Market Overview

| Study Period | 2021 - 2031 |

|---|---|

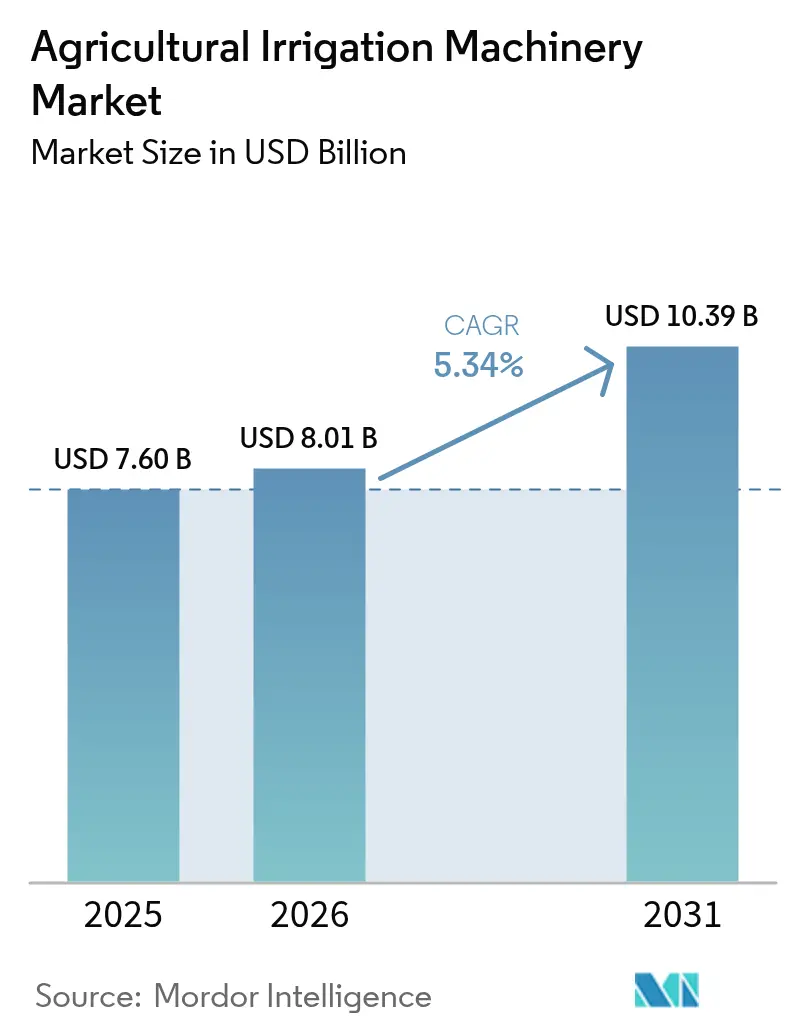

| Market Size (2026) | USD 8.01 Billion |

| Market Size (2031) | USD 10.39 Billion |

| Growth Rate (2026 - 2031) | 5.34% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Agricultural Irrigation Machinery Market Analysis by ���ϲ�����

The agricultural irrigation machinery market size was valued at USD 7.60 billion in 2025 and estimated to grow from USD 8.01 billion in 2026 to reach USD 10.39 billion by 2031, at a CAGR of 5.34% during the forecast period (2026-2031). Demand is focusing on equipment that integrates water-use efficiency with digital compliance reporting, driving changes in capital spending priorities faster than traditional subsidy cycles. State-level water-reporting mandates in California and Arizona are accelerating sensor adoption, while India’s micro-irrigation grants are compressing grower payback horizons from five years to less than three. Pivot upgrades dominate in North American grain belts, but fragmented holdings across Asia-Pacific are steering growers toward modular drip kits. Patent activity in variable-rate irrigation doubled after 2024, confirming that manufacturers see zone-specific delivery as the next competitive battleground.

Key Report Takeaways

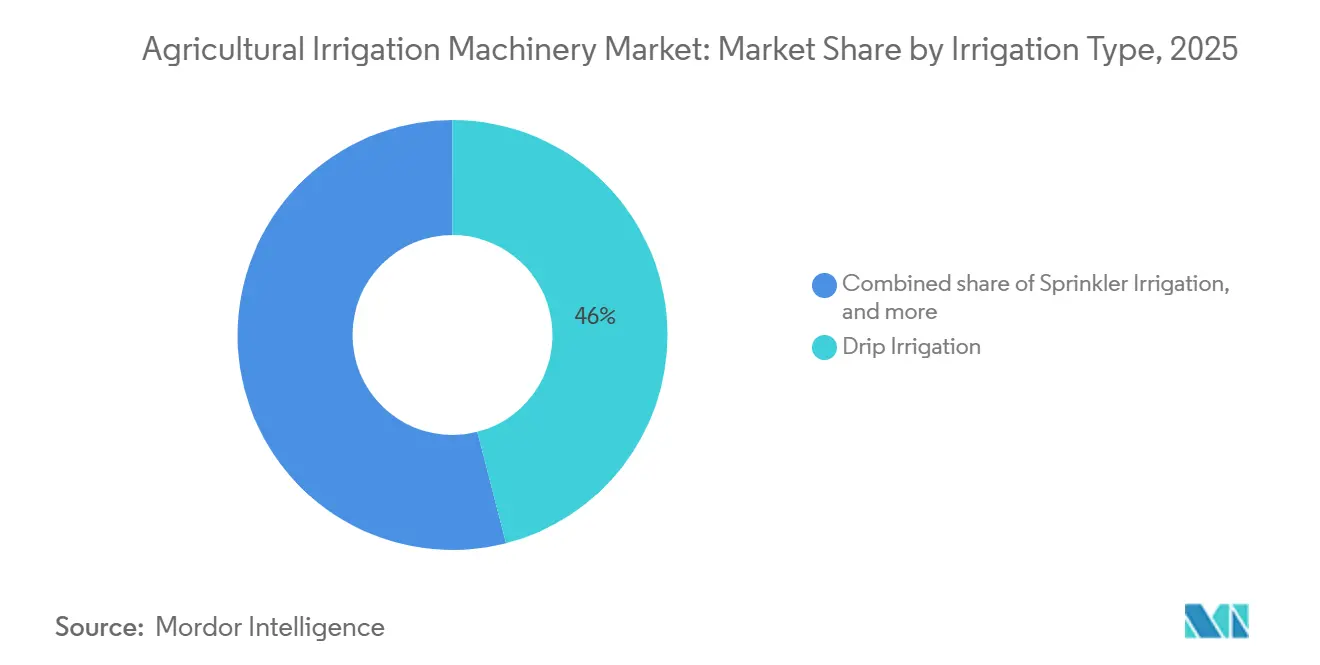

- By irrigation type, drip irrigation held the largest segment, accounting for 46.0% of the agricultural irrigation machinery market share in 2025, while sprinkler irrigation is the fastest-growing segment, projected to advance at an 8.0% CAGR through 2031.

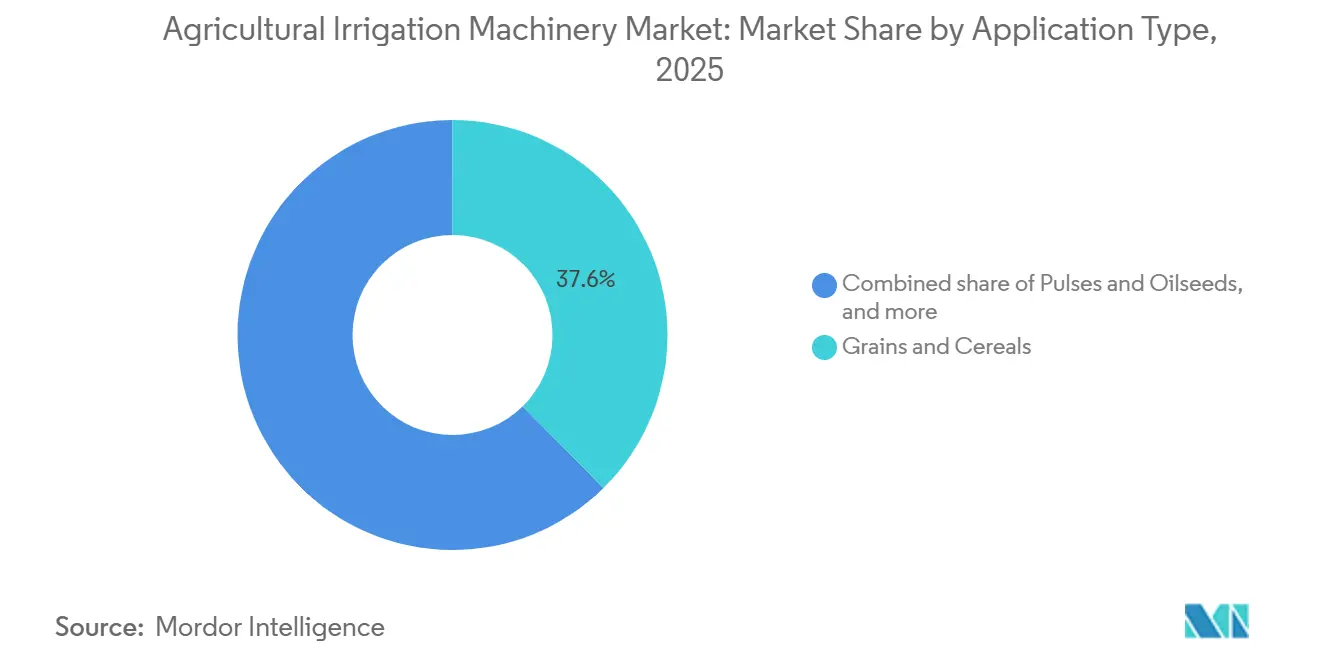

- By application, grains and cereals held the largest share, 37.6%, of the agricultural irrigation machinery market size in 2025, while fruits and vegetables are the fastest-growing segment, projected to expand at a 9.4% CAGR to 2031.

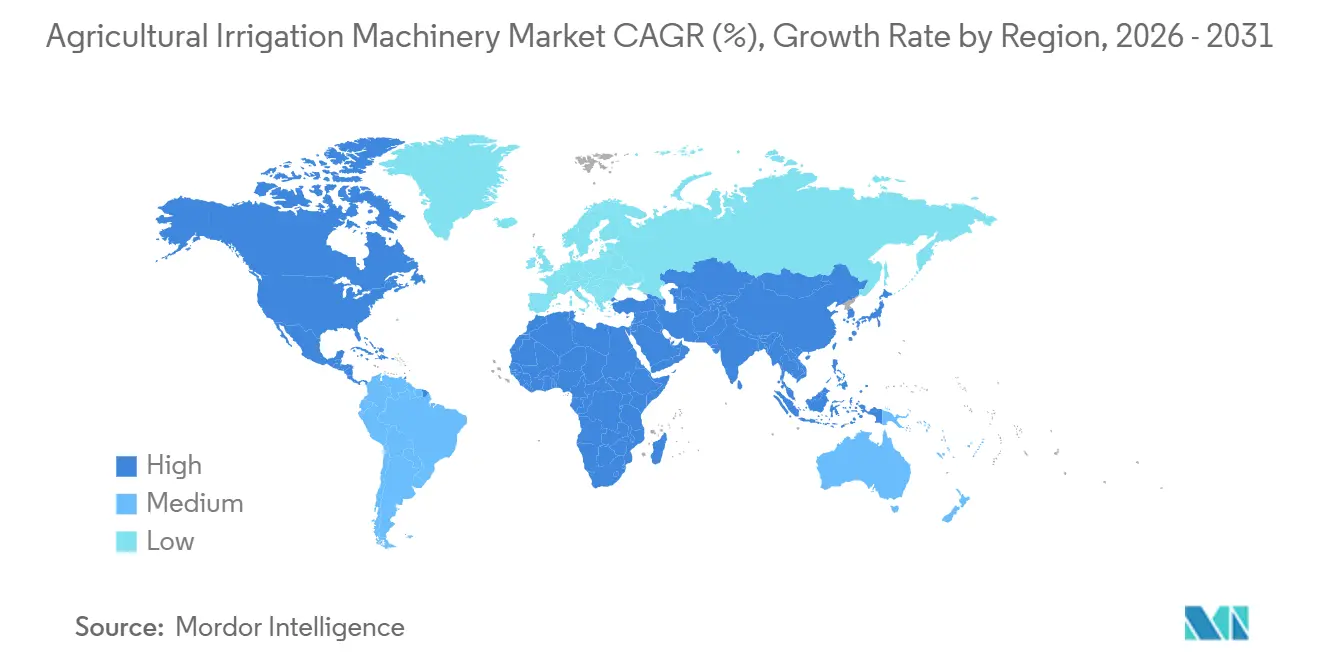

- By geography, North America was the largest region with 32.1% in 2025, and Asia-Pacific is set to log the fastest-growing regional CAGR at 8.0% through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Agricultural Irrigation Machinery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government subsidies for micro-irrigation adoption | +2.1% | Asia-Pacific core, spillover to Middle East and Africa | Medium term (2-4 years) |

| Rising water scarcity is pushing demand for precision irrigation | +2.5% | Global, with peak intensity in Middle East, North Africa, and California | Long term (≥4 years) |

| Labor shortages are accelerating the mechanization of mid-size farms | +1.8% | North America and Europe, and emerging in Asia-Pacific | Short term (≤2 years) |

| Integration of IoT sensors enabling pay-as-you-grow service models | +1.2% | North America and Europe are early adopters, and Asia-Pacific is following | Medium term (2-4 years) |

| Environmental, Social, and Governance (ESG)-linked finance rewarding water-efficiency investments | +0.9% | Europe and North America, and with selective uptake in the Asia-Pacific | Long term (≥4 years) |

| Surge in carbon-credit schemes for water-saving technologies | +0.7% | Global, with the highest activity in voluntary carbon markets | Long term (≥4 years) |

| Source: ���ϲ����� | |||

Government Subsidies for Micro-irrigation Adoption

Increased federal conservation funding has made upfront costs more manageable for medium-scale growers. In fiscal year 2024, the United States Department of Agriculture (USDA) Environmental Quality Incentives Program covered up to 75% of system expenses to efficiency initiatives upgrades[1]Source: USDA Natural Resources Conservation Service, “Environmental Quality Incentives Program,” USDA.GOV. The multi-year guarantees provided by the Inflation Reduction Act encourage manufacturers to expand production capacity, while outcome-based metrics align vendor offerings with policy objectives. The program's focus on measurable water-saving outcomes aligns with manufacturers' precision agriculture capabilities, offering a competitive advantage for technology-integrated solutions. These incentives have sparked significant annual order growth among emitter suppliers, signaling durable tailwinds for the agricultural irrigation machinery market.

Rising Water Scarcity Pushing Demand for Precision Irrigation

Mandatory reporting is replacing voluntary conservation, making sensor-equipped systems indispensable. The economic considerations extend beyond water costs to encompass regulatory compliance, as many jurisdictions enforce stricter water-use reporting requirements. The precision irrigation systems' ability to deliver detailed consumption analytics makes them essential tools for compliance rather than optional efficiency enhancements. Coupled with field trials, water savings from subsurface drip Evapotranspiration (ET) replacement, the evidence base now supports both agronomic and regulatory value propositions.

Labor Shortages are Accelerating the Mechanization of Mid-size Farms

Rising wages are forcing 50- to 200-hectare operations to automate or exit. According to the Food and Agriculture Organization of the United Nations, notes that automation reduces low-skilled jobs but increases demand for technicians who can manage sensor networks. A 2026 farmdocdaily study links precision-ag adopters with higher technician wages, illustrating a skill shift rather than a job drain. Equipment-sharing cooperatives in France, Germany, and the United States Midwest are amortizing pivot costs, expanding the agricultural irrigation machinery industry among growers previously priced out.

Integration of IoT Sensors Enabling Pay-as-You-Grow Service Models

Leasing bundles reduce upfront capital and align cash outflows with harvest inflows. Trimble’s fertigation controllers tie water and nutrient delivery to real-time crop data, cutting energy and carbon intensity in Chinese pilots. Subscription fees per hectare simplify accounting and attract tenant farmers, widening the addressable pool for the agricultural irrigation machinery market. The transition from capital expenditure to operating expense simplifies accounting and tax processes, increasing the appeal of precision irrigation for farm managers operating within corporate ownership structures.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront capital cost for pivot systems | -1.4% | Global, with peak impact in developing markets | Short term (≤2 years) |

| Fragmented land holdings limiting equipment Return on investment (ROI) in developing countries | -1.2% | Asia-Pacific and Africa, with minimal impact in North America and Europe | Long term (≥4 years) |

| Growing concern over plastic waste from drip lines | -0.6% | Europe and North America, emerging in the Asia-Pacific | Medium term (2-4 years) |

| Cyber-vulnerability of connected irrigation networks | -0.4% | North America and Europe early, Asia-Pacific, and the Middle East | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

High Upfront Capital Cost for Pivot Systems

Center pivots surpass USD 100,000 per unit, and installation can add another 30%, creating a financing gap that traditional credit seldom fills. Leasing uptake is under 15% because residual values remain opaque, especially in markets lacking secondary equipment exchanges. The capital barrier is also driving interest in hybrid systems that combine pivot infrastructure with drip laterals, allowing growers to phase investment over multiple growing seasons while maintaining flexibility to adjust coverage area as land tenure stabilizes. These systems enable growers to spread investments across multiple growing seasons while retaining the flexibility to modify coverage areas as land tenure becomes more stable. Additionally, hybrid systems offer a scalable approach, allowing farmers to gradually expand irrigation coverage without committing to the full cost upfront, making them a more viable option for resource-constrained growers.

Growing Concern over Plastic Waste from Drip Lines

The European Union updated its Single-Use Plastics Directive in 2024, compelling manufacturers to trial biodegradable polyethylene and to implement take-back schemes to achieve 50% waste reduction by 2027 [2]Source: European Commission, “Single-Use Plastics Directive,” environment.ec.europa.eu. The directive also emphasizes the need for innovation in material science and waste management practices, pushing manufacturers to invest in research and development to meet the new standards. Additionally, the policy aims to foster collaboration between stakeholders, including governments, manufacturers, and consumers, to ensure effective implementation and long-term sustainability.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Irrigation Type: Precision-Drip Captures Regulatory Tailwinds

Drip irrigation held the largest share, accounting for 46.0% of the agricultural irrigation machinery market in 2025, well above the market average. Drip irrigation's market growth is supported by California's reporting regulations favoring metered delivery and India's subsidies for emitters, tubing, and filters. The agricultural irrigation machinery market for drip irrigation components is anticipated to expand, fueled by increasing demand for moisture sensors and variable-rate controllers. While emitters and tubing continue to generate the majority of revenue, sensors represent the fastest-growing segment as farms transition from uniform to data-driven irrigation scheduling.

Sprinkler irrigation is the fastest-growing segment, projected to advance at an 8.0% CAGR through 2031, while mature dealer networks help preserve volumes, new sales skew toward variable-rate configurations that integrate soil probes and flow meters. Field trials in the United States Midwest show 15%-25% water cutbacks without yield loss when pivots shift from fixed to variable-rate application [3]Source: USDA Agricultural Research Service, “Variable-Rate Pivot Trials,” ars.usda.gov. Component innovation focuses on quick-connect couplers and self-cleaning filters, trimming installation labor by 30%-40%. Other methods, such as surface and furrow, are slipping below 10% combined share as water-scarcity policies tighten.

By Application Type: Premium Crops Drive Technology Adoption

Grains and cereals held the largest share, 37.6%, of the agricultural irrigation machinery market in 2025. Demand favors cost-per-hectare economics, which continues to anchor sprinkler volumes. The disparity highlights varying economic dynamics, as specialty crop producers achieve higher returns per acre, which justify investments in advanced irrigation systems.

Fruits and vegetables are the fastest-growing segment, projected to expand at a 9.4% CAGR to 2031. High farm-gate prices justify precision drip irrigation, enabling deficit irrigation strategies that increase sugar content in grapes and improve berry uniformity. Spain’s digital-twin trial produced 26% water savings in vegetables by linking irrigation timing to real-time soil moisture. Manufacturers are rolling out crop-specific emitters and algorithmic scheduling services, monetizing agronomic expertise as a differentiator. The agricultural irrigation machinery market share linked to horticulture is therefore projected to climb incrementally by 2031.

Geography Analysis

North America was the largest region, with 32.1% in 2025. Upgrades dominate because most irrigable acreage is already networked with pivots. Compliance mandates such as California’s Senate Bill 88 fuel retrofits that integrate flow meters and telemetry. Arizona’s grants are bridging the capital gap for sensor add-ons, sustaining pivot margins even as unit volumes plateau. Canada’s Prairie Provinces and Mexico’s Bajío region offer incremental growth but still account for only a fraction of the United States' demand.

Asia-Pacific is set to log the fastest-growing regional CAGR at 8.0% through 2031. Smallholder fragmentation means modular drip kits priced under USD 800 per hectare outsell large pivots by 4:1. Japan’s greenhouse boom is another tailwind, driving demand for high-pressure drip and fertigation controllers that command premium margins in the agricultural irrigation machinery market.

Europe is experiencing steady growth under the environmental pillar of the Common Agricultural Policy, which recognizes precision irrigation as a sustainable activity eligible for green financing. In the Mediterranean region, recurring droughts are accelerating the adoption of subsurface irrigation systems, while countries like the Netherlands and Germany focus on closed-loop greenhouse irrigation systems. In the Middle East and Africa, demand is driven by state-supported megafarms and climate-smart agricultural corridors. Meanwhile, South America's soybean-producing regions are investing in pivot irrigation systems to mitigate rainfall variability, contributing to a geographically diversified revenue stream within the agricultural irrigation machinery market.

Competitive Landscape

The agricultural irrigation machinery market is consolidated, with key players including The Toro Company, Lindsay Corporation, Valmont Industries, Inc. (Valley Irrigation), Netafim Ltd. (Orbia Advance Corporation), and Jain Irrigation Systems Limited (Rivulis Irrigation Limited). Netafim Ltd. utilizes agronomic advisory services to secure multi-season contracts, while Lindsay Corporation focuses on expanding its FieldNET analytics platform to encourage subscription renewals. Valmont Industries, Inc.’s Q1 2025 results highlight a shift toward software-enabled margin resilience, even as unit volumes stabilize in the North American market.

New entrants are targeting high-growth areas such as AI-guided scheduling and low-pressure drip tapes designed for smallholders. Patent filings are increasingly centered on sensor fusion and water-use algorithms, driving accelerated innovation cycles. Environmental, Social, and Governance (ESG) criteria are influencing procurement decisions, with preference given to companies offering recycling programs and transparent supply chains. Manufacturers that combine hardware reliability with integrated digital ecosystems are strengthening their competitive positions in the agricultural irrigation machinery market.

Cybersecurity has become a strategic priority as connected irrigation systems present potential vulnerabilities. Vendors are investing in encrypted communication protocols and remote firmware updates to address the concerns of risk-averse growers. Certification under programs such as the Environmental Protection Agency (EPA) WaterSense enhances access to subsidy opportunities, further supporting brand loyalty. Overall, established players that transition to full-stack solutions are better positioned to outperform competitors relying solely on mechanical offerings.

Agricultural Irrigation Machinery Industry Leaders

The Toro Company

Lindsay Corporation

Valmont Industries, Inc. (Valley Irrigation)

Netafim Ltd. (Orbia Advance Corporation)

Jain Irrigation Systems Limited (Rivulis Irrigation Limited)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Netafim USA, headquartered in Fresno, has introduced its FlexNet Medium Pressure Pipes, aiming to enhance the efficiency, durability, and reliability of water distribution. Unlike conventional lay-flat irrigation pipes, which are susceptible to leaks and require intensive labor for installation, FlexNet offers farmers a 20-30% reduction in labor costs and significantly reduces installation time.

- January 2025: Valley Irrigation consolidated multiple technology brands into the unified AgSense 365 platform, creating integrated data flows between pivot control, soil monitoring, and crop analytics. The platform integration enables predictive maintenance services and yield optimization capabilities that support recurring revenue generation.

- November 2024: NetafimLtd. Italia acquired precision irrigation specialist Tecnir S.r.l. to strengthen technical capabilities and expand market reach in Southern European markets. The acquisition adds specialized expertise in horticultural irrigation applications and enhances service capabilities for premium crop producers.

Global Agricultural Irrigation Machinery Market Report Scope

Irrigation machinery used to supply water to agricultural land and crops to promote hydration and growth is categorized as an agricultural irrigation system. The Agricultural Irrigation Machinery Market Report is Segmented by Irrigation Type (Sprinkler Irrigation, Drip Irrigation, Pivot Irrigation, and Other Irrigation Types), by Application Type (Grains and Cereals, Pulses and Oilseeds, Fruits and Vegetables, and Other Applications), and by Geography (North America, Europe, Asia-Pacific, South America, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

By Irrigation Type

| Sprinkler Irrigation | Pumping Unit |

| Tubing | |

| Couplers | |

| Spray or Sprinkler Heads | |

| Fittings and Accessories | |

| Sensors | |

| Controllers | |

| Injectors | |

| Flow Meters | |

| Drip Irrigation | Valves |

| Backflow Preventers | |

| Pressure Regulators | |

| Filters | |

| Emitters | |

| Tubing | |

| Other Drip Irrigation Components | |

| Pivot Irrigation | |

| Other Irrigation Types |

By Application Type

| Grains and Cereals |

| Pulses and Oilseeds |

| Fruits and Vegetables |

| Other Applications |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Netherlands | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Cambodia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Peru | |

| Rest of South America | |

| Middle East | Saudi Arabia |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Irrigation Type | Sprinkler Irrigation | Pumping Unit |

| Tubing | ||

| Couplers | ||

| Spray or Sprinkler Heads | ||

| Fittings and Accessories | ||

| Sensors | ||

| Controllers | ||

| Injectors | ||

| Flow Meters | ||

| Drip Irrigation | Valves | |

| Backflow Preventers | ||

| Pressure Regulators | ||

| Filters | ||

| Emitters | ||

| Tubing | ||

| Other Drip Irrigation Components | ||

| Pivot Irrigation | ||

| Other Irrigation Types | ||

| By Application Type | Grains and Cereals | |

| Pulses and Oilseeds | ||

| Fruits and Vegetables | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Netherlands | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Cambodia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Peru | ||

| Rest of South America | ||

| Middle East | Saudi Arabia | |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the agricultural irrigation machinery market in 2031?

The agricultural irrigation machinery market was valued at USD 7.60 billion in 2025 and estimated to grow from USD 8.01 billion in 2026 to reach USD 10.39 billion by 2031, at a CAGR of 5.34% during the forecast period (2026-2031).

Which irrigation type is growing fastest?

Sprinkler irrigation is the fastest-growing segment, projected to advance at an 8.0% CAGR through 2031.

What policy is driving sensor adoption in California?

Senate Bill 88, effective October 2025, requires diversion measurement and reporting, boosting demand for sensor-equipped systems.

How do pay-as-you-grow models affect capital cost?

Leasing bundles that include IoT sensors reduce upfront expenditure by 40% to 60%, making precision irrigation accessible to cash-constrained growers.

Page last updated on: