Allergy Diagnostics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 7.06 Billion |

| Market Size (2031) | USD 12.04 Billion |

| Growth Rate (2026 - 2031) | 11.25% CAGR |

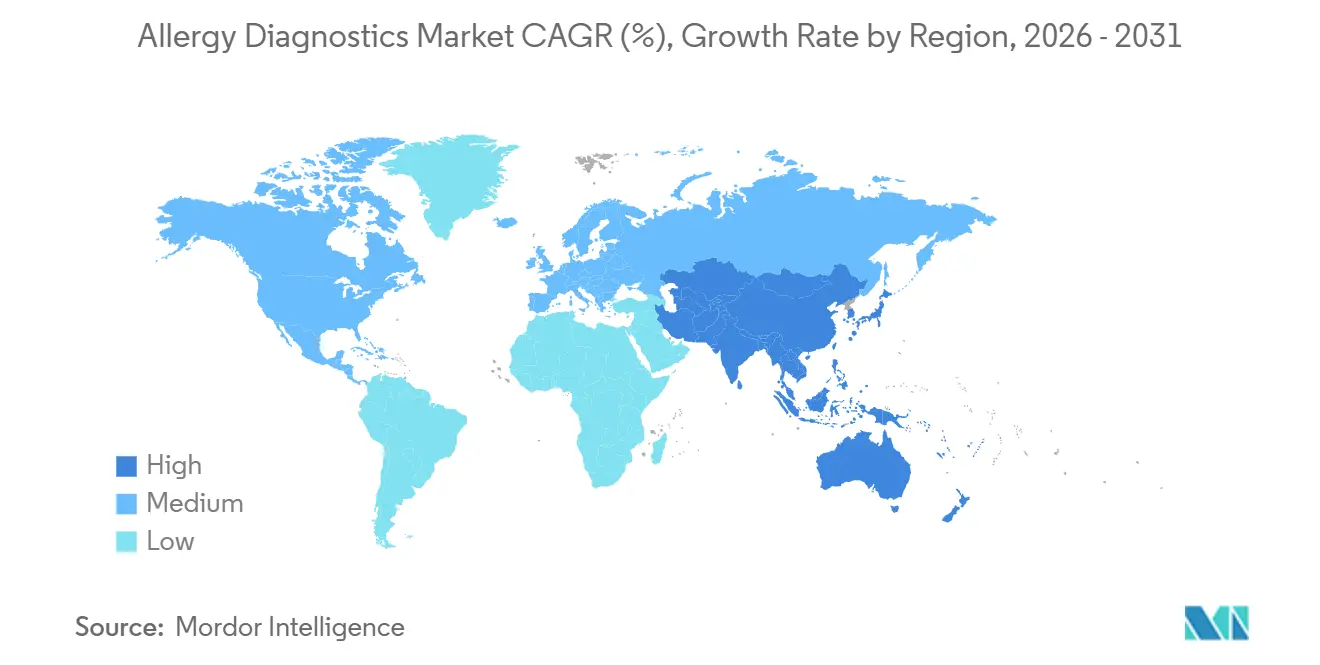

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Allergy Diagnostics Market Analysis by ���ϲ�����

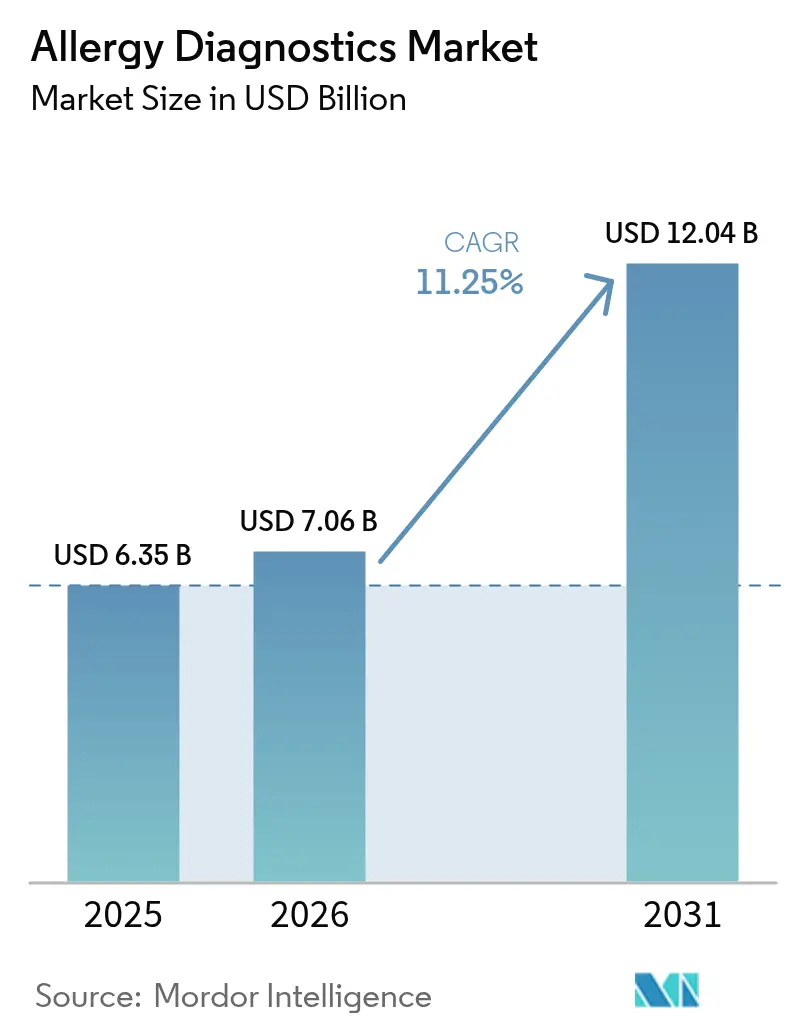

The Allergy Diagnostics Market size is projected to be USD 6.35 billion in 2025, USD 7.06 billion in 2026, and reach USD 12.04 billion by 2031, growing at a CAGR of 11.25% from 2026 to 2031.

Heightened disease awareness, broader payer coverage for specific IgE panels, and the migration from manual enzyme immunoassays to fully automated multiplex platforms are widening testing access and compressing turnaround times. Automation embedded with artificial intelligence drives consistent interpretation, while climate-linked extensions of pollen seasons sustain year-round demand. Vendors are layering tele-immunology channels on top of centralized laboratories, letting patients submit capillary samples from home. Competitive intensity is rising as incumbents add vertically integrated reagent supply, and smaller firms differentiate through low-volume assay kits, fueling recurring consumables revenue.

Key Report Takeaways

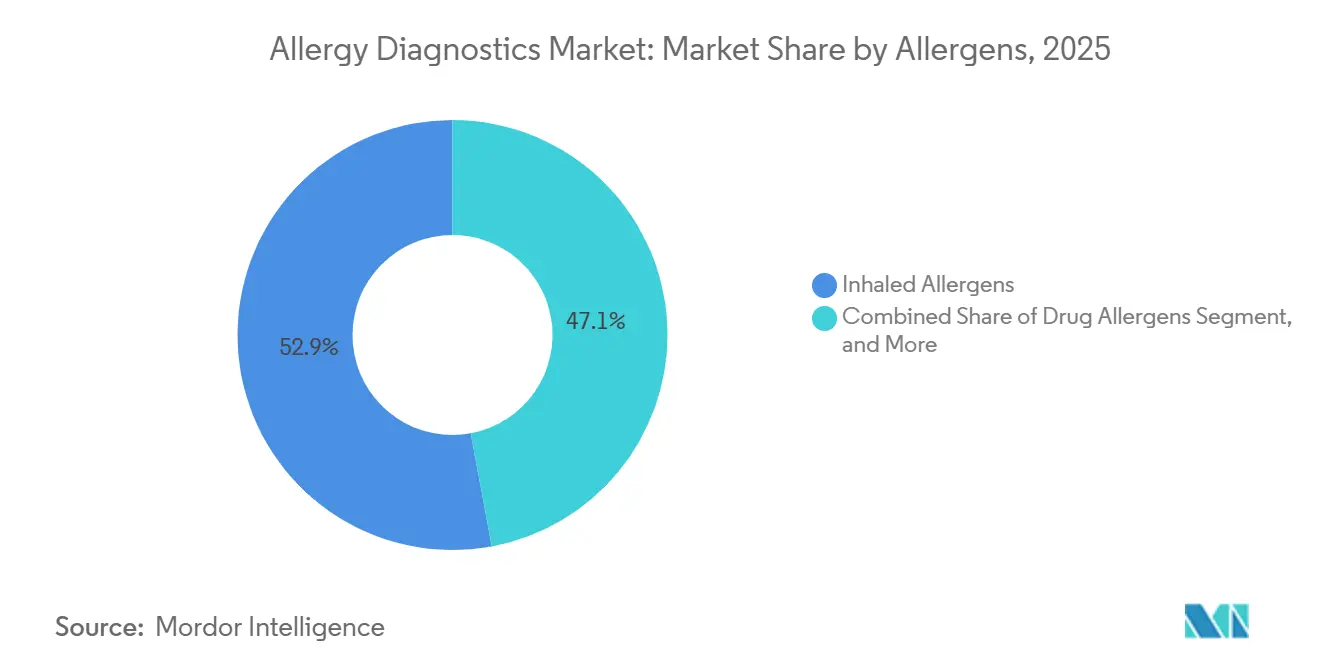

- By allergens, inhaled allergens accounted for 52.92% of 2025 demand; food allergens are poised to grow at a 13.20% CAGR through 2031.

- By product and service, consumables retained 61.74% of 2025 revenue, while instruments are forecast to expand at a 12.35% CAGR through 2031.

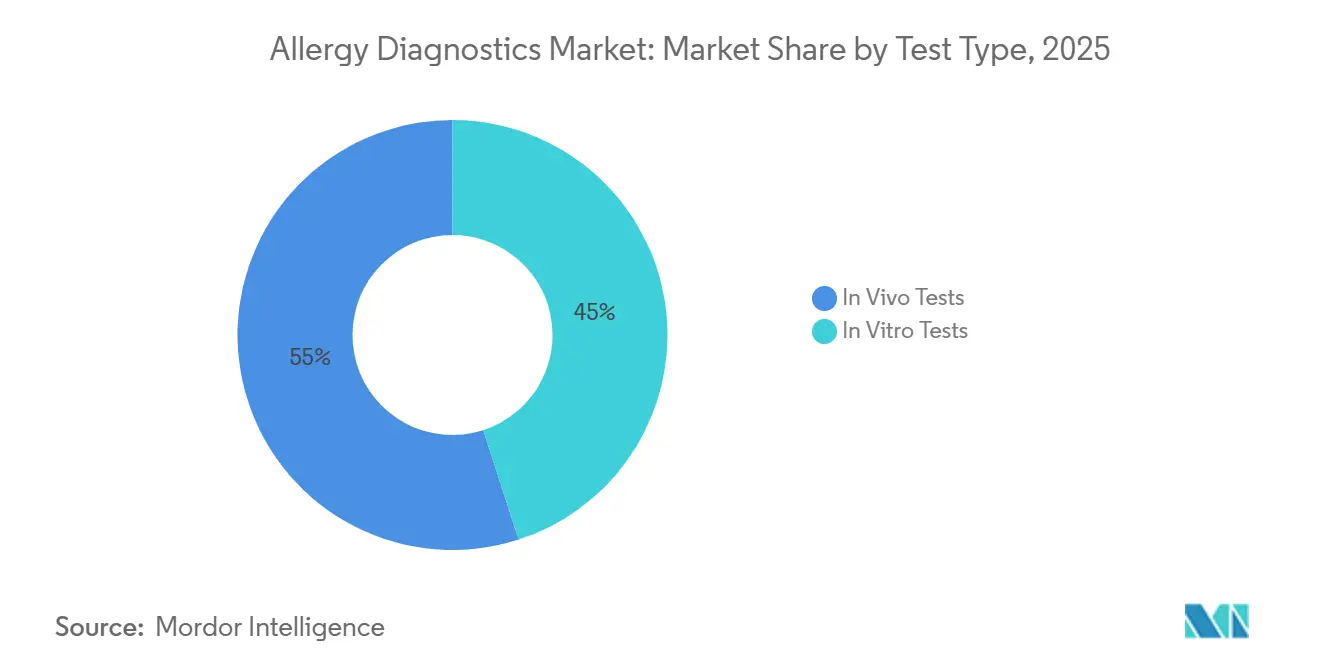

- By test type, in vivo tests held a 54.98% allergy diagnostics market share in 2025, yet in vitro assays are advancing at a 13.25% CAGR to 2031.

- By end user, diagnostic laboratories accounted for 44.62% of the 2025 value, but primary-care settings are set to rise at a 13.90% CAGR to 2031.

- By geography, North America led with 37.68% revenue share in 2025, while Asia-Pacific is projected to log the fastest 13.75% CAGR over 2027-2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Allergy Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising prevalence of polysensitization in paediatric populations | +2.1% | Global, highest in urban North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Expansion of reimbursement for specific ige blood tests | +1.8% | North America, Western Europe | Short term (≤ 2 years) |

| Technological shift to fully automated multiplex allergy platforms | +2.3% | Global, led by North America and Europe | Medium term (2-4 years) |

| Climate-induced lengthening of pollen seasons | +1.5% | North America, Europe, temperate Asia-Pacific | Long term (≥ 4 years) |

| Tele-immunology enabling remote allergy testing kits | +1.4% | North America, Western Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| Ai-driven interpretation software embedded in analysers | +1.9% | Global early adopters | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Rising Prevalence of Polysensitization in Pediatric Populations

Early-life exposure to diverse environmental antigens in dense urban settings is driving simultaneous IgE reactivity to multiple allergen sources. Component-resolved diagnostics parse cross-reactive carbohydrate determinants from genuine sensitizations, letting clinicians tailor immunotherapy and avoid unnecessary dietary restrictions. Microarray panels test more than 100 allergen components from a 4-microliter sample, reducing venipuncture trauma and improving compliance.[1]MD Clarity, “CPT Code 95044: What It Is, Modifiers, Reimbursement,” mdclarity.com Precise phenotyping also stratifies candidates for emerging biologics that target severe pediatric asthma linked to atopy. As payers document reduced emergency visits, reimbursement momentum is strengthening, further stimulating test volumes. Laboratories that adopt molecular platforms are positioned to serve longitudinal monitoring panels that track sensitization trajectories from infancy through adolescence.

Expansion of Reimbursement for Specific IgE Blood Tests

In 2024, Medicare and major U.S. commercial insurers broadened coverage for multiplex IgE panels, recognizing that early diagnosis lowers anaphylaxis admissions and downstream costs. Similar policy updates in Germany and France added component-resolved diagnostics to statutory schedules. Expanded coverage empowers primary-care physicians to initiate testing instead of referring to overbooked specialists. Laboratories amortize fixed costs across higher throughput, and smaller regional labs are consolidating into accredited networks that meet payer turnaround benchmarks. Quality prerequisites, such as ISO 15189 certification, create a compliance floor favoring scale players.

Technological Shift to Fully Automated Multiplex Allergy Platforms

Laboratories are retiring manual ELISA workflows in favor of walk-away analyzers that integrate preparation, incubation, wash, and interpretation. Siemens Healthineers’ IMMULITE 2000 XPi now supports more than 500 allergen components, enabling component-level testing for mid-volume labs without dedicated technologists.[2]Siemens Healthineers, “Making Allergy Testing Routine,” siemens-healthineers.com HYCOR’s NOVEOS requires only 4 microliters per test and delivers 13 hours of unattended operation, slashing labor and redraw costs. AI-based software flags discordances and suggests reflex panels, reducing review workloads. Capital outlays of USD 150,000–300,000 are offset by lower consumable costs per result when labs process 50+ panels daily. Vendors offering reagent-rental models and leasing accelerate adoption.

Climate-Induced Lengthening of Pollen Seasons

Rising temperatures and atmospheric CO₂ have lengthened pollen seasons by 20–30 days in temperate zones, elevating cumulative exposure and sustaining continuous demand for allergy diagnostics. In North America, ragweed now sheds into November, overlapping mold peaks and complicating differential diagnosis. Laboratories in affected states report 15–20% test-volume uplifts, especially for panels spanning multiple pollen families. Longer seasons spur demand for baseline profiling before immunotherapy and for periodic monitoring to measure desensitization. Geographic migration of plants such as Ambrosia artemisiifolia into new latitudes generates naïve patient populations with heightened severity, further expanding the addressable base.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of trained allergists in emerging regions | –1.3% | Asia-Pacific (ex-Japan, South Korea), Middle East & Africa, Latin America | Long term (≥ 4 years) |

| High false-positive rates necessitating confirmatory tests | –0.9% | Global, extract-based assays in high pollen regions | Medium term (2-4 years) |

| Data-privacy hurdles for cloud-connected instruments | –0.7% | Europe, North America, evolving Asia-Pacific | Short term (≤ 2 years) |

| Plateauing birth rates curbing paediatric volumes in east Asia | –1.1% | Japan, South Korea, Taiwan, urban China | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Shortage of Trained Allergists in Emerging Regions

Emerging markets average an allergist-to-population ratio below 1:1 million, limiting access to skin-prick testing and specialist-guided immunotherapy. General practitioners increasingly rely on blood-based assays interpreted by standardized algorithms. Yet the workforce gap tempers uptake of advanced molecular panels because empirical treatment often substitutes for confirmatory testing. Government scholarship programs exist, but certification cycles of four plus years delay relief, keeping rural areas underserved and sustaining high unmet need.

High False-Positive Rates Necessitating Confirmatory Tests

Extract-based assays can yield 30–50% false positives among polysensitized patients, driven by cross-reactive carbohydrate determinants. Component-resolved diagnostics mitigate misclassification but carry higher reagent costs and inconsistent reimbursement. False positives erode clinician confidence and prompt empirical elimination diets that risk nutrition in children. Regulatory advisories recommend evidence-based testing only, yet enforcement varies, prolonging reliance on less precise methods.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Allergens: Food Panels Outpace Inhaled Despite Smaller Base

Food allergen panels accounted for a smaller revenue base in 2025 but are projected to expand at a 13.20% CAGR through 2031, eclipsing the growth of inhaled allergens, which held a 52.92% share. The FDA’s addition of sesame as the ninth major allergen triggered a 25% surge in sesame IgE orders during 2024. Component tests such as Ara h 2 and Cor a 14 pinpoint systemic-reaction risk, guiding emergency preparedness and immunotherapy candidacy. In contrast, inhaled allergen testing is approaching saturation in developed economies, although climate shifts keep absolute volumes high. Drugs, insect venom, and latex panels remain niche yet vital for occupational and perioperative safety.

The segment benefits from direct-to-consumer ordering portals that enable self-initiated food panels, which route samples to accredited labs. Still, extract methods carry a high false-positive burden, requiring oral food challenges for confirmation. Regulatory standards require at-home kits to meet CLIA rigor, elevating compliance costs for startups but improving quality parity with on-site draws. Allergy diagnostics market size growth will therefore continue to concentrate in molecular panels that command price premiums and deliver actionable granularity.

By Product & Service: Instruments Gain as Labs Automate

While consumables accounted for 61.74% of 2025 revenue, instruments are forecast to grow at a 12.35% CAGR as laboratories automate. Automated chemiluminescence and fluorescence analyzers improve reproducibility and throughput, converting one-time capital into recurring demand for assay cartridges. Larger reference networks bundle reagent rental agreements that distribute expenses over test volumes, accelerating fleet upgrades. The shift to component-resolved diagnostics lifts average reagent selling prices, reinforcing consumables' dominance within the allergy diagnostics market.

Software and services, though currently the smallest slice, are expanding fastest as laboratories integrate cloud middleware and AI analytics with electronic health records. Vendors charge subscription fees for decision-support dashboards that flag cross-reactive patterns and suggest reflex panels, turning data stewardship into an additional revenue pillar. ISO 15189 reaccreditation cycles stimulate demand for external quality-assessment programs and calibration materials.

By Test Type: In Vitro Assays Close Gap via Tele-Immunology

In vitro assays are advancing at a 13.25% CAGR, closing the gap with in vivo modalities, which still account for 54.98% of usage. Serum-based methods avoid antihistamine washouts and are suitable for patients with severe eczema, broadening eligibility. Multiplex microarrays capable of detecting 16+ allergens from a single blood spot enhance patient comfort and laboratory efficiency. Conversely, radioallergosorbent tests are being phased out due to the burdens associated with isotope handling.

Skin-prick and intradermal tests remain rapid and sensitive when performed by trained staff, but the global shortage of allergists caps expansion in emerging economies. Point-of-care lateral-flow strips for common inhaled allergens shorten visits to under 30 minutes, a boon for primary-care uptake, yet sensitivity gaps versus laboratory immunoassays persist. The allergy diagnostics market share for in vitro diagnostics will therefore continue to rise as tele-immunology and reimbursement favor blood-based workflows.

By End User: Primary Care Gains as Point-of-Care Devices Simplify Workflows

Diagnostic laboratories accounted for 44.62% of revenue in 2025, yet physician offices and primary-care clinics are projected to record the fastest 13.90% CAGR through 2031. Medicare’s broader reimbursement for in-office IgE panels removes financial friction, allowing family physicians to diagnose rather than refer. Despite this, a 2024 Medscape audit found that fewer than 10% of asthma patients received allergen testing, underscoring the latent upside. Hand-held analyzers that deliver results during the same consultation support shared decision-making and early intervention.

Reference labs retain scale advantages in multiplex panels that require specialized hardware and rigorous quality management. Eurofins added 23 blood-collection points and 18 laboratories during 2024 to capture decentralized demand and cross-sell allergy profiles. Emergency departments remain a smaller yet high-acuity niche, relying on rapid IgE tests to inform anaphylaxis treatment. Academic centers push the innovation frontier by validating novel biomarkers, feeding pipeline growth.

Geography Analysis

Asia-Pacific will generate the fastest 13.75% CAGR through 2031, while North America held 37.68% of the allergy diagnostics market share in 2025. China’s expansion of tertiary hospitals into mid-tier cities stimulates the purchase of instruments and broader access to component-resolved diagnostics. India leverages general practitioners to order serum panels, avoiding specialist bottlenecks and propelling volume even amid workforce scarcity. Japan and South Korea face headwinds from sub-0.8 fertility rates, trimming pediatric cohorts, yet vendors pivot to adult-onset food allergies and occupational panels.

Europe benefits from robust statutory reimbursement, with Germany and France reimbursing molecular panels since 2024. The United Kingdom’s NICE guidance endorses primary-care allergy testing, though budget constraints slow its widespread adoption. The Middle East and Africa are smaller but growing as Gulf states modernize their healthcare infrastructure; however, heterogeneous regulation and training gaps temper growth in lower-income nations. South America sees momentum in Brazil, where private networks partner with equipment vendors to expand menus, while Mexico’s expansion centers on urban private labs.

North America’s dominance arises from high health spending and entrenched automated platforms. FDA 2024 cybersecurity rules raise entry barriers, giving incumbents an edge through compliance expertise. Canada’s provincial payers reimburse IgE tests, expanding volumes, especially where allergist wait times exceed six months. Ragweed-driven pollen extensions into late autumn further intensify diagnostic demand, keeping test throughput high in U.S. laboratories.

Competitive Landscape

Market concentration is moderate, with global incumbents leveraging scale, proprietary allergen libraries, and service networks to defend share within the allergy diagnostics market. Thermo Fisher Scientific deepens its reach through exclusive United States distribution of AESKU’s immunofluorescence assays, enhancing portfolio breadth. The company also signals USD 40-50 billion of planned acquisitions, underscoring an aggressive expansion strategy that targets adjacencies across diagnostics.

Siemens Healthineers posts a 1.6% revenue increase in fiscal year 2025, driven by automated inflammation and allergy panels designed to optimize lab workflows. Its analyzers include built-in AI modules that flag cross-reactivity and recommend confirmatory tests, differentiating the offering in a competitive field. Danaher’s Beckman Coulter Life Sciences partners with InBio to improve basophil activation assays, reflecting a push toward higher-specificity confirmatory tests.

Emerging players such as AliveDx and Targeted Genomics introduce microarray and genomic panels for precision-medicine use cases, while ALK expands its device lines for skin testing following FDA clearances. Competitive intensity is thus increasing, yet barriers remain high due to the need for extensive allergen libraries, validation data, and global regulatory compliance.

Smaller firms chip away at niches, point-of-care cartridges, AI-augmented interpretation, or regional allergen panels, often collaborating with larger companies for distribution. The ecosystem trend favors platform approaches that bundle instruments, reagents, software, and service contracts into unified solutions, raising switching costs for laboratories.

Allergy Diagnostics Industry Leaders

BioMerieux SA

Siemens Healthineers AG

Omega Diagnostics Group PLC

Danaher Corp. (Beckman Coulter Diagnostics)

Thermo Fischer Scientific Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Novartis has finalized an agreement to acquire Excellergy, a US-based biotechnology company focused on food allergies, in a transaction valued at up to USD 2 billion. This acquisition enhances Novartis's portfolio of advanced anti-IgE therapies. The deal enables Novartis to leverage the success of its drug Xolair and strengthen its position in the food allergy market and other IgE-mediated disease segments.

- March 2026: Eurofins Viracor launched the ExPeCT anti-CD19 (obe-cel) CAR T-cell assay. This innovative solution enables clinicians to effectively monitor the performance of CAR T-cell therapy with validated accuracy and rapid turnaround times for results.

- September 2025: Regeneron Pharmaceuticals, Inc. reported positive results from Phase 3 trials of its investigational allergen-blocking antibodies in adults with moderate-to-severe cat or birch allergies. Both trials achieved their primary and key secondary objectives. The data will be presented at an upcoming medical conference to inform confirmatory Phase 3 trials.

Global Allergy Diagnostics Market Report Scope

As per the scope of the report, allergy diagnostics are processes performed in clinical conditions in which a harmless external agent is suspected to have a pathological effect on a human being, thus causing discomfort. The diagnostic procedure for allergies depends on the type of allergens and the mode of transmission.

The allergy diagnostics market is segmented by allergen type into inhaled allergens, food allergens, and other allergens. By products, the market is segmented into instruments, consumables, and luminometers. By test type, the market is segmented into in vivo tests and in vitro tests. By end users, the market is segmented into diagnostic laboratories, hospitals, and other end users. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle-East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers market size and forecasts in value (USD) for the above segments.

| Inhaled Allergens |

| Food Allergens |

| Drug Allergens |

| Insect Venom Allergens |

| Latex Allergens |

| Others |

| Instruments | Automated Immunoassay Analysers |

| Luminometers | |

| Microarray Platforms | |

| Consumables | Assay Kits and Reagents |

| Controls and Calibrators | |

| Ancillary Supplies | |

| Software and Services |

| In Vivo Tests | Skin-Prick Tests |

| Patch Tests | |

| Intradermal Tests | |

| In Vitro Tests | ELISA / ImmunoCAP |

| Radioallergosorbent Tests | |

| Multiplex Microarray/Component-Resolved Diagnostics |

| Diagnostic Laboratories |

| Hospitals & Emergency Departments |

| Physician Offices & Primary Care Settings |

| Academic & Research Institutes |

| Direct-to-Consumer/Home Testing Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Allergens | Inhaled Allergens | |

| Food Allergens | ||

| Drug Allergens | ||

| Insect Venom Allergens | ||

| Latex Allergens | ||

| Others | ||

| By Product & Service | Instruments | Automated Immunoassay Analysers |

| Luminometers | ||

| Microarray Platforms | ||

| Consumables | Assay Kits and Reagents | |

| Controls and Calibrators | ||

| Ancillary Supplies | ||

| Software and Services | ||

| By Test Type | In Vivo Tests | Skin-Prick Tests |

| Patch Tests | ||

| Intradermal Tests | ||

| In Vitro Tests | ELISA / ImmunoCAP | |

| Radioallergosorbent Tests | ||

| Multiplex Microarray/Component-Resolved Diagnostics | ||

| By End-User | Diagnostic Laboratories | |

| Hospitals & Emergency Departments | ||

| Physician Offices & Primary Care Settings | ||

| Academic & Research Institutes | ||

| Direct-to-Consumer/Home Testing Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is the allergy diagnostics market expected to grow through 2031?

The market is projected to advance at an 11.25% CAGR between 2027 and 2031, rising from USD 7.06 billion in 2026 to USD 12.04 billion by 2031.

Which allergen segment is expanding most quickly?

Food allergen panels are forecast to post the highest 13.20% CAGR, driven by regulatory labeling mandates and rising anaphylaxis incidence.

Why are in vitro assays gaining share over in vivo procedures?

Broader reimbursement, tele-immunology convenience, and multiplex microarrays that require only a single blood draw are narrowing the historical volume gap.

What is driving instrument sales within the allergy diagnostics space?

Laboratories are automating manual workflows with walk-away analyzers that reduce labor costs and offer component-resolved testing at scale, yielding a 12.35% CAGR for instruments.

Which region is poised for the strongest growth?

Asia-Pacific is projected to log a 13.75% CAGR through 2031 as investments in diagnostic infrastructure and urbanization-linked allergen exposure rise.

How concentrated is the competitive landscape?

The top five players hold roughly 55.60% of global revenue, indicating moderate concentration but ample opportunity for regional specialists and AI-focused newcomers.

Page last updated on: