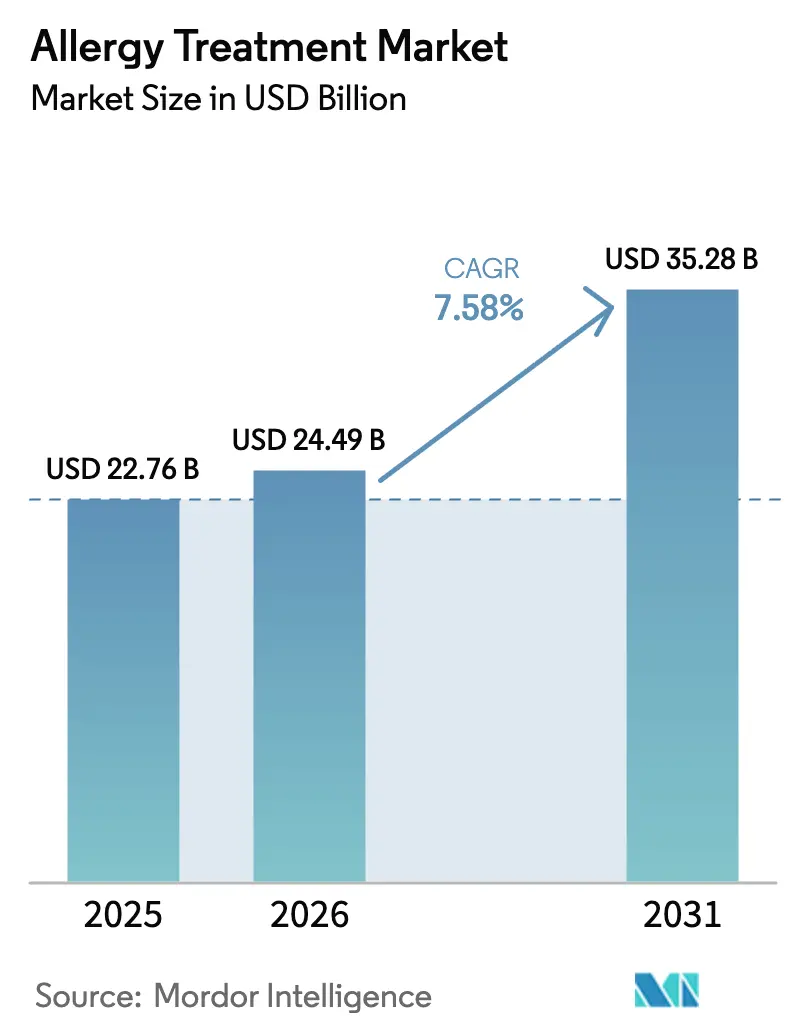

The Allergy Treatment Market size is expected to increase from USD 22.76 billion in 2025 to USD 24.49 billion in 2026 and reach USD 35.28 billion by 2031, growing at a CAGR of 7.58% over 2026-2031.

Accelerated disease prevalence, climate-driven allergen amplification, and breakthrough biologics are collectively boosting demand, while new digital health models are broadening access and improving adherence. Competitive intensity has sharpened since omalizumab won the first multi-food indication, drawing both large pharmaceutical firms and nimble biotech entrants into direct rivalry. Regulatory initiatives that accelerate biosimilar substitution add price pressure while simultaneously stimulating innovation in delivery technologies, immunotherapy personalization, and patient-centric care. Geographic divergence remains pronounced: North America sustains spending leadership on biologics, whereas Asia-Pacific records the fastest uptake of immunotherapy as urbanization deepens sensitization levels.

Key Report Takeaways

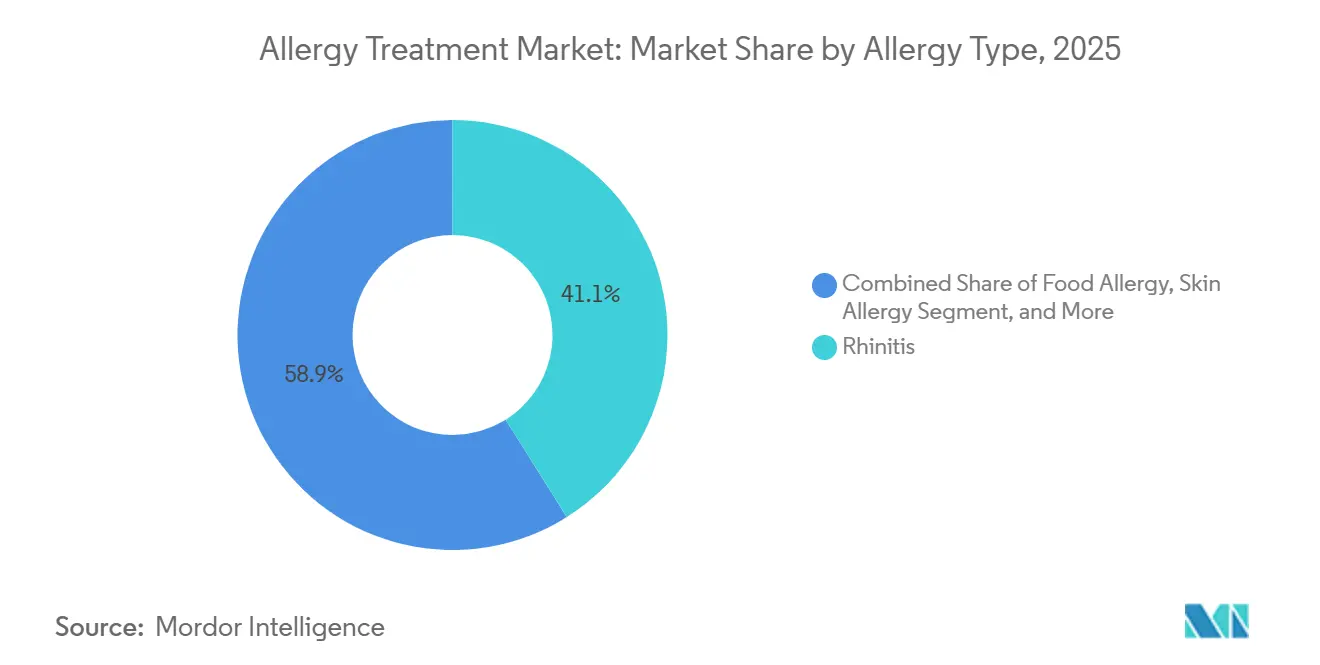

- By allergy type, rhinitis accounted for 41.08% of the Allergy treatment market share in 2025; food allergy is forecast to expand at a 9.22% CAGR through 2031.

- By treatment, anti-allergy drugs dominated the Allergy treatment market with a 64.89% share in 2025, while immunotherapy is poised for a 10.12% CAGR to 2031.

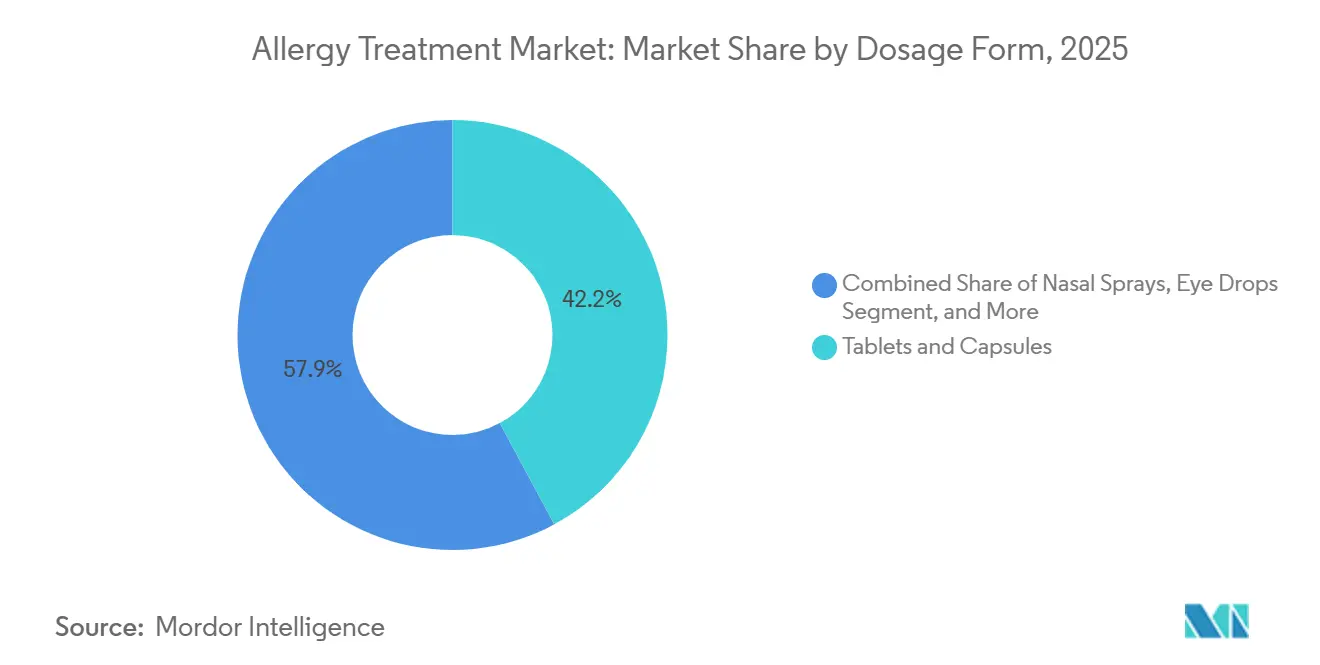

- By dosage form, tablets and capsules accounted for 42.15% of the Allergy treatment market in 2025; injectables and auto-injectors are projected to exhibit a 9.78% CAGR over 2026-2031.

- By distribution channel, hospital pharmacies led with 34.88% Allergy treatment market share in 2025; online pharmacies are projected to post a 10.96% CAGR to 2031.

- By geography, North America accounted for 37.84%% of the allergy treatment market share in 2025, whereas Asia-Pacific is advancing at a 9.31% CAGR during the forecast horizon.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Allergy Treatment Market Trends and Insights

Drivers Impact Analysis

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising prevalence of allergic rhinitis & asthma | 1.8% | Global, with acute burden in urbanized Asia-Pacific and North America | Medium term (2-4 years) |

| Increasing patient preference for OTC & self-medication | 1.2% | North America, Europe, with spillover to urban APAC | Short term (≤ 2 years) |

| Growing investments in biologics & novel therapeutics | 1.5% | North America & EU regulatory corridors, expanding to Japan, South Korea | Medium term (2-4 years) |

| Climate-induced amplification of airborne allergens | 1.0% | Temperate zones in North America, Europe; emerging in subtropical APAC | Long term (≥ 4 years) |

| AI-driven personalised immunotherapy rollouts | 0.9% | North America, Western Europe, select APAC hubs (Singapore, Japan) | Medium term (2-4 years) |

| Tariff-driven on-shoring of API/biologic capacity | 0.7% | United States, with secondary effects in EU and India | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Rising Prevalence of Allergic Rhinitis & Asthma

Global incidence curves point upward: 25% of U.S. children now carry an allergic diagnosis, and projections show China overtaking Japan in asthma incidence by 2030.[1]Medical Letter, “Omlyclo — An Omalizumab Biosimilar Interchangeable with Xolair,” medicalletter.org House-dust-mite sensitization already exceeds 85% in Singapore and southern China, while Japanese cedar pollinosis climbed from 26% to 39% between 2008 and 2024.[2]European Medicines Agency, “Eurneffy | European Medicines Agency,” ema.europa.eu These epidemiologic shifts enlarge the candidate pool for antihistamines, corticosteroids, and allergen immunotherapy, reinforcing long-term demand in the allergy treatment market. As prevalence rises fastest in densely populated cities, payers support school-based screening and vaccination-like immunotherapy campaigns, anchoring medium-term growth.

Surging urban air pollution fuels oxidative stress that flips immune responses toward a TH2 profile, anchoring demand for prescription antihistamines, leukotriene antagonists, and biologics in the Allergy treatment market. Megacities from Beijing to Delhi report sensitization rates exceeding 50%, while cost burdens in the United States already surpass USD 3.4 billion annually. The global scope of rhinitis, affecting up to 30% of adults and 40% of children, makes it the single largest patient pool and a reliable revenue base.

Increasing Patient Preference for Self-Medication & OTC Drugs

Better-tolerated second-generation antihistamines and intranasal corticosteroids have migrated from prescription to OTC status, widening consumer reach and lifting overall transaction volumes in the Allergy treatment market. United States households spent USD 645 on non-prescription medicines in 2023, up 8% from 2021, and 81% of adults now choose OTC remedies as their first response to symptoms.[3]U.S. Food and Drug Administration, “FDA Approves First Medication to Help Reduce Allergic Reactions to Multiple Foods After Accidental Exposure,” fda.gov Retail chains expand private-label antihistamine portfolios, and pharmacist-led triage directs non-responders toward biologics, shortening care pathways. Because many written prescriptions remain unfilled, self-care channels help buffer elasticity in the allergy treatment market against copay shocks. Smartphone apps that track pollen counts integrate with e-commerce refill reminders, sustaining adherence beyond peak seasons.

Growing Investments in Novel Therapeutics & Biologics

Capital allocation to IgE-, cytokine-, and alarmin-targeting antibodies has intensified since the FDA cleared omalizumab for multiple food allergies in February 2024. Sanofi’s USD 9.1 billion acquisition of Blueprint Medicines in June 2025 underscores pharma’s appetite for specialized immunology assets. Pipeline candidates like depemokimab, ligelizumab, and UB-221 promise competitive step-ups in potency and combinability, bolstering the long-term growth runway for the Allergy treatment market.

The FDA’s February 2024 green light for omalizumab in multi-allergen food allergy opened a transformative indication with few therapeutic options.[4]U.S. Food and Drug Administration, “FDA Approves First Medication to Reduce Allergic Reactions to Multiple Foods After Accidental Exposure,” fda.gov Dupixent followed in January 2024 with coverage of eosinophilic esophagitis in children, expanding its atopic franchise. September 2025 brought remibrutinib, the first oral BTK inhibitor approved for chronic spontaneous urticaria, validating a new mechanism. Concurrently, the first interchangeable omalizumab biosimilar launched in March 2025 at a 15-30% discount, broadening payer access while spurring originators to pursue delivery innovations. These advances reinforce the premium biologics segment and elevate average selling prices within the allergy treatment market.

Climate-Induced Amplification of Airborne Allergens

WHO data from July 2025 confirm that temperate pollen seasons now extend 27 days beyond historical norms. Elevated CO₂ levels boost pollen production per plant, while nitrogen dioxide and PM2.5 aggravate sensitization risk, especially in South Asian megacities that exceed WHO guidelines by 9 times. Longer exposure windows lock patients into year-round therapy, increasing unit volumes for inhaled corticosteroids and intranasal antihistamines. Extract manufacturers, exposed to harvest variability, are pivoting toward recombinant platforms to secure supply, thereby supporting sustained biologic innovation in the allergy treatment market.

Restraint Impact Analysis

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Escalating uptake of low-cost biosimilars | -0.8% | North America, Europe, with emerging penetration in APAC | Short term (≤ 2 years) |

| Limited reimbursement for biologics & SLIT | -1.0% | United States, selective EU markets, emerging in Asia-Pacific | Medium term (2-4 years) |

| Low HCP & patient awareness of AIT durability | -0.6% | Global, most acute in Asia-Pacific and Latin America | Medium term (2-4 years) |

| Biodiversity loss straining natural-extract supply | -0.4% | Europe (birch, grass), North America (ragweed), with spillover to APAC | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Escalating Uptake of Low-Cost Biosimilars Eroding Price/Margins

Interchangeable omalizumab and a wave of ustekinumab biosimilars cut unit prices by up to 40%, compressing top-line growth for originators within the Allergy treatment market.[5]U.S. Food and Drug Administration, “FDA Approves First Medication to Reduce Allergic Reactions to Multiple Foods After Accidental Exposure,” fda.gov Europe’s tender systems hasten penetration, while emerging economies embrace cost-relief as gateways to biologic access. Originators respond with device upgrades and real-world evidence dossiers to justify premium positioning. Pharmacist-level substitution became a reality when the interchangeable omalizumab biosimilar debuted in March 2025. Discounts of up to 30% erode margins for innovators, yet could stimulate volume as payers relax restrictions. Smaller companies must now prove mechanistic differentiation or superior delivery to avoid commoditization. The aggregate effect is a modest drag on revenue growth, but it is offset by heightened therapy penetration in the allergy treatment market.

Limited Reimbursement for Biologics & SLIT

Prior authorization, site-of-care rules, and variable co-insurance rates restrict access to biologics and SLIT, especially in U.S. commercial plans and select EU markets. Medicare Part B reimburses biosimilars at ASP + 6%, incentivizing cheaper alternatives. Some patients elect prolonged OTC regimens rather than shoulder-high deductibles, delaying disease-modifying care. Until value-based contracts or real-world evidence shift payer calculus, reimbursement friction will shave a whole percentage point from projected CAGR for the allergy treatment market.

Segment Analysis

By Allergy Type: Food Allergy Reshapes Pediatric Protocols

Rhinitis contributed 41.08% to the Allergy treatment market share in 2025, capitalizing on its high global prevalence and multi-modal therapy toolkit. Over-the-counter antihistamines, intranasal corticosteroids, and SLIT tablets form the therapeutic spine, while biologics gain traction in severe poly-sensitized cohorts. Seasonal and perennial variants jointly sustain an expansive prescription base, guaranteeing baseline demand regardless of emergent treatment classes.

Food allergy, the fastest-growing segment at 9.22% CAGR to 2031, benefits from the first disease-modifying biologic clearance and a broad pipeline of oral immunotherapy combinations. Epidemiological recognition of adult-onset allergy enlarges eligibility pools, and school-based anaphylaxis protocols amplify prophylactic prescriptions. Eye, skin, asthma, and other niche allergies round out the segment landscape, each adding volume through fortified diagnostic vigilance and cross-indication biologic use.

Note: Segment shares of all individual segments available upon report purchase

By Treatment: Immunotherapy Gains as Disease Modification Enters Mainstream

Anti-allergy drugs maintained 64.89% of the Allergy treatment market share in 2025, bolstered by favorable reimbursement, OTC prominence, and maturing generics. Second-generation antihistamines, topical corticosteroids, and leukotriene blockers together form a stable revenue stream that cushions price swings in novel categories.

Immunotherapy is slated for a 10.12% CAGR through 2031, reflecting payer recognition of long-term cost efficiency and rising patient preference for home-based SLIT regimens. Clinical guidelines standardize dosing and duration, minimizing variability and elevating clinician confidence. Subcutaneous protocols remain the gold standard for maximizing efficacy in high-risk patients, while combination biologic-SLIT strategies emerge for complex multisensitizations, strengthening the Allergy treatment market proposition.

By Dosage Form: Injectables Surge on Needle-Free Innovation

Tablets and capsules accounted for 42.15% of the Allergy treatment market in 2025, owing to manufacturing scalability, patient familiarity, and straightforward regulatory pathways. Their stronghold persists in OTC antihistamines and prescription leukotriene antagonists, yet innovation is gradually steering high-value therapy toward parenteral formats.

Injectables and auto-injectors are projected to grow at a 9.78% CAGR, driven by monoclonal antibody expansion and needle-free innovations such as ARS Pharmaceuticals’ nasal epinephrine spray, which sidesteps needle phobia. Nasal sprays and inhalers remain relevant through their localized delivery precision, while smart inhaler add-ons improve adherence tracking in asthma overlap cases.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Digital Transformation Accelerates Online Growth

Hospital pharmacies retained 34.88% of the allergy treatment market share in 2025, anchored by biologic initiation protocols that require clinical oversight. Risk-mitigation strategies for anaphylaxis during first-dose administration mandate the presence of observation facilities, reinforcing hospital dominance.

Online pharmacies are expected to expand at a 10.96% CAGR, supported by e-prescribing, teleconsultation integration, and upgrades to last-mile cold-chain logistics. Digital refill calendars and AI-driven adherence nudges enhance patient convenience, supporting chronic therapy retention and widening the Allergy treatment market. Retail and specialty pharmacies occupy the continuum between hospital control and direct-to-door models, diversifying channel resilience.

Geography Analysis

North America’s 37.84% share of the allergy treatment market in 2025 stems from extensive insurance coverage, early adoption of biologics, and a concentrated specialist network. The United States spearheads regulatory firsts that propagate to other regions, positioning domestic manufacturers for early revenues and prolonging lifecycle advantages. Biosimilar penetration remains moderate given substitution hesitancy and REMS constraints, preserving price integrity for innovators.

Asia-Pacific’s 9.31% CAGR through 2031 outpaces all other regions, driven by urbanization-linked sensitization surges, rising disposable incomes, and expanded public-health insurance that covers select immunotherapies. House-dust-mite sensitization exceeds 90% in atopic cohorts, driving demand for region-matched allergen extracts and fueling collaborative distribution deals, such as ALK-Abbott’s tie-up with Abbott. Mobile-first healthcare adoption accelerates SLIT tele-care in metropolitan clusters, broadening therapy reach.

Europe shows mature penetration but faces price compression under biosimilar-friendly tender frameworks. The region leads in standardizing immunotherapy quality and pharmacovigilance, contributing to sustainable yet restrained revenue growth. Middle East & Africa and South America present emergent opportunities with gradually improving specialty-care infrastructure, though economic and supply-chain volatility temper near-term traction.

Competitive Landscape

The allergy treatment market is fragmented. Top players such as GSK, Novartis, and Sanofi blend incipient biologics with entrenched antihistamines to hedge lifecycle risks. ALK-Abbello and Stallergenes Greer dominate allergen-extract supply and SLIT commercialization, while Celltrion’s Omlyclo biosimilar demonstrates the disruptive force of interchangeability.

Device innovation gains prominence. ARS Pharmaceuticals secured EMA clearance for the first nasal epinephrine spray, removing injection barriers and spotlighting patient-centric design. Biotech challengers leverage virus-like particle technology to re-engineer immunogenic profiles, as illustrated by Angany’s eBioparticle platform. Digital therapeutics and AI-predictive engines differentiate service portfolios, deepening competitive moats around adherence outcomes and real-world evidence.

Strategic deals dominate the newsflow. Sanofi’s Blueprint buyout adds KIT inhibitors to an already formidable immunology armamentarium, while alliances between global pharma and regional distributors unlock emerging-market penetration. R&D partnerships de-risk early biologic assets, spreading capital exposure and accelerating time-to-market in the Allergy treatment market.

Allergy Treatment Industry Leaders

Sanofi SA

GSK plc

ALK-Abello A/S

Novartis AG

Johnson & Johnson Services, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Aquestive received an FDA Complete Response Letter for Anaphylm sublingual epinephrine film intended for anaphylaxis in patients ≥30 kg.

- January 2026: Allergy Therapeutics lifted H1 revenues to GBP 36.3 million, launched Grassmuno in Germany, and refinanced debt to fund European expansion.

- January 2026: GSK announced a USD 2.2 billion takeover of RAPT Therapeutics, acquiring ozureprubart, a next-generation anti-IgE candidate for broad food-allergy prophylaxis.

- September 2025: FDA approved remibrutinib for chronic spontaneous urticaria, introducing the first oral BTK inhibitor in allergy care.

- March 2025: FDA granted interchangeable status to the first omalizumab biosimilar, enabling automatic pharmacy substitution at a 15-30% discount.

- February 2025: FDA expanded Odactra’s label to include children aged 5-11 with dust-mite allergic rhinitis, enlarging the pediatric immunotherapy market.

Global Allergy Treatment Market Report Scope

As per the scope of the report, an allergy is a condition in which the immune system reacts abnormally to a foreign substance. Allergy treatment involves drugs and therapies that reduce allergy symptoms and help the immune system prepare for future encounters.

The allergy treatment market is segmented by type, treatment, and geography. By type, the market is segmented into eye allergy, rhinitis, asthma, skin allergy, and other allergies. By treatment, the market is segmented into anti-allergy drugs and immunotherapy. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers market size and forecast in terms of value (USD) for the above segments.

| Eye Allergy |

| Rhinitis |

| Asthma |

| Skin Allergy |

| Food Allergy |

| Other Allergies |

| Anti-Allergy Drugs | Antihistamines - 1st Gen |

| Antihistamines - 2nd/3rd Gen | |

| Corticosteroids - Topical/Inhaled/Systemic | |

| Decongestants - Oral/Nasal | |

| Leukotriene Receptor Antagonists | |

| Biologics & mAbs | |

| Immunotherapy | Sub-cutaneous (SCIT) |

| Sub-lingual (SLIT Tablets/Drops) |

| Tablets & Capsules |

| Nasal Sprays |

| Eye Drops |

| Inhalers |

| Injectables & Auto-injectors |

| Hospital Pharmacies |

| Retail Pharmacies & Drug Stores |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Allergy Type | Eye Allergy | |

| Rhinitis | ||

| Asthma | ||

| Skin Allergy | ||

| Food Allergy | ||

| Other Allergies | ||

| By Treatment | Anti-Allergy Drugs | Antihistamines - 1st Gen |

| Antihistamines - 2nd/3rd Gen | ||

| Corticosteroids - Topical/Inhaled/Systemic | ||

| Decongestants - Oral/Nasal | ||

| Leukotriene Receptor Antagonists | ||

| Biologics & mAbs | ||

| Immunotherapy | Sub-cutaneous (SCIT) | |

| Sub-lingual (SLIT Tablets/Drops) | ||

| By Dosage Form | Tablets & Capsules | |

| Nasal Sprays | ||

| Eye Drops | ||

| Inhalers | ||

| Injectables & Auto-injectors | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies & Drug Stores | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the global Allergy treatment market in 2026?

It stands at USD 24.49 billion and is set to reach USD 35.28 billion by 2031.

Which therapy class is growing fastest?

Immunotherapy, particularly SLIT and biologics, is projected to register a 10.12% CAGR through 2031.

Why does Asia-Pacific record the quickest growth?

Rapid urbanization, extreme sensitization rates, and expanding insurance coverage drive a 9.31% CAGR.

What innovation addresses needle phobia in anaphylaxis care?

The EMA-approved nasal epinephrine spray (Eurneffy) delivers adrenaline without injections.

How are biosimilars influencing pricing?

Interchangeable omalizumab biosimilars slash costs by up to 40%, eroding originator margins yet widening access.

Which distribution channel is most dynamic?

Online pharmacies, supported by tele-care integration, are advancing at an 10.96% CAGR.