Acetaldehyde Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

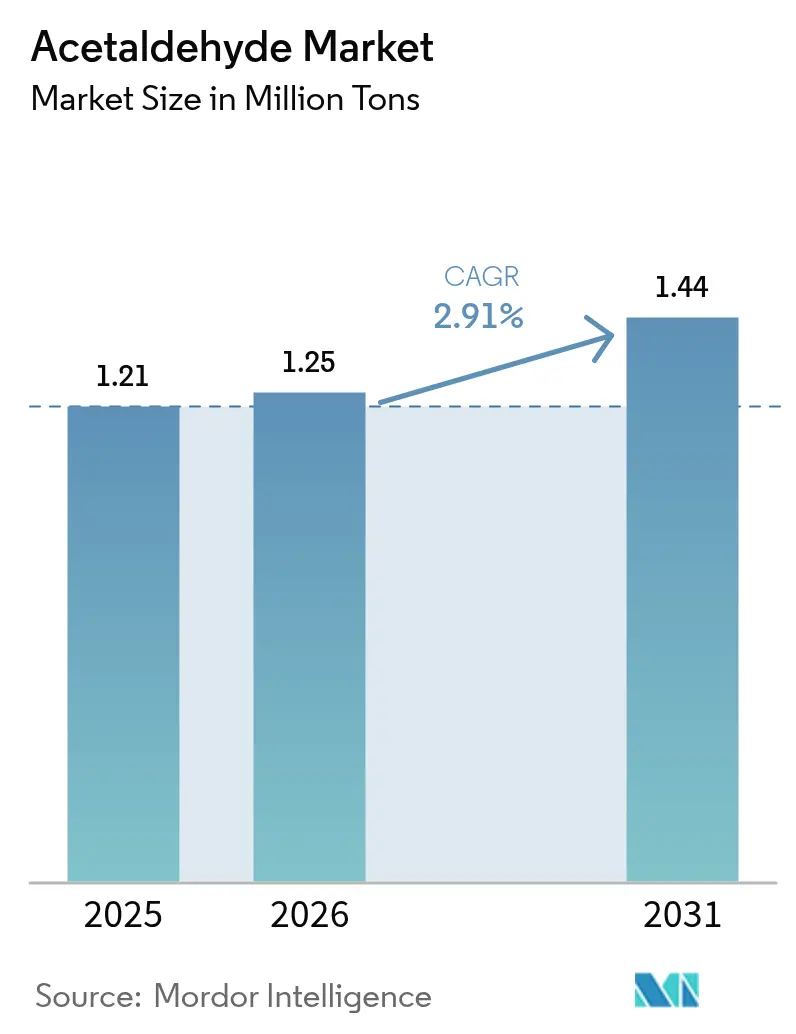

| Market Volume (2026) | 1.25 Million tons |

| Market Volume (2031) | 1.44 Million tons |

| Growth Rate (2026 - 2031) | 2.91% CAGR |

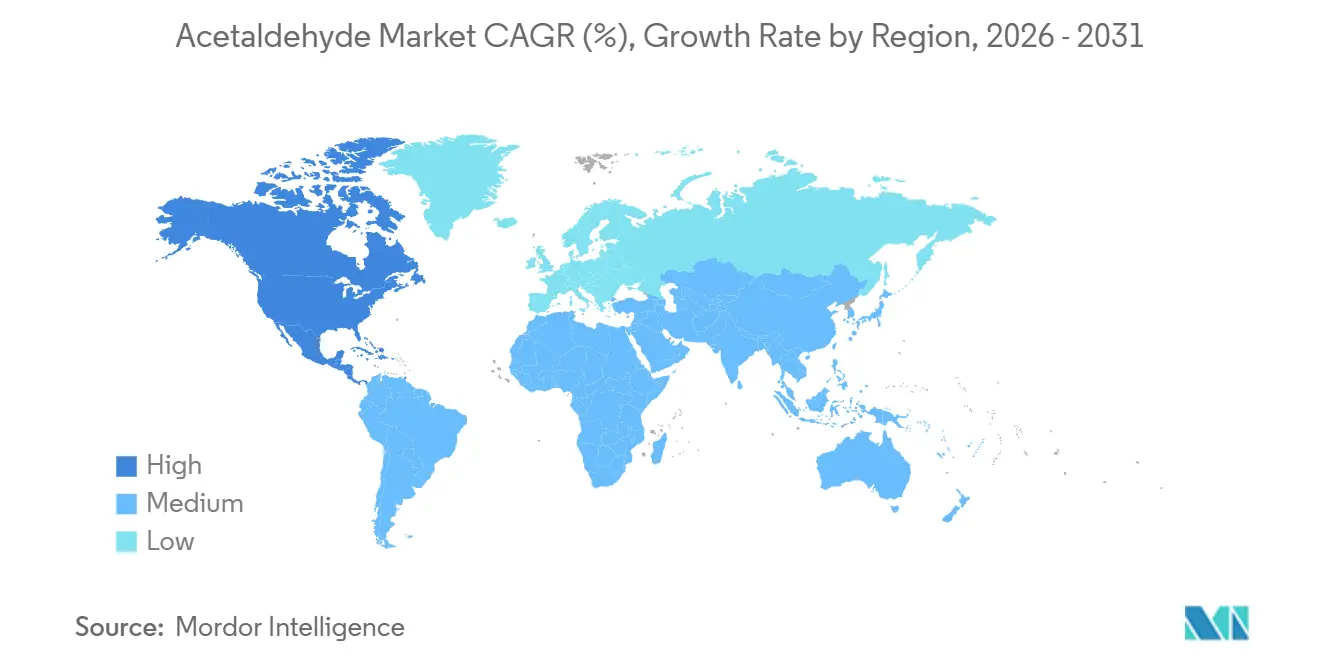

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Acetaldehyde Market Analysis by ���ϲ�����

The Acetaldehyde Market size is projected to expand from 1.21 million tons in 2025 and 1.25 million tons in 2026 to 1.44 million tons by 2031, registering a CAGR of 2.91% between 2026 to 2031. Bio-ethanol routes are scaling as producers seek lifecycle emissions near 0.75 kg CO₂ per kg, far below the 5.7 kg intensity of fossil pathways. Traditional Wacker-process units face margin pressure because ethylene prices swing with crude and gas liquids, while palladium oxide catalysis for direct ethane oxidation offers a future low-capex alternative. Downstream, acetate esters and pentaerythritol gain traction as low-VOC regulations tighten in coatings and adhesives. Regional cost curves are fragmenting: Asia-Pacific keeps scale leadership, yet North America captures fastest growth thanks to abundant ethane and policy incentives such as the Inflation Reduction Act.

Key Report Takeaways

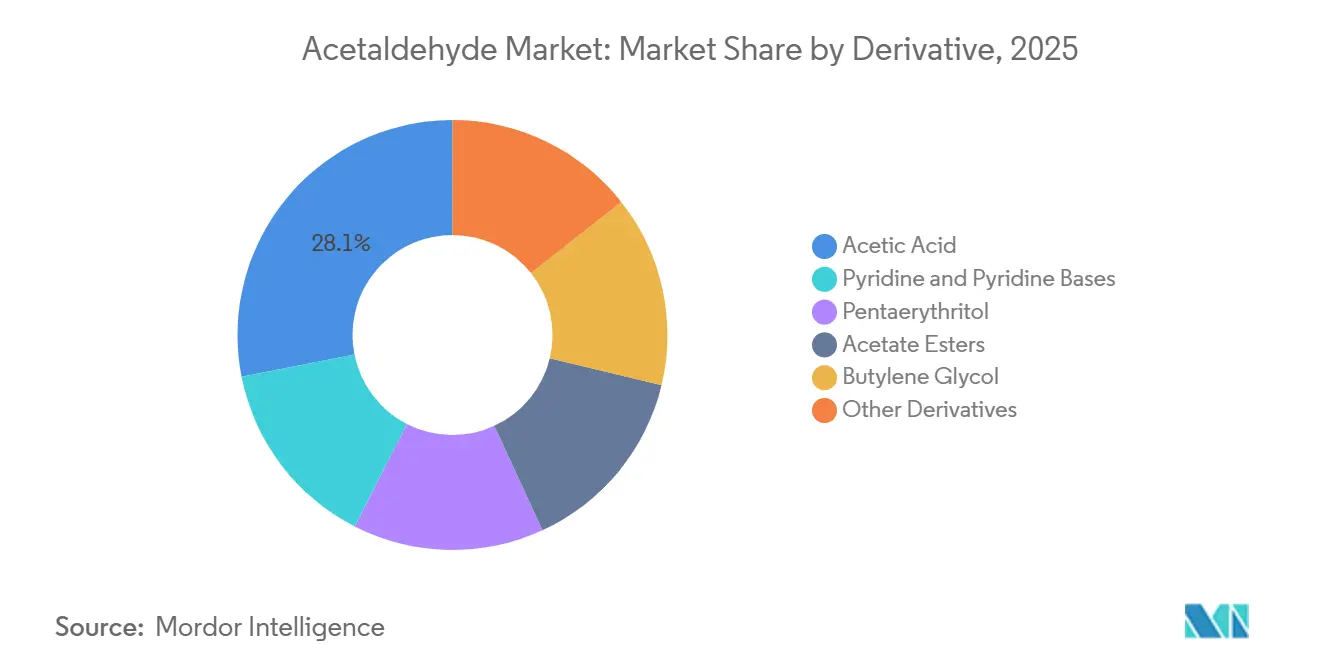

- By derivative, acetic acid led with 28.12% of the acetaldehyde market share in 2025, while pyridine and pyridine bases are projected to expand at a 3.78% CAGR through 2031.

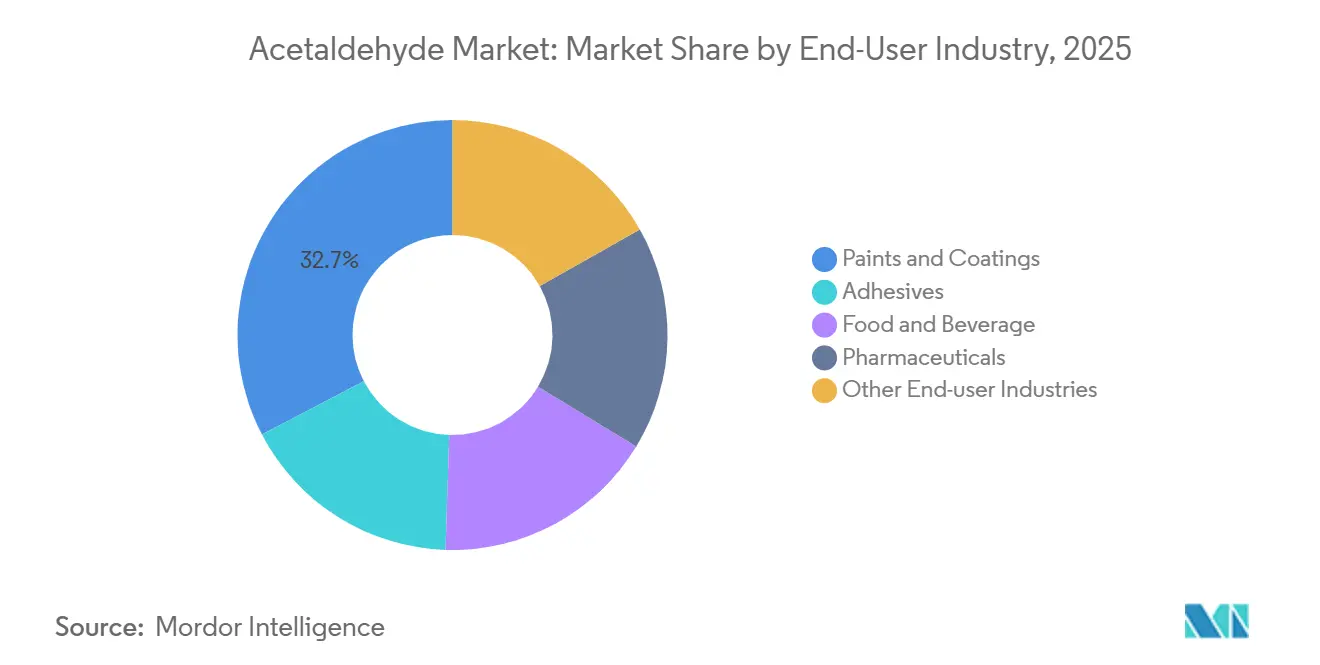

- By end-user industry, paints and coatings held 32.66% share of the acetaldehyde market size in 2025 and are advancing at a 3.22% CAGR through 2031.

- By geography, Asia-Pacific accounted for 57.25% of the 2025 volume, whereas North America is set to grow at a 3.13% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Acetaldehyde Market Trends and Insights

Driver Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding pentaerythritol use in alkyd and UV-curable resins | +0.8% | Global, with concentration in Asia-Pacific and Europe | Medium term (2-4 years) |

| Growing acetate-ester demand in low-VOC solvent blends | +0.7% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Breakthrough ethane-to-acetaldehyde PdO catalysis | +0.5% | North America, Middle East (ethane-rich regions) | Long term (≥ 4 years) |

| Circular PET de-aldehyde upgrades raising bottle-grade quality bar | +0.4% | Global, led by Europe and North America | Medium term (2-4 years) |

| Bio-ethanol derived acetaldehyde for low-carbon supply chains | +0.6% | Europe, North America, Brazil | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Expanding Pentaerythritol Use in Alkyd and UV-Curable Resins

Coatings makers are shifting toward alkyd and UV-curable systems that rely on pentaerythritol produced from acetaldehyde. These resins meet volatile-organic-compound limits below 50 g per liter in the European Union[1]European Commission, “Directive 2010/75/EU on Industrial Emissions,” europa.eu. UV-curable finishes cure without solvent loss, so demand rises in automotive and electronics. Bio-based pentaerythritol can cut lifecycle emissions by up to 30% and earns pricing premiums in sustainability-focused brands[2]Royal Society of Chemistry, “Life-Cycle Metrics of Bio-Pentaerythritol,” rsc.org . Asia-Pacific leads consumption because of ongoing construction activity, while Europe’s REACH rules encourage lower-emission feedstocks. As a result, pentaerythritol growth secures additional pull for the acetaldehyde market.

Growing Acetate-Ester Demand in Low-VOC Solvent Blends

Ethyl, butyl, and propyl acetates come from acetaldehyde via acetic acid and serve as safer solvents in paints, inks, and adhesives. Regulatory frameworks such as the EU Solvent Emissions Directive and California Rule 1113 push formulators to replace aromatics with acetate esters. Flexographic printers are adopting ethyl acetate because it evaporates cleanly and has low toxicity. China keeps adding acetic-acid capacity earmarked for esterification, supporting intra-regional supply. North American demand rebounded in 2025 despite higher ethanol feed costs, showing the resilience of downstream value. Forward-integrated producers capture higher margins than merchants who only sell commodity acetaldehyde.

Breakthrough Ethane-to-Acetaldehyde PdO Catalysis

Laboratory work published in 2024 proved that palladium oxide can convert ethane directly into acetaldehyde with more than 90% selectivity. Omitting the ethylene step promises lower capital spend for new plants, particularly in shale-rich North America and gas-rich Middle East. Commercial scaling usually needs five to seven years, so first deployments will likely be greenfield builds rather than retrofits. Operators with sunk investment in Wacker units may delay adoption to avoid stranded assets. Even so, the technology adds a disruptive option that could reshape cost leadership in the acetaldehyde market.

Circular PET De-Aldehyde Upgrades Raising Bottle-Grade Quality Bar

Recycled PET must have minimal acetaldehyde to suit food-contact bottles. Solid-state polymerization under vacuum volatilizes acetaldehyde, but new scavengers such as anthranilamide chemically bind the molecule, saving energy. Tighter European circular-economy rules that require 30% recycled content by 2030 intensify quality needs. High-purity acetaldehyde, favored for catalyst control, commands price premiums and supports differentiation. Producers segmenting between commodity and specialty grades can capture this emerging value pocket.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Carcinogenic re-classification and tighter workplace exposure limits | -0.6% | Global, with stricter enforcement in North America and Europe | Short term (≤ 2 years) |

| Ethylene price volatility squeezing Wacker-process margins | -0.5% | Europe, Asia-Pacific (naphtha-based regions) | Short term (≤ 2 years) |

| On-site formaldehyde generation replacing acetaldehyde in disinfectants | -0.3% | North America, Europe | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Carcinogenic Re-Classification and Tighter Workplace Exposure Limits

The International Agency for Research on Cancer lists acetaldehyde as Group 2B, prompting regulators to lower exposure limits. ACGIH set a ceiling value of 25 ppm in 2024, and several U.S. states consider stricter thresholds. Formulators in flavors and preservatives are reformulating or substituting to avoid compliance costs. Industrial users invest in closed-loop systems and vapor recovery, increasing fixed costs and pressuring smaller firms.

Ethylene Price Volatility Squeezing Wacker-Process Margins

Wacker oxidation depends on ethylene, whose cost tracks oil and natural-gas liquids. A 2025 academic study placed the levelized ethylene cost near USD 746 per ton under mid-range fuel assumptions. When ethylene spikes, acetaldehyde prices cannot fully adjust because acetic acid prices are capped by cheaper methanol carbonylation. Integrated players with captive ethylene or ethanol are better placed than merchant producers, who may rationalize capacity.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Derivative: Acetic Acid Dominates, Pyridine Bases Accelerate

Acetic acid captured 28.12% of the 2025 volume, confirming its position as the largest single outlet within the acetaldehyde market share. The acetaldehyde market size linked to pyridine and pyridine bases is projected to widen at a 3.78% CAGR through 2031 as agrochemical and pharmaceutical producers scale demand for acetaldehyde-ammonia trimer intermediates.

Pentaerythritol ranks second and mirrors coatings growth, while acetate esters rise on the pull from low-VOC solvents. Butylene glycol stays niche, serving cosmetics where bio-based fermentation routes compete. Peracetic acid grows in food sanitation, benefiting from a favorable regulatory status relative to chlorine.

By End-User Industry: Coatings Lead, Pharmaceuticals Offer Margin

Paints and coatings held 32.66% of 2025 demand and will advance at a 3.22% CAGR during 2026-2031, the quickest among end-uses. This trajectory roots in waterborne and UV-curable systems that contain lower solvent loads, reinforcing structural demand for downstream acetaldehyde derivatives.

Pharmaceutical applications, although smaller, deliver higher margins because they require high-purity input; bio-based acetaldehyde fetches premiums of up to 20% in this segment. Food and beverage uses face uncertainty as safety review bodies reassess acetaldehyde’s GRAS status. Adhesives and rubber additives round out the mix, providing diversification against single-segment shocks.

Geography Analysis

Asia-Pacific accounted for 57.25% of global volume in 2025, anchored by China’s 10.81 million-ton annual acetic-acid capacity. New units scheduled for 2026 indicate continuing scale additions despite thinner margins. India’s acetaldehyde demand is rising due to pharmaceutical and agrochemical investments, and mergers such as Laxmi Organic with Yellowstone Fine Chemicals highlight consolidation aimed at feedstock security.

North America is forecast to register the fastest regional pace at 3.13% CAGR from 2026-2031. Ethane-rich feedstock and policy support, including clean-energy tax credits, underpin several expansion projects. Celanese started a 1.3 million-ton acetic acid addition in March 2024 and positions it as the lowest-carbon unit globally, courtesy of co-located ethylene crackers.

Europe remains challenged by high naphtha-based ethylene costs but pursues competitiveness through renewable routes. Sekab’s wood-cellulose acetaldehyde line, certified in 2024, exemplifies the pivot. South America leverages sugarcane ethanol yet continues to export raw feedstock rather than investing heavily in downstream acetaldehyde capacity. Middle East producers monitor PdO catalysis because abundant ethane could unlock a cost advantage once the technology scales.

Competitive Landscape

The acetaldehyde market is moderately consolidated. Celanese, Eastman Chemical, and Wacker Chemie anchor the leadership tier because they combine upstream feedstock control with downstream derivative integration. Celanese’s Clear Lake complex in Texas, which started a 1.3 million-ton acetic-acid train in March 2024, is tied to an onsite ethylene cracker and gives the company one of the lowest cost positions in the acetaldehyde market. Eastman continues to leverage proprietary oxo-technology that channels internally produced acetaldehyde into acetate esters used in coatings and specialty polymers, thereby lowering exposure to spot-market volatility. Wacker Chemie still licenses the canonical ethylene-oxidation route but is retooling European units with energy-efficiency upgrades to withstand high naphtha-based feedstock costs.

Acetaldehyde Industry Leaders

Celanese Corporation

Eastman Chemical Company

Sumitomo Chemical Co., Ltd.

Jubilant Ingrevia Limited

Wacker Chemie AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Laxmi Organic raised domestic acetaldehyde prices in India, citing higher ethanol and ethylene costs alongside firm coatings demand.

- December 2024: : Sekab obtained ISCC PLUS certification for wood-cellulose–based acetaldehyde, validating a lifecycle emission footprint of 0.75 kg CO₂ per kg.

Global Acetaldehyde Market Report Scope

Acetaldehyde, a colorless liquid, is primarily used as a precursor for derivatives and other chemical compounds. Naturally present in coffee, bread, ripe fruits, and some plants, it is a critical raw material in the production of pyridine, pentaerythritol, acetic acid, peracetic acid, and ethyl acetate.

The acetaldehyde market is segmented by derivatives, end-user industry, and geography. By derivatives, the market is segmented into pyridine and pyridine bases, pentaerythritol, acetic acid, acetate esters, butylene glycol, and other derivatives. By end-user industry, the market is segmented into adhesives, food and beverage, paints and coatings, pharmaceuticals, and other end-user industries. The report also covers the market size and forecasts for the acetaldehyde market in 18 countries across major regions. For each segment, the market sizing and forecasts have been done based on volume (tons).

| Pyridine and Pyridine Bases |

| Pentaerythritol |

| Acetic Acid |

| Acetate Esters |

| Butylene Glycol |

| Other Derivatives (Chloral, Peracetic Acid, etc.) |

| Adhesives |

| Food and Beverage |

| Paints and Coatings |

| Pharmaceuticals |

| Other End-user Industries (Water Treatment, Plastics, Rubber, Fuel Additives, etc.) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC | |

| Turkey | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Derivative | Pyridine and Pyridine Bases | |

| Pentaerythritol | ||

| Acetic Acid | ||

| Acetate Esters | ||

| Butylene Glycol | ||

| Other Derivatives (Chloral, Peracetic Acid, etc.) | ||

| By End-User Industry | Adhesives | |

| Food and Beverage | ||

| Paints and Coatings | ||

| Pharmaceuticals | ||

| Other End-user Industries (Water Treatment, Plastics, Rubber, Fuel Additives, etc.) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC | ||

| Turkey | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current market size for acetaldehyde?

The acetaldehyde market is estimated to grow from 1.21 million tons in 2025 to 1.25 million tons in 2026.

What growth rate is expected for the acetaldehyde market through 2031?

Volume is projected to rise at a 2.91% CAGR between 2026-2031 as bio-routes offset slower fossil growth.

Which derivative will expand fastest over the next five years?

Pyridine and pyridine bases are forecast to post the highest CAGR at 3.78% because of agrochemical and pharmaceutical demand.

Why is North America the quickest-growing region?

Abundant shale-based ethane, clean-energy tax credits, and reshoring of chemical chains lift regional CAGR to 3.13%.

How are new technologies reshaping supply economics?

Palladium-oxide catalysis that converts ethane directly into acetaldehyde could cut capital costs for greenfield plants in gas-rich regions.

What regulatory headwinds affect acetaldehyde use?

Group 2B carcinogen status and lower occupational exposure limits are pushing formulators to re-engineer or substitute in consumer-facing products.

Where does bio-based acetaldehyde create the most value?

Low-carbon supply chains for high-purity pharmaceuticals, coatings, and recycled-PET scavengers command 15-20% price premiums.

Page last updated on: