Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

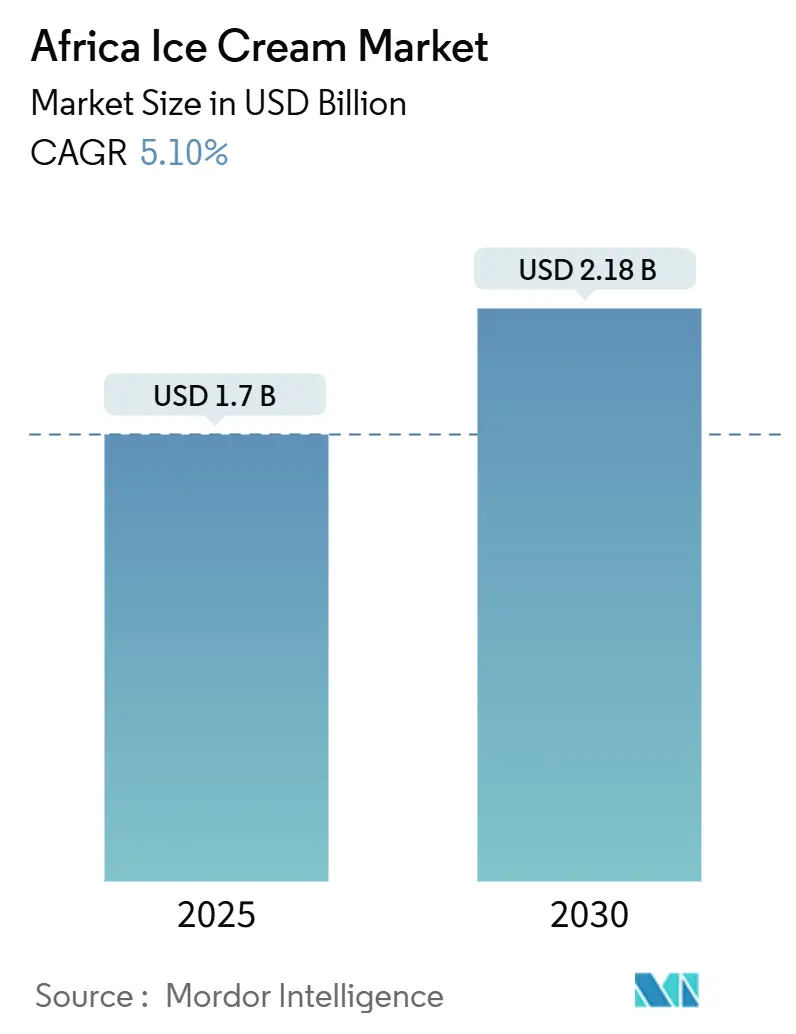

| Base Year Market Size (2025) | USD 1.7 Billion |

| Market Size (2026) | USD 1.79 Billion |

| Market Size (2031) | USD 2.29 Billion |

| Growth Rate (2026 - 2031) | 5.07% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. |

|

Africa Ice Cream Market Analysis by ���ϲ�����

The Africa Ice Cream Market size is expected to grow from USD 1.70 billion in 2025 to USD 1.79 billion in 2026 and is forecast to reach USD 2.29 billion by 2031 at 5.07% CAGR over 2026-2031. Urban household incomes are rising fastest in Nigeria, Kenya, and Ghana, prompting a shift from unbranded frozen desserts toward packaged products stocked in supermarkets and neighborhood kiosks. Organized retail expansion by chains such as Shoprite and Carrefour is widening cold-chain coverage and shelf visibility for leading brands. A median population age of 19 years is expanding the impulse-buyer base that favors single-serve treats and digital marketing touchpoints. Capital investments by Unilever, Nestlé, and regional producers are modernizing production lines and freezer fleets, although fragmented rural logistics and erratic milk supply continue to compress margins in price-sensitive segments

Key Report Takeaways

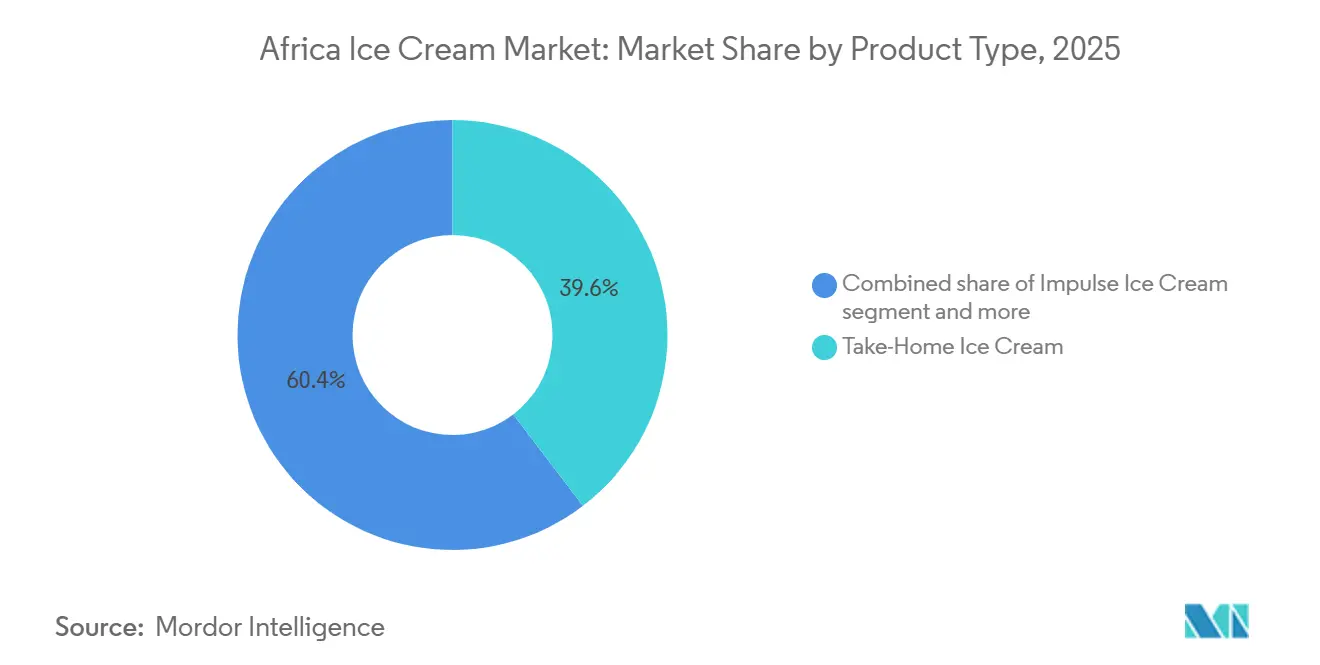

- By product type, take-home packs captured 39.61% share of the Africa Ice Cream Market size in 2025; artisanal formats are poised to expand at a 6.82% CAGR to 2031.

- By flavor, chocolate accounted for 48.77% share of the African ice cream market size in 2025, whereas fruit-based variants are advancing at a 7.05% CAGR to 2031.

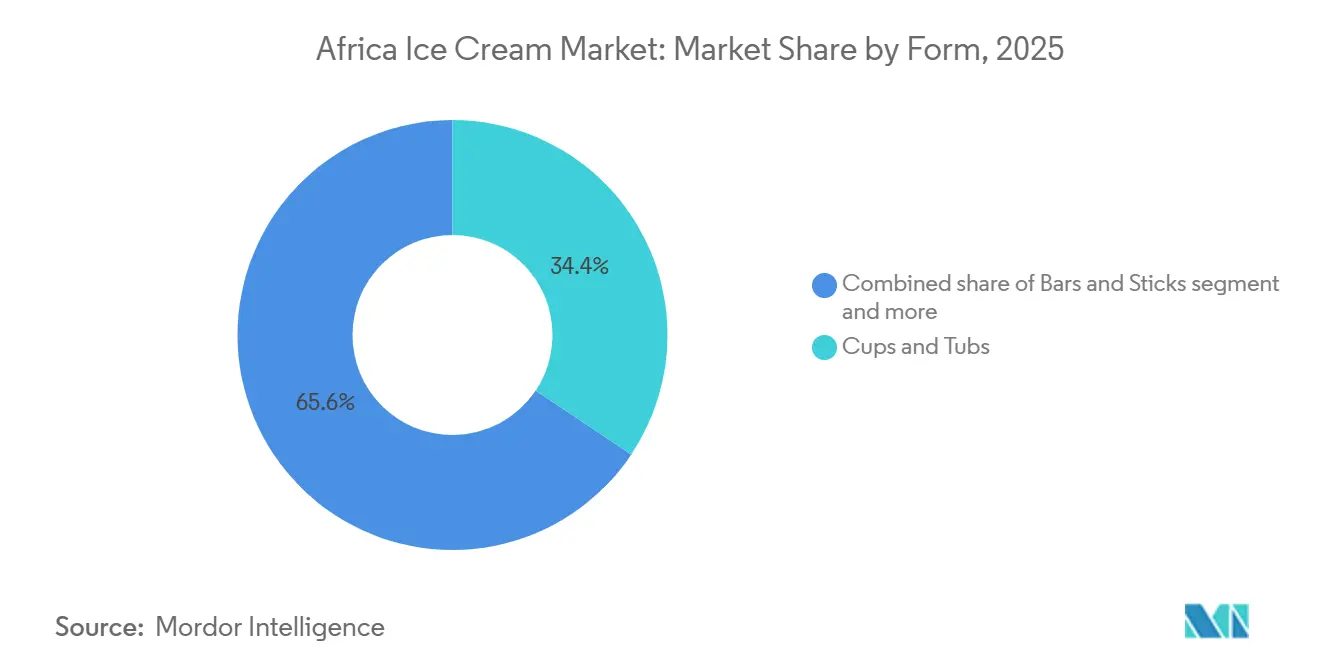

- By form, cups and tubs held 34.38% share of the Africa Ice Cream Market size in 2025, and bars and sticks are forecast to post the fastest 7.10% CAGR through 2031.

- By distribution channel, off-trade outlets commanded 41.59% share in 2025; on-trade venues are projected to grow at a 7.40% CAGR to 2031.

- By geography, South Africa led with 46.40% of the African ice cream market share in 2025, while Nigeria is projected to record the highest 6.76% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Africa Ice Cream Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strengthening household purchasing power in emerging urban clusters | +0.8% | Nigeria, Kenya, Ghana, Tanzania (urban corridors) | Medium term (2-4 years) |

| Proliferation of organized retail and supermarket chains | +0.7% | South Africa, Nigeria, Kenya (metro areas) | Short term (≤ 2 years) |

| Large youth demographic driving on-the-go indulgence | +0.6% | Africa-wide, concentrated in West and East Africa | Long term (≥ 4 years) |

| Heightened capital deployment by global and regional manufacturers | +0.5% | Nigeria, South Africa, Tanzania, Egypt | Medium term (2-4 years) |

| Adoption of solar-powered refrigeration in semi-urban and off-grid zones | +0.4% | Nigeria, Kenya, Tanzania, Ghana (peri-urban and rural) | Long term (≥ 4 years) |

| Micro-entrepreneurship and mobile distribution models | +0.3% | Nigeria, Ghana, Kenya, Tanzania (informal trade channels) | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Strengthening household purchasing power in emerging urban clusters

Rising employment and income security in emerging urban clusters across Africa are enhancing household purchasing power, driving demand for affordable indulgences such as ice cream and other FMCG products. The International Labour Organization reports that Africa’s employed population grew to approximately 529.4 million in 2024, up from 514 million in 2023, reflecting a steady increase in earners who are gradually shifting spending from basic staples to occasional treats [1]Source: International Labour Organization, “Statistics on Employment,” ilostat.ilo.org. This trend is encouraging companies to adapt their offerings by tailoring pack sizes and price points to suit constrained but improving household budgets. For instance, Unilever leverages single-serve products sold through informal kiosks, while local players like Bakhresa Group’s Azam Dairy in Tanzania utilize localized cold-chain networks to maintain affordability. As households gain regular wages, purchasing behavior diversifies, with consumers increasingly favoring modern trade channels and quick-service outlets. Brands such as Famous Brands’ Milky Lane promote family sharing through sit-in formats and take-home tubs, fostering higher basket sizes within budget constraints. This evolution in consumer behavior, combined with investments in distribution and retail partnerships, reduces inefficiencies and stabilizes pricing. As affordable quality becomes consistent, brand loyalty deepens, encouraging firms to innovate with new flavors and culturally relevant formats, further aligning with emerging middle-class aspirations.

Proliferation of organized retail and supermarket chains

The expansion of organized retail and supermarket chains is a key driver of structural growth in the ice cream market across Africa. Formal retail networks are improving product visibility, ensuring cold-chain reliability, and fostering consumer trust. The rise of hypermarkets and supermarkets in urban centers is shifting sales from informal kiosks to regulated retail environments, where consistent refrigeration safeguards product quality and enhances brand credibility. International retailers like Carrefour are accelerating this transformation by establishing outlets in high-growth cities, introducing modern freezer infrastructure to support a wider range of ice cream formats. Regional players such as Pick n Pay are strengthening private-label offerings and dedicating freezer aisles to ice cream, encouraging planned purchases during routine shopping trips. Premium positioning is further advanced by chains like Woolworths Holdings Limited, which focus on artisanal and higher-margin products appealing to brand-conscious consumers. Manufacturers, including FanMilk, benefit from structured distribution agreements and scalable access to urban markets through centralized procurement systems. Standardized merchandising, promotional cycles, and in-store sampling increase consumer exposure to new flavors and formats, driving trial and repeat purchases. Reliable cold storage, improved inventory management, and promotional bundling further enhance consumer confidence, elevating ice cream consumption patterns across Africa’s evolving retail landscape.

Large youth demographic driving on-the-go indulgence

The large youth demographic in Africa is a key driver of demand for on-the-go indulgence, as younger consumers increasingly favor impulse-based, convenience-oriented treats. As per Statistics South Africa in 2025, approximately 20.8 million individuals in South Africa are aged between 15 and 34 years, forming a significant consumer base with evolving lifestyles and snacking preferences [2]Source: Statistics South Africa, "Inside the Numbers: SA Population Trends for 2025," statssa.gov.za. This group’s association with urban mobility, socialization, and time spent outside the home fuels demand for portable, single-serve ice cream formats. Social media exposure to global food trends further shapes preferences for branded cones, sticks, and novelty products that align with experiential consumption. Quick-service restaurant chains, such as McDonald's, capitalize on this trend by integrating soft-serve and McFlurry-style desserts into affordable combo offerings, embedding ice cream into everyday dining occasions. Local manufacturers like Dairy Belle are innovating with vibrant packaging and youth-focused flavors to appeal to price-sensitive yet brand-conscious consumers. Peer influence, social outings, and digital visibility amplify impulse purchases, while youth-driven foot traffic in malls, transport hubs, and entertainment districts supports freezer placements in high-traffic retail outlets. This demographic shift is structurally expanding the on-the-go indulgence segment, embedding ice cream as a socially integrated and frequently consumed treat in urban areas.

Adoption of solar-powered refrigeration in semi-urban and off-grid zones

The integration of solar-powered refrigeration in semi-urban and off-grid areas is enhancing household purchasing power by ensuring reliable access to chilled products, such as ice cream, in regions with limited traditional power infrastructure. Supermarket chains are leveraging these solar units in peripheral kiosks to expand organized retail, minimize spoilage, and cater to the increasing demand for convenient, on-the-go products, particularly among younger demographics in South Africa. Companies like Koolboks are addressing this demand by providing pay-as-you-go solar freezers to street vendors in Nigeria, enabling them to keep products like FanMilk-style ice cream sticks fresh for mobile consumers. Similarly, Sokofresh's solar cold rooms in Kenya support small traders by offering reliable storage solutions, reducing waste, and integrating with supermarket logistics to meet family consumption needs while improving job stability. These advancements lower operational costs for micro-retailers, ensure consistent pricing, and foster consumer trust in emerging urban areas. The strategic placement of solar refrigeration units near transit hubs further capitalizes on youth mobility, converting foot traffic into regular purchases. By strengthening the cold chain and linking employment, retail growth, and demographic trends, solar-powered refrigeration is positioning ice cream as an accessible and dependable product in off-grid communities.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited cold-chain penetration in deep rural markets | -0.5% | Nigeria, Tanzania, Kenya, Ghana (rural and peri-urban zones) | Long term (≥ 4 years) |

| Fluctuating milk procurement costs and supply volatility | -0.4% | Kenya, Tanzania, Nigeria, South Africa (dairy-producing regions) | Short term (≤ 2 years) |

| Rising implementation of sugar taxation policies | -0.3% | South Africa (national), Kenya (under consideration) | Medium term (2-4 years) |

| Shift toward clean-label formulations increasing production costs | -0.2% | South Africa, Nigeria, Kenya (urban markets) | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Fluctuating milk procurement costs and supply volatility

Fluctuating milk procurement costs and supply volatility significantly impact the production economics and pricing strategies of ice cream manufacturers in Africa. Dairy remains a critical raw material, and its cost directly influences profitability. As reported by Milk South Africa, the average price of unprocessed milk in South Africa rose from ZAR 5.86 per litre in 2022 to ZAR 7.75 per litre in 2024, reflecting input cost inflation that compresses manufacturer margins [3]Source: Milk SA, "Lacto Data May 2025," milksa.co.za. This volatility complicates cost planning, making it challenging to maintain stable pricing without eroding profitability or passing higher costs to price-sensitive consumers. Companies like Clover Industries Limited, which are integrated with local dairy supply chains, are particularly exposed to farm-level price fluctuations that affect their frozen dessert portfolios. Rising procurement costs also limit promotional activities, reducing competitiveness in impulse-driven segments where affordability is essential. Furthermore, inconsistent milk supply due to climatic variability, feed costs, and farm-level challenges disrupts production schedules and increases reliance on spot-market sourcing. For manufacturers targeting urban and semi-urban markets, higher raw material costs restrict expansion into lower-income segments, where pricing sensitivity is acute. These combined factors narrow operating margins and intensify competition from non-dairy alternatives, creating structural challenges for scalability and long-term profitability.

Rising implementation of sugar taxation policies

The implementation of sugar taxation policies is increasingly impacting the ice cream industry in Africa, as governments strengthen public health measures to curb sugar consumption and address obesity. Fiscal tools, such as sugar levies, elevate production costs for manufacturers of sweetened products, forcing brands to either absorb these costs or pass them on to consumers, thereby affecting price competitiveness in mass-market segments. In markets like South Africa, health-promotion levies on sugar-sweetened products have driven manufacturers to reformulate products, reassess sugar content, and adjust positioning strategies. Premium brands, such as Ferrero’s Kinder ice cream, must balance consumer taste expectations with compliance pressures, often requiring the use of higher-cost alternative sweeteners or stabilizers, which increases research and development and production expenses. Higher retail prices due to taxation can also reduce impulse purchases, particularly among price-sensitive youth and lower-income households, which are key drivers of volume sales. The policy environment creates uncertainty for long-term investments, as manufacturers must anticipate potential tax expansions to other dessert categories. Smaller local producers face disproportionate challenges due to limited financial flexibility compared to multinational competitors. Collectively, these factors constrain pricing strategies, pressure margins, and necessitate reformulation, moderating growth momentum in the market.

Segment Analysis

By Product Type: Take-Home Dominance, Artisanal Acceleration

Take-home ice cream accounted for the largest share of 39.61% in 2025, driven by its strong alignment with household consumption patterns in Africa. Multi-liter tubs and family packs offer significant per-serving cost advantages, making them particularly appealing to multi-generational households that prioritize bulk purchases for shared consumption and effective budget management. Manufacturers such as Froneri focus on value-oriented tubs and larger formats to secure high-volume placements in supermarkets and neighborhood stores. This segment benefits from planned grocery shopping behaviors, with ice cream increasingly included in monthly or weekly baskets rather than being purchased impulsively. Impulse formats, including cones, bars, and sticks, cater to on-the-go demand but face margin pressures from informal vendors offering lower-priced alternatives. These dynamics position take-home ice cream as a critical volume driver, ensuring scale efficiencies and consistent turnover despite broader economic fluctuations.

Artisanal ice cream, while representing a smaller market share, is projected to grow at a 6.82% CAGR through 2031, reflecting increasing premiumization in metropolitan areas. Affluent consumers are willing to pay a premium for craft formulations and exotic flavors, highlighting a clear market divide. Value-driven households remain focused on bulk formats, while urban middle- and upper-income consumers seek differentiated taste experiences and perceived quality. Companies like Famous Brands leverage this trend through premium dessert concepts and café-linked offerings that emphasize indulgence, provenance, and experiential consumption. This dual-speed evolution compels manufacturers to balance high-volume affordability with high-margin exclusivity, showcasing the market's simultaneous growth across value and premium segments.

Note: Segment shares of all individual segments available upon report purchase

By Flavor: Chocolate Leads, Fruit Flavors Surge with Local Ingredients

Chocolate flavor held the largest market share at 48.77% in 2025, underscoring its widespread appeal and strong familiarity among African consumers across various age groups. This dominance reflects entrenched taste preferences, cultural acceptance, and its role as a reliable indulgence in both take-home and impulse purchase formats. Global brands such as Mars Incorporated leverage chocolate's popularity by extending their confectionery lines into ice cream, fostering brand loyalty and repeat purchases. Vanilla and strawberry flavors maintain secondary but stable positions, with vanilla valued for its versatility as a base for mix-ins, syrups, and toppings in family-sized tubs, while strawberry resonates strongly with children and female consumers in single-serve formats. These core flavors act as volume drivers, ensuring consistent sales and reducing demand fluctuations. Manufacturers rely on chocolate and vanilla to stabilize revenues while using them as platforms for innovations such as swirls, inclusions, and hybrid dessert concepts.

Fruit flavors are projected to grow at a 7.05% CAGR through 2031, driven by localization strategies and the use of indigenous African ingredients like baobab, mango, and hibiscus. These ingredients align with consumer preferences for authenticity and health-conscious options. The popularity of baobab ice-lollies and frozen juices in Malawi demonstrates strong consumer acceptance of fruit-based frozen desserts rooted in regional taste profiles. Companies such as Increda Ingredients support this trend by promoting locally sourced fruit inclusions, which enhance flavor differentiation and streamline supply chains. Fruit-based innovations appeal to younger, experimental consumers and enable premium pricing due to their perceived naturalness and functional benefits, creating a strategic balance between traditional and emerging flavors.

By Form: Cups and Tubs for Households, Bars and Sticks for Impulse

Cups and tubs held the largest market share at 34.38% in 2025, driven by their dominance in household consumption. These formats appeal to consumers seeking cost efficiency per serving and shared usage, particularly among multi-member families. Larger pack sizes align with value-oriented purchasing behavior, allowing for consumption over multiple occasions. This planned buying pattern, primarily through supermarkets and neighborhood grocery stores, ensures volume stability compared to the variability of impulse-driven sales. Cones, while representing a smaller share, cater to a niche segment focused on experiential consumption. Their customization and presentation justify premium pricing, with brands like Cold Stone Creamery in Nigeria leveraging waffle cones and personalized toppings to command higher margins and offset elevated labor and ingredient costs.

Bars and sticks are the fastest-growing format, with a projected CAGR of 7.10% through 2031. These single-serve products thrive in high-footfall locations such as street kiosks, school gates, transport hubs, and informal markets, where consumers prioritize immediate gratification. Their portability and ready-to-eat convenience make them particularly suitable for environments with limited refrigeration, such as vendor pushcarts or compact freezers. Players like Polar Ice Cream emphasize stick-based novelties and individually wrapped bars, catering to quick purchases and youth-oriented demand. The segment's growth is closely tied to urban commuting patterns and spontaneous snacking behavior, where affordability and accessibility outweigh bulk value considerations. Together, these formats illustrate a balanced market structure, with cups and tubs anchoring household demand, bars and sticks driving impulse growth, and cones enhancing premium experiential positioning.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Off-Trade Anchors Volume, On-Trade Captures Premiums

Off-trade channels held the largest market share of 41.59% in 2025, anchoring overall volume through supermarkets, hypermarkets, convenience stores, specialist shops, and emerging online retail platforms. Supermarkets and hypermarkets utilize dedicated freezer aisles and in-store promotions to drive trial and repeat purchases. Convenience stores and specialist outlets cater to quick top-up shopping needs, while online retail, though nascent, is gradually improving accessibility for tech-savvy consumers. Traditional trade, including mobile vendors and informal kiosks, remains a dominant volume driver in markets such as Nigeria, Ghana, and Kenya, highlighting the enduring importance of grassroots distribution. Companies like Unilever employ dual distribution strategies to balance high-margin modern trade presence with volume-driven traditional trade penetration, creating a complementary ecosystem that ensures scale and reach.

On-trade channels, including hotels, restaurants, cafes, and quick-service restaurants, are expanding at a CAGR of 7.40% through 2031, driven by tourism recovery and increasing urban middle-class dining-out frequency. These venues enable manufacturers to capture premium pricing, as consumers are willing to pay more for ice cream served in curated, experiential settings. Brands such as Cold Stone Creamery capitalize on this trend by offering artisanal cones, sundaes, and mix-ins that emphasize customization and indulgence, enhancing both brand prestige and profit margins. On-trade also serves as a platform for new product launches and flavor experimentation, allowing manufacturers to test market acceptance before scaling through retail channels. This segment’s growth is closely tied to urban lifestyle shifts, social dining trends, and tourism-led footfall, reinforcing its role in driving premiumization.

Geography Analysis

South Africa is expected to account for 46.40% of the market share in 2025, supported by its well-established retail infrastructure, advanced dairy processing capabilities, and relatively affluent consumer base. Vertically integrated companies, such as Lactalis South Africa, which produces ice cream under the Aylesbury brand in gelato and dairy-soft formats, ensure cost efficiency and consistent quality through controlled sourcing and processing. Supermarkets and hypermarkets act as key distribution channels, efficiently delivering household-sized tubs and family packs to multi-generational consumers. However, the Health Promotion Levy on sugar presents a structural challenge, driving reformulation toward lower-sugar variants. This shift increases production costs and may constrain volume growth in price-sensitive segments. The combination of sophisticated infrastructure and regulatory pressures positions South Africa as a market focused on both volume and premium offerings.

Nigeria is the fastest-growing market, with a projected CAGR of 6.76% through 2031. This growth is fueled by a youthful population, rapid urbanization, and a median age below 20 years, which supports demand for impulse and on-the-go frozen treats. Multinational operators like Nestlé, with three factories producing dairy and ice cream products, leverage local manufacturing to scale single-serve bars, sticks, and cones for urban and peri-urban consumers. Informal vendors, kiosks, and mobile carts complement formal distribution channels, particularly in high-footfall areas, fostering innovation in affordable and portable formats. These demographic advantages and urban mobility establish Nigeria as a critical market for volume expansion and youth-focused product strategies.

Kenya, Tanzania, and Ghana are emerging growth hubs, collectively contributing 5–8% of regional sales in 2025. Rising urban incomes and the expansion of organized retail drive growth in these markets. Companies like Azam Dairy in Tanzania utilize extensive beverage distribution networks and packaging capabilities to expand ice cream availability, while local brands such as Mihan Dairy in Ethiopia and King Cone Egypt cater to niche segments in smaller, fragmented markets across the Rest of Africa. This segmentation highlights a dual-market structure: mature markets like South Africa emphasize premiumization and regulatory-compliant innovation, fast-growing hubs like Nigeria focus on volume and youth-centric formats, and emerging markets in East and North Africa rely on local players and modern retail expansion to capture incremental growth.

Competitive Landscape

The Africa ice cream market is moderately consolidated, with multinational corporations operating alongside established regional players, resulting in a competitive and dynamic market environment. Companies such as Unilever, Danone, Nestlé, Froneri, and Clovers dominate premium and urban channels by introducing innovative flavors, fortified products, and artisanal formats. These offerings cater to urban middle-class and affluent consumers, enabling multinationals to maintain premium positioning and high-margin product portfolios. Their capital-intensive infrastructure and advertising efforts further strengthen their foothold in the market.

Regional players, including Brookside Dairy, Pearl Dairy, and Azam Dairy, maintain a strong presence by focusing on affordability, local flavors, and proximity to rural and semi-urban distribution networks. These companies effectively compete in price-sensitive segments by offering single-serve impulse products and leveraging their understanding of regional taste preferences. Markets such as Kenya, Uganda, and Tanzania highlight the importance of these strategies, where regional players capitalize on established supply chains and informal retail channels to drive growth.

The competitive landscape is shaped by the interplay between global and local players, creating a dual strategic approach. Multinational corporations prioritize premiumization, urban modern trade, and product diversification, while regional players emphasize affordability and localized offerings. For example, Unilever ensures consistent product availability through robust freezer networks in supermarkets, convenience stores, and online platforms. Meanwhile, Azam Dairy utilizes beverage distribution infrastructure to reach semi-urban and rural consumers. This balance between scale, innovation, and local expertise defines the moderately consolidated yet highly competitive nature of the Africa ice cream market, where strategic partnerships, dual-channel strategies, and product differentiation are critical for sustained growth.

Africa Ice Cream Industry Leaders

-

Nestlé S.A.

-

Unilever PLC

-

Danone S.A.

-

Froneri International Ltd

-

Clover Industries Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Food and Beverage company Bakhresa launched a second 100ml Azam Ice Cream range. This rollout was designed to offer portion-controlled packaging for consumers in the Tanzanian, Kenyan, and Zambian markets.

- December 2025: Cadbury Dairy Milk Hazelnut Ice Cream was offered in a multipack, intended for family gatherings, social occasions with friends, and other enjoyable moments.

- February 2025: Dairyland, a well-known Kenyan dairy and chocolate brand, introduced redesigned packaging for its ice cream tubs that combines modern aesthetics with functionality. The updated designs reflected the brand's focus on creativity while maintaining its commitment to quality.

Africa Ice Cream Market Report Scope

Ice cream is a frozen dessert made using milk, cream, and artificial or natural flavorings.

The Middle East & African ice cream market is segmented into product type, distribution channel, and geography. By product type, the market is segmented into impulse ice cream, take-home ice cream, and artisanal ice cream. Based on the distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores, specialist stores, online retail stores, and other distribution channels. Based on geography, the market includes major geographies across the region, South Africa, Saudi Arabia, the United Arab Emirates, and the Rest of the Middle East & Africa.

For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

By Product Type

| Impulse Ice Cream |

| Take-Home Ice Cream |

| Artisanal Ice Cream |

By Flavor

| Chocolate |

| Fruit |

By Form

| Cups and Tubs |

| Bars and Sticks |

| Cones |

By Distribution Channel

| On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Specialist Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

By Geography

| Nigeria |

| South Africa |

| Kenya |

| Tanzania |

| Ghana |

| Rest of Africa |

| By Product Type | Impulse Ice Cream | |

| Take-Home Ice Cream | ||

| Artisanal Ice Cream | ||

| By Flavor | Chocolate | |

| Fruit | ||

| By Form | Cups and Tubs | |

| Bars and Sticks | ||

| Cones | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Specialist Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | Nigeria | |

| South Africa | ||

| Kenya | ||

| Tanzania | ||

| Ghana | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the Africa Ice Cream Market?

The market stood at USD 1.70 billion in 2025 and is projected to reach USD 2.29 billion by 2031.

Which country leads regional sales?

South Africa held 46.40% of regional revenue in 2025 thanks to its advanced retail network and dairy processing base.

Which country will grow fastest to 2031?

Nigeria is forecast to post a 6.76% CAGR, fueled by rapid urbanization and a youthful population.

Which product segment shows the highest growth?

Bars and sticks are projected to expand at 7.10% CAGR through 2031 on the back of impulse street-vendor sales.

Page last updated on: